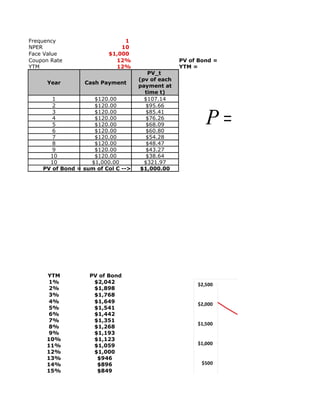

5. Face Value $1,000

Coupon Rate 10%

YTM 10%

PV_t Year*Weight in

(pv of each Share of Col D

payment at time total PV = (weighted Avg

Year Cash Payment t) PV_t/Price B of each Year)

1 $100.00 $90.91 9.09% 0.09

2 $100.00 $82.64 8.26% 0.17

3 $100.00 $75.13 7.51% 0.23

4 $100.00 $68.30 6.83% 0.27

5 $100.00 $62.09 6.21% 0.31

6 $100.00 $56.45 5.64% 0.34

7 $100.00 $51.32 5.13% 0.36

8 $100.00 $46.65 4.67% 0.37

9 $100.00 $42.41 4.24% 0.38

10 $100.00 $38.55 3.86% 0.39

10 $1,000.00 $385.54 38.55% 3.86

PV of Bond = sum of Col C --> $1,000.00 6.76

Interest Rate Risk

%∆P = - DUR x ∆i/(1+i)

Duration 6.76

Original Price 1000.00

New YTM 11.00%

Old YTM 10.00%

∆i/(1+i) 0.91% <-- (B18 - B19)/(1+B19)

%∆P = -6.14% <-- -DUR*B27

New P = $938.55

6. DURATION(settlement,maturity,coupon,yld,frequency,bas

settlement 2-Jan-09

M

Ct Maturity 2-Jan-19

∑t ×

t =1 (1 + r ) t

coupon

Yield

10%

10%

D= freq 1

P basis 3

DURATION(settlement,maturity,coupon,yld,

6.76

Day count

Basis

<-- Sum of Col E = Duration basis

0 or omitted US (NASD)

30/360

1 Actual/actual

2 Actual/360

3 Actual/365

∆ r 4 European

−D

30/360

P

1 +r

7. ,coupon,yld,frequency,basis)

Settlement is the security's settlement date. The security settlement date is the date after the i

Maturity is the security's maturity date. The maturity date is the date when the security expires

Coupon is the security's annual coupon rate.

Yld is the security's annual yield.

Frequency is the number of coupon payments per year. For annual payments, frequency = 1; fo

Basis is the type of day count basis to use.

ment,maturity,coupon,yld,frequency,basis)

which is what we found above

8. ate is the date after the issue date when the security is traded to the buyer.

when the security expires.

yments, frequency = 1; for semiannual, frequency = 2; for quarterly, frequency = 4.