Recommended

More Related Content

What's hot

What's hot (20)

Viewers also liked

Viewers also liked (20)

Similar to 3rd Quarter 2015

Similar to 3rd Quarter 2015 (20)

Recently uploaded

Recently uploaded (20)

3rd Quarter 2015

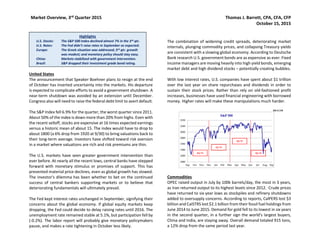

- 1. Market Overview, 3rd Quarter 2015 Thomas J. Barrett, CPA, CFA, CFP October 15, 2015 United States The announcement that Speaker Boehner plans to resign at the end of October has inserted uncertainty into the markets. His departure is expected to complicate efforts to avoid a government shutdown. A near-term shutdown was avoided by an extension until December. Congress also will need to raise the federal debt limit to avert default. The S&P Index fell 6.9% for the quarter, the worst quarter since 2011. About 50% of the index is down more than 20% from highs. Even with the recent selloff, stocks are expensive at 16 times expected earnings versus a historic mean of about 15. The index would have to drop to about 1800 (a 6% drop from 1920 at 9/30) to bring valuations back to their long-term average. Investors have shifted toward risk aversion in a market where valuations are rich and risk premiums are thin. The U.S. markets have seen greater government intervention than ever before. At nearly all the recent lows, central banks have stepped forward with monetary stimulus or promises of support. This has prevented material price declines, even as global growth has slowed. The investor's dilemma has been whether to bet on the continued success of central bankers supporting markets or to believe that deteriorating fundamentals will ultimately prevail. The Fed kept interest rates unchanged in September, signifying their concerns about the global economy. If global equity markets keep dropping, the Fed could decide to delay raising rates until 2016. The unemployment rate remained stable at 5.1%, but participation fell by (-0.2%). The labor report will probably give monetary policymakers pause, and makes a rate tightening in October less likely. The combination of widening credit spreads, deteriorating market internals, plunging commodity prices, and collapsing Treasury yields are consistent with a slowing global economy. According to Deutsche Bank research U.S. government bonds are as expensive as ever. Fixed income managers are moving heavily into high yield bonds, emerging market debt and high dividend stocks – potentially creating bubbles. With low interest rates, U.S. companies have spent about $1 trillion over the last year on share repurchases and dividends in order to sustain their stock prices. Rather than rely on old-fashioned profit increases, businesses have used financial engineering with borrowed money. Higher rates will make these manipulations much harder. Commodities OPEC raised output in July by 100k barrels/day, the most in 3 years, as Iran returned output to its highest levels since 2012. Crude prices have returned to six year lows as stockpiles and refinery shutdowns added to oversupply concerns. According to reports, CalPERS lost $3 billion and CalSTRS lost $2.1 billion from their fossil fuel holdings from June 2014 to June 2015. Demand for gold fell to its lowest in six years in the second quarter, in a further sign the world's largest buyers, China and India, are staying away. Overall demand totaled 915 tons, a 12% drop from the same period last year. HighlightsHighlights U.S. Stocks: The S&P 500 Index declined almost 7% in the 3rd qtr. U.S. Rates: The Fed didn’t raise rates in September as expected. Europe: The Greek situation was addressed; 3rd qtr. growth was modest; and monetary policy should stay easy. China: Markets stabilized with government intervention. Brazil: S&P dropped their investment grade bond rating.

- 2. Market Overview, 3rd Quarter 2015 Thomas J. Barrett, CPA, CFA, CFP October 15, 2015 Europe The IMF warned that world GDP growth expectations of 3.3% this year are not realistic. With mixed economic data and relatively large exposure to international developments, the ECB is expected to keep easy monetary policies in place past their September 2016 deadline. Eurozone business activity recovered and accelerated in August as the PMI was 54.3, its highest level since May 2011. While the survey provided some good news, it still points to very moderate 3rd quarter GDP growth. Eurozone unemployment held steady at 11% in August versus forecasts of 10.9%. A global push in mergers and acquisitions, which reached a $1 trillion for the quarter, has not diminished, despite concerns about slower economic growth in China. "The trends that have been driving M&A - global scale, synergies, low financing costs, strong balance sheets - continue to be there, and should drive more activity," said Barclays. Greece The Eurozone and Greece agreed in principle to a 3rd bailout that will keep the troubled country in the currency zone, for now, after almost total capitulation from Prime Minister Alexis Tsipras. Subsequently, Tsipras won overwhelming support in Parliament for the more stringent reforms demanded by international creditors. Greece will control cash transactions of banks while the government awaits aid. Japan & Korea Trade negotiators among 12 countries including the US and Japan reached an agreement on the broad-based Trans-Pacific Partnership (TPP). It is the largest regional trade accord in history, a potentially precedent-setting model for global commerce and worker standards that would tie together 40% of the world’s economy, from Canada and Chile to Japan and Australia. Japan's economy contracted at an annualized rate of -1.2% in the 2nd quarter versus an initial estimate of -1.6%. While it is too early to say that “Abenomics” is working, there are signs that progress is being made to end deflation and improve Japan’s growth potential. Japan did drop back into deflation for the first time since April 2013, with core inflation down 0.1% compared with a year ago. But the decline was largely due to slumping global energy prices. South Korean exports worsened by the most in six years in August, reinforcing expectations its central bank will cut rates to tackle a darkening outlook. Exports fell 14.7% from the year before, dragged down by a slowdown in exports to China, Europe and Japan.

- 3. Market Overview, 3rd Quarter 2015 Thomas J. Barrett, CPA, CFA, CFP October 15, 2015 China For all of its flaws, many outside of China had viewed its leaders as economically adroit, capable of creating rapid growth and keeping down risks - now they are not so sure. The financial sector has not allocated capital efficiently. There have been huge over-investments in fixed assets, from airports to housing. The country has a lot of debt, which must be worked down. China’s stock market experienced huge sell-offs in July, but finally subsided when a barrage of measures, to boost liquidity and calm investors, were instituted. The government is attempting to stabilize the stock market bubble while 3 other bubbles have yet to deflate: real estate, local government debt, and manufacturing overcapacity. The central Chinese government gave approval for local government- run pensions to invest in the equity markets. State media estimates $97B will be eligible to be invested under the new rules. Goldman Sachs decreased its forecast for Chinese growth over the next three years to 6.4% (2016), 6.1% (2017) and 5.8% (2018). Many well-known investment managers have commented on the Chinese markets recently. Bridgewater, the world's biggest hedge fund, told investors that the country's recent stock market rout will likely have broad, negative repercussions. "If you look at the Chinese financial system, shadow banking, and leverage levels - it looks worse to me than 2007 in the U.S," Pershing Square's Bill Ackman said. Managers Paul Singer and Jeff Gundlach called the Chinese situation "way bigger than subprime" and "far too volatile to invest in." China's electricity usage was up 3.6% over the last year. Unless the country is rapidly becoming more energy efficient, it appears actual growth is significantly lower than what is being reported. China has represented a good portion of the marginal commodity demand for over a decade. The China slowdown is the main reason commodities like copper, iron and coal are at multi-year lows. Emerging Markets Looking out to 2016, a great risk to U.S. stocks remains an emerging market induced global recession. Emerging markets account for a growing percentage of global growth, and the recent slowdown in the emerging world isn't limited to China. Economies in Brazil and Russia are contracting, and most large emerging markets, with the exception of India, are slowing. Emerging markets are on track to suffer their first annual net outflow since 1988. Amid the gloom in emerging markets, one economy stands out. India data for August showed its GDP rose by 7% in Q2, year-on-year. India has not been hurt by the China slowdown since it exports little there. The Reserve Bank of India is poised to cut rates before year end, since inflation has come in well below the bank's 6% target. S&P stripped Brazil of its investment-grade credit rating, held since 2008. The country was downgraded from BBB- to BB+, S&P's highest high-yield rating. S&P cited political turmoil that is interfering with the government's implementation of necessary economic policies. Brazil's currency hit its lowest level against the dollar in two decades.