1. THE NET LEASE MARKET REPORT

Q4 2013

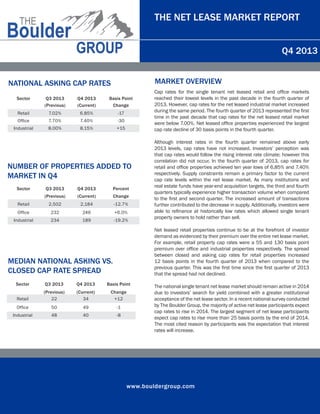

NATIONAL ASKING CAP RATES

MARKET OVERVIEW

Cap rates for the single tenant net leased retail and office markets

reached their lowest levels in the past decade in the fourth quarter of

2013. However, cap rates for the net leased industrial market increased

during the same period. The fourth quarter of 2013 represented the first

time in the past decade that cap rates for the net leased retail market

were below 7.00%. Net leased office properties experienced the largest

cap rate decline of 30 basis points in the fourth quarter.

Sector

Q3 2013

(Previous)

Q4 2013

(Current)

Basis Point

Change

Retail

7.02%

6.85%

-17

Office

7.70%

7.40%

-30

Industrial

8.00%

8.15%

+15

NUMBER OF PROPERTIES ADDED TO

MARKET IN Q4

Sector

Q3 2013

Q4 2013

Percent

(Previous)

(Current)

Change

Retail

2,502

2,184

-12.7%

Office

232

246

+6.0%

Industrial

234

189

-19.2%

Net leased retail properties continue to be at the forefront of investor

demand as evidenced by their premium over the entire net lease market.

For example, retail property cap rates were a 55 and 130 basis point

premium over office and industrial properties respectively. The spread

between closed and asking cap rates for retail properties increased

12 basis points in the fourth quarter of 2013 when compared to the

previous quarter. This was the first time since the first quarter of 2013

that the spread had not declined.

MEDIAN NATIONAL ASKING VS.

CLOSED CAP RATE SPREAD

Although interest rates in the fourth quarter remained above early

2013 levels, cap rates have not increased. Investors’ perception was

that cap rates would follow the rising interest rate climate; however this

correlation did not occur. In the fourth quarter of 2013, cap rates for

retail and office properties achieved ten year lows of 6.85% and 7.40%

respectively. Supply constraints remain a primary factor to the current

cap rate levels within the net lease market. As many institutions and

real estate funds have year-end acquisition targets, the third and fourth

quarters typically experience higher transaction volume when compared

to the first and second quarter. The increased amount of transactions

further contributed to the decrease in supply. Additionally, investors were

able to refinance at historically low rates which allowed single tenant

property owners to hold rather than sell.

Sector

Q3 2013

Q4 2013

Basis Point

Retail

(Previous)

22

(Current)

34

Change

+12

Office

50

49

-1

Industrial

48

40

-8

The national single tenant net lease market should remain active in 2014

due to investors’ search for yield combined with a greater institutional

acceptance of the net lease sector. In a recent national survey conducted

by The Boulder Group, the majority of active net lease participants expect

cap rates to rise in 2014. The largest segment of net lease participants

expect cap rates to rise more than 25 basis points by the end of 2014.

The most cited reason by participants was the expectation that interest

rates will increase.

www.bouldergroup.com

2. THE NET LEASE MARKET REPORT

Q4 2013

SELECTED SINGLE TENANT SALES COMPARABLES

Sale

Date

Sector

Price

Per SF

Cap

Rate

Oct-13

Retail

LA Fitness

Houston

TX

$12,000,000

$267

7.50%

15

Oct-13

Retail

Dick’s Sporting Goods

Durham

NC

$11,800,000

$204

7.50%

9

Oct-13

Retail

Trader Joe’s

Evanston

IL

$11,000,000

$733

5.08%

15

Dec-13

Retail

Kohl’s

Avondale

AZ

$10,600,000

$120

6.55%

10

Nov-13

Retail

Walgreens

Greenwood

IN

$9,200,000

$695

5.92%

25

Nov-13

Retail

Besy Buy

Mishawaka

IN

$7,000,000

$140

10.83%

10

Oct-13

Retail

Bank of America

Chicago

IL

$6,940,000

$733

5.62%

12

Oct-13

Retail

Walgreens

Memphis

TN

$6,410,000

$440

5.90%

22

Oct-13

Office

GSA - DEA

Tallahassee

FL

$6,150,000

$322

7.64%

6

Dec-13

Retail

Aldi

Addison

IL

$5,475,000

$198

5.81%

15

Oct-13

Retail

CVS

Opelika

AL

$5,250,000

$482

6.66%

19

Tenant

City

State

Price

Lease Term

Remaining

NET LEASED CAP RATE TRENDS

8.75%

8.25%

7.75%

7.25%

6.75%

Q2

Q3

Q4

Q1

Q2

2006 2006 2006 2007 2007

Q3

2007

Q4

2007

Q1

2008

Q2

2008

Q3

2008

Q4

2008

Q1

2009

Q2

2009

Q3

2009

Q4

2009

Q1

2010

Q3

Q2

Q3

Q4 Q1 Q2 Q3

Q4

Q1

Q2

2010 2010 2010 2011 2011 2011 2011 2012 2012 2012

Retail

www.bouldergroup.com

Q4

2012

Q1

2013

Office

Q2

Q3

Q4

2013 2013 2013

Industrial