Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

En vedette (20)

Similaire à 2.0 declared services sec 66_e

Similaire à 2.0 declared services sec 66_e (20)

Dernier

Dernier (20)

2.0 declared services sec 66_e

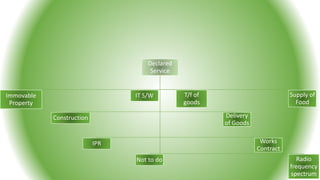

- 1. Declared Service Immovable Property IPR Construction IT S/W Not to do T/f of goods Delivery of Goods Supply of Food Works Contract Radio frequency spectrum

- 2. Vacant Land for agricultural purpose Residential dwelling for residential purpose By RBI By Govt./LA to Non-Business Entity Precincts of Specified Religious Places for General Public Hotel/Inn/Club/Guest house/others commercial places for lodging/residence purpose + Declared tariff <1000/day or equivalent Proportionate part of Property Tax can claimed as exemption from gross Rental Income from such property If failed to claim, then claim within 1yr from the date of payment of tax + intimate to superintendent of CE within 15days of such adjustment. Hotel/Inn/Club/Guest house/others commercial places for lodging/residence purpose + Declared tariff ≥1000/day or equivalent Then 40% of value of taxable service is Exempt But CENVAT Credit = Only Input Service 1. Renting of Immovable Property MEN :Negative List : Abatement :

- 3. 2. Temporary t/f for use of IPR MEN: Section 13 of Copy Right Act Remarks (a) Original Literacy, dramatic, Musical & Artistic Works MEN (b) Cinematograph Films MEN (c) Sound Recording Pay ST Must Exhibit in cinema hall/theatre Intellectual Property Right includes Copyright Patents Trademarks Designs Similar right in Intangible Property If Permanent T/f ,it amounts to sales and NO ST POT is as per Rule 8 of POT rules, 2011 See MEN: Exhibition of movie in next Slide

- 4. Film distribution & exhibition Operating on Principle to Principle Basis (No JV/PF) Exhibited on his own by Exhibitor Amounts to Temporary t/f of copyright. Hence Exempt from ST (MEN). Exhibited on behalf of distributor by Exhibitor Amounts to Renting of immovable property service and is liable to ST Under Unincorporated PF or Collaboration (JV/PF) Service provided by each (JV/PF, distributor, exhibitor) is liable to ST @ applicable head of service. But if exhibitor exhibits movies as its member to AOP or to distributor is Exempt from ST (MEN).

- 5. 3. EXECUTION OF WORK CONTRACT Ref: Work Contract PPT

- 6. 4. CONSTRUCTION WORK Ref: Construction work PPT

- 7. 5. Service Portion as a part of activity where goods (Food, drinks etc. for human consumption) is supplied Restaurant Services Outdoor Catering Service Without A/C or central heating system in any part of Est. at any point of time during the year With A/C or central heating system in canteen of a Factory Catering including Mid day meals scheme to Educational Inst. Sponsored by Govt. Ref. Deemed sale {article 366(29A)} MEN: MEN: In case of AC + Non AC in same complex + Common kitchen, then Non-AC is Exempt only when it is clearly demarcated + separately named. RULE 2C of Valuation Rules A Gross Amount Charged XXX + FMV of Goods Supplied (as per GAAP) X - Amount Charged for goods supplied to SP (X) - VAT/ others levied, if any (X) - Goods sold @ MRP as part of bill/invoice (X) B Total Amount Charged XX S. No Service % on Tot amt. Chg. 1 Restaurant Service 40% 2 Outdoor Catering 60% 3 Supply of food + Renting of Premises 70%

- 8. It is a representation of instructions, data, sound/image, includes Source code + Object code , Recorded in Machine readable form , Capable to interact with user by means of computer or other automatic processing machines Development, Design, Programming, Customization, Adaptation, Upgradation, enhancement, implementation of IT Software Service Pre-packed or Canned Software is not liable to ST IT software on with Excise duty is levied are exempted Software given on hire is liable to ST License to use prepacked software is liable to ST Onsite development of software is liable to ST Customized development of software is liable to ST Advice/assistance/consultancy on matters relating to IT is liable to ST 6. Information Technology software Service

- 9. 7. Delivery of Goods by Hire-Purchase or any system of payment by instalment Delivery is not covered as it is deemed sales {Article 366(29A)}. Only activity related to such delivery is covered here Must have option to purchase the Goods on payment of Last Instalment (as per terms of agreement) Generally operating lease do not fall here, but if we point out ant t/f of right to use the goods then it amounts to deemed sale Finance Lease & Capital Lease amounts to deemed sales. Must be nature of financing and Lessee pays maintenance + tax & has option to purchase the goods Abatement of 90% is available. i.e. 90% interest is exempt

- 10. Goods available for delivery Consensus ad idem as to identity of goods T/f of possession & effective control Transferee has legal right to use such goods Right transferred to one cannot be again transferred to another person by the owner during that period Hiring Car with driver (Chgs. are monthly/mileage) Supply trucks etc. to project and is returned after specified time Pandal/Shamiana Contract Bank Lockers hiring Hiring of Motor Vehicle Motor Vehicle >12 Passengers TO State Trans. Corp. A means of Transp. Of Goods TO GTA Renting of Motor Cab {Abatement = 60%} Only below mentioned input service is eligible for credit 1 Refer: Rule-9 POPS of POPS Rules, 2012 PRCM of Renting of motor vehicle 8. T/f of goods by Hiring, Leasing, any manner without T/f of right to use such Goods Input SP paid CENVAT Credit available On Full Value 40% of CENVAT Credit On 40% Value Full CENVAT Credit For the purpose of abatement consideration should include FMV (as per GAAP) cost goods (Fuel also) and service supplied by recipient of service MEN:

- 11. To refrain/tolerate/do an act • Examples : • Demurrage Charges • Advance forfeited on cancellation of Agreement • Late delivery Charges • Non-Compete Fee • Forfeiture of security charges (not due to unforeseen actions or accidental damages • MEN : • Fines or Liquidated damages paid to Govt./local authority for tolerating non-performance of contract. Assignment by Govt. of right to use radio-frequency spectrum and its subsequent transfer { w.e.f FY 2016-17 } • Up FY 2015-16 it is covered under MEN