The Unbanked

•

1 j'aime•226 vues

Tanmia Capital has launched its Economic Papers series to address key topics in simple and informative manner The series will be issued in alternate Arabic and English regularly. Today's topic highlights financial inclusion and provides recent data from selected countries. (in English)

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à The Unbanked

Similaire à The Unbanked (20)

Dernier

Dernier (20)

The Unbanked

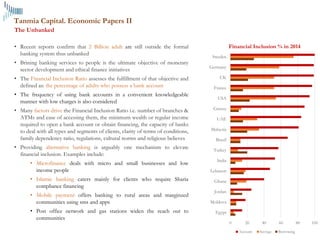

- 1. The Unbanked Tanmia Capital. Economic Papers II 0 20 40 60 80 100 Egypt Moldova Jordan Ghana Lebanon India Turkey Brazil Malaysia UAE Greece USA France UK Germany Sweden Financial Inclusion % in 2014 Account Savings Borrowing • Recent reports confirm that 2 Billion adult are still outside the formal banking system thus unbanked • Brining banking services to people is the ultimate objective of monetary sector development and ethical finance initiatives • The Financial Inclusion Ratio assesses the fulfillment of that objective and defined as: the percentage of adults who possess a bank account • The frequency of using bank accounts in a convenient knowledgeable manner with low charges is also considered • Many factors drive the Financial Inclusion Ratio i.e. number of branches & ATMs and ease of accessing them, the minimum wealth or regular income required to open a bank account or obtain financing, the capacity of banks to deal with all types and segments of clients, clarity of terms of conditions, family dependency ratio, regulations, cultural norms and religious believes • Providing alternative banking is arguably one mechanism to elevate financial inclusion. Examples include: • Microfinance deals with micro and small businesses and low income people • Islamic banking caters mainly for clients who require Sharia compliance financing • Mobile payment offers banking to rural areas and marginzed communities using sms and apps • Post office network and gas stations widen the reach out to communities

- 2. The Unbanked Tanmia Capital. Economic Papers II 0 20 40 60 80 100 Egypt Moldova Jordan Angola Ghana Lebanon India Kazakhstan Turkey Brazil Malaysia UAE Greece USA France UK Germany Sweden Financial Inclusion % in 2014• Recent reports confirm that 2 Billion adult are still outside the formal banking system thus unbanked • Brining banking services to people is the ultimate objective of monetary sector development and ethical finance initiatives • The Financial Inclusion Ratio assesses the fulfillment of that objective and defined as: the percentage of adults who possess a bank account • The frequency of using bank accounts in a convenient knowledgeable manner with low charges is also considered • Many factors drive the Financial Inclusion Ratio i.e. number of branches & ATMs and ease of accessing them, the minimum wealth or regular income required to open bank account or obtain financing, the capacity of banks to deal with all types and segments of clients, clarity of terms of conditions, family dependency ratio, regulations, cultural norms and religious believes • Providing alternative banking is arguably one mechanism to elevate financial inclusion. Examples include: • Microfinance deals with micro and small businesses and low income people • Islamic banking caters mainly for clients who require Sharia compliance financing • Mobile payment offers banking to rural areas and marginzed communities using sms and apps • Post office network and gas stations widen the reach out to communities