1. Industrial Analysis February2011

Michael Porter's Five Forces Model Residential Development Business in China

By Robert Fong

June 2011

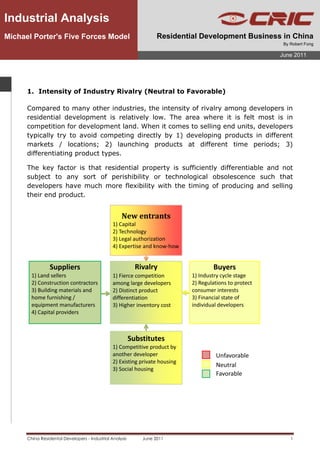

1. Intensity of Industry Rivalry (Neutral to Favorable)

Compared to many other industries, the intensity of rivalry among developers in

residential development is relatively low. The area where it is felt most is in

competition for development land. When it comes to selling end units, developers

typically try to avoid competing directly by 1) developing products in different

markets / locations; 2) launching products at different time periods; 3)

differentiating product types.

The key factor is that residential property is sufficiently differentiable and not

subject to any sort of perishibility or technological obsolescence such that

developers have much more flexibility with the timing of producing and selling

their end product.

China Residental Developers - Industrial Analysis June 2011 1

2. 2. Threat of new entrants (Neutral to Unfavorable)

When an industry has over 60,000 registered participants, it is hard to conclude

that barriers to entry are high. Although the number of entrants varies over time

and according to market condition, they are sufficiently low relative to other

industries that new entrants can continue to enter and eventually push above

average returns back to historical means.

Generally speaking, the potential barriers to entry to any industry fall into

several broad categories: 1) capital; 2) technology; 3) legal authorization; and 4)

expertise and know-how.

Legal authorization is necessary for certain types of industries such as telecoms

and utilities. The number of participants in these industries is limited due to the

nature of the businesses (“natural monopolies”) or the return profiles (massive

upfront investments which can only be recovered through limited operating

competition).

For most real estate development, no special legal authority is needed to enter

the industry. That is why many non-property companies find it relatively easy to

migrate into this industry as and when returns become attractive or simply out of

interest.

Furthermore, the technological and expertise/know-how component of this

industry is not particularly high. Designs, names and concepts can all be copied

as there is less ability to protect these through patents or copyright. Large value

supply chains such as agents, consultants, property managers and employees of

rivals can all be hired or co-opted.

Capital can be considered a barrier but mostly to larger scale projects. The gross

amount of capital needed to “enter” the industry is paltry compared to the likes

of steel mills or chip fabs.

In addition to the above factors, the wide range of different types and scales of

development each entail different barriers to entry. Obviously larger, more

specialized developments in top tier cities (i.e., a massive mixed use residential,

commercial development in Beijing) would have much higher barriers to entry

than a small residential project in Taiyuan.

China Residental Developers - Industrial Analysis June 2011 2

3. 3. Threat of substitutes (Favorable for End Use; Neutral for

Investment)

Real estate development involves different types of products – residential, office,

retail and industrial being the most common. To narrow the scope of discussion,

we will just consider private residential real estate.

Currently in China, residential real estate is in high demand both for its utilitarian

value as accommodation and also for its investment value as a stable, inflation-

proof store of wealth. As such we need to consider the substitutability on both

fronts.

As accommodation, new private housing from any firm can be replaced by 1)

competitive product from another developer; 2) existing private housing for sale

or for rent; 3) social housing either for sale or rent. Any specific developer can

lower the risk of substitution by differentiating their product offering by i)

location; ii) type and iii) quality. The more generic a developer’s product,the

more substitutable . Developers that have managed to distinguish their product

or image will fare the best.

The threat from the secondary market varies by city. In T1 and large T2 cities, a

sufficiently large stock of housing exists for the secondary market to be a viable

choice for potential homebuyers. In many T3 and T4 cities, there are either not

enough secondary units for sale or the market is simply is too illiquid.

The threat from social housing exists but not significant. Usually, those allowed

to buy or rent social housing would only be able to enter the low end of the

private housing market anyway – if at all. Moreover, resale and other restrictions

make it a far less liquid asset class. For that reason, the threat is only to the

lower end of the private housing market.

Given China’s current state of negative real interest rates and capital controls,

most individuals have limited channels for savings and investment. Real estate

has helped fill this void. If investors were given more alternatives and if other

asset classes such as equities start to perform better, investment demand for

real estate would quite likely cool.

China Residental Developers - Industrial Analysis June 2011 3

4. 4. Bargaining power of suppliers (Favorable)

Overall, developers are in a favorable bargaining position relative to the key

suppliers in the industry. The 3 key suppliers to any residential developer are 1)

land sellers (usually cities or other developers); 2) construction contractors; 3)

building materials and home furnishing / equipment manufacturers; 4) capital

providers. This situation is more or less reflected in that the typical cost of sales

for any developer is made up of roughly 1/3 land, 1/3 construction and 1/3

financing costs.

A typical developer’s bargaining position relative to a land seller varies according

to 1) nature of sale and 2) location of sale. Developers typically prefer to buy

land through direct bilateral negotiations with the government or 3rd party

rather than be involved in a multi-party bidding ware. Auctions are the least

desired channel for land acquisition but sometimes a necessity. For land bought

in smaller cities or newer areas of larger cities, developers wield a lot more

bargaining power. Smaller cities are generally eager to entice well known

national developers. For example, if Vanke or COLI buys into a smaller T3/4 city,

it would signal to other developers that this city is worthy of investment. In such

cases, local officials are willing to give a discount to entire desired players. This

logic is also true of newly emerging districts in T1/2 cities.

Construction companies do not command much if any pricing power and many

work on thin margins. Although developers can backward integrate and take on

construction duties themselves, this is often more for ensuring timeliness of

completion or maintaining quality standards than for cost savings. Also, the

construction materials and household furnishings that developers buy are mostly

commodity goods for which the manufacturers not only command no particular

pricing power but would also yield a discount on bulk or volume purchases.

Lastly, capital providers, be they banks, shareholders or bondholders, may have

different investment appetite for this industry at different times but whether

investors or bankers demand a specific risk premium to provide capital is more

dependent on the perceived risks at any point in the property cycle and not any

kind of structural risk premium.

China Residental Developers - Industrial Analysis June 2011 4

5. 5. Bargaining Power of Buyers (Neutral)

Of all the five forces, this is perhaps the most dependent on 1) the stage in the

industry cycle; 2) regulations to protect consumer interests and 3) financial state

of individual developers. Given this wide variance, it is very difficult to conclude

definitively that buyer power is always strong or always weak. The truth is buyer

power will fluctuate greatly. Thus developers that have a larger proportion of

their business in markets with weaker buyer bargaining power will obviously

realize higher returns.

Near the peak of a property cycle, the

combination of investment and end user

demand generally outstrip available supply.

This gives developers tremendous pricing

power and leads to outsized returns.

Conversely, near the bottom of the cycle,

developers are usually overstocked and

must cut prices to move units.

In the transaction of any large sized

purchases, information is the key to

knowing what a reasonable price to pay is.

Figure 1 Property Cycle In the absence of rules and regulations,

developers often maximize revenue by

trying to extract the maximum possible price for each unit. They can do this by 1)

not publishing any standard price lists and 2) not reporting critical information

such as how many units have been sold and at what price. This situation is

generally known as asymmetric information and gives the developer tremendous

power. However, in most large markets, regulators are aware of this and have

enacted laws to protect consumer interests by making information more

transparent and readily available. In general, all else being equal, consumers in

T1/2 cities or those with consumer protection laws have more bargaining power

than cities without protection.

Lastly, developers that are on solid financial footing (larger resulting from a more

prudent management of working capital) would generally have greater pricing

and operational flexibility than those that are financially overstretched heading

into a cyclical trough.

China Residental Developers - Industrial Analysis June 2011 5