2.

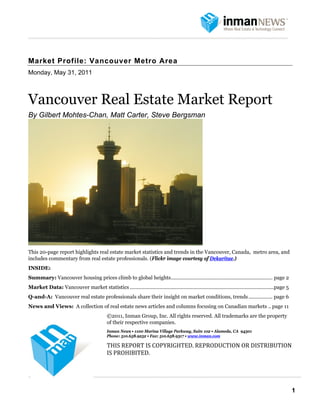

Vancouver Real Estate Market Report

Vancouver housing prices climb to global heights

By Gilbert Mohtes-Chanr May 31, 2011

Home prices in Greater Vancouver, Canada, continue to rise as the region's spring homebuying season got off to a

strong start.

Buyers flocked to the market during the first quarter, fueled by heavy sales volume in the Richmond and

Vancouver West areas. Although housing sales slowed in April, the benchmark housing price increased, topping

$620,000.

Recent changes in mortgages rules could make it even tougher for first-time homebuyers to enter the market,

considered one of the priciest housing markets in the world.

This report highlights real estate market statistics and trends in the Vancouver metro area and includes a chart

with detailed market data and commentary from local real estate professionals.

Overview

Greater Vancouver housing sales cooled off in April after moving at a red-hot pace the previous two months.

Canada's third-largest metropolitan area saw residential sales of single-family detached, attached and

condominium properties decline 21 percent to 3,225 year-over-year, according to the latest report from the Real

Estate Board of Greater Vancouver. Sales were off 8.2 percent from March. The board attributed the April sales

decline to a slowdown in condo sales.

The board's benchmark Housing Price Index for all residential properties rose to $622,991 in April, up 5 percent

from $593,419. The benchmark represents the sales price of a typical property within the market and is

considered a more accurate reflection of prices.

A sales spurt of multimillion-dollar homes in some parts of Vancouver skewed the average sales price of a home

nationally, pushing it up to $372,544 in April, according to the Canadian Real Estate Association.

An influx of homebuyers from mainland China in the past six months has triggered a wave of seven-figure housing

sales, especially in the Richmond and West Vancouver locales.

The Canadian Real Estate Association reported the average sales price in April for a Vancouver residential

property at $815,252, easily outpacing the average sales price tracked for 15 other major Canadian cities.

Neighboring Victoria ranked second nationally, at an average sales price of $508,005, followed by Toronto at

$477,406. Vancouver real estate officials say April's residential sales reflect typical spring activity and indicate a

better balance between the supply of housing on the market and demand from homebuyers.

In fact, sales were up 8.8 percent compared to the same period in 2009, and were unchanged from 2008.

In contrast, the number of homes sold and added to the market moved at a near-record pace in February and

March.

Fewer new properties came onto the market in April than the year-ago period -- 5,847 compared with 7,648 in

April 2010, a 23.5 percent drop. New listings were down 14 percent from the previous month.

"We are sitting on a good, strong, stable market. The consumer out there is always more comfortable with a

normal, stable market," said Rosario Setticasi, president of the Real Estate Board of Greater Vancouver. "Right

now we are sitting at that edge. If sales pick up, it's a seller's market again."

Here's the April sales breakdown by housing type:

2

3.

Vancouver Real Estate Market Report

1,402 single-family detached homes, up 2.3 percent from a year ago; the benchmark price of $879,039 is up 7.4

percent year-over-year.

1,201 condos, down 21.3 percent from a year ago; the benchmark price of $409,242 is up 2.9 percent year-over-

year.

622 attached homes, up 1 percent from a year ago; the benchmark price of $514,670 is up 2.4 percent year-over-

year.

Unlike many of their counterparts in the U.S., Vancouver real estate professionals are seeing a steady housing

market in a post-recession recovery. Because of tighter and more conservative lending practices by the nation's

financial institutions, Canada's housing market isn't burdened by a glut of distressed properties as in the U.S.

"Our banking system tends to be a little more conservative in providing loans for homes. That (mortgage)

meltdown did not have any affect in our banking industry." Setticasi said.

"Bank foreclosure properties are not spiking. There's the usual amount of bank foreclosures that seem to be

related just to personal issues," said David Hutchinson, an agent at Century 21 In Town Realty in Vancouver.

"Foreclosures rarely are really good deals in Vancouver. There is a system in place to ensure market value of the

sales price."

In British Columbia, only 0.49 percent of all residential mortgages were at least three months in arrears in

February, according to the latest figures from the Canadian Bankers Association. That's up slightly from 0.41

percent during the same period a year ago, 0.27 percent in 2009, and 0.16 percent in 2008.

Canada's economy sputtered in the second half of 2008, fell into a recession, and then began to rebound by the

end of 2009. Last spring, the British Columbia Business Council predicted the province would become one of the

country's growth leaders over the next couple of years.

The council's British Columbia Economic Index continued to rise in the first quarter of 2011, signaling moderate

growth for the province.

"Our economy seems to be clicking pretty good out here," Setticasi said. "The West Coast is a desirable area."

Desirability comes with a price, as Vancouver is one of the world's least affordable housing markets.

In a February Housing Trends and Affordability report, Royal Bank of Canada senior economist Robert Hogue

wrote, "In our view, the area's poor affordability -- the RBC measures for Vancouver are still far above their long-

run average -- will continue to weigh on local demand and cause a high degree of stress within the market."

Compounding the affordability issue, Hogue said, is the cost of borrowing, which is expected to rise in the next

two years.

"With prices rising, there is always a concern about affordability," Setticasi said.

Yet Vancouver and British Columbia, in general, remain attractive markets for Canadians looking for better job

prospects or a place to retire. Statistics show more Canadians are moving to the province than leaving, the British

Columbia Business Council reports.

Considered Canada's gateway to the Pacific, Vancouver increased its global visibility as host to the 2010 Winter

Olympics. It has seen a recent wave of foreign investors, especially homebuyers from mainland China, who are

purchasing properties in areas such as Richmond and the west side of Vancouver.

To seize this opportunity, some brokerages have formed Mandarin-speaking real restate teams.

"The Vancouver West detached home market is red-hot with mainland China foreign investment. Some homes

(are selling at) a half-million dollars over asking price," Hutchinson said.

3

4.

Vancouver Real Estate Market Report

"The Vancouver West market is now pushing the same trend eastward to traditional blue-collar East Vancouver.

It's now pushing these usually affordable, older-type homes into the $1 million range."

Gilbert Mohtes-Chan is a freelance writer based in California.

4

5.

Vancouver Real Estate Market Report

Market Data

Vancouver Metro Area

Population (2010 estimate) 2,374,628 million

Population growth (2001‐10) +19.5%

Total closed sales (2010) 30,595

% change closed sales (2009‐10) ‐14.2%

% change closed sales (April '10‐April '11) ‐8.2%

Sales per person 1 sale per 78 people

Benchmark sales price (April 2011) $622,991

% change benchmark sales price (April '10‐April '11)+5%

% mortgages in arrears (British Columbia, Feb. '11) 0.49%

% of sales distressed (March 2011) +60%

% household income needed to afford a house 77.8%

% unemployment (April '11, 3‐month moving avg.) 11.8%

Walk Score 72

Rent‐vs.‐ownership ratio (% households in 2006) 35%/65%

Sources: Statistics Canada, British Columbia Ministry of Citizens' Services, Real Estate Board of

Greater Vancouver, Canadian Bankers Association, Walk Score and RBC Economics Research.

5

6.

Vancouver Real Estate Market Report

Q-and-A

Inman News asked some area real estate professionals to share their insights on the latest real estate market

trends in the Vancouver, Canada, metro housing market.

Q: What types of properties are selling fastest and slowest in your market area?

Susan Keevil

Agent

Re/Max Select Properties

In regard to the downtown attached markets, we continue to see high activity in the entry-

level price points, with one-bedrooms in the $399,000 to $499,000 range moving well,

especially in the core areas.

Similarly, entry-level two-bedrooms in the $500,000 to $625,000 range continue to move at

Susan Keevil a good pace. Westside neighborhoods with proximity to the downtown core have also seen

transaction volume increases over the past few months.

Renovations have been the flavor of the day on the Westside, with many owners opting for full upgrades in hope of

tapping into the demographic of first-time buyers who seem to prefer "new and contemporary."

Luxury properties continue to move at a more moderate rate, with a number of relatively recent project

completions. Westside detached homes continue to move at a great pace; the market has displayed resounding

stability over the past year or so with entry-level homes.

Andrew Peck

Vice president and general manager

Royal Pacific Realty

The Westside of Vancouver and West Vancouver are hot for single-family property purchases.

Chinese immigrant buyers are driving this market. Since Jan. 1, for West Vancouver homes

priced from $3 million to $10 million, there have been 74 sales, with the top price being $6.5

million, whereas in the same period last year there were only 32 sales for that same five

months.

Interestingly, the new-house market in the Vancouver Westside area is slow due to

anticipation that there may be a tweaking of Harmonized Sales Tax (a combination of the

federal and provincial sales taxes) in the upcoming referendum. Also the buyers are Andrew Peck

purchasing older properties with the intent to have a custom home built for them at a later

date, thus saving the HST on the land component.

Scott Russell

Managing broker

Sutton Group

Seafair Realty

Richmond, Canada

The fastest-selling properties in our market are single-family homes ... where the new buyer

will be redeveloping in the near future to accommodate a new home.

Scott Russell

6

7.

Vancouver Real Estate Market Report

Matthew Collinge

Agent

Royal LePage Westside

Single-family homes are selling fast. This is being driven by in influx of buyers from

mainland China who are looking for a safe place to invest in real estate. The condo market is

slower. There is a ... growing supply of condos. They aren't building any more single-family

lots in the city of Vancouver.

David Hutchinson

Agent

Century 21 In Town Realty Matthew Collinge

I feel Vancouver is now going through its real estate renaissance. I have

seen the dynamic changes that have taken place over the years: Expo

'86, 2010 Winter Olympics, and the huge influx of foreign investment over the years from all

over the world.

David Hutchinson

Dan Scarrow

Vice president, corporate strategy

Macdonald Realty Group

Single-family homes in the city proper are the best-selling asset class. Apartments and

townhomes are still strong; however, the market is more "normal" and less "heated" the

further outside of Vancouver you go.

Q: Is anything changing about the demographics of buyers and sellers in your market

area? Dan Scarrow

KEEVIL: Vancouver has long been a very global market, with participants ranging all the way from mainland

China and Hong Kong to the Middle Eastern areas, as well as Europe and the United States. Along with these very

worldly market actors we have the local Vancouverites, including many first-time buyers who quite often operate

under the dual-income models, who help fuel much of the entry-level condominium activity.

Overall, the Vancouver markets have remained a steady mix of many people from many places; though we have

seen a bit of a tail-off in the luxury international "jet setter," markets with very-high-value properties often taking

a bit longer to sell, with a slight downward pressure on prices.

PECK: I have seen a very strong immigrant market from Asia and ASEAN member countries, particularly those

whose economies are quite sound and where there might be political uncertainty. As the region comes out of

recession, we see more employment, particularly of young new immigrants, and they are very keen to be

homeowners quickly.

Because of tightened mortgage entry standards, a lot of buyers were jumping early to get their mortgage qualified

sooner and to hold rates. Most expect there to be some shift upward in the Bank of Canada prime rate -- slowly,

over the balance of the year.

This is also causing new buyers to be very conscious of rates. While most commissions we see being charged on

paper are quite typical, we do see a lot of discounting on closing deals, with rebates to both buyers and sellers.

This is quite typical of new immigrants expectations in this marketplace.

HUTCHINSON: I'm seeing more first-time homebuyers purchasing homes with the help of their parents.

SCARROW: Locals are being priced out of the single-family home market in Vancouver and are looking more at

apartments and townhomes, as well as outlying suburban areas.

7

8.

Vancouver Real Estate Market Report

Q: What are recent trends with prices, sales and inventory?

KEEVIL: Downtown attached condominium and townhouse sales continued to be a strong point for the

Vancouver market. Entry-level activity has been especially busy (in) ... the False Creek North corridor and

Yaletown proper areas. We have, however, seen a bit of a peak in a recovery wave we have been riding for the

greater part of the past year.

Westside detached homes have continued to demonstrate stability, with much of the product still moving in good

time, and quite close to asking prices.

PECK: Prices will continue to rise over the balance of this year, but not nearly as rapidly as they did in those first

three months. We haven't seen too much movement upwards in condo prices, particularly in the high end, but

new condo projects continue to have a speculative market for people who purchase with the intent to eventually

flip for a small profit. We are also seeing a large number of sales (more than 50 percent in the key market areas)

selling for more than the asking price.

The other thing we have seen this year is the number of days on the market is very short for preferred areas. Good

locations have only been on the market for mere days, whereas last year we would see properties on the market for

30 to 90 days for the same area. This might modify as the spring market settles down with more listings.

HUTCHINSON: There's a marginal higher inventory of homes for sale, but prices are not declining. Richmond,

which is a predominately Asian community where street signs are in Chinese and English, has skyrocketed 20

percent in price over the last year.

SCARROW: Prices have increased significantly in the past year, predominantly for single-family homes in the

more tony neighborhoods of Vancouver. Some areas have experienced price gains in excess of 30 percent in the

past 12 months. Sales have remained brisk for the past couple of years, consistently beating the 10-year average,

while inventory is low.

Q: What worries you most about the current state of the market, and what represents a sign of optimism and

opportunity for the real estate market?

KEEVIL: As far as the central Vancouver West real estate markets are concerned (including downtown and the

Westside neighborhoods), there should be room for optimism grounded in stability. We have been riding the post-

recession wave for the greater part of 12 months,

And though it may "crest" to a degree, we feel confident in the markets' sustainability and insulation from

potential shocks. Alongside a strong contingent of global investors and part-time residents, we see a strong push

from our local buyers and sellers, with first-timers fueling much of the entry-level condo market, new families

moving up to starter homes, and empty nesters downsizing -- plus, just about everything in the middle.

Healthy banking conditions and mortgage considerations make for predominantly stable and solid ownership,

with minimal risk of foreclosure or short-sale activity in our core markets.

RUSSELL: Affordability is always a concern in a rising market. With interest rates trending upward, it will only

provide more pressure on first-time buyers.

PECK: Affordability and government intervention to try to quiet a market (particularly in mortgage markets) tend

to have a short-term flurry effect, which drives prices up further. I also think that governments are not paying

attention to the fact that we are overly taxed in the real estate sector.

COLLINGE: My biggest concern is the high prices and affordability for the average Vancouver homebuyer. This

past month has shown a calming of the Vancouver real estate market, and it is approaching a more balanced

market.

8

9.

Vancouver Real Estate Market Report

SCARROW: Prices have been increasing at an unsustainable rate for the past 12 months, while local buyers are

being priced out of the market. Chinese immigration has always played a large role in the health of the Vancouver

real estate market and this trend is expected to continue for the foreseeable future.

Q: Where are sellers moving to, and where are the buyers moving from in your market area? Does this

represent a change?

KEEVIL: Our markets tend to act in tandem much of the time with the interactivity between the downtown

attached and Westside attached markets also influencing the detached markets as families move from condos in

Yaletown to starter homes in Cambie or Mount Pleasant.

We continue to see the influence of the global actor, with many potential buyers still coming from areas like

mainland China and the Middle East. Recent developments in the Fairview and Cambie areas, including the new

Canada Line, have assisted in linking many areas of Vancouver and have drawn buyers to new developments and

older condominiums in these areas due to the ease of travel around the city.

RUSSELL: Many sellers are downsizing or leaving the city as they are taking advantage of lower prices in

surrounding communities. This is probably pretty typical of a seller's market.

PECK: Local sellers are seeing the opportunity to cash out of single-family properties and move to a condo

lifestyle, particularly in the high-end downtown core. Also, some are sitting on cash, waiting for what some

speculate (will be) a course correction. However, that may not be proven in the long run.

An informal survey of the Okanagan retirement areas of Kelowna and Penticton has not seen a flood of Vancouver

buyers who are seeking a retirement home. I don't expect too many buyers coming from other areas of Canada or

the United States. The Asian market will remain the strong market influence.

HUTCHINSON: Sellers are moving to the suburbs, where they can get more bang for their buck. For example, a

couple just sold their house in Vancouver West Kitsilano, and bought another house in Vancouver East; and could

put $500,000 cash in their pocket. Also, with SkyTrain, some young couples starting new families are moving

from downtown along to the SkyTrain line to New Westminster and Surrey, making a lateral move cash-wise, but

into larger homes.

SCARROW: Locals are looking to downsize, switch asset classes, or move to other, cheaper areas of the province.

A recent Macdonald Realty study found that Chinese buyers purchased 78 percent of homes priced over $2

million. And while $2 million represents a luxury home in most other jurisdictions, it is the benchmark price for

an average home on the Westside of Vancouver.

Q: How have you changed your business to mirror the market and to capitalize on market trends?

KEEVIL: The Internet continues to offer a progressive and constantly changing marketing landscape with

limitless potential for lead generation, client maintenance, and social media. Still, we remain committed to our

clients and referral system, with many of our new listings and buyers coming from recommendations from past

clients, friends and family.

The Internet continues to develop and be an important tool for us as well, though we do still participate in some

targeted paper marketing and ad campaigns aimed at augmenting our other marketing types.

RUSSELL: Our marketing plan is traditional real estate: Build strong relationships, encourage sellers to list at

realistic levels, and have a healthy communication plan with your clients.

PECK: We have had to hire significantly more support staff to keep up with the increased number of transactions.

We have seen a surge in the number of new Realtors joining the profession as well, and they are younger than

before -- particularly those from Asian countries. Brokerage models have not adapted too much to changing

demographics, meaning that large brokerages with several hundred agents remain core to the business.

9

10.

Vancouver Real Estate Market Report

While sales prices might be skyrocketing, commissions have not kept similar pace. Those new entrants are willing

to do more work for less money in order to get a foothold into the market. The conventional paper mail-out

through the local postal service is now being superseded by social media and Internet advertising.

This represents less cost, but is a more time-consuming approach to marketing; which, naturally has an increased

labor cost. So, there is a trade-off there.

SCARROW: Many companies now have an "Asian" strategy to try to capitalize on this market. These brokerages

have hired Mandarin-speaking agents and staff to meet this growing demand.

Q: What are some overall economic trends you are seeing in your market area that will guide the real estate

market?

KEEVIL: Vancouver remains a unique market due to the international variables that see a large amount of foreign

capital flowing both into and out of the city; as such, the core Vancouver West markets tend to be a bit more

sensitive to fluctuations in global economics. Anything from commodity prices to currency exchange rates can

have an immediate or delayed impact on real estate activity in the city.

The stability of the Canadian banking system, election of a new Conservative majority government, and

progressively strong commodity valuations will all assist in making Vancouver a desirable area in which to own

real estate assets, and assist in spreading the perception that Canada as a whole is better equipped, from a

financial standpoint, to deal with possible shocks and economic downturns in the future.

PECK: British Columbia has come through the recession relatively unscathed. However, the shining market is

really in the Vancouver metro area rather than in other areas that have been traditionally more resource

dependent on export to the United States and other places.

We don't expect any significant changes in the mortgage rates, which remain a good sign. However there remains

concern that if buyers are overextended and once rates finally do shift upward, that some will feel shrinking

disposable income once their mortgage debt is serviced. With rising energy prices in the region (second-highest

gas prices in the country) consumers will continue to seek housing closer into the central core, which will trend

prices upward.

SCARROW: Canada remains a strong personal and investment destination for overseas buyers. The immigration

consultants I work with believe that Canada is now the No. 1 desired destination for Chinese immigrants, ahead of

the U.S. and Australia, with Vancouver absorbing the most investment-category immigrants. These factors will

ensure that the Vancouver real estate market will remain buoyant in the near term and midterm.

Gilbert Mohtes-Chan is a freelance writer in California.

10

11.

Vancouver Real Estate Market Report

News and Views

Regulators' lawsuit seeks real estate VOWs

Toronto Real Estate Board says it's moving to implement rule change

By Matt Carter May 27, 2011

(Flickr image courtesy of Abel Cheung.)

Canadian regulators have sued the Toronto Real Estate Board (TREB),

saying it's denying agents the ability to share in-depth listing information

with consumers through password-protected Virtual Office Websites, or

VOWs.

TREB -- which with 31,000 members is the largest real estate board in

North America -- says it's working to implement rules governing VOWs

by the end of August, and that the suit by Canada's Competition Bureau

amounts to little more than political grandstanding.

Technology-based U.S. brokerages like ZipRealty and Redfin employ

VOWs to provide consumers with access to deeper listings data, rivaling

what brokers and agents see when they log in to their multiple listing

service (MLS).

VOW sites let consumers see previous listing and sale prices, historical prices for comparable properties in the

area, and the amount of time a property has been on the market, for example.

While agents who belong to TREB can provide detailed MLS listings information to customers by hand, mail, fax

or email, "there are currently no VOWs operating in the Toronto real estate market that enable customers to

search a full inventory of listings," the Competition Bureau said in announcing the suit.

In its complaint, the Competition Bureau said real estate boards and associations in other Canadian jurisdictions,

such as Nova Scotia, allow members to provide Internet-based services.

VOW brokerages "have lower operating costs and are able to offer markedly reduced commission rates or

significant rebates to their customers, a practice denied to would-be innovative brokers" in the greater Toronto

area, the complaint said.

In 2007, the Competition Bureau alleged in its complaint, TREB went to court to enforce its right to terminate a

prospective VOW operator's access to the MLS.

"TREB has cultivated a reputation for shutting down any broker who develops an innovative service that is

prohibited by the TREB MLS restrictions, including VOWs," the complaint states. The board "has created a hostile

environment for VOWs" in the Greater Toronto area, "resulting in a chilling effect on any broker who would

otherwise wish to invest the time and money (including legal fees) necessary to begin operating a VOW."

TREB President William E. Johnston said the board sees allowing VOWs "as a reasonable thing to do," and began

a process for implementing the necessary changes to MLS policies in July.

11

12.

Vancouver Real Estate Market Report

TREB's board of directors has signed off on the concept, and an MLS committee is drafting proposed rules,

Johnston said. Under TREB's bylaws, the proposed rules would be subject to member comment for 60 days before

the board of directors votes on them in August.

Johnston said the rules will be similar to those adopted by the National Association of Realtors in 2008 to settle a

lawsuit filed by the U.S. Department of Justice.

The settlement gave brokers and agents who belong to NAR-affiliated MLSs the right to operate VOW sites, and

many non-Realtor-affiliated MLSs also offer such capabilities.

"It's heading in a good place -- as a board we're fully in favor of VOWs, we just want to make sure it's done

properly," with consumer protection in mind, Johnston said.

Canada has "very strong privacy laws and laws around identification of financial transactions," said TREB board

member Richard Silver.

"We have been using the NAR VOW policy as a model and are on track moving forward but sadly, not fast enough

for the Competition Commissioner," Silver said, referring to the Competition Bureau's head, Melanie Aitken. "As

you know, member organizations don’t have the flexibility the corporations may have."

A spokesman for the Competition Bureau said regulators have been in discussions with TREB since early this year,

with the goal of achieving a "mutually agreeable voluntary resolution."

Eventually, the spokesman said, "it became clear to us that (TREB) was not willing to make substantive changes to

(its) practices" to address the bureau's claims that the board's policies amounted to anticompetitive restrictions.

Johnston called that assertion "totally ridiculous," saying TREB was engaged in good faith discussions when the

Competition Bureau filed a "headline grabbing" lawsuit with Canada's Competition Tribunal, an administrative

court that decides disputes over issues ranging from mergers to restrictive trade practices.

Asked whether other Canadian real estate boards restrict members from operating VOW sites, the Competition

Bureau spokesman said it took action against TREB after receiving complaints about that board's practices.

"Should any other real estate board be engaging in similar activity, we'd like to know about it," the spokesman

said.

The Competition Bureau and the Canadian Real Estate Association last year entered into a consent agreement that

ended a 3 1/2-year battle over rules that the bureau alleged were aimed at restricting competition from flat-fee,

limited-service brokerages.

12

13.

Vancouver Real Estate Market Report

North America's newest real estate renaissance

Natural resources fuel housing, population boom in North Dakota,

Saskatchewan

By Steve Bergsman March 11, 2011

Six years ago, my wife and I took a car ride through the center of Saskatchewan, Canada, spending a few days in

the capital city of Regina and the small, isolated town of Moose Jaw. We preferred Moose Jaw.

At least Moose Jaw had some quirky things going for it, such as an underground town trail. Regina seemed beat-

up and despondent. I guess I arrived two years too early, because around 2007 the province of Saskatchewan

caught economic fire, uplifting its two biggest cities: Saskatoon and Regina.

When the U.S. and Eastern Canada began slipping into recession and residential real estate values collapsed like

deflated balloons, home prices skyrocketed in Saskatoon and Regina and investors partied like it was 1999 in a

Miami Beach condo. They are still partying today, but more moderately.

"In Regina, three-bedroom houses that sold for about $110,000 in 2006 saw prices climb to $270,000 before

leveling off," reported Rod Spence of Century 21 Conexus Realty Ltd. in Regina.

Things were even better in Saskatoon, where the $160,000 average home price in 2007 vaulted to $300,000 by

the spring of 2010, said Norm Fisher with Royal LePage Saskatoon Real Estate. Prices have leveled off there, too,

with average homes prices now fluctuating between $275,000 and $300,000.

The person who clued me into the Saskatchewan renaissance was Bill Madder, executive vice president for the

Association of Saskatchewan Realtors. "Saskatchewan used to be known for cheap houses and not many people,"

he said.

For the past decade, I'd been visiting Canada at least twice every year and that was my impression as well. Next to

Newfoundland, Saskatchewan was the most disparaged province in the country. Ask about Saskatchewan and the

first thing someone would do is repeat the painful canard that the province is so flat you can watch your dog run

away -- for days.

Realtors and homebuyers suffered. "The way it used to be in Regina was you would buy a house for $150,000 and

five years later it was worth $150,000," Spence joked, but the comment had a strong grain of truth to it.

What changed for Saskatchewan were two things: one temporal and the other of more sustenance.

As in the U.S., home prices were quickly escalating in most major Canadian cities since the mid-1990s so investors

looking around for cheaper playing fields discovered Saskatchewan, which had completely missed the residential

run-up. Investment dollars poured in.

"In 2007, we had 4,000 transactions -- that was a 33 percent increase over the year before," Spence said about

Regina. (In 2010, 3,500 homes were sold through November.) In Saskatoon, during that wacky 2007, home prices

jumped 20 percent. (Prices are still rising but at a much more moderate rate, said Madder, probably at a 4 percent

to 5 percent pace in 2011.)

As prices escalated, pure investment interest in residential housing waned, which is OK because sustainable

investment capital has taken its place.

Although mostly known for its agriculture, Saskatchewan has blossomed because demand for its natural resources

skyrocketed, attracting billions of dollars in investment and immigration from other provinces. Saskatchewan

boasts 51 percent of the world's deposits of potash, which is used in fertilizers.

13

14.

Vancouver Real Estate Market Report

Less known is the fact that Saskatchewan is Canada's second-largest producer of oil behind Alberta. However,

much of Alberta's oil comes from tar sands; in Saskatchewan you can get the product the old way, by pumping it

out of the ground.

With the development of natural resources came jobs and people to fill those jobs. "We have been running about

60,000 new immigrants a year across the province over the last couple of years," said Fisher. Most of those folk

settle in or near Saskatoon or Regina.

Saskatoon's population has grown 10 percent since the start of 2007 and today is around 225,000 people, slightly

more than Regina, which has a population of about 210,000. The latter city boasts one of the lowest vacancy rates

in the country, under 1 percent for rental housing.

Both cities are playing catch-up. According to the Canada Mortgage and Housing Corp., during the first 11 months

of 2010, 650 single-family houses were built in Regina, up from 569 units the year before. In Saskatoon, 1,522

detached single-family units were built over the same time period, up from 1,004 units in 2009.

Apparently, Saskatchewan's good fortune has spilled south of the border into North Dakota. The Wall Street

Journal, with a headline screaming, "Resource-Rich States Surge," reported, "The states that weathered the

recession best were the energy-rich states of North Dakota and Alaska."

I gave a call to Dan Deutsch of www.fargohomes.com to see what was happening in North Dakota's largest city.

"Our economy is good; unemployment is close to 3 percent; the state budget is in the black; we have few

foreclosures; and homes on the market close in three months," he said.

The median home price in Fargo stands at $160,000, about where it was last year, and very close to peak, said

Deutsch. While appreciation isn't great, the good news for Fargo homeowners is the last time the market saw a

significant downturn in residential values was back in the 1970s.

From 1990-2000, the city of Fargo grew just over 20 percent, to about 91,000 people. In the past decade, Fargo

grew another 10 percent to about 100,000. (The metro area counts about 200,000 people.)

According to Deutsch, business has been good, as he closed an average two home sales a month in 2010. "Loans

are easy to get here," he said. "The banks aren't afraid to lend money."

For a long time, North Dakota, like Saskatchewan, had not been on anyone's radar as place to find work and live,

but the northern Midwest states and provinces are finally having their day in the economic sunshine.

Steve Bergsman is a freelance writer in Arizona and author of several books. His latest book, "After the Fall:

Opportunities and Strategies for Real Estate Investing in the Coming Decade," has been ranked as a top-selling

real estate investment book for the Amazon Kindle e-reader.

14

15.

Vancouver Real Estate Market Report

Real estate tales from the borderlands

Sizing up capital cities along U.S.-Canada boundary

By Steve Bergsman Nov. 29, 2010

About two months ago, I took a look at how the housing markets in two of North America's capital cities --

Washington, D.C., and Ottawa, Canada -- fared in the recent downturn.

As it turned out, both markets saw some slight downturn, but with a stable employment base of federal workers

and government lobbyists, the cities came through the global recession without the bruising real estate market

maladies experienced in other major cities.

That got me thinking about state and provincial capital cities, so I abstractly chose a region in North America

along the Canada/U.S. border to take a peek at municipalities where smaller but equally prevalent government

bureaucracies were a key factor in the local economies.

My region of choice was northern New England and the province of Quebec, which borders my three states of

focus: Vermont, New Hampshire and Maine.

It was interesting to throw the province of Quebec's capital city, Quebec City, into the mix because of the four

locations it is really the only one of significant size with a population of almost 500,000 (the metro population is

more than 700,000).

In comparison, the three northern New England capital cities are tiny. The largest is Concord, N.H., at 43,000

people, and then we get to two of this country's smallest capital burghs: Augusta, Maine, at 19,000 people; and

Montpelier, Vt., at 7,800.

While the three U.S. capital cities experienced minor economic tremors from the global recession, Quebec City

probably did as well, if not better, than most major metropolitan areas in North America. Of course, these are all

older cities where the local housing markets saw modest gains during the boom times and didn't really expect too

much disappointment in the bust.

As a provincial capital city, Quebec City is extremely dependent on its government bureaucracy, which accounts

for 30 percent of jobs. Toss in a big, still-expanding insurance industry presence and that's about 50 percent of all

jobs.

There is also a growing manufacturing sector. Earlier this year, Quebec City boasted the lowest unemployment

rate in Canada, at below 4 percent.

After extrapolating that cursory employment information, you might hazard a guess that the housing market in

Quebec City rests on very stable ground. And you would be right.

"The market is strong today, and prices continue to rise," reported Jeannette Casavant, an independent real estate

agent in the city.

However, the one sign of weakness in the market is that it is taking longer to sell a house today. "Before, if a house

was on sale you would immediately have three offers at the same time. Now, it sells within 60 days. There are still

a lot of buyers out there," said Casavant.

Going back a decade, Canada suffered an economic slowdown and housing prices weakened across the country,

including in Quebec City. So back in 2002, if you were lucky you might have a found a two-bedroom condominium

in a great Old Town location for $200,000. Today, if it went on the market it would sell for $500,000.

"Prices have appreciated quite a bit lately and that means we have gained back what we lost 10 years ago,"

Casavant said. "Prices will continue to rise."

15

16.

Vancouver Real Estate Market Report

In 2008, the unemployment rate in New Hampshire was a mere 4.3 percent. A year later, unemployment spiked

upward to 7.2 percent, the state's highest rate in 17 years.

That wasn't felt too severely in Merrimack County, where the capital city of Concord can be found.

"It always seems as if the state has a lot of job openings," said Karen Hatch, regional development manager for

The Bean Group in Bedford, N.H.

"If you are looking for employment, go to the state site -- there are always listings for jobs," she said. "I haven't

heard the state was laying off; it seems as if we are not at capacity for jobs."

As for the housing market in Merrimack, the downturn has been very mild.

"In 2009, the average selling price in Merrimack County was $206,000; it was $201,066 in 2010," Hatch

reported. "As for the average amount on time on market before a house sells, it's averaging 146 days this year,

about the same as the year before."

Things are looking even better in Kennebec County, Maine, home to the capital city of Augusta and a population

base of 117,000 folks.

The median sale price of a home from January 2010 to July 2010 was up 2 percent over the same period the year

before, noted Anne-Marie Haywood, regional development manager for The Bean Group, in Portsmouth, N.H.

"The number of units sold from January 2010 to July 2010 hit 560 -- that's up from 507 units, again for the same

period of time in 2009."

Both the private and public sectors cut jobs in Kennebec County, said Haywood. She suspects the salubrious

numbers in the first part of 2010 had something to do with the tax incentive. It will take a few more months, post-

ending of the tax credits, to see if the local market has indeed held strong.

One troubling sign for Kennebec County and the surrounding region: After government, the biggest industry is

tourism, and visitation numbers are down.

The one regional capital city where the housing market noticeably softened was Montpelier, Vt., which is the

smallest capital city in the country. The shire is located in Washington County, home to 58,000 very independent

citizens.

"Our major industries are government, government-associated industries and insurance," said Tim Heney, a

principal with Heney Realtors in Montpelier. All that couldn't bolster the housing market.

Average home prices peaked in 2006 at $242,600 and then fell to $188,100 in 2009. Back in 2006, homes sold

briskly with an average time on market of about 40 days. Today, it takes 120 to 140 days to sell a home.

The numbers look worse than they are, said Heney, because what has been selling has been lower-end homes.

"Montpelier is very stable," he stressed. "People are buying homes -- there are just not as many buyers as we

would like."

More than 200 years ago, the English kicked the French out of North America. Today, the economy in the former

colony of New France outpaces neighboring New England. Revenge is sweet, even if it is a bit late.

Steve Bergsman is a freelance writer in Arizona and author of several books. His latest book, "After the Fall:

Opportunities and Strategies for Real Estate Investing in the Coming Decade," has been ranked as a top-selling

real estate investment book for the Amazon Kindle e-reader.

16

17.

Vancouver Real Estate Market Report

Cashing in on capital city real estate

Investment qualities that make these areas good buys

By Steve Bergsman Aug. 20, 2010

(The Parliament House in Ottawa, Canada. Flickr image courtesy

of spettacolopuro.)

Anyone lucky enough to be living in or near the national capitals in the

U.S. or Canada over the last four years lived through something few other

homeowners in those countries experienced: home-price stability.

Sure, in certain sections of city metros surrounding national capitals,

home values softened, but for the most part homeowners saw little price

deflation. That's because capital cities boast a very stable workforce of

government bureaucrats and a panoply of private-sector consultants,

lobbyists and contractors that feed the federal bureaucracies.

In addition, in recent years, a number of companies have shifted major

operations to capital city areas just to be closer to their government paymasters.

"The largest movement of people occurs with the shadow government, which relates to government contractors,"

said Pauline Thompson, president and founder of Tysons Realty Inc., in the Washington, D.C., suburb of Tyson's

Corner, Va.

"Northrop Grumman, Hilton and Volkswagen International have moved headquarters or key operations to the

D.C. area. And there are so many computer companies coming here because they are getting huge contracts. The

computer firms are looking to hire thousands of employees."

She added, "We are still in a war so military contractors are being awarded billions of dollar in contracts, and they

bring in 200 to 400 subcontractors. They all need a place to live."

The salubrious capital city home markets occupied my attention because in early summer I had the opportunity to

visit Ottawa, Canada's lovely, but often overlooked, capital.

Americans who travel often to Canada end up having favorite places -- usually it's Vancouver, Toronto or Old

Quebec. Those with a yearning for the great outdoors go to the Canadian Rockies.

No one ever chooses Ottawa, the country's capital. It's a prejudice probably felt more strongly among Canadians,

themselves. In the U.S., almost all Americans will at some point in their lives make the hegira to Washington, D.C.

Canadians fly over Ottawa on their way to somewhere else.

However, ask Ottawans where they prefer to live, and nine out of 10 would choose their home city, which mixes

cultured urbanity with an accessibility to the great outdoors. It also has good politics.

The Ottawa housing market resembles, but not too closely, that of Washington, D.C.

The global recession also hit Canada, but Ottawa suffered less than other big Canadian cities. In Ottawa, six of 10

workers are employed by the federal government, education (four universities) and health care.

Changes in administrations generally cause minor housing-market tremors. In Ottawa, incoming politicians rent.

In Washington, D.C., the Republicans of the Bush administration were buyers of homes, but the Democrats

arriving with the Obama administration have been renters.

17

18.

Vancouver Real Estate Market Report

The population of District of Columbia proper stands at about 600,000, with the metro area at 5.3 million. The

population of Ottawa city now totals 900,000, but the metro is much smaller than D.C. at 1.4 million.

The average cost of a home in the Washington, D.C., metro is around $500,000, Thompson said. In Ottawa, the

average home is $333,000, reported Chris Rhodes of Coldwell Banker Rhodes in that city.

Although, Rhodes adds, the "average" home price is misleading. Unlike Washington, D.C., Ottawa is not

surrounded by vast suburbs but by a large rural area where homes are much cheaper. The city of Ottawa boasts a

good population density and, as Rhodes points out, finding a home in the $333,000 range is "a challenge."

At the high end, homes are still cheaper in Ottawa.

The most prominent high-end neighborhood in Ottawa is called Rockcliffe Park, which can be found about two

miles from the center of the city.

"The leader of the opposition has a house here, as does the prime minister and the governor general," Rhodes

said. "It's a very pretty area and not a lot of homes under $1 million. Many homes fall into the $3 million to $4

million range, although one recently sold for $8 million."

That home had some history, as Princess Juliana of The Netherlands lived there during World War II. Recent

owners acquired the neighboring property, so the grounds now total more than an acre, part of which sits on a

small lake. No politicians were involved in this purchase. The past owner was in high tech, as is the new owner.

"Rockcliffe now represents just one-third of the high-end transactions in the city, as million-dollar home sales are

occurring in different areas," Rhodes said. "The other sales have occurred along the waterfront of the Ottawa and

Rideau rivers and in a nice (actually, one of the hippest core city locations) neighborhood called The Glebe."

Ottawa's original condo market began developing back in the 1970s and then fizzled out until around 2000, when

another huge spurt of construction created mid-rise condo developments in or near the downtown. Although

some high-end condo sales have been near the seven-figure mark, this is a market that is unstable, Rhodes said, as

about 50 percent of recent sales have been to investors, not end-users.

Of course, both the Washington, D.C., and Ottawa metros have lower-end neighborhoods. Ottawa was built on the

banks of the Ottawa River and once you cross the bridge to the other side, you enter French-speaking Quebec,

where the population is generally poorer.

In the D.C. area, Thompson reported many foreclosures in markets like Woodbridge, Manassas and Sterling in

Virginia, and Gaithersburg in Maryland, where there was a higher proportion of subprime loans.

I asked Rhodes how he, personally, was doing, and he lit up.

Back in 2005, he sold 25 homes. In 2009, which was a low point for U.S. home sales, he sold 35 homes. This year,

he thinks he will hit the same high-water mark. Last year, his high-priced deal was a $950,000 home.

This year, he has a listing on a $975,000 property in another higher-end neighborhood on the west side of Ottawa.

By the time you read this column, that home could already be sold, as homes are selling briskly, often turning over

within 40 days of listing.

"We have been blessed," said Rhodes. "We have a low unemployment rate here; prices have been climbing

steadily; and from a Canadian standpoint, we are reasonably priced."

Steve Bergsman is a freelance writer in Arizona and author of several books. His latest book, "After the Fall:

Opportunities and Strategies for Real Estate Investing in the Coming Decade," has been ranked as a top-selling

real estate investment book for the Amazon Kindle e-reader.

18

19.

Vancouver Real Estate Market Report

Westmount: Canada's Beverly Hills?

Montreal borough has celebs, multimillion-dollar homes

By Steve Bergsman April 14, 2011

(Homes in Westmount, a Montreal borough. Flickr image courtesy of

Peter Blanchard.)

This past winter, my wife and I were taking a tour of Montreal when our

guide mentioned that Westmount, the area of the city we had just passed,

was probably the only place in Canada where homes hadn't lost value

during the global recession of the past four years.

My attention, which had been waning, suddenly perked up and I asked

the guide to give my wife and me a quick swing through the area.

My guide, a lovely, informative Montreal native, Annique Dufour, was

absolutely right on about all things Montreal -- except for Westmount

homes not losing value -- but she is forgiven since Westmount's recession

barely lasted 12 months and the homes lost value in the single digits, at

most.

Westmount, which is really a borough of Montreal, experienced a drop in

prices of 5 percent from 2009-10, notes Marie-Yvonne Paint, a broker

with Royal LePage Heritage in Montreal. "2009 was the year of the global economic crisis, and people stopped

buying because they were waiting to see what would happen. They were holding back, but by 2010 Canada's and

Montreal's economy appeared to be fine and everyone came back to the market."

The years 2002-09 were excellent years for Westmount, and 2009 weakened only because of the economic crisis,

Paint adds. "By 2010, sales were flying. There was such a demand for Westmount homes that the number of

homes sold in 2010 increased by more than 17 percent."

Paint, who specializes in high-end properties, does about 80 percent of her business in Westmount because "this

is where we have the most expensive homes."

In 2010, Paint boasted an extraordinary year, personally selling over $100 million in properties. She's hoping the

market stays hot, hot, hot through 2011, although realistically she doesn't think it can maintain that kind of

momentum.

Westmount begins (or ends, depending on your perspective) near the crest of Mount Royal, the iconic mountain

park at the center of Montreal. Most of the expensive homes, with values in the multimillion-dollar range, are

close to the higher elevations because of the extraordinary views of the St. Lawrence River in the distance.

As the neighborhood eases into the flatlands, it becomes more urban looking and instead of large single-family

dwellings there are more duplexes, triplexes, condos and apartments.

Dufour's parents lived closer to the heart of Westmount, while she and her daughter lived in an apartment

building where the land eases into the city proper.

The homes attract a lot of attention because of prices, but it's the urban part of Westmount that has been very

active lately because properties are cheaper and demand has been strong -- especially from young professionals

looking for a more citified experience, i.e., walking distance to shops, services and restaurants.

19

20.

Vancouver Real Estate Market Report

Westmount has all types of properties, and some of those in the flats, although somewhat standard, have seen very

strong prices, observes Thomas Castle, also a Royal LePage broker. He recently sold half a duplex for $250,000.

Homes closer to the flatlands can still be found in the $600,000 to $700,000 price range, but they need a lot of

work, and have little land and no garage, Paint says. Also, condominiums in Westmount are selling very well, at

about $700 to $800 a square foot.

"Right now in Westmount, there's a feeling that there should be more product on the market, but what is presently

on the market is being looked at and purchased," Castle says. "Real estate prices are the result of the balance

between supply and demand, and in Westmount the demand is stronger than the supply."

During the intense growth years of Montreal's history, between the 1850s and 1930s, most of the English-

speaking, wealthy families of the city lived closer downtown, in an area called the Golden Square Mile.

Then, by the turn of the 20th century, the adult children of the wealthy began settling in Westmount, which was

on the west side of Mount Royal. The wealthy French-speaking families preferred the east side of Mount Royal, in

an area that is called Outremount. To some extent, that language divide still exists today.

Outremount home prices can challenge those in Westmount, although on a general level Westmount remains the

priciest neighborhood. Still, Paint's most expensive deal in 2010 was an Outremount home that sold for $5.3

million to a couple from Paris.

That house totaled 8,000 square feet and rested on a 20,000-square-foot plot of land. Paint's other big deals,

homes that sold above $2 million, were in Westmount.

The highest-priced home Paint sold in Westmount fetched $3.5 million -- that home has 4,500 square feet,

nestled on 11,000 square feet of land. "This home sits on the top of the mountain with an incredible view of the

river and the city," she says.

Generally, you have good company in Westmount. Former motion picture actress Norma Shearer and singer

Leonard Cohen were born in this neighborhood. Today, you can find a smattering of Montreal Canadian hockey

players, former Prime Minister Brian Mulroney, Quebec Premier Jean Charest, racing driver Jacques Villeneuve,

and fashion magnate Lawrence Stroll (Michael Kors).

As its own borough, Westmount has a few other desirable advantages, says Dufour.

"My parents moved to Westmount because as its own municipality (borough) you pay a little more in taxes, but

the services are phenomenal," she says. "We get six months of winter, and even in a huge snowfall the streets are

plowed within 36 hours, whereas the rest of Montreal can take upward of two weeks."

Steve Bergsman is a freelance writer in Arizona and author of several books. His latest book, "After the Fall:

Opportunities and Strategies for Real Estate Investing in the Coming Decade," has been ranked as a top-selling

real estate investment book for the Amazon Kindle e-reader.

20