Sample Report: 2021 Key Trends of the Payment Industry: Global Real-Time Paym...

TIO - Initiation Report (July 2016)

1. Equity Research

Technology | Canadian Small Cap

July 19, 2016

Alex Cutulenco

Analyst

alex@gravitasfinancial.com

1-416-992-6731

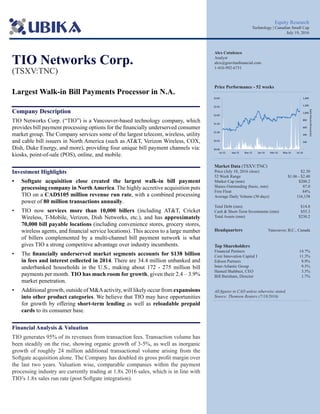

Price Performance - 52 weeks

Market Data (TSXV:TNC)

Price (July 18, 2016 close) $2.30

52 Week Range $1.06 - $2.40

Market Cap (mm) $200.2

Shares Outstanding (basic, mm) 87.0

Free Float 84%

Average Daily Volume (30 days) 116,158

Total Debt (mm) $14.8

Cash & Short-Term Investments (mm) $55.3

Total Assets (mm) $230.2

Headquarters Vancouver, B.C., Canada

Top Shareholders

Financial Partners 14.7%

Core Innovation Capital I 11.3%

Edison Partners 9.9%

Inter-Atlantic Group 9.5%

Hamed Shahbazi, CEO 3.5%

Bill Burnham, Director 1.7%

All figures in CAD unless otherwise stated.

Source: Thomson Reuters (7/18/2016)

TIO Networks Corp.

(TSXV:TNC)

Largest Walk-in Bill Payments Processor in N.A.

Company Description

TIO Networks Corp. (“TIO”) is a Vancouver-based technology company, which

provides bill payment processing options for the financially underserved consumer

market group. The Company services some of the largest telecom, wireless, utility

and cable bill issuers in North America (such as AT&T, Verizon Wireless, COX,

Dish, Duke Energy, and more), providing four unique bill payment channels via:

kiosks, point-of-sale (POS), online, and mobile.

Investment Highlights

• Softgate acquisition close created the largest walk-in bill payment

processing company in NorthAmerica. The highly accretive acquisition puts

TIO on a CAD$105 million revenue run rate, with a combined processing

power of 80 million transactions annually.

• TIO now services more than 10,000 billers (including AT&T, Cricket

Wireless, T-Mobile, Verizon, Dish Networks, etc.), and has approximately

70,000 bill payable locations (including convenience stores, grocery stores,

wireless agents, and financial service locations). This access to a large number

of billers complemented by a multi-channel bill payment network is what

gives TIO a strong competitive advantage over industry incumbents.

• The financially underserved market segments accounts for $138 billion

in fees and interest collected in 2014. There are 34.4 million unbanked and

underbanked households in the U.S., making about 172 - 275 million bill

payments per month. TIO has much room for growth, given their 2.4 – 3.9%

market penetration.

• Additional growth, outside of M&Aactivity, will likely occur from expansions

into other product categories. We believe that TIO may have opportunities

for growth by offering short-term lending as well as reloadable prepaid

cards to its consumer base.

Financial Analysis & Valuation

TIO generates 95% of its revenues from transaction fees. Transaction volume has

been steadily on the rise, showing organic growth of 3-5%, as well as inorganic

growth of roughly 24 million additional transactional volume arising from the

Softgate acquisition alone. The Company has doubled its gross profit margin over

the last two years. Valuation wise, comparable companies within the payment

processing industry are currently trading at 1.8x 2016 sales, which is in line with

TIO’s 1.8x sales run rate (post Softgate integration).

-

200

400

600

800

1,000

1,200

1,400

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16

DailyVolume(thousands)

2. Ubika Research

Page 2 - July 19, 2016

Table of Contents

Investment Thesis .................................................................................................................................................. 3

Leading Walk-in Bill Payment Processor in North America ................................................................................................................ 3

Strong Recurring Revenues Built from a Robust Group of Blue-Chip Customers .............................................................................. 3

1 in 4 Americans are Financially Underserved ...................................................................................................................................... 3

Strong Barriers to Entry and Competitive Advantages Protect TIO ..................................................................................................... 4

Future Growth to come from Product Expansion ................................................................................................................................. 4

The Company ......................................................................................................................................................... 5

Financial markets in the U.S. are very different than in Canada ........................................................................................................... 6

String of Accretive Acquisitions Add on to Core Business ................................................................................................................... 7

Competition ............................................................................................................................................................................................ 9

Other Product Areas – Low Hanging Fruit for TIO ............................................................................................................................. 10

Financial Underserved – Industry Overview .................................................................................................... 11

Reasoning the Refusal to Bank ............................................................................................................................................................ 11

Demographic Analysis and Trends ...................................................................................................................................................... 12

Current minorities are more suitable to use AFS ........................................................................................................................... 12

Millennials continue to disrupt conventional banking ideals ......................................................................................................... 13

Strong correlation between (financial) education & use of banks ................................................................................................. 13

Geographical Look Shows Optimal TIO Positioning .......................................................................................................................... 14

There is a Prominent Shift to Mobile Financial Tech .......................................................................................................................... 15

Forecasts and Valuation ...................................................................................................................................... 16

Transactional Volume/Revenue ............................................................................................................................................................ 16

Operating Margins ............................................................................................................................................................................... 16

Comparables ........................................................................................................................................................................................ 17

Risks ...................................................................................................................................................................... 18

TIO’s Inability to Capture Additional Biller Relationships ................................................................................................................. 18

Rise in Financial Technology Companies Negatively Affecting TIO’s Mobile Expansion Plans ....................................................... 18

Conclusion ............................................................................................................................................................ 18

Appendix A: Recent News .................................................................................................................................. 19

Appendix B: Management & Board of Directors ............................................................................................. 20

TIO Networks Corp.

3. Investment Thesis

Leading Walk-in Bill Payment Processor in North America

The Company is an established leader in providing a multi-channel network of bill payment

options to the unbanked and underbanked consumer population. The Company offers

consumers the ability to pay their bills individually (via kiosks, mobile or online), or at a clerk-

serviced location (via a POS terminal). Consumers are able to pay their bills through a network

of 69,000 locations (via established location partners including grocery stores, convenience

stores, financial service locations, and wireless agents). This scale has given TIO a huge

competitive advantage over industry incumbents and potential new entrants.

However, even with TIO’s large scale, there is still a lot of room for growth. There are 34.4

million unbanked and underbanked households in the U.S. An average household needs to

pay anywhere from 5 to 8 bills a month. This brings the market to roughly 172 - 275 million

bill payments per month, whereas TIO currently only processes 6.7 million, or roughly a

2.4 – 3.9% market penetration.

Strong Recurring Revenues Built from a Robust Group of Blue-Chip Customers

Everyone pays bills. Even if you don’t have a bank account, you still need to pay your phone,

gas, utilities, and other appliances. This requirement to pay these essential bills is what makes

the bill payments industry so attractive for payment processors. Bill payment processors can

reasonably expect payers to keep making monthly bill payments for prolonged periods of time.

TIO, over the years, has accumulated an impressive list of large national service providers

which are currently using its bill payments platform. Its payment network now supports

well over 10,000 billers throughout the U.S., including some of the largest wireless carriers

(AT&T, Verizon Wireless, T Mobile and Sprint), TV operators (COX, Dish, CenturyLink and

DIRECTV), utility providers (Duke Energy, MLGW, CPS Energy, and FPL) as well as other

large billers.

1 in 4 Americans are Financially Underserved

Financially underserved U.S. consumers spent approximately $138 billion in fees and interest

to access financial products and services in 2014. This may come as a surprise to many, but

20-25% of U.S. households are unbanked (do not have a bank account) or underbanked (have

a bank account yet still rely on alternative financial services). U.S. consumers are noted to be

financially underserved due to illegibility issues such as not having enough cash to support a

bank account, as well as a result of their own choosing due to a customer’s distrust of banks.

The financially underserved market trait is something that is unique to the American market.

There are over 5,000 different commercial banks in the U.S., created due to the numerous

regions, states, and counties abiding by individual regional or state laws. Due to the sheer

number of banks, consumers are often refused access to a bank account due to the bank not

willing to service a small account (under US$1,000 account balance). The situation is different

in Canada, as the nation is dominated by the 5 large commercial banks.

The $138 billion in fees collected from this financially-underserved market is an increase of

8% from 2013, and is estimated to expand 7% in 2015, reaching $147 billion. Payments, the

subcategory in which TIO competes, generated $10.1 billion in fees and interest.

Page 3 - July 19, 2016

Ubika Research TIO Networks Corp.

4. Strong Barriers to Entry and Competitive Advantages Protect TIO

TIO integrates its transaction processing software with each biller’s back-office accounting,

which creates a sticky biller relationship. Additionally, it is the access to many billing clients

that puts TIO ahead of its competition. This access to billers combined with high barriers to

entry and high biller switching costs, has created a competitive advantage for the Company.

Future Growth to come from Product Expansion

TIO’s future growth will be a function of gaining additional transactional volume within the

bill payments space, in addition to trying to expand into other product categories. One of those

categories we feel that fits synergistically with TIO’s business is consumer loan origination.

The underserved consumer market is a combination of various sources of fee and interest

revenues from services such as: short/long term loans, remittance, overdraft, money orders,

prepaid cards and others. We believe that the structure of TIO’s operating business (collecting

funds from customers to settle future bill payments), has created a material asset (and liability)

account, which can be strategically used for short-term lending purposes. TIO’s largest asset on

the books is “Funds held to settle bill payments/money order obligations”, at $100.5 million.

A monthly compounding interest rates of 0.5 - 1% on these funds, would translate to an

additional $6 - 13 million in interest fees.

Page 4 - July 19, 2016

Ubika Research TIO Networks Corp.

5. The Company

TIO Networks is a Vancouver-based company, focused on developing its proprietary payment

processing technology. The Company specifically caters its payment processing technology

to handle bill payments (such as electricity, hydro, TV, and other bills), with a distinct focus

on the financially underserved consumer market group in the United States. The Company

services some of the largest telecom, wireless, utility and cable bill issuers in North America

(such as AT&T, Verizon Wireless, T Mobile, Dish, Duke Energy, and other).

The Company has had a long history dating back to its founding year of 1997, at which point

it was called Info Touch Technologies. Its focus at the time was to manufacture and sell

kiosks, which provided Internet access at various public places such as cafes. In 2006, the

Company rebranded into TIO Networks Corp. and transitioned its kiosks business model into

a network of bill payment processing machines. Throughout eventual growth and strategic

business acquisitions, the Company became a leader in providing multi-channel bill payment

options for the financially-underserved consumer.

Page 5 - July 19, 2016

Ubika Research

Figure 1: TIO Networks Corp. logo, and TIO kiosk

Source: Ubika Research, corporate office visit (06/07/2016)

TIO Networks Corp.

6. Page 6 - July 19, 2016

Figure 2: TIO’s Bill Payment Options

Source: Corporate website

Ubika Research

Financial markets in the U.S. are very different than in Canada

There are over 5,200 commercial banks in the United States, as well as over 6,000 credit

unions. This is very different than Canada, which holds only 28 domestic banks (and is

mostly dominated by the big 5 – BMO, CIBC, RBC, Scotiabank, TD). Due to the size

difference of large banks vs small regional banks in the U.S., more scrutiny is placed over

accepting a customer as a banking client. Small U.S. banks are more likely to turn down an

applicant due to various reasons, some of which include having a small account balance. Due

to this, a lot of households in the U.S. are unbanked or underbanked.

One in 13 (or 7.7%) of U.S. households were unbanked in 2013. This represents nearly 9.6

million households comprised of approximately 16.7 million adults and 8.7 million children.

An additional 20.0% of U.S. households were underbanked in 2013, representing 24.8

million households comprised of approximately 50.9 million adults and 16.6 million children.

Ultimately, whether you have a bank account or not, you still need to pay your bills. If you

are a banked client, paying bills is as simple as adding a “payee” account, and entering your

bill payment information. The payment is then routed by the financial institution to the biller.

However, if you’re planning to pay your bills in cash, the operation becomes a little more

complicated – which is where TIO comes in. Its multi-channel approach to bill payments

gives the customer four bill payment options: via kiosks, clerk-assisted point-of-sale (POS)

machines, mobile, or on the Web.

TIO Networks Corp.

7. Ubika Research

Page 7 - July 19, 2016

String of Accretive Acquisitions Add on to Core Business

Prior to going on an acquisition spree, TIO’s business was heavily reliant on a few key

billers. Specifically, the Company’s two largest billers used to account for over 50% of TIO’s

business. Acquisitions have helped diversify the client base, with the combined revenue from

the Company’s top two billers accounting for 20% post-Softgate integration.

The string of several highly successful business acquisitions began in 2014, and has since

constructed TIO a very strong network of billers and payment locations for customers. The

Company services more than 10,000 billers (including AT&T, Cricket Wireless, T-Mobile,

Verizon, Dish Networks, etc.), and has over 70,000 bill payable locations (including

convenience stores, grocery stores, wireless agents, and financial service locations). The

access to a large number of billers complemented by a multi-channel bill payment network is

what we believe gives TIO a strong competitive advantage over industry incumbents.

Figure 3: TIO Networks’ National Footprint

Source: Company Filings

Thus far, they have made three deals, which we attribute largely to management’s competence

of capital markets and alignment with shareholder interests:

TIO Networks Corp.

8. Page 8 - July 19, 2016

Ubika Research

1. Global Express was acquired in January 2014 for US$8 million. The deal was financed

through $2.2 million in cash, $3.0 million in debt, and $2.8 million in shares. The value

proposition through this deal came from expansion of big-name billers. This payment

system provided TIO with exposure to the utility billers segment (Duke Energy, Florida

Power & Light, Baltimore Gas and Electric, etc.). Global Express expanded TIO’s

footprint across the mid-Atlantic and Southeast states. Revenue synergies were created

through cross selling initiatives with the core TIO business.

2. ChargeSmart was acquired in August 2014 for US$2 million in cash. The San Francisco-

based company belonged to giant financial services provider – VeriFone Systems at the

time. We believe this deal exemplifies management’s ability to proactively anticipate future

trends. ChargeSmart was (and remains) a leading provider of online bill payment services,

a business model that runs off the online-payment trend that is booming across the globe.

In addition, margins on the online segment are (as to be expected) significantly higher.

The segment has been rebranded to tio.com and represented 10% of revenues in FY15.

Management is expecting the segment to represent ~12% of revenue in FY16, and a drop

to ~6% in FY2017 due to more revenue contributions through Softgate.

3. Softgate Systems acquisition was closed in April 2016 for US$31 million. The deal was

financed through $4.6 million cash, $4.1 million in debt, and 25 million shares (based on

$0.91/share of TIO) to Softgate shareholders (private). Silicon Valley Bank provided a

secured loan of $5.7 million with interest at 5% annually, repayable after 5 years. Note that

there were no warrants or other “sweeteners” as part of the deal.

As its largest acquisition to date, New Jersey-based Softgate will benefit TIO in several

ways:

• Perhaps most importantly, Softgate will provide significant scale to the business

through its additional 24 million in annual transactions, $37 million in revenue and $5

million in forecasted EBITDA contributions to TIO. Softgate has a portfolio of ~9,000

billers in different industries.

• Softgate also contributes ~21,000 locations across the U.S. The locations are heavily

based in the Northeast, a populous which TIO had not been exposed prior to the

acquisition.

• Softgate has 46 money services business (MSB) licenses in order to provide money

transmitter services throughout the U.S.

• Softgate operated at a net loss in the years prior to CY2014. As such, TIO will benefit

from offsetting taxable income with the US$31 million in accumulated net operating

losses. Concurrently, this will make TIO more profitable in the short term.

• Both revenue and cost synergies will be inherently present in the upcoming quarters as

the integration ramps up. On the revenue side: cross selling of products and services

into Softgate’s billing base. From a cost perspective, synergies will be created through

consolidated hosting activities, workforce reduction, and savings through consolidation

of operating expenses.

TIO Networks Corp.

9. Page 9 - July 19, 2016

Ubika Research

Competition

With the addition of Softgate, TIO will now be processing roughly 80 million transactions

annually. Although this figure may seem enormous, it only accounts for roughly 2 - 4% of bill

payment volume originating from the financially underserved market segment. We would like

to find out who owns the other 96% of the transactional volume.

Some of the more direct competitors to TIO would include companies that offer walk-in bill

payment processing to clients within the U.S. Throughout our research we have found these to

be the closest competitor matches:

1. ChechFreePay (owned by Fiserv (NASDAQ:FISV))

CheckFreePay is a direct competitor to TIO, as they are a walk-in bill payment processor.

With an operating history of over 20 years, the company boasts having over 1,000 biller

relationships as well as a network of 25,000 bill payment walk-in locations. Additionally,

the platform also has same-day payment delivery.

2. Western Union (NYSE:WU)

Western Union is mostly known for its money transmitting business line, where individuals

send money to friends and family in all parts of the world. This business line accounts for

roughly 80% of Western Union’s revenues. However, consumer-to-consumer is not its only

line of business, as the company also offers walk-in bill payment services. Given that the

company has 500k+ agent locations globally (50k in the U.S.) capable of accepting bill

payments, we view Western Union as a large competitor to TIO.

3. PreCash (private)

PreCash is a payment processing platform that delivers payments to an ever-growing

universe of billers. This proprietary platform offers same-day delivery to billers covering

all major billing and invoicing categories, including utilities, cable, satellite, telecom,

insurance and more. PreCash has more than 35,000 convenient retail locations in the U.S.

4. InComm Agent Solutions

InComm creates POS-based payment processing solutions. Its slew of services include

activating prepaid products, paying bills, enjoying real-time discounts through a

membership card, purchasing digital goods in-store or adding funds to an online account.

The company boasts over 255k retail locations where consumers can make bill payments,

as well as over 11,000 retail partners - both staggering statistics. InComm manages more

than 9 million transactions a month.

5. Prepaid Cards: Blackhawk (NASDAQ:HAWK) & GreenDot (NYSE:GDOT)

We view prepaid cards as a major alternative to walk-in bill payments. In contrast to

walking up to a clerk-assisted POS terminal to make a bill payment, a customer can

purchase a prepaid card, load it up with funds, and thereafter make bill payments online

using this card. A couple names operating within the space are Blackhawk Networks

and GreenDot Corp. Prepaid cards are all able to be recharged at specific retailers (and

convenience stores) using cash.

TIO Networks Corp.

10. Page 10 - July 19, 2016

Ubika Research

Other Product Areas – Low Hanging Fruit for TIO

Although TIO’s main business competency is bill payments, future growth will occur as

TIO enters other product categories. At this stage, we believe that the Company has reached

a point where it can leverage its current client base, and provide additional services to the

financially underserved.

Based on CFSI’s 2014 Underserved Market Size report, short term lending accounts for

21% of overall fees, and is one of the highest growing product groups, growing 37% since

2012. We believe that short-term lending is a service in which TIO may offer to its large

network of bill payers. This product area fits synergistically to TIO’s current business model

via its “Funds held to settle bill payment obligations” asset account.

Given TIO’s business model of collecting payments from bill payers, and concurrently

paying for the respective bills in due time – this lag creates a short-term asset account that

amounts to a substantial monetary figure. In the latest financial statements, TIO reported a

$100.5 million asset figure, which could concurrently be leveraged to provide short-term

lending. This is the exact same model as what banks use when taking deposits and lending

out a large percentage of it.

Figure 4: Other Product Areas within Payment Processing

Source: Ubika Research

Another product category that may work synergistically with TIO is providing reloadable

prepaid cards to its network of bill payers. These reloadable prepaid cards would then

be offered at TIO’s 69,000 walk-in bill payment locations, acting as an up-sell during a

customer’s visit.

TIO Networks Corp.

11. Financial Underserved – Industry Overview

Unbeknownst to many, a significant portion of the U.S. population does not transact with

insured large banks. This group is deemed as “unbanked.” Similarly, there are also households

that do have a bank account, but also obtain financial services from alternative service

providers. These consumers are known to be “underbanked,” or “unhappily banked.”

This may come as a surprise to the Canadian population, but this unbanked and underbanked

market consists of roughly 35 million households across the U.S., representing 20 - 25% of the

population. Combined, fees and interest income earned from this market was a staggering $138

billion in 2014, as researched by the Center for Financial Services Innovation (CFSI). The

market displayed a CAGR of 6.4% (2010 – 2014) and is estimated to grow an additional 6.8%

in 2015 to reach $147 billion.

TIO’s operations focus precisely on this financially underserved consumer market group.

Page 11 - July 19, 2016

Ubika Research

Figure 5: Financially Underserved Market – Distribution by Product Group

Source: Center for Financial Services Innovation (CFSI)

Reasoning the Refusal to Bank

According to the 2013 FDIC National Survey, 58% of respondents stated that they are

unbanked because they do not have enough money, 34% stated that they don’t like dealing

with banks and don’t trust them, and 31% stated that account and service fees are too high.

TIO Networks Corp.

12. Page 12 - July 19, 2016

Ubika Research

Figure 6: Reasons Households are Unbanked

Source: FDIC

From this data, we have a better understanding of the unbanked and underbanked market

in the U.S., and furthermore, to the reasons why 7.7% of the household population chooses

not to bank at all. At this point, it is also worth noting that the proportion sizes have stayed

relatively stagnant throughout the years (in particular 2011 - 2013) for the percent of

unbanked households. We assume throughout the report that the proportions remain relatively

the same.

Demographic Analysis and Trends

From our understanding, there are specific demographics that make up the majority of the

underbanked or unbanked population in the U.S. In particular, we have noted the following

demographics and their trends that are associated with the market:

Current minorities are more suitable to use AFS

Minorities in the U.S. have a higher propensity to use AFS. From our understanding, this

is due to many reasons. Primarily, we see a greater distrust of banks abroad, and when

minorities immigrate to the U.S., these feelings of bank distrust are also brought over.

TIO Networks Corp.

13. Page 13 - July 19, 2016

Ubika Research

Figure 7: Households that Use AFS in Last 12 Months

Source: FDIC, Ubika Research

Millennials continue to disrupt conventional banking ideals

About 31% of the underbanked or unbanked consumers in the U.S. were under 34, compared

to only 18% of the fully banked being under 34. Indeed, millennials continue to pose a

growing challenge to banks. Compared to the entire population, they are twice as likely to not

hold bank accounts or credit cards. Accenture’s 2014 Survey on millennials also found that

41% prefer AFS compared to just 27% of the general population.

A scratch survey of 10,000 millennials found that all 4 of the leading banks are among the 10

least-loved brands by the group. A key reason for this trend, we believe, is due to the digital

savviness of the millennials. They are becoming more and more likely to use and hold their

cash in tech financial providers (i.e. Google, Apple, PayPal, Square, etc.) instead of banks.

In any case, a significant portion of growth that the unbanked and underbanked markets are

experiencing can be represented by millennials.

Strong correlation between (financial) education & use of banks

It is important to be cognizant of the fact that AFS’ fees are often several times greater

than the standard bank transaction fees. However, as noted above, we find lower-income

households more in favor of AFS than their higher-income counterparts. We attribute this

strange phenomenon to a lack of financial education.

According to S&P’s Global Financial Literacy Survey, only 57% of Americans are financially

literate (i.e. can pass a simple 5-question test on topics like diversification, compounding,

interest and inflation). This is a relatively low rating when compared to Northern Europe’s

~70% figure. Furthermore, there is a negative correlation between states with lower

financial education mandates and their populous’ propensity to use AFS and be unbanked or

underbanked.

In addition, immigration trends continue to witness positive growth: Migration Policy

Institute shows that the immigrant share of the total U.S. population is still rising (currently at

13.3%). Combining that fact with the much lower financial literacy scores of key immigrant

nations (namely Mexico, China, and India with 32%, 28%, and 24% of adult population

being financially literate, respectively), we can imply that this outlines a higher share of

financially illiterate residents, and thus a growing demand for AFS in the years to come.

TIO Networks Corp.

14. Page 14 - July 19, 2016

Ubika Research

Geographical Look Shows Optimal TIO Positioning

TIO’s network itself is also well established to harbour the states and localities in the U.S. with

the most unbanked populace. As seen from Figure 9 below, The Southern/South-Western most

states are more likely to be unbanked. This is largely due to the different demographics in these

states, in which TIO has strategically positioned its assets and services. Specifically, the two

largest economies in the U.S. (and populations) have relatively high unbanked rates: California

and Texas. In these states, the population proportion of Hispanics is greater than 35%. Figure

3 (pg. 7) shows that TIO has joint coverage in these two powerhouse states, giving us further

reassurance in management’s geographic positioning acumen.

Figure 8: Unbanked Population Proportion based on Education Status

Source: FDIC, Ubika Research

Figure 9: Unbanked Rates by State, 2013

Source: FDIC, Ubika Research

TIO Networks Corp.

15. Page 15 - July 19, 2016

Ubika Research

There is a Prominent Shift to Mobile Financial Tech

On one front, mobile banking continues to revolutionize the sector, with more than one

fourth of all households using smartphones to bank. Perhaps not intuitively, the underbanked

households are actually more likely to have access to smartphones and use them to engage in

transactions. The FDCI reports that the underbanked households are more likely to use mobile

devices as primary methods of banking, as roughly 65% of the households have access to

a mobile device. It is the unbanked ones that have a substantially lower rate of smartphone

access: 33% (compared to those fully banked at 59%).

This brings us to believe that the unbanked population would much rather rely on mobile

technology, as opposed to dealing with a bank, if they have enough funds to pay for a mobile

smartphone.

TIO has repeatedly made strides to take full advantage of the mobile trends. Its online platform

(tio.com) is mobile-friendly and will likely contribute a rising share of revenue throughout the

years. Management has estimated the website’s proportion of revenue to be ~12% for FY16.

TIO Networks Corp.

16. Page 16 - July 19, 2016

Ubika Research

Forecasts and Valuation

Transactional Volume/Revenue

The Company runs a lean business model, generating roughly 95% of revenue from

transactions. As a bill payment processing operator, the number of transactions indicates the

amount of revenue collected, hence being a business driver. We would like to direct your

attention to the graphical representation of the Company’s transactions against the dollar value

collected per transaction.

Figure 10: Transactions on the Rise, Organic Revenue Growth in Mid Single Digits

Source: Ubika Research, Company Financials

The drop in revenue/transaction can be attributed to a change in revenue recognition from

one of the Company’s largest billers – Cricket Wireless. Following AT&T’s acquisition of

Cricket Wireless in 2014, revenue recognition switched from a front-end to a back-end model.

Effectively, revenue per transaction decreased, while keeping gross profit per transaction

unaffected. This for obvious reasons had good and bad interpretations: (good) being that

overall profit margins look to be increasing, while (bad) being that revenues look to be

decreasing. In our opinion, this has no fundamental impact on the business.

We are forecasting a modest 3.0% growth in transactional growth for the rest of 2016 (in line

with 3.5% growth in 2014 – 2015), falling to 2.0% in 2017. We are also forecasting Softgate

revenue to fully integrate with the rest of TIO’s business by Q4/2016, and to see growth of

6.0% and 3.0% for 2016 and 2017, respectively (conservative compared to Softgate’s 18%

growth in 2014).

Operating Margins

Operationally, TIO has been able to double its gross profits over the past two years, raising its

GP margin from 25% at the beginning on 2014, to over 50% in the latest quarter.

We can attribute some of this profitability to the Company’s scale arising from its transactional

volume. TIO appears to gain from economies of scales, and given that it is currently going

through the Softgate business integrations, we can expect to see further margin improvement.

-40%

-20%

0%

20%

40%

60%

80%

100%

120%

140%

160%

-

5

10

15

20

25

Millions

Number of Transactions Revenue Growth %:

TIO Networks Corp.

17. Page 17 - July 19, 2016

Ubika Research

Figure 11: Operating Margins

Source: Ubika Research

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

G&A %: R&D %: Sales and Marketing %:

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

GP%

Operating expenses have mostly been in line with revenue growth. As a percentage of

revenues, general and administrative (G&A) expenses have trended around the 22% mark. For

most part, this trend makes intuitive sense. As the Company scales its transactional volume,

it will require additional manpower and development work to keep up with rising demands,

although the additional expenses should be marginally decreasing.

Additionally, research and development (R&D) as well as sales and marketing costs have

trended around 5 - 7% of revenue.

Comparables

We recognize that valuing TIO is a significantly hard task, considering that the Company

is structured for both organic and inorganic growth. Speculating on future acquisitions is

not ideal, therefore our estimates only account organic business growth, with the addition

of Softgate revenues starting in Q4/2016. As well, since the Company is still scaling its bill

payment business, operating margins have not reached a desired level. Therefore, we believe

that a forward revenue multiple for a software/IT Company is well fitted.

In selection of our comps universe, we gave preference to North American listed companies,

with a market cap of between $50 and $600 million.

Figure 12: Comparable Companies within Payment Processing

Source: Ubika Research

TIO Networks Corp.

18. Risks

TIO’s Inability to Capture Additional Biller Relationships

TIO operates in a space where processor-biller relationships are very sticky. Due to the back

office software integration, it would seem that acquiring biller relationships from competitors

might only result from complete competitor acquisitions. Attaining clients organically may be

a timely process, with slow sales cycles.

Rise in Financial Technology Companies Negatively Affecting TIO’s Mobile

Expansion Plans

Financial technologies are revolutionizing the way clients interact with their financial

providers. Although not directly associated to TIO, IOU Financial is a great example of this

change. As opposed to businesses/consumers needing to go through the regular one-month

procedure of securing a loan via a bank, these clients may now fill out a form online, and have

funds transferred to them within 24 hours.

Conclusion

TIO Networks has come a long way since its inception in 1997 as a kiosk solution provider.

Hamed Shahbazi has since transitioned TIO into a multi-channel payment solution provider

specializing in bill payment through a variety of automated self-serve, retail point-of-sale,

mobile and web-based methodologies, processing approximately 80 million transactions worth

roughly $9 billion in payments annually in the United States.

The Company’s acquisitive strategy has propelled TIO to become one of the largest walk-in

bill payment processing companies in North America. However, the Company still has much

room for growth, considering its 2 - 4% market penetration. Additional future growth will also

occur outside bill payments, and in other promising product areas.

Page 18 - July 19, 2016

Ubika Research TIO Networks Corp.

19. Appendix A: Recent News

TIO Reports Record Quarterly Revenue and Year to Date Net Profit

Company reports the 5th

consecutive quarter of record adjusted EBITDA. Third quarter net

income increased to $1.6M. Nine month net income increased to $4.67M or $0.08 EPS.

Quarterly Adjusted EBITDA increased 188% (Y/Y) to $2.9M from $1.0M and increased

sequentially on a quarter over quarter (Q/Q) basis by 8.5% from Q2 2016.

TIO Networks to Present at the LD Micro Invitational

Hamed Shahbazi, Chairman and CEO will be giving the presentation and meeting with

investors. LD Micro was founded in 2006 with the sole purpose of being an independent

resource in the micro-cap space.

Chargesmart.com Rebrands as TIO.com, Becoming TIO’s Direct-to-Consumer

Destination

Company announced the launch of TIO.com, a mobile optimized web portal where

consumers can pay bills in less than a minute from any Internet enabled device. TIO.com

offers access to over 9,000 common U.S. household and consumer bills, ranging from utility,

telecom, auto, mortgage, cable, satellite, and much more.

TIO Networks Closes Acquisition of Softgate Systems Inc.

The acquisition creates the largest North American provider of walk-in bill payment services

with a pro-forma revenue run-rate of over CAD$105 million. Acquisition is highly accretive

driving additional USD$37 million in revenue and USD$5 million in EBITDA.

TIO Network Announces Closing of CAD$5 Million Bought Deal Private Placement

TIO Networks Corp. reported that it has closed its previously announced bought deal private

placement of 2,726,214 common shares of TIO, including the partial exercise of the over-

allotment option, at an issue price of $1.88 per Common Share, for aggregate gross proceeds

to TIO of $5,125,282.32.

Page 19 - July 19, 2016

Ubika Research

May 17, 2016

June 1, 2016

June 28, 2016

April 25, 2016

February 1, 2016

TIO Networks Corp.

20. Appendix B: Management & Board of Directors

Hamed Shahbazi, Chairman and CEO

Mr. Hamed Shahbazi founded TIO Networks as a kiosk solution provider in 1997. Mr.

Shahbazi has since transitioned TIO Networks into a multi-channel payment solution

provider specializing in bill payment.

The Cantech Letter named Mr. Shahbazi the TSX Venture Tech Executive of the Year and

TIO Networks the TSX Venture Tech Stock of the Year for both 2014 and 2015. In 2013,

KIOSK.COM recognized Hamed with the Hall of Fame award for his “distinguished service”

to the kiosk industry. Business in Vancouver Magazine also named Mr. Shahbazi one of the

prestigious 40 Under 40 in 2001.

Hamed is a passionate advocate of impact entrepreneurship where new companies aim to

doing well by doing good, which he promotes as the role of an “Impactreneur”. He regularly

mentors founders and entrepreneurs of early stage companies.

Chris Ericksen, Chief Revenue Officer

Mr. Ericksen has been with TIO for over 14 years, and is currently responsible for TIO

Networks’ enterprise business planning as well as organic growth strategy and execution.

Previous to this position, Mr. Ericksen was the EVP of POS Solutions, leading TIO’s point-

of-sale business unit.

Richard Cheung, CFO

Mr. Cheung is currently responsible for TIO Networks’ finance, administrative operations

and public company matters. Previously, Mr. Cheung was formerly the VP of business

development at FuseMail (subsidiary of j2 Global, Inc.), and was responsible for M&A and

all financial and operational matters.

Hessam Shahbazi, Executive VP, Independent Service Operators (“ISO”)

Hessam Shahbazi assists in the foundation and development of TIO’s sales growth, as well

as overseeing the direction of the sales team, lead generation along with strategic operational

issues.

Page 20 - July 19, 2016

Ubika Research TIO Networks Corp.

21. Disclosures

Copyright

This report may not be reproduced in whole or in part, or further distributed or published or referred to in any manner whatsoever, nor may the information,

opinions or conclusions contained in it be referred to without in each case the prior express written consent of Ubika Corporation.

Disclaimer

The Content contained on this page (including any facts, views, opinions, recommendations, description of, or references to, products or securities) made

available by SmallCapPower/Ubika Research is for information purposes only and is not tailored to the needs or circumstances of any particular person. Any

mention of a particular security is merely a general discussion of the merits and risks associated there with and is not to be used or construed as an offer to sell,

a solicitation of an offer to buy, or an endorsement, recommendation, or sponsorship of any entity or security by SmallCapPower/Ubika Research. The Reader

should apply his/her own judgment in making any use of any Content, including, without limitation, the use of any information contained therein as the basis

for any conclusions. The Reader bears responsibility for his/her own investment research and decisions. Before making any investment decision, it is strongly

recommended that you seek outside advice from a qualified investment advisor. SmallCapPower/Ubika Research does not provide or guarantee any financial,

legal, tax, or accounting advice or advice regarding the suitability, profitability, or potential value of any particular investment, security, or information source.

Ubika and/or its affiliates and/or their respective officers, directors or employees may from time to time acquire, hold or sell securities and/or commodities

and/or commodity futures contracts in certain underlying companies mentioned in this site and which may also be clients of Ubika’s affiliates. In such

instances, Ubika and/or its affiliates and/or their respective officers, directors or employees will use all reasonable efforts to avoid engaging in activities that

would lead to conflicts of interest and Ubika and/or its affiliates will use all reasonable efforts to comply with conflicts of interest disclosures and regulations

to minimize the conflict.

Safe Harbour Statement for US Residents/ Investors

The information set forth in this report may contain “forward-looking statements.” Statements in the report, which are not purely historical, are forward-

looking and include statements regarding beliefs, plans, expectations or intentions regarding the future.

Except for the historical information presented herein, matters discussed in this document contain forward-looking statements that are subject to certain

risks and uncertainties that could cause actual results to differ materially from any future results, performance or achievements expressed or implied by such

statements. There can be no assurance that the highlighted company’s efforts will succeed and the company will ultimately achieve sustained commercial

success. These forward-looking statements are made as of the date of this document, and neither Ubika Corporation nor the highlighted company assumes

any obligation to update the forward-looking statements, or to update the reasons why actual results could differ from those projected in the forward-looking

statements.

The forward looking statements contained in the document have been prepared by management of the highlighted company who believe and have so advised

Ubika Corporation, without independent verification by Ubika Corporation that a reasonable basis exists for making such statements.

Analyst’s Comments

The analyst was given the opportunity to travel to the Company’s head office on June 7th

, 2016. All accommodations were paid by Gravitas. No part of the

Analyst’s compensation was, is, or will be, directly or indirectly, related to the recommendations or views expressed in this research report.

Investor Quick Links

• Investing Newsletter on www.smallcappower.com

• Visit us at www.ubikaresearch.com for more details of our offering

• Reach us at info@ubikacorp.com for any questions or comments

333 Bay Street, Suite #1700

Bay-Adelaide Centre

Toronto, ON, Canada, M5H 2R2