UXPA Boston 2024 Maximize the Client Consultant Relationship.pdf

Project on lupin pharmaceutical(3) (1)

1. 1

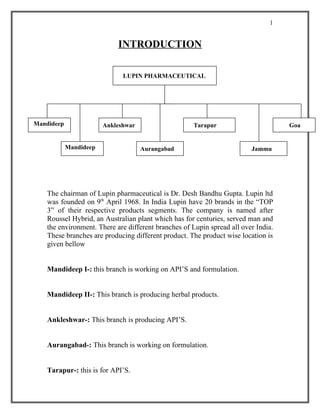

INTRODUCTION

LUPIN PHARMACEUTICAL

Mandideep Ankleshwar Tarapur Goa

Mandideep Aurangabad Jammu

The chairman of Lupin pharmaceutical is Dr. Desh Bandhu Gupta. Lupin ltd

was founded on 9th April 1968. In India Lupin have 20 brands in the “TOP

3” of their respective products segments. The company is named after

Roussel Hybrid, an Australian plant which has for centuries, served man and

the environment. There are different branches of Lupin spread all over India.

These branches are producing different product. The product wise location is

given bellow

Mandideep I-: this branch is working on API’S and formulation.

Mandideep II-: This branch is producing herbal products.

Ankleshwar-: This branch is producing API’S.

Aurangabad-: This branch is working on formulation.

Tarapur-: this is for API’S.

2. 2

Jammu-: This branch is for formulation.

Goa-: This is producing Non Cephalosporin Dosage forms.

API’S-: This is the active pharmaceutical ingredient. This is in the form of

powder and this is generally using in the formulation of medicine. It is the

kind of production.

FORMULATION -: This is production of capsules, tablets and syrup with

the help of API’S. A branch which is producing API’S will send this for

formulation.

In India Lupin have 20 brands in the “TOP 3” of their respective

products segments. Global leader in anti-tuberculosis products and

cephalosporin. Lupin products sold in over 70 countries.

When it comes to reliability and quality, Lupin’s name is amongst in

the mind of specialists. More and more specialists such as chest physicians,

consulting physicians, general surgeons, pediatricians, cardiologists and

diabetologists are choosing its products everyday. Despite the fact that the

Indian urban prescription market showed stagnation with only 0.1% of

growth, Lupin has bucked the trend by recording a strong growth of 8.2%

during the year.

AAMLA (Asia, Africa, Middle East & Latin America)-:

In its pursuit to be an innovation led translation pharmaceutical company,

Lupin has ventured penetrated into chosen markets represented by its

AAMLA division. The AAMLA geographic provide unique challenge and

opportunity. On one hand, there are highly regulated markets such as

Japan, Australia, South Korea, Mexico, U.A.E., Saudi Arabia etc. while,

on the there, there are less regulated markets such as Myanmar, Nigeria,

Kenya and Peru.

3. 3

1200

1000

800

600

400

200

0

2002-03 2003-04 2004-05 2005-06

sales (rs. in million)

INDIA PHARMACEUTICAL MARKET-

Today, the pharmaceutical industry in India is estimated to be over a

US $5 billion. 2005 marked the beginning of an era in the Indian

pharmaceutical industry with the introduction product patent regime. The

bill not only provided the confidence to multinational companies to bring in

their research molecule but, it also gave Indian companies reason to focus on

developing brands and exploring in-licensing and marketing alliances. The

Indian pharmaceutical market continued to grow in size, powered by 9%

value and 7%volume growth respectively.

FINANCIAL OVERVIEW-:

In financial year 2005-06, the net sales of the company increased by 38%

from Rs. 11611.3 million to Rs. 16061 million in net profit, a 117% increase

over the previous year’s Rs. 843.6 million. Higher sales volume, especially

in the high value market of US and in formulations in the domestic markets

triggered the higher profitability. These entire factors contributed to the

growth in earning before interest, tax, depreciation and amortization

(EBITDA) by 106%, from Rs. 1457.9 million. During the year EBITDA

constituted 19% of net sales. The company registered strong export sales

constituted 46% of gross sales.

4. 4

3500

3000

2500

2000

1500

1000

500

0

2004-05 2005-06

--EBITDA (Rs, in million)

1- On the strength of the various ANDA’s filled by the company in the

previous year, the company, the company was able to launch 7 new

products in the US, from which sales of Rs. 2233 million were added

to the company’s top line. In particular, Ceftriaxone has been a major

success for the company, for which it now enjoys around 25% market

share. The price drop for the product was about 70% in hospital

market, being less intense, with fewer competitors participating in this

high-end niche generic product.

2- Domestically, the company’s strong performances within the recently

entered Anti-Asthma segment and its overall market penetration of its

multitude of leading products in other therapeutic areas have

generated significant revenues additions.

3- In terms of other product, Lupin has been able to maintain optimal

cost positioning and quality maintenance, the keys to success in this

industry. Despite price drops in various products, the company has

been able to maintain and grow its market share to make strong

margins from these products, contributed to the strong financial

performance of the company.

5. 5

45

40

35

30

25

20

15

10

5

0

2004-05 2005-06

--EPS (Rs. In million)

As a result of these factors, the profit after tax recorded was Rs. 1827.2

million, with cash profits amounting to Rs. 2230.7 million. The earning per

share was Rs. 44.59. The Board recommended a dividend of 65%, absorbing

a sum of Rs. 297.5 million, inclusive of tax on dividend.

8000

7000

6000

5000

4000

3000

2000

1000

0

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06

--API SALES GROWTH

6. 6

FINANCIAL OVERVIEW (2004-05)-:

In financial year 2004-05, the net sales of the company by 4% from

Rs.11192.8 million to Rs.11611.3 million. The net profit after extraordinary

items was Rs.843.6 million as against Rs.987.1 million in the previous year.

The company made a strategic decision to significantly increase investment

in intellectual capital, marketing and R&D. The company witnessed a dip in

margin in its Pen G based API product and faced market uncertainty in the

last quarter owing to the introduction of VAT. These entire factors

contributed to the reduction of the Earning before tax, Depreciation and

Amortization (EBITDA) from Rs.2801.7 million in the previous year to

Rs.1457.9 million.

2500

2000

1500

1000

500

0

2004-05 2005-06

--PBT (Rs. In million)

The company registered strong export sales worth Rs.5619.1 million,

thereby constituting 48% of the net sales. The company expanded its product

pipe line, R&D Company investing substantially higher amount in R&D

(Rs.760.1 million in revenue, Rs.76 million in capex). The R&D expenditure

increased to7.2% of net sales in the previous financial year 2004-05 up from

4.11% in the previous year.

7. 7

90

80

70

60

50

40

30

20

10

0

2004-05 2005-06

--REGULATED MARKETS

-- SEMI REGULATED MARKET

Ratio Analysis: Introduction

A ratio is a quantity that denotes the proportional amount or

magnitude of one quantity relative to another

Ratio Analysis is the most commonly used analysis to judge the

financial strength of a company. A lot of entities like research

houses, investment bankers, financial institutions and investors

make use of this analysis to judge the financial strength of any

company.

Fundamental Analysis has a very broad scope. One aspect looks at the

general (qualitative) factors of a company. The other side considers tangible

and measurable factors (quantitative). This means crunching and analyzing

numbers from the financial statements. If used in conjunction with other

methods, quantitative analysis can produce excellent results.

8. 8

Ratio analysis isn't just comparing different numbers from the balance sheet,

income statement, and cash flow statement. It's comparing the number

against previous years, other companies, the industry, or even the economy

in general. Ratios look at the relationships between individual values and

relate them to how a company has performed in the past, and might perform

in the future.

Financial ratios are calculated from one or more pieces of information from

a company's financial statements. For example, the "gross margin" is the

gross profit from operations divided by the total sales or revenues of a

company, expressed in percentage terms. In isolation, a financial ratio is a

useless piece of information. In context, however, a financial ratio can give a

financial analyst an excellent picture of a company's situation and the trends

that are developing.

A ratio gains utility by comparison to other data and standards. Taking our

example, a gross profit margin for a company of 25% is meaningless by

itself. If we know that this company's competitors have profit margins of

10%, we know that it is more profitable than its industry peers which is quite

favorable. If we also know that the historical trend is upwards, for example

has been increasing steadily for the last few years, this would also be a

favorable sign that management is implementing effective business policies

and strategies.

This analysis makes use of certain ratios to achieve the above-mentioned

purpose. There are certain benchmarks fixed for each ratio and the actual

ones are compared with these benchmarks to judge as to how sound the

company is. The ratios are divided into various categories, which are

mentioned below:

Financial ratio analysis groups the ratios into categories which tell us about

different facets of a company's finances and operations. An overview of

some of the categories of ratios is given below.

• Leverage Ratios which show the extent that debt is used in a

company's capital structure.

• Liquidity Ratios which give a picture of a company's short term

financial situation or solvency.

9. 9

• Operational Ratios which use turnover measures to show how

efficient a company is in its operations and use of assets.

• Profitability Ratios which use margin analysis and show the return

on sales and capital employed.

• Solvency Ratios which give a picture of a company's ability to

generate cash flow and pay it financial obligations.

CLASSIFICATION OF RATIOS

The use of ratio analysis is not confined to financial manager only. There are

different parties interested in the ratio analyses for knowing the financial

position of a firm for different purposes. In vies of various users of ratios,

there are many types of ratio which can be calculated from the information

given in the financial statements. The particular purpose of the user

determines the particular ratios that might be used for financial analysis.

Similarly the interests of the owners and the management also differ. The

shareholders are generally interested in the profitability or dividend position

of a firm while management requires information on almost all the financial

aspects of the firm to enable it to protect the interests of all parties.

RATIOS

(A) (B) (C)

TRADITIONAL FUNCTIONAL CLASSIFICATION SIGNIFICANCE RATIOS

CLASSIFILCATION OR OR

OR

STATEMENT RATIOS CLASSIFICATION ACCORDING TO RATIOS ACCORDING TO

TESTS IMPORTANCE

1. BALANCE SHEET RATIOS

1.LIQUIDITY RAT IOS 1.PRIMARY RATIOS

POSI TION STATEMENT 2.LEVERAGE RATIOS 2.SECONDARY RATIOS

RATIOS 3.ACTIVITY RATIOS

2. PROFIT AND LOSS A/C 4.PROFITABILITY

RATIOS

OR

REVENUE/INCOME

STATEMENT RATIOS

3.COMPOSITE/MIXED RATIOS

OR

INTER STATEMNT RATIOS

10. 10

(A)TRADITIONAL CLASSIFICATION OR STATEMNT

RATIOS

Traditional classification or classification according to statement, from which these

ratios are calculated, is as follows.

TRADITIONAL CLASSIFICATION OR STATEMENT RATIOS

(A) (B)

BALANCE SHEET RATIOS PROFIT AND LOSS A/C RATIOS COMPOSITE/MIXED

OR OR OR

POSITON STATEMENT RATIOS REVENUE/INCOME STATEMENT RATIOS INTER-STATEMENT

RATIOS

1. CURRENT RATIO 1.GROSS PROFIT RATIO 1. STOCK TURNOVER RATIO

2. LIQUID RATIO (ACID TEST 2.OPERATING RATIO 2. DEBTORS TURNOVER

OR QUICK RATIO) 3. OPERATING PROFIT RATIO 3. PAYABLE TURNOVER RATI0

3. ABSOLUTE LIQUIDITY RATIO 4.NET PROFIT RATIO 4. FIXED ASSET

4. DEBT EQUITY RATIO 5.EXPENSE RATIO TURNOVER RATIO

5. PROPRIETORY RATIO 6.INTEREST COVERAGE RATIO 5. RETURN ON EQUITY

6. CAPITAL GEARING RATIO 6. RETURN ON

7. ASSETS-PROPRIETORSHIP SHAREHOLDERS FUNDS

RATIO 7. RETURN ON CAPITAL

8. CAPITAL INVENTORY TO CAPITAL EMPLOYED

WORKING CAPITAL RATIO 8. CAPITAL TURNOVER RATIO

9. RATIO OF CURRENT 9. WORKING CAPITAL

ASSETS TO FIXED ASSETS TURNOVER RATIO.

10. RETURN ON TOTAL

RESOURCES

11. TOTAL ASSETS TURNOVER

EXPLAINATION

1. BALANCE SHEET OR POSITION STATEMENT RATIOS:

Balance sheet ratios deal with the relationship between the two

balance sheet items. Both its items must however, pertain to the same

balance sheet.

2. PROFIT AND LOSS A/C OR REVENUE/INCOME

STATEMENT RATIOS: These ratios however deal with the

relationship between two profit and loss A/C items. Both the items

must however belong to the same profit and loss A/C.

3. COMPOSITE/MIXED RATIOS OR INTER STATEMNT

RATIOS: These ratios exhibit the relation between a profit and loss

A/C of income statement item and a balance sheet item.

11. 11

(B)

FUNCTIONAL CLASSIFICATION OR

CLASSIFICAITON ACCORDING TO TESTS

In view of the financial management or according to the tests satisfied,

various ratios have been classified as below:

FUNCTIONAL CLASSIFICATION IN VIEW OF FINANCIAL MANAGEMENT OR

CLASSIFICATION ACCORDING TO TESTS

LIQUIDITY RATIOS LONGTERM SOLVENCY AND ACTIVITY RATIOS PROFITABILITY RATIOS

LEVERAGE RATIOS

(a)1.CURRENT RATIO FINANCIAL OPERATING 1.INVENTORY TURNOVER (a)IN RELATION TI SALE

2.LIQUID RATIO(ACID COMPOSITE RATIO 1.GROSS PROFIT

TEST OR QUICK RATIOS 1.DEBT EQITY RATIO 2.DEBTORS TURNOVER RATIO

3.ABSOLUTE LIQUID 2.DEBT TO TOTAL CAPITAL 3.FIXED ASSET TURNOVER 2.OPERATING RATIO

OR CASH RATIO 3.INTEREST COVERAGE 4.TOTAL ASSET TURNOVER 3.OPERATING PROFIT

4. INTERNAL MEASURE 4.CASH FLOW/DEBT RATIO RATIO

5. CAPITAL GEARING 5.WORKING CAPITAL 4.NET PROFIT RATIO

(b)1. DEBTORS TURNOVER TURNOVER RATIO 5.EXPENSE RATIO

RATIO 6.PAYABLE TURNOVER (b)IN RELATION TO

2. CREDITOR TURNOVER RATIO INVESTMENTS

RATIO 7.CAPITAL EMPLOYED 1. RETURN ON

3. INVENTORY TURNOVER TURNOVER INVESTMENTS

RATIO 2. RETURN ON

CAPITAL

3. RETURN ON EQITY

CAPITAL

4. RETURN ON TOTAL

RESOURCES

5. EARNING PER SHAR

6. PRICE EARNING

RATIO

EXPLAINATION

1. LIQUIDITY RATIOS: There are ratios, which measure the short-

term solvency or financial position of a firm. These ratios are

calculated to comment upon the short term paying capacity of a

concern or the firm ability to meet its current obligations.

2. LONG TERM SOLVENCY AND LEVERAGE RATIOS: Long-

term solvency ratios convey a firm’s ability to meet the interest cots

and repayments schedules of its long term obligations.

3. ACTIVITY RATIOS: Activity ratios are calculated to measure the

efficiency with which the resources of a firm have been employed.

These ratios are also called turnover ratios because they indicate the

speed with which assets are being turned over into sales.

12. 12

4. PROFITABILITY RATIOS: These ratio measures the results of

business operations or overall performance and effectiveness of the

firm. There are two type of profitability ratios 1.in relation to sales

2.in relation to investments.

(C) CLASSIFICATION ACCORDING TO SIGNIFICANCE OR

IMPORTANCE

The ratios have also been classified according to their significance or

importance. Some ratios are more important then others and the firm may

classify them al primary and secondary ratios. The British Institute of

management has recommended the classification of the ratios according to

importance for inter firm comparison. For inter-firm comparisons the ratios

may be classified as Primary and Secondary ratios. The primary ratios is one

of which is of the prime importance to a concern; thus return on the capital is

employed is named as primary ratio. The other ratios, which support the

other ratios, are called secondary ratios.

IMPORTANT FORMULA USED IN RATION ANALYSIS

Liquidity Analysis Ratios

Current Ratio

Current Assets

Current Ratio = ------------------------

Current Liabilities

Quick Ratio

Quick Assets

Quick Ratio = ----------------------

Current Liabilities

13. 13

Quick Assets = Current Assets - Inventories

Net Working Capital Ratio

Net Working Capital

Net Working Capital Ratio = --------------------------

Total Assets

Net Working Capital = Current Assets - Current Liabilities

Profitability Analysis Ratios

Return on Assets (ROA)

Net Income

Return on Assets (ROA) = ----------------------------------

Average Total Assets

Average Total Assets = (Beginning Total Assets + Ending Total Assets) / 2

Return on Equity (ROE)

Net Income

Return on Equity (ROE) = --------------------------------------------

Average Stockholders' Equity

Average Stockholders' Equity

= (Beginning Stockholders' Equity + Ending Stockholders' Equity) / 2

Return on Common Equity (ROCE)

Net Income

Return on Common Equity (ROCE)

--------------------------------------------

=

Average Common Stockholders' Equity

Average Common Stockholders' Equity

= (Beginning Common Stockholders' Equity + Ending Common Stockholders' Equity) / 2

Profit Margin

Net Income

Profit Margin = -----------------

Sales

14. 14

Earnings Per Share (EPS)

Net Income

Earnings Per Share (EPS) = ---------------------------------------------

Number of Common Shares Outstanding

Activity Analysis Ratios

Assets Turnover Ratio

Sales

Assets Turnover Ratio = ----------------------------

Average Total Assets

Average Total Assets = (Beginning Total Assets + Ending Total Assets) / 2

Accounts Receivable Turnover Ratio

Sales

Accounts Receivable Turnover Ratio = -----------------------------------

Average Accounts Receivable

Average Accounts Receivable

= (Beginning Accounts Receivable + Ending Accounts Receivable) / 2

Inventory Turnover Ratio

Cost of Goods Sold

Inventory Turnover Ratio = ---------------------------

Average Inventories

Average Inventories = (Beginning Inventories + Ending Inventories) / 2

Capital Structure Analysis Ratios

Debt to Equity Ratio

Total Liabilities

Debt to Equity Ratio = ----------------------------------

Total Stockholders' Equity

Interest Coverage Ratio

15. 15

Income Before Interest and Income Tax Expenses

Interest Coverage Ratio = -------------------------------------------------------

Interest Expense

Income Before Interest and Income Tax Expenses

= Income Before Income Taxes + Interest Expense

Capital Market Analysis Ratios

Price Earnings (PE) Ratio

Market Price of Common Stock Per Share

Price Earnings (PE) Ratio = ------------------------------------------------------

Earnings Per Share

Market to Book Ratio

Market Price of Common Stock Per Share

Market to Book Ratio = -------------------------------------------------------

Book Value of Equity Per Common Share

Book Value of Equity Per Common Share

= Book Value of Equity for Common Stock / Number of Common Shares

Dividend Yield

Annual Dividends Per Common Share

Dividend Yield

------------------------------------------------

=

Market Price of Common Stock Per Share

Book Value of Equity Per Common Share

= Book Value of Equity for Common Stock / Number of Common Shares

Dividend Payout Ratio

Cash Dividends

Dividend Payout Ratio = --------------------

Net Income

16. 16

ROA = Profit Margin X Assets Turnover Ratio

ROA = Profit Margin X Assets Turnover Ratio

Net Income Net Income Sales

ROA = ------------------------ = -------------- X ------------------------

Average Total Assets Sales Average Total Assets

Profit Margin = Net Income / Sales

Assets Turnover Ratio = Sales / Averages Total Assets

INTERPRETATIONS THEORY OF THE RATIOS

The interpretations of the ratios are an important factor. Though calculation

of the ratios is important but it is only a clerical task whereas interpretation

needs skill, intelligence and foresightedness. The inherent limitations of the

ratio analysis should be kept in mind while interpreting them. The impact of

the factors such as price level changes, change in accounting policies,

window dressing etc., should be also be kept in mind when attempting to

interpret ratios. The interpretation of the ratios can be made in the following

ways.

1. SINGLE ABSOLUTE RATIOS: the single ratios can be studied in

relation to certain rules of thumb, which are based upon well-proven

conventions.

2. GROUP OF RATIOS: Ratios may be interpreted by calculating a

group of related ratios. A single ratios supported by a group of related

ratios become more understandable and meaningful.

3. HISTORICAL COMPARISION: one of the earliest and most popular

ways of evaluating the performance of the firm is to compare its

present ratios with the past ratios called comparision overtime.

17. 17

4. PROJECT RATIOS: Ratios can be also calculated for future

standards based upon the projected or perform financial statements.

These future ratios may be taken as standard for comparison and the

ratios calculated on actual financial statements can be compared with

the standard ratios to find out variances.

5. INTER FIRM COMPARISION: Ratios of one firm can also be

calculated with the ratios of the other selected firm in the same

industry at the same point of time. This kind of comparison helps in

evaluating relative financial position and performance of the firm.

GUIDELINES OR PRECUATIONS FOR THE USE OF RATIOS

The calculation of the ratios may not be a difficult task but their use is not

easy. The information on which these are based, the constraints of the

financial statements, objective for using them, the caliber of the analyst, etc.

are the important factors which influence the use of ratios. Following are the

guidelines for interpreting ratios.

1. ACCURACY OF THE FINANCIAL STATEMENTS: The reliability

of the ratios are linked with the data available in the financial

statements. Before calculating the ratios one should see whether the

proper conventions have been used for preparing financial statements

or not.

2. OBJECTIVE OF THE PURPOSE OF ANALYSIS: The type of

ratios to be calculated will depend upon the purpose for which these

are required. If the purpose is to study the financial position then the

ratios of current assets and liabilities will be studied. The purpose of

“user” is important for the analysis of ratios.

3. SELECTION OF RATIOS: another precaution in ratio analysis is

the proper selection of appropriate ratios. The ratios should match the

purpose for which these are required.

18. 18

4. USE OF STANDARDS: The ratios will give an indication of

financial position only when discussed with the reference to certain

standards. Unless otherwise these ratios are compared with certain

standards one will not be able to reach at conclusions.

5. CALIBER OF THE ANALYST: The ratios are only the tools of the

analysis and their interpretation will depend upon the caliber and

competence of the analyst. He should be familiar with the various

financial statements and significant changes etc.

6. RATIOS PROVIDE ONSY A BASE: The ratios are only guidelines

for there analyst, he should not base his decisions entirely on them. He

should study any other relevant information, situation in concern,

other economic environment.

USE AND SIGNIFICANCE OF RATIO ANALYSIS

The ratio analysis is one of the most powerful tools of financial

analysis. It is used as a device to analyze and interpret the financial health of

enterprise. Just like the doctor examines the patient by recording his body

temperature, blood pressure, and etc. before making his conclusion

regarding the illness and before giving his treatment.

The use of ratios is not confined to financial managers only but

there are different parties also which are interested in the ratio analysis for

knowing the financial position of a firm for different purposes like supplier

of goods on credit, financial institutions, invertors, shareholders etc. With

the use of ratio analysis one can measure the financial condition of a firm

and can point our whether the condition is strong, good, poor etc.

Applications of the ratio analysis are:

MANAGERIAL USES OF RATIO ANALYSIS

1. HELPS IN DECISION MAKING: Financial statements are

prepared primarily for decision-making. Ratio analysis helps in

19. 19

making decisions from the information provided in these

financial statements.

2. HELPS IN FINANCIAL FORECASTING AND

PLANNING: Ration analysis is of much help in financial

forecasting and planning. Planning is looking ahead and the

ratios calculated for a number of years work as a guide for the

future. Meaningful conclusions can be drawn from these ratios.

3. HELPS IN COMMUNICATING: The financial strengths and

weakness of the firm are communicated in a more easy and

understandable manner by the use of these ratios. The ratios

help in communication and enhance the value of the financial

statements.

4. HELPS IN COORDINATION: Ratios even help in

coordination, which is of utmost importance in effective

business management. Better communication of efficiency and

weakness of an enterprise results on better coordination in the

enterprise.

5. HELPS IN CONTROL: Ratio analysis even helps in making

effective control of the business. Standard ratios can be based

upon Performa of financial statements and variance or

deviations, if any, helps in comparing the actual with the

standards so as to take a corrective action at the right time.

6. OTHER USES: There are so many other uses of the ratio

analysis. It is an essential part of the budgetary control and

standard costing. Ratios are of immense importance in the

analyses and interpretation of financial statements as they bring

the strength or weakness of the firm

UTILITY TO SHARE HOLDERS AND INVESTORS

The investor in the company will like to assess the financial

position of the concern where he is going to invest. Firstly the investor

20. 20

will try to ass3ess the value of fixed assets and the loans raised against

them. The investor will feel satisfied only if the concern has sufficient

amount of assets. Long-term solvency ratios will help him in assessing

the financial position of the concern. Profitability ratios, on the other

hand, will be useful to determine profitability position. Ratio analysis

will be useful to the investor in making up his mind whether present

financial position of the concern warrants further investment or not.

UTILITY TO THE CREDITORS

The creditors or the suppliers extend short-term credit to the

concern. They are interested to know whether financial position of the

concern warrants their payments at a specified time or not. The concern

pays short-term creditors out of its current assets. If the current assets are

quiet sufficient to meet current liabilities then the creditor will not

hesitate in extending credit facilities. Current and acid test ratios will give

an idea about their current financial position of the concern.

UTILITY TO THE EMPLOYEES

The employees are also interested in the financial position of

the concern especially profitability. Their wage increase and amount

of fringe benefits are related to the volume of profits earned by the

concern. The employees make use of information available in the

financial statements. Various profitability ratios relating to gross

profit, operating, net profit, etc., enable the employees to put forward

their viewpoint for the increase of wages and other benefits.

UTILITY TO GOVERNMENT

Government is interested to know the overall strength of the

industry. Various financial statements published by industrial units are

21. 21

used to calculate ratios for determining short-term. Long-term and overall

financial position of concerns. Profitability indexes can also be prepared

with the help of ratios. Government may base its future policies on the

bases of industrial information available from various units. The ratios

may be used as indicators of overall financial strength of public as well

as private sector. In the absence of the reliable economic information,

government plans and policies may not prove successful.

TAX AUDIT REQUIREMENTS

The Finance Act, 1984, inserted section 44 AB in the Income Tax Act.

Under this section every assessed engaged in any business and having

turnover or gross receipts exceeding Rs. 40 lakh is required to get the

accounts audited by a charted accountant and submit the tax audit report

before the due date for filing the return of income under section 139(1). In

case of a professional, a similar report is required if the gross receipts

exceeds Rs. 10 lacks. Clause 32 of the income Tax Act trequires that the

following accounting ratios should be given:

1. Gross Profit/turnover

2. Net Profit/turnover

3. Stock-in-trade/turnover

4. Materials consumed/Finished Goods Produced

22. 22

LIMITATIONS OF THE RATIO ANALYSIS

LIMITED USE OF A SINGLE RATIO: A single ratio, usually,

does not convey much of a sense. To make a better interpretation a

number of ratios have to be calculated which is likely to confuse the

analyst than help him in making any meaningful conclusion.

LACK OF ADEQUATE STANDARDS: There are no well-accepted

standards or rules of thumb for all ratios, which can accept as norms.

It renders interpretation of the ratios difficult.

INHERENT LIMITATIONS OF ACCOUNTING: like financial

statements, ratios also suffer from the inherent weakness of

accounting records such as their historical nature.

CHANGES OF ACCOUNTING PROCEDRURE: Changes in

accounting procedure by a firm often makes ratio analysis misleading

e.g. Changes in the valuation of inventories.

WINDOW DRESSING: Financial statements can easily be window

dressed to present a better picture of its financial and profitability

position to outsiders. Hence one has to be very careful from making a

decisions from ratios calculated from such financial statements.

PERSONAL BIAS: Ratios are only a means to financial analysis and

not an end in itself. Ratios have to be interpreted and different people

may interpret the same ratios in different ways.

UNCOMPARABLE: Not only industries differ in their nature but

also the firms of the similar business widely differ in their size and

accounting procedures etc., It makes the comparison of ratios difficult

and misleading. Moreover, comparisons are made difficult due to

differences in definitions of various financial terms used in the ratio

analysis.

ABSOLUTE FIGURES DISTORTIVE: Ratios devoid of absolute

figures may prove distractive as ratio analysis is primarily a

quantitative analysis and not qualitative analysis.

23. 23

PRICE LEVEL CHANGES: While making ratio analysis, no

consideration is made to the changes in price levels and this makes the

interpretation of the ratios invalid.

RATIOS NO SUBSTITUTE: Ratio analysis is merely a tool of

financial statements. Hence, ratios become useless if separated from

the statements from which they are computed.

CURRENT RATIO

Current ratio may be defined as the relationship between current assets and

current liabilities. This ratio is also known as working capital ratio, is a

measure of general liquidity and is most widely used to make the analysis of

the short-term position or liquidity of a firm. It is calculated by dividing the

total of current assets by total of the current liabilities.

CURRENT RATIO = __CURRENT ASSETS__

CURRENT LIABILITIES

Two basic components of this ratio are: current assets and current liabilities.

Current assets include cash and those assets, which can be easily converted

into cash within a short period of time generally, one year, such as

marketable securities, bills receivable, sundry debtors etc. Current liabilities

are those obligations which are payable within a short period of generally

one year and include outstanding expenses, bills payable, sundry creditors,

accrued expenses, dividend payable etc.

24. 24

SIGNIFICANCE AND LIMITATIONS OF CURRENT RATIO

Current ratio is a general and a quick measure of liquidity of a firm. It

represents the ‘margin of safety’ or ‘cushion’ available t the creditors and

current liabilities. It is most widely used for making short-term analyses of

the financial position or short-term solvency of the firm. But one has to be

careful while using current ratio as a measure of liquidity because it suffers

from the following limitations:

CRUDE RATIO: It is the crude ratio because it measures only the

quantity but not the quality if the current assets.

WINDOW DRESSING: Valuation of current assets and window

dressing is another problem of the current ratio. Current assets and

liabilities are manipulated in such a way that current ratio loses its

significance.

IMPORTANT FACTORS FOR REACHING A CONCLUSION

A number of factors should be taken into consideration before reaching a

conclusion about short-term financial position. Sone of these factors is.

25. 25

I. TYPE OF BUSINESS

II. TYPE OF PRODUCTS

III. REPUTATION OF THE CONCERN

IV. SEASONAL INFLUENCE

V. TYPE OF ASSETS AVAILABLE

PRACTILCAL CALCULATION OF CURRENT RATIO

CURRENT RATIO = CURRENT ASSETS : CURRENT LIABILITIES

TABLE

YEAR 2004 2005 2006

CONTENTS

ASSETS 4461.7 5102.5 11144.8

LIABILITIES 1967.3 2396.4 2995.4

CURRENT RATIO 2.267:1 2.111:1 3.720:1

WORKING NOTES-:

CURRENT ASSETS= INVENTORIES+SAUNDRY DEBTORS+CASH

AND BANK BALANCES

26. 26

2004 = 2153+2158.3+150.4 =4461.7

2005 = 2480.8+2353.9+177.8 = 5102.5

2006 = 3102.0+3483.9+4558.0 = 111444.8

CURRENT LIBILITIES

2004= 1967.3

2005 = 2396.4

2007 = 2995.4

GRAPH

4

3.702

3.5

3

2.5

2.267 2.111

2 CURRENT

1.5 RATIO

1

0.5

0

2004 2005 2006

INTERPRETATION OF CURRERENT RATIO

In the year 2004 the current ratio of LUPIN LABORATORIES PVT

(LTD) was satisfactory as the ratio was 2.26:1 which was more than

the standard ratio 2:1 for the current ratio. This means that the firm

27. 27

was liquid and has the ability to pay its current obligations in time as

and when they become due.

In the year 2005 the current ratio of the company was 2.11:1, which

was also satisfactory as was more than the standard ratio of 2:1. Thus

the company at that time also was in the position to pay the current

obligations as and when they become due.

In the year 2006 the current ratio of the company was 3.72:1, which

was, much more than the standard figure of the current ratio i.e. 2:1.

This means that the firm was liquid but the cash and the bank balance

was high which showed that the cash and the bank balance is lying

idle due to many reasons.

The current ratio in the year 2005 was less than the year 2004, which

indicates that the liquidity of the company was reduced and that the

liabilities were more than the paying capacity. The main reason of the

reduction of the ratio was reduction in the bank balances.

The current ratio in the year 2006 was more than the year 2005, which

indicates that the liquidity of the company was increased and the

capacity to pay the liabilities was more. The main reason of this was

the increase in the bank balances, which increased drastically nearly

20% in the year 2006.

WEIGHTED CURRENT RATIO

(PART OF CURRENT RATIO)

28. 28

The two basic determinants pf current ratio as measure of liquidity are

current assets and current liabilities. However all types of current assets are

not equally liquid and all current liabilities are not repayable with the same

degree of quickness. So the discrimination can be made among the different

components of current assets and current liabilities, the former on the basis

of relative quickness with which each individual item of current liabilities

mature for payment. The discrimination can be expressed by assigning by

assigning proper weight among each component of current assets and

current liabilities. Weights to be assigned on each individual components of

current assets and current liabilities, will depend upon the degree of their

relative liquidity in case of current assets and relative urgency payments in

case of current liabilities having due regard, however in each case the nature

and types of business. For e.g. cash and bank balance being most liquid asset

may be assigned a weightage of 100% followed by short-term securities

90% receivables 80% inventories 70%and so on. In the same manner,

advances received from the customers, tax payable and proposed dividend

may be assigned an weighted of 100% followed by trade creditors and

accounts payable 90%, bank overdraft 80%. Formula of weighted current

ratio:

29. 29

WEIGTED CURRENT RATIO=

TOTAL PRODUCT OF CURRENT RATIO

TOTAL PRODUCT OF CURRENT LIABILITY

PRACTICAL CALCULATLION OF WEIGHTED CURRENT RATIO

WIGHTED CURRENT RATIO=TOTAL PRODUCT OS CURRENT ASSETS : TOTAL

PRODUCT OF CURRENT LIABILITIES

TABLE

YEAR

2004 2005 2006

CONTENTS

PRODUCT OF 309684 354940 920686

CURRENT ASSETS

PRODUCT OF 157384 189944 204752

CURRENT

LIABILITIES

WEIGHTED 1.96 1.86 4.49

CURRENT RATIO

WORKING NOTES

TOTAL PRODUCT OF CURRENT ASSETS=(AMOUNT OF A PERTICULAR

CURRENT ASSET) X (PERCENTAGE WEIGHT)

30. 30

2004= CASH AND BANK BALANCES X 100% =150.4 X 100% = 15040

DEBTORS X 80% = 2158.3 X 80% = 172664

INVENTORIES X 60% = 2153.0 X 60% = 129180

TOTAL = 309684

SIMILARLY FOR YEARS 2005 AND 2006 AND ALSO

CURRENT LIABILITIES

TOTAL PRODUCT OF CURRENT LIABILITIES=(AMOUNT OF A

PETICULAR CURRENT LIABILITY) X (PERCENTAGE WEIGHT)

GRAPH

4.5 4.49

4

3.5

3

2.5

weighted current

2 1.96 ratio

1.86

1.5

1

0.5

0

2004 2005 2006

ANALYSIS OF THE WEIGHTED CURRENT RATIO

The weighted current ratio is measured on the basis of the weightage

given to the current assets and current liabilities so it is more reliable

than the current ratio.

31. 31

In the year 2004 the weighted current ratio of Lupin Ltd. was 1.96:1

which indicates the satisfactory ratio and the liquidity of the company

is more and that the company is at the capacity to pay the liabilities

due as the current assets are more than the current liabilities.

In the year 2005 the ratio was 1.86:1 which indicates that the

company is in a good position as the current assets are more than the

current liabilities and the company is in the position to pay all the

current liabilities due to the company.

In the year 2006 the ratio was 4.49:1 which was almost double than

the standard ratio, which is 2:1. This is basically because of the

increase in the bank balance and the cash in hand which increased

almost 20 times to that of the 2005. But this is not a very good sign

for the company as the cash in bank is so much that it is remaining

idles after paying dues to the creditors and there are not many

opportunities to invest that money.

In the year 2005 the ratio was decreased as compared to the 2004 ratio

basically because the more increase in the current liabilities less

increase in the current assets (bank balance, inventories).

In the year 2006 the ratio had increased drastically mainly due to the

great increase in the bank balance in the current assets.

QUICK OR ACID TEST OR LIQUID RATIO

Quick Ratio, also known as acid test or Liquid Ratio is more rigorous test of

liquidity than the current ratio. The term ‘liquidity’ refers t o the ability of a

firm to pay its short-term obligations as and when they become due. The two

determinants of current ratio, as a measure of liquidity are current assets and

current liabilities. Current assets include inventories and prepaid expenses,

which are not easily convertible into cash within a short period. Current

assets include inventories and prepaid expenses, which are not easily

32. 32

convertible into cash within a short period. Quick ratio may be defined as

the relationship between quick/liquid assets and current or liquid liabilities.

An asset is said to be liquid if it can be converted into cash within a short

period without loss of value. In that sense, cash in hand and cash art bank are

most liquid assets. The other assets, which can be included in the liquid

assets and sundry debtors, marketable securities and short-term or temporary

investments. Inventories cannot be termed to be liquid asset because they

cannot be converted into cash immediately without a sufficient loss of value.

In the same manner, prepaid expense is also excluded from the list of

quick/liquid assets because they are not expected to be converted into cash.

The quick ratio can be calculated by dividing the total of the quick assets by

total current liabilities. Thus:

QUICK/LIQUID OR ACID TEST RATIO=QUICK OR LIQUID ASSETS

QUICK/LIQUID LIABILITIES

PRACTICAL CALCULATION OF THE LIQUID, ACID TEST OR

QUICK RATIO

QUICK/LIQUID OR ACID TEST RATIO = QUICK OR LIQUID

ASSETS______

LIQUID/CURRENT LIABILITIES

TABLE

YEAR

CONTENTS 2004 2005 2006

2308.7 2531.7 8041.9

LIQUID ASSETS

LIQUID 1967.3 2374.3 2995.4

LIABILITIES

1.17:1 1.06:1 2.68:1

LIQUID RATIO

33. 33

WORKING NOTES

LIQUID ASSETS=CURRENT ASSETS-INVENTORIES

2004 = 4461.7 – 2153.0 = 2308.7

2005 = 5102.5 – 2480.8 = 2531.7

2006 = 11144.8 – 3102.9 = 8041.9

CURRENT LIABILITIES = REFER FROM ABOVE CALCULATION

GRAPH

(REFERRING THE ABOVE TABLE)

3

2.68

2.5

2

1.5

LIQUID RATIO

1.17

1 1.06

0.5

0

2004 2005 2006

ANALYSIS OF QUICK, ACID TEST OR LIQUID RATIO

In the year 2004 the current ratio was 1.17:1 which indicates the high

liquidity of the company and good ratio for paying the liabilities for

lupin laboratories. The ratio is good as there are funds left after paying

the liabilities to put in some more new emerging opportunities.

34. 34

In the year 2005 the liquid ratio of Lupin was 1.06:1 which indicates

the satisfactory liquidity position of the company because during the

payment of the dues of the creditors there will be hardly any funds left

to use in any other opportunity as the funds left will be reserved for

the next years liability.

In the year 2006 the ratio was 2.68:1 which was more than double if

the satisfactory ratio i.e. the company is in an a high liquidity position.

But such high ratio is also not good for the company as the funds are

left idle as they are not fully in the further opportunities due to many

reasons

The ratio was decreased in the year 2005 mainly because of the high

increase in the liquid liabilities and less increase in the liquid assets.

The ratio was increased in the year 2006 mainly because of the very

high increase in the cash and bank balance and less increase in the

liquid liabilities.

ABSOLUTE LIQUID RATIO OR CASH RATIO

Although receivables, debtors and bills receivables are generally more liquid

than inventories, yet there may be doubts regarding their realization into

cash immediately or in time. Hence, some authorities are of the opinion that

the absolute liquid ratio should also be calculated together with current ratio

and acid test ratio so as to exclude even receivables from the current assets

and find our the absolute liquid assets. Absolute liquid assets include cash in

35. 35

hand and at bank and marketable securities or temporary investments. The

acceptable norm for this ratio is 50% or .5:1 or 1:2 i.e. Re. 1 worth absolute

liquid assets are considered are considered adequate to pay Rs. 2 worth

current liabilities in time as ass the creditors are not expected to demand

cash at the same time and then cash may also be realized from debtors and

inventories. Thus

ABSOLUTE LIQUID RATIO=ABSOLUTE LIQUID ASSETS

CURRENT LIABILITIES

CASH RATIO= CASH AND BANK+SHORT-TERM SECURITIES

CURRENT LIABILITIES

PRACTICAL CALCULATION OF ABSOLUTE LIQUID RATIO OR

CASH RATIO

CASH RATIO = CASH & BANK+SHORT TERM SECURITIES

CURRENT LIABILITIES

TABLE

YEAR 2004 2005 2006

CONTENTS

CASH & BANK + 604.7 631.3 5070

SHORT TERM

SECURETIES

36. 36

CURRENT 1967.3 2396.4 2995.4

LIABILITIES

CASH RATIO 0.30 : 1 0.26 : 1 1.62 : 1

WORKING NOTES:

CASH AND BANK + SHORT TERM SECURITIES

2004 = 150.4 + 454.3 = 604.7

2005 = 177.8 + 453.5 = 631.3

2006 = 4558 + 512 = 5070

CURRENT LIABILITIES= REFER FROM ABOVE CALCULATION

GRAPH

(REFERRING THE ABOVE TABLE)

1.8

1.6 1.62

1.4

1.2

1

0.8 CASH RATIO

0.6

0.4

0.3 0.26

0.2

0

2004 2005 2006

ANALYSIS OF THE CASH RATIO OR ABSOLUTE LIQUIDITY

RATIO

1. The absolute liquid ratio in 2004 was .30:1 which is less than the

accepted norm i.e. .5:1. the ratio less than the standard ratio denotes

that the liabilities for LUPIN is more and that its liquid assets are less

37. 37

but all the creditors do not ask for the cash at the same time so the

situation can be handled.

2. The absolute liquid ratio in 2005 was .26:1 which is very less than the

accepted norm and thus the asset liquidity condition of LUPIN is not

good and thus the creditors are more.

3. The absolute liquid ratio in 2006 is 1.62:1 which is very favorable for

LUPIN but it is advisable that the company should try to collect funds

from public more to use its ideal liquid assets on other big projects.

4. The absolute liquid ratio in 2006 is more favorable than 2004 and

2005 mainly because of the increase in the liquidity of the assets and

decrease in the creditors for LUPIN.

CURRENT ASSETS MOVEMENT OR EFFICIENCY/ACTIVITY

RATIOS

Funds are invested in various assets in business to make sales and earn

profits. The efficiency with which asserts are managed directly affect the

volume of sales. The better the management of assets, the larger is the

amount of sales and the profits. Activity ratios measure the efficiency or

effectiveness with which a firm manages its resources or assets. These ratios

are also called turnover ratios because they indicate the speed rate at which

the funds invested in inventories are converted into sale. Depending upon

the purpose a number of turnover ratios can be calculated as debtors

turnover capital turnover, etc.

There are 4 types of current assets movement or efficiency ratios:

I. INVENTORY OR STOCK TURNOVER RATIO.

II. CREDITORS/PAYABLES TURNOVER RATIO.

III. WORKING CAPITAL TURNOVER RATIO.

IV. DEBTORS/RECEIVIBLES TURNOVER RATIO.

EXPLAINATION

38. 38

CREDITORS/PAYABLES TURNOVER RATIO

In the course of business operations, a firm has to make credit purchases and

incur short-term liabilities. A supplier of goods i.e. creditor is naturally

interested in finding out how much time the firm is likely to take in repaying

its trade creditors. The analysis for creditor’s turnover is basically the same

as of debtor’s turnover ratio except that in place of average daily sales,

average daily purchases are taken as the other component of the ratio and in

place of average daily sales; creditor’s turnover ratio can be calculated as:

CREDITORS/PAYABLE TURNOVER RATIO=NET CREDIT ANNUAL PURCHASES

AVERAGE TRADE CREDITORS

If the information about the credit purchases is not available, the figure of

total purchases may be taken as the numerator and the trade creditors include

sundry creditors and bills payable. If opening and closing balances of the

creditors are not known, the creditors are turned over in relation to purchase.

Generally, higher the creditor’s velocity better it is or otherwise lower the

creditor’s velocity less favorable are the results.

PRACTICAL CALCULATLION ON CREDITORS/PAYABLES

TURNOVER RATIO

CREDITORS TURNOVER RATIO=NET CREDIT ANNUAL PURCHASES

AVERAGE TRADE CREDITORS

TABLE

YEAR 2004 2005 2006

CONTENTS

NET CREDIT 846.2 1192.2 1861

40. 40

7 6.8

6

5.7

5.3

5

4

CREDITORS

TURNOVER

3

RATIO

2

1

0

2004 2005 2006

ANALYSIS OF CREDITORS/PAYABLE TURNOVER

RATIOS

The creditor’s turnover ratio in the year 2004 was 5.7 times which

indicates that velocity with which the creditors are turned over in relation

to purchases is in a satisfactory position.

The creditors turnover ratio in the year 2005 was 5.3 times which

indicate the velocity with which the creditors are turned over in relation

to purchases is in a satisfactory position. Basically the ratio should be

more than 5 times.

41. 41

The creditors turnover ratio in the year 2006 was 6.8 times which

indicates that the velocity with which the creditors are turned over in

relation to purchases is high which indicates a good sign for LUPIN.

The creditor’s turnover ratio in the year 2004 was more that 2005 which

indicates that the turn over of creditor’s rate had decreased which is not a

good sign. This is mainly due to the increase in the net credit annual

purchases.

The creditor’s turnover ratio in the year 2006 had increased from 2005,

which is a good sign for the liquidity position of LUPIN. This is mainly

due to the increase in the net credit purchases.

WORKING CAPITAL TURNOVER RATIO

Working capital of a concern is directly related to sales, the current assets

like debtors, bills receivables, cash, and stock, etc. change with the increase

or decrease in sales. The working capital is taken as:

WORKING CAPITAL = CURRENT ASSETS-CURRENT LIABILITIES

Working capital turnover ratio indicates the velocity of the utilization of net

working capital. This ratio indicates the number of times the working capital

is turned over in the course of a year. The ratio measures the efficiency with

42. 42

which the working capital is being used by the firm. The higher ratio

indicated the efficient utilization of the working capital and low ration

indicated otherwise. But a very high working capital turnover ratio is not

good situation for any firm and hence care must be taken while interpreting

the ratio. Making of comparative and trend analysis can use the ratio for

different firms in the same industry and for various periods. The ratio can be

calculated as:

Working capital turnover ratio = Cost of Sales_____

Average working capital

Average working capital =

Opening working capital + closing working capital

2

If the figure of the cost of sale is not given then the figure of sales can be

used instead. On the other hand if opening working capital is not disclosed,

then working capital at the year-end will be used, In that case the ratios will

be:

WORKING CAPITAL TURNOVER RATIO= _________SALES________

NET WORKING CAPITAL

PRACTICAL CALCULATION ON WORKING CAPITAL TURNOVER

RATIO

WORKING CAPITAL TURNOVER RATIO= COST OF SALES

AVERAGE WORKING CAPITAL

43. 43

TABLE

YEAR 2004 2005 2006

CONTENTS

COST OF SALES 11192.8 11611.3 16061

AVERAGE 2638.2 2627.15 5517.75

WORKING

CAPITAL

WORKING 2.91 times 4.41 times 4.20 times

CAPITAL

TURNOVER

RATIO

WORKING NOTES

WORKING CAPITAL=CURRENT ASSETS-CURRENT LIABILITIES

2004 = 4461.7 - 1967.3 = 2494.4

2005 = 5102.5 - 2374.3 = 2728.2

2006 = 11144.8 - 2995.4 = 8149.4

AVERAGE WORKING CAPITAL=

OPENING WOKING CAPITAL+CLOSING WORKING CAPITAL

2

2004 = 2242+2494.4 / 2 = 2638.2

2005 = 2494.4+2728.2 / 2 = 2627.15

44. 44

2006 = 2728.2+8149.4 / 2 = 5517.75

NET CREDIT ANNUAL SALES = REFER FROM THE EXCEL SHEET

GRAPH

4.5 4.41

4.2

4

3.5

3 2.91

2.5 W.C

2 TURNOVER

RATIO

1.5

1

0.5

0

2004 2005 2006

ANALYSIS OF WORKING CAPITAL TURNOVER RATIO

The working capital turnover ratio in the year 2004 was 2.91 times,

which is not a satisfactory ratio, and the company does not use which

indicates that LUPIN is not in a good position and the working capital

efficiently.

The working capital turnover ratio in the year 2005 was 4.41 times

which a satisfactory ratio for the company and which indicates that

LUPIN is using efficiently the working capital and that the resources

are efficiently being utilized.

45. 45

The working capital turnover ratio in the year 2006 was 4.20 times

which indicates the satisfactory position of LUPIN and the working

capital is being reutilized efficiently more and more times by the

company.

The working capital turnover ratio in the year 2004 was less than 2005

mainly because of the decrease in the cost of sales and the average

working capital of LUPIN.

The working capital turnover ratio in the year 2005 was more than the

year 2006 mainly because of the increase in the working capital and

the decrease in the cost of sales of the company.

I. INVENTORY/STOCK TURNOVER RATIO

Every firm has to maintain a certain level on inventory for finished goods

so as to be able to meet the requirements of the business. But the level of

inventory should neither to be too high or too low. But the level of

inventory should neither be too high nor too low. It is harmful to hold more

inventories for the following reasons.

a) It unnecessarily blocks capital which can otherwise be profitability

used somewhere else.

b) Over stocking will require more godown space, so more rent will be

paid.

46. 46

c) There are chances of obsolescence of stocks. Consumers will prefer

goods of latest design, etc.

d) Slow disposal of stocks means slow delivery of cash also which will

adverselu affect liquidity.

e) There are chances of deterioration in quality if the stock are held for

more periods.

Inventory turnover ratio also known as stock velocity is normally calculated

as sales/average inventory. It would indicate whether inventory has been

efficiently used or not. The purpose is to see whether only the required

minimum funds have been locked up in inventory. Inventory turnover ratio

(I.T.R.) indicates the number of times the stock has been turn over during

the period and evaluates the efficiency with which a firm is able to manage

the inventory.

Inventory turnover ratio = _cost of goods sold______

Average inventory at cost

PRACTICAL CALCUALTION ON INVENTORY/STOCK TURNOVER

RATIO

INVENTORY TURNOVER RATIO =

NET SALES__

AVERAGE INVENTORY AT COST

TABLE

47. 47

YEAR 2004 2005 2006

CONTENTS

NET SALES 11192.8 11611.3 16061.0

AVERAGE 1785.8 2316.9 2791.85

INVENTORY AT

COST

INVENTORT 6.26 : 1 5.01 : 1 5.75 : 1

TURNOVER

RATIO

WORKING NOTES

NET SALES =

2004 = 11192.8

2005 = 11611.3

2006= 16061.0

AVERAGE INVENTORY AT COST=OPENING STOCK+CLOSING STOCK

2

2004 = 1418.6+2153.0 = 1785.8

2

2005 = 2153.0+2480.8 = 2316.9

2

2006 = 2480.8+3102 = 2791.85

2

GRAPH

(REFERRING THE ABOVE TABLE)

48. 48

7

6.26

6 5.75

5.01

5

4

Inventory

3 turnover ratio

2

1

0

2004 2005 2006

ANALYSIS OF THE INVENTORY/STOCK TURNOVER

RATIO

The inventory turnover ratio of the LUPIN in the year 2004 was 6.26:1,

which is more than the standard ratio i.e. 5:1. The increased amount of

ratio indicates that the sales are high but the stock is not sufficient in the

company so as to meet the high demand which in turn decreases the

market share.

The inventory turnover ratio in the year 2005 was 5.01:1, which was very

accurate, and up to the mark of the standard ratio. This ratio indicates that

there was a perfect balance in LUPIN of the sales and there the market

demands were timely fulfilled and there was no shortage of goods.

The inventory turnover ratio in the year2006 was 5.75:1, which indicates

that the sales of LUPIN were good but the stock of sales was some less

than required.

49. 49

The inventory turnover ratio decreased from 2004 to 2005 from 6.26:1 to

5.01:1, which indicates that the net sales were less and that the balance

was gained between the sales and the stock in LUPIN.

The inventory turnover ratio was increased from 2005 to 2006 from

5.01:1 to 5.75:1, which indicates that the the sales of the product has

increased but the balance of the stocks in LUPIN has decreased.

DEBTORS OR RECEIVIBLES TURNOVER RATIO

A concern may sell goods on cash as well credit. Credit is one of the most

important elements of sales promotion. The volume of sales can be increased

but following a liberal credit policy. But the effect of a liberal credit policy

may result in tying up substantial funds of a firm in the form of trade debtors

(or receivables i.e. debtors plus bills receivables). Trade debtors are expected

50. 50

to be converted into cash within a short period and are included in current

assets. Hence the liquidity position of a concern to pay its short-term

obligations in time depends upon the quality of its trade debtors.

Debtor’s turnover ratio indicates the velocity of debt

collection of firm. In simple words, it indicates the number of times average

debtors (receivables) are turned over during a year, thus:

DEBTORS(RECEIVIBLES)TURNOVER/VELOCITY=NET CREDIT ANNUAL SALE

AVERAGE TRADE DEBTORS

TRADE DEBTORS=SUNDRY DEBTORS+BILLS RECEIVIBLES AND ACCOUNTS

RECEIVIBLES

AVERAGE TRADE DEBTORS=OPENING TRADE DEBTORS+CLOSING TRADE DEBTOR

2

PRACTICAL CALCULATION ON DEBTORS/RECEIVIBLES

TURNOVER RATIO

DEBTORS/RECEIVIBLES TURNOVER RATIO= NET CREDIT ANNUAL SALES

AVERAGE TRADE DEBTORS

TABLE

YEAR 2004 2005 2006

CONTENTS

NET CREDIT 11192.8 12611.4 16954.0

ANNUAL SALES

52. 52

1.85

1.81

1.8

1.75

1.7 debtor turnover

1.69

ratio

1.66

1.65

1.6

1.55

2004 2005 2006

ANALYSIS OF THE DEBTORS TURNOVER RATIO

The ratios in the year 2004 indicate that the ratio turned over 1.69 times

in a year which is satisfactory for LUPIN. The more times the ratio

turnovers in a year the more efficient are it for the company.

The ratio in the year 2005 indicates that the ratio turned over for 1.66

times in a year which is satisfactory for a company.

The ratio in the year 2006 indicates that the ratio is turned over for 1.81

times in a year which is approximately equal to 2 times which is good for

LUPIN which denotes that the management of the debtors is good as well

as more liquid are the debtors.

ANALYSIS OF LONG TERM FINANCIAL POSITION OR

LONG TERM SOLVENCY

53. 53

The term solvency refers to the ability of a concern to meet its long-term

obligations. The long-term in debt ness of a firm includes debentures

holders, financial institutions providing medium and long-term loans and

other creditors selling goods on installment bases. The long-term creditors of

a firm are primarily interested in knowing the firms ability to pay regularly

interested on long term borrowings, repayment of the principal amount at the

maturity and the security of their loans. Accordingly, long-term solvency

ratios indicate a firm’s ability to meet the fixed interest and costs and

repayments schedules associated with its long-term borrowings. The

following ratios serve the purpose of determining the solvency of the

concern.

DEBT-EQUITY RATIO.

FUNDED DEBT TO TOTAL CAPIT ALISATION RATIO.

PROPRIETORY RATIO OR EQUITY RATIO.

SOLVENCY RATIO OR RATIO OF TOTAL LIABILITIES TO

TOTAL ASSETS.

FIXED ASSETS TO NET WORTH OR PROPRIETORS FUNDS

RATIO.

FIXED ASSETS TO LONG-TERM FUNDS OR FIXED ASSETS

RATIO.

RATIO OF CURRENT ASSETS TO PROPRIETOR’S FUNDS.

DEBT SERVICE RATIO OR INTEREST COVERAGE RATIO.

CASH TO DEBT SERVICE RATIO.

(I) DEBT EQUITY RATIO

54. 54

Debt equity ratio is also known as External internal equity ratio is calculated

to measure the relative claims of outsiders and the owners against the firm’s

assets. These ratios indicates the relationship between the external equities

or the outsider’s funds and the internal equities or the share holders funds,

thus:

DEBT-EQUITY RATIO = OUTSIDERS FUNDS

SHARE HOLDERS FUNDS

The two basic components of the ratio are outsider’s funds, i.e.., external

equities and shareholders funds, i.e. internal equities. The outsiders funds

include all debts/liabilities to outsiders, whether long-term or short term or

whether in the form of debentures bonds, mortgage or bills. The

shareholders funds consist of equity share capital, preference share capital,

capital reserves, revenue for contingencies, sinking funds etc. the

accumulated losses and differed expenses, if any, should be deducted from

the total to find out shareholders funds. When the accumulated losses or

differed expenses are deducted from the shareholders funds, it is called net

worth and the ratio may be termed as the ratio ma be termed as debt to net

worth ratio.

(II) FUNDED DEBT TO TOTAL CAPITALISATION RATIO

55. 55

The ratio establishes a link between the long-term funds raised from

ortsiders and total long-term funds available in the business. The two words

used in this ratio are

1. Funded debt

2. Total capitalization

Funded debt or total capitalization ratio = Funded debt_____

Total capitalization

Funded debt is a part of total capitalization, which is financed by outsiders.

Though there is no ‘rule of thumb’ but still the lesser the reliance on

outsiders the better it will be. If this ratio is smaller, better it will be, up to

50% or 55% this ratio may be to tolerable and not beyond.

PRACTICAL CALCULATION OF FUNDED DEBT TO TOTAL

CAPITALISATION RATIO

FUNDED DEBT OR TOTAL CAPITALISATION RATIO=FUNDED DEBT

TOTAL CAPITALISATION

FUNDED DEBT=DEBENTURE+MORTGAGE LOANS+BONDS+OTHER

LONG TERM LOANS

TOTAL CAPITALISATION=EQUITY SHARE

CAPITAL+PREFERENCE SHARE CAPITAL+RESERVES AND

SURPLUS+OTHER UNDISTRIBUTED

RESERVES+DEBENTURES+FUNDED DEBT

56. 56

TABLE

2004 2005 2006

YEAR

CONTENTS

FUNDED DEBT 3777.3 4421 9128.5

TOTAL 11160.4 12720.1 19517

CAPITALISATION

FUNDED DEBT .33 : 1 .34 : 1 .46 : 1

RATIO

GRAPH

(REFERRING THE TABLE OF FUNDED DEBT RATIO)

0.5

0.45 0.46

0.4

0.35 0.34

0.33

0.3

0.25 FUNDED DEBT

0.2 RATIO

0.15

0.1

0.05

0

2004 2005 2006

57. 57

ANALYSIS OF FUNDED DEBT TO TOTAL

CAPITALISATION RATIO

The ratios in the year 2004-.33:1, 2005-.34:1, 2006-.46:1 indicate that

LUPIN has not much relied on the outsiders for taking long-term

funds and tried to raise all the finance from its own working capital.

The ratio has constantly increased from 2004 to 2006 mainly due to

increase in the long-term borrowings from the outsiders but in a small

amount.

58. 58

(III) PROPRIETORY RATIO OR EQUITY RATIO

The variant to the debt-equity ratio is the proprietary, which is also known as

Equity Ratio or shareholders to total equities ratio or net worth to total

assets ratio. The ratio establishes the relationship between shareholders

funds to total assets of the firm. The ratio of proprietor’s funds to total funds

is an important ratio for determining long-term solvency of a firm. The

components of this ratio are shareholders funds or proprietor’s funds and

total assets. The shareholders funds are equity share capital, preference share

capital, undistributed profits, reserves and surpluses. Ort of this amount,

accumulated losses should be deducted. The total assets on t he other hand

denote total resources of the concern. The ratio can be calculated as under:

PROPRIETORY RATIO OR EQUITY RATIO=SHAREHOLDERS FUNDS

TOTAL ASSETS

PRACTICAL CALCULATION OF EQUITY OR PROPRIETORY RATIO

EQUITY RATIO = SHAREHOLDERS FUNDS

TOTAL ASSETS

TABLE

60. 60

(REFERRING THE EQUITY RATIO TABLE)

0.5

0.45 0.46

0.44

0.4

0.35 0.36

0.3

0.25

EQUITY RATIO

0.2

0.15

0.1

0.05

0

2004 2005 2006

ANALYSIS OF THE PROPRIETORY RATIO OR EQUITY RATIO

The long-term financial position of LUPIN the company in the year

2004 was not so good but it gradually increased in the year 2005 due to

the decrease of the total assets.

The ratio in the year 2006 was more than the year 2005 because of the

more decreasing in the assets.

The more is the equity ratio the more is the liquidity position of the

company.

61. 61

(IV) SOLVENCY RATIO OR THE RATIO OF TOTAL

LIABILITIES TO TOTAL ASSETS

This ratio is a small variant of equity ratio and can be simply calculated as

100-equity ratio i.e., continuing the example taken for the equity ratio,

solvency ratio = 100-66.7% or say 33.33%. The ratio indicates the

relationship between the total liabilities to outsiders to total assets of a firm

and can be calculated as follows:

SOLVENCY RATIO=TOTAL LIABILITIES TO OUTSIDERS

TOTAL ASSETS

Generally, lower the ratio of total liabilities to total assets, more satisfactory

or stale is the long-term solvency position of a firm.

62. 62

PRACTICAL CALCULATION FOR SOLVENCY RATIO OR THE

RATIO IF TOTAL LIABILITIES TOTOTAL ASSETS

SOLVENCY RAITO= TOTAL LAIBILITIES TO OUTSIDERS / TOTAL ASSETS

TABLE

YEAR 2004 2005 2006

CONTENTS

TOTAL 11404.8 6328 6275.5

LIABILITIES TO

OUTSIDERS

TOTOAL ASSETS 17820 11300 9805.5

SOLVENCY .54 .44 .42

RATIO

GRAPH

(REFERRING THE SOLVENCY RATIO TABLE)

63. 63

0.6

0.54

0.5

0.44 0.42

0.4

0.3 SOLVENCY

RATIO

0.2

0.1

0

2004 2005 2006

ANALYSIS OF SOLVENCY RATIO OR THE RATIO OF

TOTAL LIABILITIES TO TOTAL ASSETS

The solvency ratio in the year 2004 was .54 which is not

sufficient for LUPIN to for the long-term solvency position of

the firm.

The solvency ratio in the year 2005 was less than the year 2004

mainly due to the decrease in the assets. Thus the ratio .44 in the

year 2005 is satisfactory.

The solvency ratio in the year 2006 was less than 2005 which

indicates the great financial position of LUPIN.

(V) FIXED ASSETS TO NET WORTH RATIO OR FIXED

ASSETS TO PROPRIETORS FUNDS

64. 64

The ratio establishes the relationship between fixed assets and shareholders

funds, i.e., share capital plus reserves, surpluses and retained earnings. The

ratio fcan be calculated as follows:

FIXED ASSET TO NET WORTH RATIO=FIXED ASSETS

SHAREHOLDERS FUNDS

The ratio of the fixed assets to net worth indicates the extent to which

shareholders funds are sunk into the fixed assets. Generally the purchase of

fixed assets should be financed by shareholders equity including reserves,

surpluses and retained earnings.

PRACTICAL CALCULATIO ON FIXED ASSET TO NET WORTH

RATIO

FIXED ASSET TO NET WORTH RATIO=FIXED ASSET

SHAREHOLDERS FUNDS

TABLE

YEAR 2004 2005 2006

CONTENTS

FIXED ASSET 5343.8 6287.5 6676.1

SHAREHOLDERS 6439.5 5005 4480.3

FUNDS

FIXED ASSET TO .82 1.25 1.49

NET WORTH

RATIO

GRAPH OF THE FIXED ASSET TO NET WORTH RATIO

65. 65

1.6

1.49

1.4

1.25

1.2

1

0.8 0.82 fixed assets to

net worth ratio

0.6

0.4

0.2

0

2004 2005 2006

INTERPRETATION

The ratio in the year 2004, 2005 and 2006 indicates that the net worth

ratio of the company is good and that the company has sufficient fixed

assets and that the share holders are less than the fixed assets in the

organization.

The ratio in 2004 is .82:1 indicates that the there are sufficient fixed

assets with the company.

The ratio in 2005 is 1.25:1 indicates that the company does not have

the sufficient fixed assets and the company has to depend more on the

public funds for sufficient working capital.

The ratio in 2006 is 1.45:1 which is not at all satisfactory and thus the

company has to depend totally on the shareholders for sufficient

working capital.

66. 66

RATIO OF CURRENT ASSETS TO PROPRIETORY’S

FUNDS

The ratio is calculated by dividing the total of current assets by the amount

of shareholders funds.

RATIO OF CURRENT ASSETS TO PROPRIETORY’S FUNDS = CURRENT ASSETS

SHAREHOLDERS FUNDS

The ratio indicates the extent to which proprietor’s funds are invested in

current assets. There is no ‘rule of thumb’ for this ratio and depending upon

the nature of the business there may be different ratios for different firms.

PRACTICAL CALCULATLION ON RATIO OF CURRENT ASSETS

TO PROPRIETORY FUNDS

RATIO OF CURRENT ASSETS TO PROPRIETORY’S FUNDS=CURRENT ASSET

SHAREHOLDERS FUNDS

TABLE

YEAR 2004 2005 2006

CONTENTS

CURRENT 4461.7 5102.5 11144.8

ASSETS

SHAREHOLDERS 6439.5 5005 4480.3

FUNDS

NET WORTH .69 : 1 1.01 : 1 2.48:1

RAITO

67. 67

GRAPH

(REFERRING THE ABOVE TABLE OF CURRENT ASSETS TO

PROPRIETORY FUNDS)

2.5 2.48

2

1.5

NET WORTH

1 1.01 RATIO

0.69

0.5

0

2004 2005 2006

INTERPRETATION

The ratio in the year 2004 and 2005 is satisfactory as the main part of

the proprietor’s funds are invested in the current asserts through which

the production increases and thus the profit also increases.

The ratio in 2006 indicates that the funds are invested in the current

assets also but a large part of the assets are remaining idle and LUPIN

has to use its own capital more as due to the less amount of public

funds as compared to the current assets.

68. 68

(VII) DEBT SERVICE RATIO OR INTEREST

COVERAGE RATIO

Net income to debt service ratio or simple debt service ratio is used to test

the debt servicing capacity of a firm. The ratio is also known as interest

coverage ratio or coverage ratio or fixed charges cover or times interest

earned. This ratio is calculated by dividing the net profit before interest and

taxes by fixed interest charges:

DEBT SERVICE RATIO/INTEREST COVERAGE= __NET PROFIT________

FIXED INTEREST CHARGES

PRACTICAL CALCULATION OF DEBT SERVICE

RATIO/INTEREST COVERAGE

DEBT SERVICE RATIO/INTEREST COVERAGE= __NET PROFIT________

FIXED INTEREST CHARGES

TABLE

YEAR 2004 2005 2006

CONTENTS

NET PEOFIT 1481.1 578.9 2299

FIXED 515.1 273.1 303

INTEREST

CHARGES

DEBT SERVICE 2.87 2.11 7.58

RATIO

VALUES ARE FROM THE BALANCE SHEET

69. 69

GRAPH

(REFERRING THE DEBT SERVICE TABLE)

8

7.58

7

6

5

4 DEBT SERVICE

RATIO

3

2.67

2 2.11

1

0

2004 2005 2006

INTERPRETATION

In the year 2004 and 2005 the ratio is satisfactory for the company as

well as for the long-term creditors because even if the earnings of the

firm’s earnings fall then also LUPIN will be in the position to pay the

interest.

In the year 2006 the ratio is not satisfactory for the company as well

for the shareholders as it implies that LUPIN is not using debt as a

source of finance so as to increase the earnings per share.

70. 70

ANALYSIS OF PROFITABILITY OR PROFITABILITY

RATIOS

The primary objective of the business undertaking is to earn profit. Profit

earning is considered essential for the survival of the business. In the works

of Lord Kenyes, “Profit is the engine that drives the business enterprise”. A

business needs profits not only for its existence but also for expansion and

diversification. The investors want an adequate return on their investments,

workers want higher wages, creditors want higher security for their interest

and loan and so on. A business enterprise can discharge its obligations to the

various segments of the society only through earning of profits. Profits are

thus a useful measure of overall efficiency of a business. Profits to the

management are the test of efficiency and a measurement of control; to

owners, a measure of worth of their investment to the creditors etc.

Generally, the profitability ratios are calculated either in the relation of their

sales or in relation to investment. The various profitability ratios are

discussed.

GENERAL PROFITABILITY RATIO

1. GROSS PROFIT RATIO

2. OPERATING RATIO

3. OPERATING PROFIT RATIO

4. EXPENSES RATIO

5. NET PROFIT RATIO

OVERALL PROFITABLITY RATIOS

1. RETURN ON SHAREHOLDERS INVESTMENT OR NET WORTH

RATIO

2. RETURN ON EQUITY CAPITAL RATIO

3. EARNING PER SHARE RATIO

4. RETURN ON CAPITAL EMPLOYED RATIO

5. CAPITAL TURNOVER RATIO

6. DIVIDEND YIELD RATIO

7. DIVIDEND PAYOUT RATIO

8. PRICE EARNING RATIO

71. 71

GROSS PROFIT RATIO

Gross profit ratio measures the relationship of gross profit to net sales