VIP Call Girl in Mumbai 💧 9920725232 ( Call Me ) Get A New Crush Everyday Wit...

Lupin

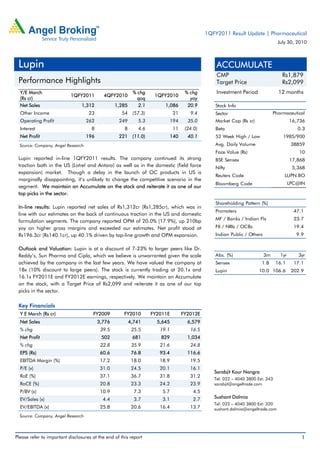

1. 1QFY2011 Result Update | Pharmaceutical

July 30, 2010

Lupin ACCUMULATE

CMP Rs1,879

Performance Highlights Target Price Rs2,099

Y/E March % chg % chg Investment Period 12 months

1QFY2011 4QFY2010 1QFY2010

(Rs cr) qoq yoy

Net Sales 1,312 1,285 2.1 1,086 20.9 Stock Info

Other Income 23 54 (57.3) 21 9.4 Sector Pharmaceutical

Operating Profit 262 249 5.3 194 35.0 Market Cap (Rs cr) 16,736

Interest 8 8 4.6 11 (24.0) Beta 0.3

Net Profit 196 221 (11.0) 140 40.1 52 Week High / Low 1985/900

Source: Company, Angel Research Avg. Daily Volume 38859

Face Value (Rs) 10

Lupin reported in-line 1QFY2011 results. The company continued its strong BSE Sensex 17,868

traction both in the US (Lotrel and Antara) as well as in the domestic (field force Nifty 5,368

expansion) market. Though a delay in the launch of OC products in US is

Reuters Code LUPN.BO

marginally disappointing, it’s unlikely to change the competitive scenario in the

Bloomberg Code LPC@IN

segment. We maintain an Accumulate on the stock and reiterate it as one of our

top picks in the sector.

Shareholding Pattern (%)

In-line results: Lupin reported net sales of Rs1,312cr (Rs1,285cr), which was in

Promoters 47.1

line with our estimates on the back of continuous traction in the US and domestic

MF / Banks / Indian Fls 23.7

formulation segments. The company reported OPM of 20.0% (17.9%), up 210bp

yoy on higher gross margins and exceeded our estimates. Net profit stood at FII / NRIs / OCBs 19.4

Rs196.3cr (Rs140.1cr), up 40.1% driven by top-line growth and OPM expansion. Indian Public / Others 9.9

Outlook and Valuation: Lupin is at a discount of 7-23% to larger peers like Dr.

Reddy’s, Sun Pharma and Cipla, which we believe is unwarranted given the scale Abs. (%) 3m 1yr 3yr

achieved by the company in the last few years. We have valued the company at Sensex 1.8 16.1 17.1

18x (10% discount to large peers). The stock is currently trading at 20.1x and Lupin 10.0 106.6 202.9

16.1x FY2011E and FY2012E earnings, respectively. We maintain an Accumulate

on the stock, with a Target Price of Rs2,099 and reiterate it as one of our top

picks in the sector.

Key Financials

Y E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

Net Sales 3,776 4,741 5,645 6,579

% chg 39.5 25.5 19.1 16.5

Net Profit 502 681 829 1,034

% chg 22.8 35.9 21.6 24.8

EPS (Rs) 60.6 76.8 93.4 116.6

EBITDA Margin (%) 17.2 18.0 18.9 19.5

P/E (x) 31.0 24.5 20.1 16.1

Sarabjit Kour Nangra

RoE (%) 37.1 36.7 31.8 31.2

Tel: 022 – 4040 3800 Ext: 343

RoCE (%) 20.8 23.3 24.2 23.9 sarabjit@angeltrade.com

P/BV (x) 10.9 7.3 5.7 4.5

EV/Sales (x) 4.4 3.7 3.1 2.7 Sushant Dalmia

Tel: 022 – 4040 3800 Ext: 320

EV/EBITDA (x) 25.8 20.6 16.4 13.7 sushant.dalmia@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. Lupin | 1QFY2011 Result Update

Exhibit 1: 1QFY2011 performance (consolidated)

Y/E March (Rs cr) 1QFY2011 4QFY2010 % chg (qoq) 1QFY2010 % chg (yoy) FY2010 FY2009 % chg

Net Sales 1,312 1,285 2.1 1,086 20.9 4,741 3,776 25.5

Other Income 23 54 (57.3) 21 9.4 144 95 51.3

Total Income 1,335 1,339 (0.3) 1,107 20.6 4,885 3,871 26.2

Gross profit 809 797 1.5 618 30.8 2,771 2,172 27.6

Gross margins 61.6 62.0 56.9 58.5 57.5

Operating profit 262 249 5.3 194 35.0 853 649 31.6

OPM (%) 20.0 19.4 17.9 18.0 17.2

Interest 8 8 4.6 11 (24.0) 38 50 (22.8)

Dep & Amortisation 40 41 (1.7) 23 73.8 124 88 40.8

PBT 237 254 (6.8) 181 30.6 835 606 37.8

Provision for Taxation 35 29 19.5 36 (3.9) 136 98 38.4

Reported Net Profit 202 225 (10.2) 145 39.3 699 508 37.7

Less : Exceptional Items - - - -

MI & Share in Associates 6 4 28.4 5 14.6 18 6 189.5

PAT after Exceptional Items 196 221 (11.0) 140 40.1 681 502 35.9

EPS (Rs) 22.1 24.8 16.8 76.8 60.6

Source: Company, Angel Research

Exhibit 2: 1QFY2011- Actual v/s Angel estimates

Rs cr Actual Estimates Variation

Net Sales 1,312 1,298 1.1

Other Income 23 22 4.6

Operating Profit 262 245 7.0

Interest 8 9 (4.1)

Tax 35 35 (0.1)

Net Profit 196 176 11.5

Source: Company, Angel Research

Revenue in line with estimates: Lupin reported net sales of Rs1,312cr (Rs1,285cr),

which was in line with our estimates on the back of continuous traction in the US

and domestic formulation segments. Sales in the advanced markets grew by a

stellar 29.0% yoy to Rs626.5cr (Rs485.8cr) driven by the US. Branded generic

business in the US grew by 51% due to Antara and Suprax (suspension 5% and

tablets 50% volume growth). In spite of slow pick up in Antara prescriptions, the

company expects to clock sales of US $60-65mn in FY2011. Lupin does not expect

any competition in Suprax in FY2011, post acceptance of the citizen petition by the

FDA. The company plans to launch Allernaze by end September 2010. Overall,

the generic business grew by 45% yoy driven by Lotrel (>20% market share), which

was launched in 4QFY2010.

In Europe, sales fell 18% yoy due to the currency impact and planned shut down of

the cephalosporin facility. Sales in Japan remained flat following change in the

accounting treatment and price cuts in the market. Lupin expects growth to be

back on track in the Japan region (10-12%) in the ensuing quarters.

July 30, 2010 2

3. Lupin | 1QFY2011 Result Update

Exhibit 3: Advanced markets sales trend

800

713

643 627

600

486 482

(Rs cr)

400

200

0

1QFY2010 2QFY2010 3QFY2010 4QFY2010 1QFY2011

Source: Company, Angel Research

The domestic formulation segment grew 23.2% yoy to Rs424.4cr (Rs344.4cr) on

account of the field force expansion and new product introductions.

Exhibit 4: Domestic formulation sales trend

450 424

344 347 345

300 264

(Rs cr)

150

0

1QFY2010 2QFY2010 3QFY2010 4QFY2010 1QFY2011

Source: Company, Angel research

OPM expands on favorable product mix: The company reported OPM of 20.0%

(17.9%), up by 210bp yoy on higher gross margins and was ahead of our

estimates. Raw material costs (including traded goods) increased by a mere 7.7%

to Rs503.6cr (Rs467.7cr) due to favorable product mix (Lotrel and Antara).

Employee expenses increased 35.4% to Rs178.1cr (Rs131.5cr) as the company

expanded its sales force in the domestic and US markets.

July 30, 2010 3

4. Lupin | 1QFY2011 Result Update

Exhibit 5: OPM trend

22.0

20.0 20.0

19.6 19.4

18.0 17.9

(%)

16.0

14.7

14.0

12.0

10.0

1QFY2010 2QFY2010 3QFY2010 4QFY2010 1QFY2011

Source: Company, Angel Research

Net profit ahead of estimates: Lupin reported net profit of Rs196.3cr (Rs140.1cr),

up 40.1% driven by top-line growth and OPM expansion. Further, tax charge at

15% was lower than estimated on the back of higher R&D weighted deduction.

Exhibit 6: Net profit trend

250

221

196

200

161 161

150 140

(Rs cr)

100

50

0

1QFY2010 2QFY2010 3QFY2010 4QFY2010 1QFY2011

Source: Company, Angel Research

Concall takeaways

The company has indicated a delay of 6 months (from March 2011 earlier to

September 2011) in the launch of oral contraceptive (OC) products due to the

longer-than-expected time taken in the US FDA review. However, the

company does not expect the delay to affect its competitive position in the

market.

Lupin expects to launch 3-4 products in the US in FY2011.

July 30, 2010 4

5. Lupin | 1QFY2011 Result Update

Recommendation Rationale

US market the key driver: The high-margin branded generic business has been the

key differentiator for Lupin in the Indian pharma space. The company has further

cemented its position in the segment by acquiring rights for two products, viz.

Allernaze and Antara. With this, Lupin has been able to clock sales of US $127mn

in FY2010, up 72% yoy and higher OPM. Lupin now has a sales force of 170

personnel in the US. On the generic turf, Lupin is currently the fifth largest generic

player in the US in terms of prescriptions, with 22 out of its 25 products in the top-

3 by market share. In the OC segment, Lupin has filed 22 ANDAs and expects the

approval to commence from 2HFY2012.

As per management, OC could contribute US $100mn to top-line over the next

two-three years. The company has filed for 37 ANDAs in FY2010, taking the

cumulative filings to 127, of which 41 have been approved. Lupin plans to launch

6 products in the US in FY2011, and another 80 products over the next three

years. Lupin now has 34 Para IV, of which 11 are FTFs (the company is the

exclusive holder in three of them: Glumetza, Fortamet and Cipro DS) addressing a

market size of US $8bn.

Domestic formulations on a strong footing: Lupin continues to make strides in the

Indian market. Currently, Lupin ranks No.5 climbing up from being No.11 six

years ago. Lupin has been the fastest growing company among the top-5

companies in the domestic formulation space, registering strong CAGR of 20.0%

over the last three years. Six of Lupin's products are among the top-300 brands in

the country. Lupin introduced 42 new products in the Indian market in FY2010 and

has a strong field force of 3,700 MRs.

First mover advantage in Japan: With Kyowa’s acquisition in FY2008, Lupin figures

among the few Indian companies with a formidable presence in the world’s

second largest pharma market. The Japanese government has introduced a new

policy and regulatory reforms to increase the generic drugs’ contribution from a

relatively low 17% in CY2007 to 30% of prescriptions by CY2012. This is estimated

to open up a US $10bn opportunity for the global generic players. We expect

Lupin to post a CAGR of 20% over FY2009-12E in the Japanese market and the

region is likely to contribute 12% of its FY2012E total sales.

Valuation: Lupin is trading at a discount of 7-23% to larger peers like

Dr. Reddy’s, Sun Pharma and Cipla, which we believe is unwarranted given the

scale achieved by the company in the last few years (FY2010 revenue stood at

Rs4,741cr, registering 33.0% CAGR over FY2007-10), best in class operating

margins (FY2010 OPM stood at 18%) and superior return ratios (FY2010 RoE of

37%). We have valued the company at 18x (10% discount to large peers). The

stock is currently trading at 20.1x and 16.1x FY2011E and FY2012E earnings,

respectively. We maintain an Accumulate on the stock, with a Target Price of

Rs2,099 and reiterate it as one of our top picks in the sector.

July 30, 2010 5

11. Lupin | 1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Lupin

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock Yes

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns) : Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

July 30, 2010 11