(INDIRA) Call Girl Mumbai Call Now 8250077686 Mumbai Escorts 24x7

PNB

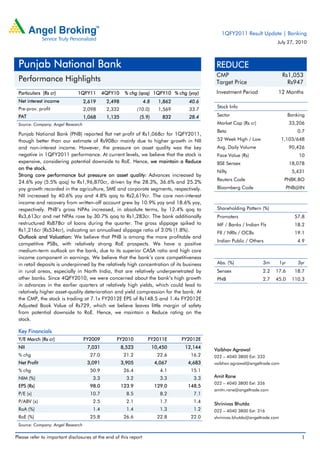

1. 1QFY2011 Result Update | Banking

July 27, 2010

Punjab National Bank REDUCE

CMP Rs1,053

Performance Highlights Target Price Rs947

Particulars (Rs cr) 1QFY11 4QFY10 % chg (qoq) 1QFY10 % chg (yoy) Investment Period 12 Months

Net interest income 2,619 2,498 4.8 1,862 40.6

Pre-prov. profit Stock Info

2,098 2,332 (10.0) 1,569 33.7

PAT 1,068 1,135 (5.9) 832 28.4 Sector Banking

Source: Company, Angel Research Market Cap (Rs cr) 33,206

Beta 0.7

Punjab National Bank (PNB) reported flat net profit of Rs1,068cr for 1QFY2011,

though better than our estimate of Rs908cr mainly due to higher growth in NII 52 Week High / Low 1,103/648

and non-interest income. However, the pressure on asset quality was the key Avg. Daily Volume 90,426

negative in 1QFY2011 performance. At current levels, we believe that the stock is Face Value (Rs) 10

expensive, considering potential downside to RoE. Hence, we maintain a Reduce BSE Sensex 18,078

on the stock.

Nifty 5,431

Strong core performance but pressure on asset quality: Advances increased by

Reuters Code PNBK.BO

24.6% yoy (5.5% qoq) to Rs1,96,870cr, driven by the 28.3%, 36.6% and 25.2%

yoy growth recorded in the agriculture, SME and corporate segments, respectively. Bloomberg Code PNB@IN

NII increased by 40.6% yoy and 4.8% qoq to Rs2,619cr. The core non-interest

income and recovery from written-off account grew by 10.9% yoy and 18.6% yoy,

respectively. PNB’s gross NPAs increased, in absolute terms, by 12.4% qoq to Shareholding Pattern (%)

Rs3,613cr and net NPAs rose by 30.7% qoq to Rs1,283cr. The bank additionally Promoters 57.8

restructured Rs878cr of loans during the quarter. The gross slippage spiked to MF / Banks / Indian Fls 18.2

Rs1,216cr (Rs534cr), indicating an annualised slippage ratio of 3.0% (1.8%).

FII / NRIs / OCBs 19.1

Outlook and Valuation: We believe that PNB is among the more profitable and

Indian Public / Others 4.9

competitive PSBs, with relatively strong RoE prospects. We have a positive

medium-term outlook on the bank, due to its superior CASA ratio and high core

income component in earnings. We believe that the bank’s core competitiveness

in retail deposits is underpinned by the relatively high concentration of its business Abs. (%) 3m 1yr 3yr

in rural areas, especially in North India, that are relatively underpenetrated by Sensex 2.2 17.6 18.7

other banks. Since 4QFY2010, we were concerned about the bank’s high growth PNB 2.7 45.0 110.3

in advances in the earlier quarters at relatively high yields, which could lead to

relatively higher asset-quality deterioration and yield compression for the bank. At

the CMP, the stock is trading at 7.1x FY2012E EPS of Rs148.5 and 1.4x FY2012E

Adjusted Book Value of Rs729, which we believe leaves little margin of safety

from potential downside to RoE. Hence, we maintain a Reduce rating on the

stock.

Key Financials

Y/E March (Rs cr) FY2009 FY2010 FY2011E FY2012E

NII 7,031 8,523 10,450 12,144

Vaibhav Agrawal

% chg 27.0 21.2 22.6 16.2 022 – 4040 3800 Ext: 333

Net Profit 3,091 3,905 4,067 4,683 vaibhav.agrawal@angeltrade.com

% chg 50.9 26.4 4.1 15.1

NIM (%) 3.3 3.2 3.3 3.3 Amit Rane

022 – 4040 3800 Ext: 326

EPS (Rs) 98.0 123.9 129.0 148.5

amitn.rane@angeltrade.com

P/E (x) 10.7 8.5 8.2 7.1

P/ABV (x) 2.5 2.1 1.7 1.4 Shrinivas Bhutda

RoA (%) 1.4 1.4 1.3 1.2 022 – 4040 3800 Ext: 316

RoE (%) 25.8 26.6 22.8 22.0 shrinivas.bhutda@angeltrade.com

Source: Company, Angel Research

Please refer to important disclosures at the end of this report 1

2. Punjab National Bank | 1QFY2011 Result Update

Exhibit 1: 1QFY2011 performance

% chg % chg

Particulars (Rs cr) 1QFY2011 4QFY2010 1QFY2010

(qoq) (yoy)

Interest earned 5,992 5,608 6.9 5207 15.1

Interest expenses 3,373 3,110 8.5 3346 0.8

Net interest income 2,619 2,498 4.8 1862 40.6

Non-interest income 872 935 (6.7) 970 (10.2)

Total income 3,490 3,433 1.7 2832 23.2

Operating expenses 1,392 1,100 26.5 1263 10.2

Pre-prov. profit 2,098 2,332 (10.0) 1569 33.7

Provisions & cont. 534 622 (14.1) 302 77.0

PBT 1,564 1,711 (8.6) 1268 23.4

Prov. for taxes 496 576 (13.9) 436 13.8

PAT 1,068 1,135 (5.9) 832 28.4

EPS (Rs) 33.9 36.0 (5.9) 26.4 28.4

Cost-to-income ratio (%) 39.9 32.0 44.6

Effective tax rate (%) 31.7 33.6 34.4

Net NPA (%) 0.7 0.5 0.2

Source: Company, Angel Research

Exhibit 2: 1QFY2011 Actual v/s Angel estimates

Particulars (Rs cr) Actual Estimates Var. (%)

Net interest income 2,619 2,429 7.8

Non-interest income 872 757 15.1

Total income 3,490 3,186 9.5

Operating expenses 1,392 1,266 9.9

Pre-prov. profit 2,098 1,920 9.3

Provisions & cont. 534 562 (4.9)

PBT 1,564 1,358 15.2

Prov. for taxes 496 450 10.1

PAT 1,068 908 17.7

Source: Company, Angel Research

July 27, 2010 2

3. Punjab National Bank | 1QFY2011 Result Update

Advances growth

Advances increased by 24.6% yoy (5.5% qoq) to Rs1,96,870cr, driven by a 28.3%,

36.6% and 25.2% yoy growth in the agriculture, SME and corporate segments,

respectively. Deposits grew by 16.6% yoy to Rs2,55,335cr in 1QFY2011. CASA

deposits grew at a healthy 24.3% yoy, taking the CASA ratio to 40.9% (40.8% in

4QFY2010 and 38.3% in 1QFY2010).

Exhibit 3: Trend in advances and deposits

(Rs cr) Deposits (LHS) Advances (LHS) Credit-Deposit ratio (%) (RHS) (%)

300,000 78

77

250,000 76

75

200,000 74

73

150,000

72

100,000 71

70

50,000 69

68

- 67

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Source: Company, Angel Research

Exhibit 4: Domestic advances break-up (1QFY2011)

Services & Others

Agri

17%

16%

Comm. Real

Estate

Retail

6%

10%

Medium & Large MSME

Corporates 11%

40%

Source: Company, Angel Research

July 27, 2010 3

4. Punjab National Bank | 1QFY2011 Result Update

Exhibit 5: Trend in CASA deposits

(%) CASA ratio

50

40 41 41

37 39 38 38

40

30

20

10

-

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Source: Company, Angel Research

Sequential NIMs down marginally

During 1QFY2011, NII increased by 40.6% yoy and 4.8% qoq to Rs2,619cr. The

yield on advances increased by 6bp sequentially to 10.28%, however, cost of

deposits increased at higher rate by 14bp sequentially to 5.02%. As a result,

reported NIMs declined marginally by 5bp sequentially to 3.94%. The impact of

daily interest payment on savings deposits was about 10bp.

Exhibit 6: Trend in quarterly reported NIM

(%) Reported NIM

4.5

4.0 3.9

4.0 3.7

3.6 3.6 3.6

3.5

3.5 3.3 3.2

3.1

3.0

2.5

2.0

4QFY08

1QFY09

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Source: Company, Angel Research

July 27, 2010 4

5. Punjab National Bank | 1QFY2011 Result Update

Non-interest income declines yoy but improves sequentially

The non-interest income declined 10.2% yoy to Rs872cr, driven by a 66.2% yoy

reduction in treasury gains. The core non-interest income and recovery from

written-off accounts grew by 10.9% yoy and 18.6% yoy, respectively.

Asset quality under pressure

PNB’s gross NPAs increased in absolute terms by 12.4% qoq to Rs3,613cr and net

NPAs rose by 30.7% qoq to Rs1,283cr. The gross and net NPA ratios deteriorated

to 1.8% and 0.7% (as against 1.7% and 0.5% respectively, in 4QFY2010),

respectively. The bank’s provision coverage ratio including technical write-offs

stood at 77.6% (81.2% in 4QFY2010 and 92.9% in 1QFY2010). PNB has

cumulatively restructured Rs12,973cr of its loans till date (6.6% of loans, 68% of

the net worth). The bank additionally restructured Rs878cr of loans during the

quarter. The gross slippage spiked to Rs1,216cr (Rs534cr), indicating an

annualised slippage ratio of 3.0% (1.8%). Till date, Rs1,038cr worth of loans have

slipped into NPAs from the restructured accounts (8% of the total restructuring), of

which Rs263 slipped during the current quarter. Management has indicated a

broad range of 10-15% as expected slippages from the restructured accounts.

Exhibit 7: Trend in asset quality

(%) Gross NPA % (LHS) Net NPA % (LHS) Provision Coverage % (RHS) (%)

5.0 100.0

4.5

4.0 90.0

3.5 80.0

3.0

2.5 70.0

2.0

1.5 60.0

1.0 50.0

0.5

- 40.0

1QFY08

2QFY08

3QFY08

4QFY08

1QFY09

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Source: Company, Angel Research, Note: NPA coverage % excluding technical write-offs

Increased NPA provisions

The bank made provisions of Rs550cr towards the NPAs in 1QFY2011, compared

to Rs462cr in 4QFY2010 and Rs269cr in 1QFY2010. Provision for investments

stood at Rs14cr, compared to a write-back of Rs50cr in 1QFY2010 (due to the low

interest rate environment in 1QFY2010). The bank’s SLR stood at 25.1%. Out of

the total investment book of Rs81,036cr, the bank’s AFS portfolio constituted

18.2%, with a modified duration of 2.2 years.

July 27, 2010 5

6. Punjab National Bank | 1QFY2011 Result Update

Operating cost under control

Employee cost increased by 52.4% sequentially to Rs995cr on account of

provisions for pension fund (Rs125cr), gratuity fund (Rs125cr) and towards

AS-15 (Rs107cr). Other operating expenses increased by 11.7% yoy to Rs397cr. As

a result, total operating cost increased by 10.2% yoy to Rs1,392cr. The cost-to-

income ratio of the bank stood at 39.9% (from 32.1% in 4QFY2010 and 44.6% in

1QFY2010).

Exhibit 8: Trend in productivity

(%) Cost-to-Income ratio

55 51

48 48 48

50

45

45 42 43 42

40 41 40

40 38

35 32

30

25

20

1QFY08

2QFY08

3QFY08

4QFY08

1QFY09

2QFY09

3QFY09

4QFY09

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Source: Company, Angel Research

Comfortable capital adequacy

PNB’s CAR stood at a healthy 13.8% at the end of 1QFY2011, with a Tier-I ratio

of 8.7%. Tier-I capital constituted 63.1% of the bank’s CAR.

Exhibit 9: Comfortable capital adequacy

(%) Tier-I CAR Tier-II CAR

16.0

14.0

12.0

10.0

8.0

6.0

4.0

2.0

-

1QFY10

2QFY10

3QFY10

4QFY10

1QFY11

Source: Company, Angel Research

July 27, 2010 6

7. Punjab National Bank | 1QFY2011 Result Update

Investment Arguments

Relatively higher YoA could lead to relatively higher asset quality deterioration: The

yield on advances of the bank increased by 49bp in 9MFY2010 over FY2008

levels, as against an average decrease of 5bp for the PSU banks. This gap

reduced in 4QFY2010 indicating unsustainable yields for PNB. PNB has

cumulatively restructured Rs12,096cr of loans till date (6.5% of loans, 75% of the

net worth) which is higher than the industry standards. In our view, the bank’s

strategy of high growth in advances at relatively high yields could contribute to

relatively higher asset quality deterioration and NIM compression for the bank

going forward.

Strong CASA legacy, but losing market share: PNB has a structural advantage of a

high CASA ratio of 40.8%, which is driven by strong rural and semi-urban

presence, especially in North India (total of 4,707 branches and 2,910 ATMs).

That said, the bank is losing market share like other PSBs (except SBI) on account

of slow branch expansion and competition from the private banks -savings market

share down by 50bp to 7.1% over FY2007-10.

Expensive valuations: The stock is trading at 1.4x FY2012E ABV of Rs729, which is

expensive considering its 5-year range of 1.0-1.5x and median of 1.3x. While we

believe the bank can deliver healthy core RoEs of 17-18% due to its strong legacy,

actual RoEs are unsustainably high at 26.6%. In our view, super-normal RoEs

cannot be sustainably earned through higher-than-sector average risk-adjusted

yield on assets and tend to decline in subsequent years either through an increase

in NPA costs or decline in yields. We believe that current valuations fairly reflect

PNB’s structural positives, but do not provide a sufficient margin of safety from

potential near-term asset quality pressures/decline in asset yields. Hence, we

maintain a Reduce rating on the stock, with a Target Price of Rs947.

July 27, 2010 7

8. Punjab National Bank | 1QFY2011 Result Update

Exhibit 10: Key assumptions

Earlier estimates Revised estimates

Particulars (%)

FY2011E FY2012E FY2011E FY2012E

Credit growth 19.0 18.0 22.0 18.0

Deposit growth 19.0 18.0 19.0 18.0

CASA ratio 40.2 39.4 40.2 39.4

NIM 3.3 3.2 3.3 3.3

Other income growth (15.0) 15.2 (15.1) 15.1

Growth in staff expenses 17.0 19.0 17.0 19.0

Growth in other expenses 13.0 19.0 13.0 19.0

Slippages 1.8 1.7 1.8 1.7

Coverage ratio 69.2 68.9 70.4 70.1

Treasury gain/(loss) (% of investments) 0.1 0.1 0.1 0.1

Source: Company, Angel Research

Exhibit 11: Change in estimates

FY2011E FY2012E

Particulars (Rs cr) Earlier Revised Earlier Revised

% chg % chg

estimates estimates estimates estimates

NII 10,362 10,450 0.9 11,948 12,144 1.6

Non-interest income 3,030 3,026 (0.1) 3,489 3,483 (0.2)

Total income 13,392 13,477 0.6 15,437 15,627 1.2

Operating expenses 5,506 5,506 - 6,552 6,552 -

Pre-prov. profit 7,886 7,971 1.1 8,885 9,075 2.1

Provisions & cont. 1,812 1,809 (0.2) 1,946 1,980 1.7

PBT 6,074 6,162 1.5 6,939 7,095 2.3

Prov. for taxes 2,065 2,095 1.5 2,359 2,412 2.3

PAT 4,009 4,067 1.5 4,580 4,683 2.3

Source: Company, Angel Research

Exhibit 12: P/ABV band

1600 Price 0.25x 0.65x 1.05x 1.45x 1.85x

1400

1200

1000

800

600

400

200

0

Oct-02

Oct-07

Sep-05

Feb-06

Sep-10

Feb-11

Nov-04

Nov-09

May-02

May-07

Jun-04

Jun-09

Dec-06

Jan-04

Jan-09

Aug-03

Apr-05

Jul-06

Aug-08

Apr-10

Mar-03

Mar-08

Source: Company, Angel Research

July 27, 2010 8

12. Punjab National Bank | 1QFY2011 Result Update

Research Team Tel: 022 - 4040 3800 E-mail: research@angeltrade.com Website: www.angeltrade.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make

investment decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this

document are those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or

other advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in

the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important `Stock Holding Disclosure' report on the Angel website (Research Section). Also, please

refer to the latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and

its affiliates may have investment positions in the stocks recommended in this report.

Disclosure of Interest Statement Punjab National Bank

1. Analyst ownership of the stock No

2. Angel and its Group companies ownership of the stock Yes

3. Angel and its Group companies' Directors ownership of the stock No

4. Broking relationship with company covered No

Note: We have not considered any Exposure below Rs 1 lakh for Angel, its Group companies and Directors.

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

July 27, 2010 12