In a time of historically low bond returns and high realized and potential equity market

volatility, two strategies that investors are turning to are commodity trading advisors (CTAs)

and global macro hedge funds. In adopting these strategies, it is important for investors to

distinguish the similarities and differences between these strategies. CTAs in a hedge fund

portfolio can be both a complement to and a substitute for a global macro allocation.

Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

Asset Alliance understanding managed futures

1. Hedgeharbor Navigator

June 2012

Understanding Managed Futures

In a time of historically low bond returns and high realized and potential equity market

volatility, two strategies that investors are turning to are commodity trading advisors (CTAs)

and global macro hedge funds. In adopting these strategies, it is important for investors to

distinguish the similarities and differences between these strategies. CTAs in a hedge fund

portfolio can be both a complement to and a substitute for a global macro allocation.

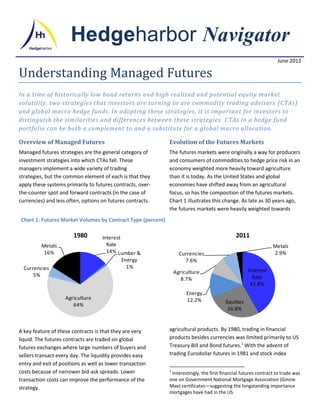

Overview of Managed Futures Evolution of the Futures Markets

Managed futures strategies are the general category of The futures markets were originally a way for producers

investment strategies into which CTAs fall. These and consumers of commodities to hedge price risk in an

managers implement a wide variety of trading economy weighted more heavily toward agriculture

strategies, but the common element of each is that they than it is today. As the United States and global

apply these systems primarily to futures contracts, over- economies have shifted away from an agricultural

the-counter spot and forward contracts (in the case of focus, so has the composition of the futures markets.

currencies) and less often, options on futures contracts. Chart 1 illustrates this change. As late as 30 years ago,

the futures markets were heavily weighted towards

Chart 1: Futures Market Volumes by Contract Type (percent)

1980 Interest 2011

Metals Rate Metals

16% 14% Lumber & Currencies 2.9%

Energy 7.6%

Currencies 1%

Agriculture Interest

5% Rate

8.7%

41.8%

Energy

Agriculture 12.2% Equities

64%

26.8%

A key feature of these contracts is that they are very agricultural products. By 1980, trading in financial

liquid. The futures contracts are traded on global products besides currencies was limited primarily to US

futures exchanges where large numbers of buyers and Treasury Bill and Bond futures.1 With the advent of

sellers transact every day. The liquidity provides easy trading Eurodollar futures in 1981 and stock index

entry and exit of positions as well as lower transaction

costs because of narrower bid-ask spreads. Lower 1

Interestingly, the first financial futures contract to trade was

transaction costs can improve the performance of the one on Government National Mortgage Association (Ginnie

strategy. Mae) certificates—suggesting the longstanding importance

mortgages have had in the US.

2. Table 1: Examples of Contracts that CTAs trade

Currencies

Equity Indexes Interest Rates Government Bonds (vs. US Dollar)

S&P 500 Eurodollar 30-Year US Treasury Bond Canadian Dollar

CAC-40 Fed Funds Rate German Bunds British Pound

DAX Short Sterling Japanese Government Bonds Euro

NASDAQ

Grains &

Energy Metals Soft Commodities Livestock

Crude Oil Gold Corn Live Cattle

Natural Gas Silver Soybeans Lean Hogs

Unleaded- Gasoline Copper Coffee Pork Bellies

Electricity Tin Wheat Feeder Cattle

Aluminum Sugar

futures in 1982, the futures industry took a decided turn variety of underlying asset classes with a diverse

toward financial instruments trading. These contracts geographic focus. Although global macro managers may

along with the Treasury Bill and Bond contracts also trade individual equities, as well as ETFs and cash

permitted financial market participants to hedge and bonds, futures are an important way they express a

speculate on a variety of financial risks. view in the markets they trade. As Table 1 illustrates,

futures contracts can cover the government bond

The development of these new futures contracts-

markets as well as the equity markets in a variety of

combined with the agricultural and industrial contracts

countries. In addition, the physical commodities—such

already in existence opened vast new opportunities for

as oil, gold or wheat—that managers in both strategies

traders in these instruments. Government regulation of

use are traded on global markets. As such, the price

the futures markets—part of which created the CTA

movements of these commodities reflect overall global

designation for an asset manager—also played a role in

economic strength or weakness, as well as the relative

the growth of the managed futures industry.

economic conditions of one versus others.

Prior to the development of futures markets in

In addition to trading similar instruments, the strategies

extensive and diverse underlying assets, futures traders

of CTAs and global macro managers can be assigned to

could still implement trading systems in the markets

similar categories. Both types of managers can take long

that did exist. Likewise, global macro managers could

and short positions in the markets that they trade. Both

implement their views in cash markets for government

can trade systematic strategies, discretionary strategies

bonds and equities, but while using already existing

or a combination of the two. Systematic strategies

futures markets for instruments such as precious

utilize quantitative models to identify trade

metals. The development of the futures markets,

opportunities and to make decisions about entry and

however, made taking positions in these markets easier

exit points for trades. Discretionary strategies rely on

and more capital efficient because margin requirements

the managers’ judgment to make trading decisions.2

on the futures exchanges enable managers to gain the

desired exposures to the markets with less upfront In order to identify the differences between CTAs and

commitment. The liquidity of the futures markets also global macro managers, it is necessary to make some

permitted manages to put on and take off positions generalizations. CTA managers often focus on the price

with relative ease. movements and trading volumes that individual

commodities display. If they utilize technical analysis as

How CTA and global macro strategies are

alike and different

2

Both CTAs and global macro hedge funds often trade For a fuller discussion of the strategies and styles that CTAs

the same instruments, namely futures contracts on a employ, see the Asset Alliance presentation, The Benefits of

Managed Futures, 2012

3. part of their trading strategy, price and volume data macro managers might not look at technical

may be the only data they look at. Even if CTAs view indicators—but they both observe and respond to the

commodity prices within a more fundamental, supply- same set of prices. Those prices in turn are influenced

demand framework, it will often be the case that they by the factors that the managers are responding to.

look at price movements most heavily in the trades that

One implication of the above observation is that CTAs

they make.

can be considered a subset of a larger trading strategy

Global macro managers in contrast, will often make that includes both CTAs and global macro manager. For

trading decisions with the context of an array of this reason, many investors include both CTAs and

macroeconomic data. The will base their view on “pure” global macro manages in their allocations to a

whether to take long or short positions in government global macro portfolio.

debt or equities in a particular country based on overall

CTA performance in different market

changes in such economic data. This is not to say that

environments

global macro managers ignore asset prices; clearly they

We shift our focus now to the performance of CTAs

do not. It is simply generally true that they base their

during different market environments. As any financial

trades on more than just prices.

market observer over the last two decades can attest,

Both types of managers can adopt relative value the market environment has varied greatly. The

strategies in their trading, meaning that they will take a environment in each market period has presented

long position in one instrument or market and a short different challenges to each asset class and strategy of

position in another. In such a case, each strategy will be investing.

basing their trade on the expectation that the spread

Although the division of the last twenty years into

between the instruments will tighten or widen,

different sub-periods is somewhat arbitrary, we have

depending on the type of position they have taken.

chosen to delineate the different environment into

Even in this case, however, the focus of their analysis

periods marked by crises. For that reason we chose the

will be different. CTAs generally will be focused on

following periods to examine the performance of CTAs:

historical relationships between the two instruments

themselves, while global macro traders will base their 1990-1998—the run-up to the Russian/Asian debt

judgments on spread widening or tightening on crises

macroeconomic relationships. 1998-2007—the period between the above crisis

Despite these differences in approach, however, for and the global financial crisis

both types of managers, the prices that both types of 2007-2012—the global financial crisis and its

managers observe and at which they trade are aftermath.

influenced by the same set of factors. Some CTAs might

Chart 2 depicts the performance of CTAs with respect to

not look at macroeconomic data, and some global other asset classes and to hedge funds generally in each

Chart 2: 1990-1998 1998-2007 2007-2012

20% 20% 16%

S&P

18% HFRI 18% 14%

500 TR

16% Index 16%

14% GSCI 12%

14% HFRI

12% Total 10% Bond

Compound ROR

Compound ROR

10% 12% Index Return

Barclay Barclay

Compound ROR

8% Index

8% 10% Bond CTA

CTA GSCI

6% Bond Index 8% Index 6% Index

Total Barclay S&P 500

4% Index 6% 4% S&P

Return TR GSCI

2% 4% CTA 500 TR

2% Total

0% Index HFRI

2% Return

-2% 0% Index

-4% 0%

-2% 0% 10% 20% 30%

-6% -2% 0% 10% 20% 30%

-4% -4%

0% 5% 10% 15% 20%

-6% -6%

Standard Deviation Standard Deviation Standard Deviation

4. of these two periods. In the first two periods, CTAs alpha that CTAs produce—that is the uncorrelated

produced a comparable compound returns to bonds, return relative to the benchmark under comparison—is

but with somewhat higher volatility. In all three periods, significant across the board. These data are monthly

CTAs produced lower volatility than either equities or numbers, so for example, from 2007-2012, CTAs

commodities. In the third period, CTAs have produced a monthly uncorrelated return of 0.4 percent

outperformed equities, commodities and hedge funds relative to the S&P 500.

overall. It is interesting to note that the risk and return

Table 2: Diversification benefits of CTAs

performance of CTAs has been much more stable during

Barclays GSCI HFRI Fund

these periods than have equities, commodities or S&P Aggregate Total Weighted

overall hedge funds. These charts demonstrate that 500 TR Bond Index Return Composite Index

while it is true that CTAs do not always outperform 1990-1998

Correlation -8.9% 14.0% 13.1% -10.8%

standard asset classes or hedge funds, the performance

Alpha 0.8% 0.4% 0.7% 0.9%

of the strategy overall is much more similar to the

1998-2007

performance of bonds than are other strategies.

Correlation -22.6% 27.9% 27.9% -3.7%

Diversification benefits of CTAs Alpha 0.5% 0.1% 0.4% 0.5%

2007-2012

A number of analyses have focused on the

Correlation -6.0% 0.8% 19.3% 18.9%

diversification benefits of CTAs in an overall portfolio.

Alpha 0.4% 0.4% 0.4% 0.4%

We focus here on two indicators of this diversification

benefit—correlation and alpha.

Final thoughts

Table 2 presents these two statistics for the same three

time periods as in the risk-return comparison above. As In this article we have shown how CTAs compare as an

the table shows, CTAs have exhibited a low or negative investment strategy to global macro hedge fund

correlation to equities in all three periods that we strategies. In general, CTAs can be considered either a

examine. CTAs are also negatively correlated to a broad substitute or a complement to global macro

hedge fund index in two of the three periods—the strategies—despite the differences in the approaches—

aftermath of the global financial crisis being the because the instruments they trade are responding to

exception. CTAs also show a low correlation to both the same conditions in the global economy. We have

bonds and commodities in all three periods. Recent also seen how the performance and diversification

months represent examples of the lack of correlation. In characteristics of CTAs can add value in an overall asset

May, when the S&P 500 Index was down 6.1 percent, allocation. We have also seen that over the period since

the Barclay CTA Index rose 2.7%; In contrast, for June 1990, the performance of CTAs contrasts with the

the CTA Index fell 1.62% whereas the S&P rose 4.1 performance of commodities in having lower volatility.

percent. The staff of Hedgeharbor will be glad to discuss further

As more evidence that CTAs provide diversification, the how one or more CTA managers can add benefit an

alpha that they produce relative to other investments is existing portfolio—whether or not it already contains a

significant in each of the time periods we consider. The hedge fund allocation. We look forward to discussing

this issue further.