BGSA on the GENCO Acquisition of ATC

•

0 j'aime•135 vues

BG Strategic Advisors (BGSA) analyzes the GENCO acquisition of ATC. Issues include the strategic rationale, technology, valuation, and other key factors.

Recommandé

Recommandé

Contenu connexe

Similaire à BGSA on the GENCO Acquisition of ATC

Similaire à BGSA on the GENCO Acquisition of ATC (20)

Plus de Benjamin Gordon

Plus de Benjamin Gordon (20)

Dernier

Dernier (20)

BGSA on the GENCO Acquisition of ATC

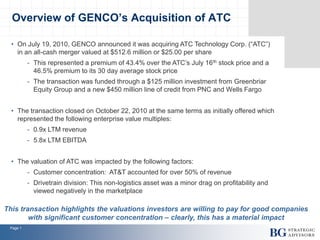

- 1. Page 1 • On July 19, 2010, GENCO announced it was acquiring ATC Technology Corp. (“ATC”) in an all-cash merger valued at $512.6 million or $25.00 per share - This represented a premium of 43.4% over the ATC’s July 16th stock price and a 46.5% premium to its 30 day average stock price - The transaction was funded through a $125 million investment from Greenbriar Equity Group and a new $450 million line of credit from PNC and Wells Fargo • The transaction closed on October 22, 2010 at the same terms as initially offered which represented the following enterprise value multiples: - 0.9x LTM revenue - 5.8x LTM EBITDA • The valuation of ATC was impacted by the following factors: - Customer concentration: AT&T accounted for over 50% of revenue - Drivetrain division: This non-logistics asset was a minor drag on profitability and viewed negatively in the marketplace Overview of GENCO’s Acquisition of ATC This transaction highlights the valuations investors are willing to pay for good companies with significant customer concentration – clearly, this has a material impact

- 2. Page 2 Historical Trading Levels 1.0x 2.0x 3.0x 4.0x 5.0x 6.0x 7.0x 8.0x ATC has predominantly traded at a range of 2.0 to 5.0x over the past three years. Over that time period, the average enterprise value to EBITDA is 4.7x. EnterpriseValuetoLTMEBITDA Average = 4.7x