Kalorama Information Report - Global Market for Medical Devices

•

1 j'aime•2,064 vues

The global medical device market is expected to grow steadily between 2013 and 2018. In 2013, the market was valued at around $300 billion. Major challenges facing the industry include reimbursement reductions, new taxes, and regulatory changes. Device companies are responding by innovating new products, finding new markets, and acquiring competitors. The top 18 companies earn most of the global revenue, with Johnson & Johnson, GE Healthcare, and Medtronic as the largest players by market share.

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (19)

Similaire à Kalorama Information Report - Global Market for Medical Devices

Similaire à Kalorama Information Report - Global Market for Medical Devices (20)

Plus de Bruce Carlson

Plus de Bruce Carlson (13)

Dernier

Dernier (20)

Kalorama Information Report - Global Market for Medical Devices

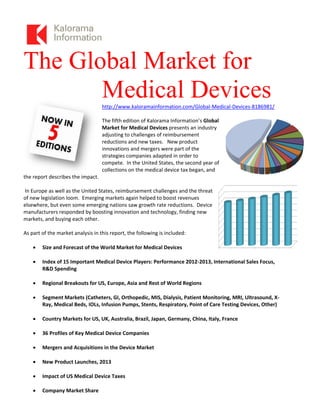

- 1. The Global Market for Medical Deviceshttp://www.kaloramainformation.com/Global-Medical-Devices-8186981/ The fifth edition of Kalorama Information’s Global Market for Medical Devices presents an industry adjusting to challenges of reimbursement reductions and new taxes. New product innovations and mergers were part of the strategies companies adapted in order to compete. In the United States, the second year of collections on the medical device tax began, and the report describes the impact. In Europe as well as the United States, reimbursement challenges and the threat of new legislation loom. Emerging markets again helped to boost revenues elsewhere, but even some emerging nations saw growth rate reductions. Device manufacturers responded by boosting innovation and technology, finding new markets, and buying each other. As part of the market analysis in this report, the following is included: Size and Forecast of the World Market for Medical Devices Index of 15 Important Medical Device Players: Performance 2012-2013, International Sales Focus, R&D Spending Regional Breakouts for US, Europe, Asia and Rest of World Regions Segment Markets (Catheters, GI, Orthopedic, MIS, Dialysis, Patient Monitoring, MRI, Ultrasound, X- Ray, Medical Beds, IOLs, Infusion Pumps, Stents, Respiratory, Point of Care Testing Devices, Other) Country Markets for US, UK, Australia, Brazil, Japan, Germany, China, Italy, France 36 Profiles of Key Medical Device Companies Mergers and Acquisitions in the Device Market New Product Launches, 2013 Impact of US Medical Device Taxes Company Market Share

- 2. Kalorama Information considers estimates of manufacturer revenues the most important and valid methodology for business planning. In many of the largest device markets, Kalorama Information has already conducted studies and has examined manufacturer revenue estimates, rendering the total market visible. This report was assembled using data from Kalorama Information's previous medical device reports. Primary and secondary research was used. Research into company annual reports, trade publications, government and medical literature was used as a foundation. Interviews with executives at medical device companies were conducted and are the key source of estimates. http://www.kaloramainformation.com/Global-Medical-Devices-8186981/

- 3. Global Market for Medical Devices, 5th Ed. 5th

- 4. Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. THE GLOBAL MARKET FOR MEDICAL DEVICES, 5TH EDITION A KALORAMA INFORMATION MARKET INTELLIGENCE REPORT The Global Market for Medical Devices has been prepared by Kalorama Information. We serve business and industrial clients worldwide with a complete line of information services and research publications. Kalorama Information Market Intelligence Reports are specifically designed to aid the action-oriented executive by providing a thorough presentation of essential data and concise analysis. www.kaloramainformation.com

- 5. Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. T A B L E O F C O N T E N T S CHAPTER ONE: EXECUTIVE SUMMARY.........................................................................................1 Top Companies........................................................................................................................................2 Mergers and Acquisitions.......................................................................................................................4 Medical Device Tax.................................................................................................................................4 Scope and Methodology..........................................................................................................................6 Conclusions..............................................................................................................................................6 CHAPTER TWO: INTRODUCTION......................................................................................................8 Definition .................................................................................................................................................8 Regulation in the US ...............................................................................................................................8 Classification of Medical Devices ........................................................................................................8 510(k) Process.....................................................................................................................................12 Regulation in the European Union......................................................................................................13 Regulation in Japan ..............................................................................................................................15 Regulation in China ..............................................................................................................................16 Trends in World Demographics ..........................................................................................................17 Global Aging Population ......................................................................................................................19 Group Purchasing Organizations........................................................................................................20 Unique Device Identifier (UDI)............................................................................................................22 UDI Rule and GUDID Guidance........................................................................................................23 Healthcare Reform and Taxes.............................................................................................................26 Expedited Access Premarket Approval ..............................................................................................27 Hospital Market Update.......................................................................................................................28 A Look at Representative Hospital Chains.........................................................................................29 Medical Device Tax...............................................................................................................................33 CHAPTER THREE: MERGERS AND ACQUISITIONS ...................................................................35 Significant Device Industry M&As .....................................................................................................35 Zimmer-Biomet...................................................................................................................................35 Boston Scientific.................................................................................................................................35 Stryker Makes Several Buys...............................................................................................................36

- 6. Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. CareFusion..........................................................................................................................................36 Thermo Fisher and Life ......................................................................................................................37 J&J Sells Clinical Diagnostics............................................................................................................37 Medtronic............................................................................................................................................37 CHAPTER FOUR: SPECIFIC DEVICE MARKETS ..........................................................................42 Market Size, Specific Medical Devices................................................................................................42 Catheters................................................................................................................................................45 Gastrointestinal Devices .......................................................................................................................45 Orthopedics ...........................................................................................................................................46 Minimally Invasive Surgery.................................................................................................................47 Patient Monitoring................................................................................................................................48 Dialysis ...................................................................................................................................................48 MRI ........................................................................................................................................................49 Ultrasound .............................................................................................................................................50 Medical Beds..........................................................................................................................................51 X-Ray Markets......................................................................................................................................52 Intraocular Lens Devices......................................................................................................................53 Infusion Pumps......................................................................................................................................53 Point Of Care Tests...............................................................................................................................54 Stents......................................................................................................................................................55 Respiratory Devices ..............................................................................................................................56 CHAPTER FIVE: BELLWETHER COMPANIES ..............................................................................57 Revenue Performance – 15 Bellwether Companies ...........................................................................58 US versus International sales...............................................................................................................60 Investment in Research and Development..........................................................................................61 CHAPTER SIX: MARKET ANALYSIS................................................................................................63 Size and Growth....................................................................................................................................63 Market by Region .................................................................................................................................64 Market by Country...............................................................................................................................69 Revenues of Top Companies................................................................................................................70 CHAPTER SEVEN: COMPANY PROFILES.......................................................................................73 Johnson & Johnson...............................................................................................................................73 GE Healthcare.......................................................................................................................................75

- 7. Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Siemens Healthcare...............................................................................................................................77 Company Overview ............................................................................................................................77 Product Launches................................................................................................................................77 Medtronic...............................................................................................................................................79 Company Overview ............................................................................................................................79 Product Launches................................................................................................................................79 Acquisitions ........................................................................................................................................80 Baxter International .............................................................................................................................81 Company Overview ............................................................................................................................81 Product Launches................................................................................................................................81 Acquisitions ........................................................................................................................................82 Philips Healthcare.................................................................................................................................83 Company Overview ............................................................................................................................83 Cook Medical.........................................................................................................................................84 Product Launches................................................................................................................................84 Covidien .................................................................................................................................................86 Company Overview ............................................................................................................................86 Product Launches................................................................................................................................86 Acquisitions ........................................................................................................................................87 Becton Dickinson &Co. ........................................................................................................................88 Company Overview ............................................................................................................................88 Product Launches................................................................................................................................88 B. Braun.................................................................................................................................................90 Company Overview ............................................................................................................................90 Product Launches................................................................................................................................90 St. Jude Medical....................................................................................................................................91 Company Overview ............................................................................................................................91 Product Launches................................................................................................................................91 Acquisitions ........................................................................................................................................92 Mindray Medical...................................................................................................................................93 Company Overview ............................................................................................................................93 Product Launches................................................................................................................................93

- 8. Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Hill-Rom.................................................................................................................................................94 Company Overview ............................................................................................................................94 Product Launches................................................................................................................................94 Acquisitions ........................................................................................................................................95 3M Healthcare.......................................................................................................................................96 Company Overview ............................................................................................................................96 Acquisitions ........................................................................................................................................97 Toshiba Medical Systems .....................................................................................................................98 Company Overview ............................................................................................................................98 Product Launches................................................................................................................................98 Acquisitions ........................................................................................................................................99 Smith &Nephew, Plc...........................................................................................................................100 Company Overview ..........................................................................................................................100 Acquisitions ......................................................................................................................................101 Product Launches..............................................................................................................................101 Hospira.................................................................................................................................................102 Company Overview ..........................................................................................................................102 Acquisitions ......................................................................................................................................103 Fresenius Medical ...............................................................................................................................104 Company Overview ..........................................................................................................................104 Boston Scientific..................................................................................................................................105 Company Overview ..........................................................................................................................105 Product Launches..............................................................................................................................105 CR Bard...............................................................................................................................................107 Company Overview ..........................................................................................................................107 Stryker Corporation ...........................................................................................................................109 Company Overview ..........................................................................................................................109 Acquisitions ......................................................................................................................................109 Product Launches..............................................................................................................................110 CareFusion...........................................................................................................................................112 Company Overview ..........................................................................................................................112 Acquisition........................................................................................................................................112 Product Launches..............................................................................................................................113

- 9. Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Thermo Fisher Scientific Inc..............................................................................................................114 Company Overview ..........................................................................................................................114 Acquisition........................................................................................................................................115 Product Launches..............................................................................................................................115 Terumo Corporation ..........................................................................................................................116 Company Overview ..........................................................................................................................116 Cardinal Health...................................................................................................................................117 Company Overview ..........................................................................................................................117 Acquisitions ......................................................................................................................................117 Biomet ..................................................................................................................................................118 Company Overview ..........................................................................................................................118 Acquisition........................................................................................................................................119 Product Launches..............................................................................................................................119 Dentsply ...............................................................................................................................................120 Company Overview ..........................................................................................................................120 Product Launches..............................................................................................................................121 Coloplast ..............................................................................................................................................122 Company Overview ..........................................................................................................................122 Product Launches..............................................................................................................................123 Paul Hartmann AG.............................................................................................................................124 Company Overview ..........................................................................................................................124 Teleflex Inc. .........................................................................................................................................126 Company Overview ..........................................................................................................................126 Acquisitions ......................................................................................................................................127 Product Launches..............................................................................................................................127 Haemonetics.........................................................................................................................................128 Company Overview ..........................................................................................................................128 Acquisitions ......................................................................................................................................129 Product Launches..............................................................................................................................129 Zimmer.................................................................................................................................................130 Company Overview ..........................................................................................................................130 Acquisitions ......................................................................................................................................130

- 10. Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Varian Medical Systems.....................................................................................................................131 Company Overview ..........................................................................................................................131 Product Launch .................................................................................................................................132 PerkinElmer, Inc.................................................................................................................................133 Company Overview ..........................................................................................................................133 Nobel Biocare ......................................................................................................................................134 Company Overview ..........................................................................................................................134 Product Launches..............................................................................................................................134 Olympus Medical Systems..................................................................................................................136

- 11. Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. L I S T O F E X H I B I T S CHAPTER ONE: EXECUTIVE SUMMARY.........................................................................................1 Figure 1-1: Global Medical Device Market, 2013-2018.......................................................................2 Figure 1-2: Medical Device Market Share, 2013..................................................................................3 Table 1-1: Medical Device Excise Tax Payment of Selected Industry Leaders, 2013.......................5 TWO: INTRODUCTION ..........................................................................................................................8 Table 2-1: 2013 FDA Device Approvals..............................................................................................11 Table 2-2: World Population, 2010 - 2050 ..........................................................................................18 Table 2-3: Percent Population Over 65, 2010-2050............................................................................19 Table 2-4: GPOs in the United States..................................................................................................21 Figure 2-1: Example of a Simulated Unique Device Identifier (UDI) ..............................................23 Table 2-5: Compliance Dates for UDI Requirements........................................................................25 Figure 2-2: Number of Hospitals in the US, 1975-2011 .....................................................................28 Figure 2-3: HCA Corporation: Revenues, Salary Costs, Bad Debt..................................................29 Figure 2-4: Community Health Hospitals Corporation: Revenues, Salary Costs, Bad Debt.........30 Figure 2-5: Net Income, HCA and Community Health.....................................................................31 Table 2-6: Leading For-Profit U.S. Hospital Chains, 2008 and 2010...............................................32 Table 2-7: Medical Device Excise Tax Payment of Selected Industry Leaders, 2013.....................33 THREE: MERGERS AND ACQUISITIONS........................................................................................35 Table 3-1: Mergers and Acquisitions in the Medical Device Market, 2013-2014............................39 FOUR: SPECIFIC DEVICE MARKETS...............................................................................................42 Figure 4-1: Medical Device Market Share by Category...................................................................43 Table 4-1: Markets for Medical Devices, 2013...................................................................................44 FIVE: BELLWETHER COMPANIES...................................................................................................57 Table 5-1: Revenue Performance, Bellwether Companies, 2013 vs. 2012 .......................................58 Table 5-2: Revenue Performance, Bellwether Companies’ Growth Rates, 2013............................59 Table 5-3: Percent of Sales from US, 2013 and 2012 .........................................................................60 Table 5-4: Research and Development Spending, Bellwether Companies ......................................61 Table 5-5: Research and Development Spending as a Percentage of Revenues, Bellwether Companies..........................................................................................................................62 SIX: MARKET ANALYSIS ....................................................................................................................63 Figure 6-1: Medical Device Market, 2013-2018 .................................................................................64

- 12. Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Figure 6-2: Medical Device Market by Region, 2013.........................................................................65 Figure 6-3: US Market Forecast, 2013-2018.......................................................................................67 Table 6-1: Significant Country Device Markets (US, UK, Australia, Brazil, Japan, Germany, China, Italy, France).............................................................................................................................69 Table 6-2: Top Medical Device Company Revenues, FY 2013 .........................................................71 Figure 6-4: Estimated Market Share of Medical Device Market by Competitor ...........................72

- 13. C H A P T E R O N E Executive Summary The fifth edition of Kalorama Information’s Global Market for Medical Devices finds a market with tremendous opportunity for a range of device makers, but also a number of challenges. In the United States, the second year of collections on the medical device tax began. In Europe as well as the United States, reimbursement challenges and the threat of new legislation loom. Emerging markets again helped to boost sagging revenues elsewhere, but even some emerging nations saw declines. Device manufacturers responded by boosting innovation and technology, finding new markets, and buying each other. Because of the broad definition, estimates of medical device markets vary as any item from a nuclear camera or catheter to a latex glove can be considered a medical device. It is a scattered market in which hundreds of companies worldwide participate. Despite this, not more than forty companies earn most of the revenue in the market and much of the revenue is earned in a few key categories. The medical device market in terms of revenues is not even half as large as the global pharmaceutical market, though it sees many more transactions. This is due to pricing, as in volume terms there are more units sold and more patients are impacted by the device market. Although the largest component of the market is in the United States, the majority of sales are non-US, and growth is occurring in other markets. Chapter Six of this report breaks down the overall market by region.

- 14. One: Executive Summary 2 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Figure 1-1 Global Medical Device Market TOP COMPANIES Because of the variety of types of medical devices, there are many competitors. Still eighteen companies earn most of the global revenue in the device market. Most companies operate in just a few markets, though the top companies such as J&J, GE Healthcare, Siemens and Medtronic are multi-billion dollar companies that operate in several categories. There are thousands of companies making devices in the United States alone, most of these are private concerns having less than 50 employees. The market share of the top medical device companies is provided in the following figure. 2013 2014 2015 2016 2017 2018

- 15. One: Executive Summary 3 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Figure 1-2 Medical Device Market Share, 2013 Major companies are profiled in Chapter Seven of this report. In Chapter Five, Kalorama has isolated 15 “bellwether” companies based on revenues and also diversity of medical devices produced. The results of the bellwethers between 2012 and 2013, the geographic breakout of their sales and their decisions on R&D spending are part of the analysis for the report’s findings on the market.

- 16. One: Executive Summary 4 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. MERGERS AND ACQUISITIONS In 2013 and early 2014, key market players were active in acquiring companies, among these were Boston Scientific, Stryker Corporation, CareFusion, ThermoFisher Scientfic, The Carlyle Group, and Medtronic. Stryker’s purchase of MAKO Surgical, Zimmer’s purchase of Biomet and the sale of J&J’s Ortho Clinical Diagnostic Group to the Carlyle Group were among the larger purchases. Chapter Three of this report focuses on merger activities. MEDICAL DEVICE TAX The beginning of 2013 saw the medical device industry make the first payments to the IRS for the new 2.3% excise tax on all classes of medical devices as part of the 2009 Patient Protection and Affordable Care Act (referred to in this report as US healthcare reform). Medical device manufacturers have to date paid an estimated $1 billion to the Internal Revenue Service for the medical device excise tax, according to the Medical Imaging & Technology Alliance (MITA), the Advanced Medical Technology Association (AdvaMed) and the Medical Device Manufacturers Association (MDMA), the tax costing an estimated average of $194 million per month by device manufacturers in an industry that spends nearly $10 billion in R&D each year. Net income was broadly impacted in 2013, though the actual amounts vary. Table 1-1 shows the medical device excise tax payment totals of selected industry leaders. Johnson & Johnson, the largest device company, paid $200 million, which was recorded in selling, marketing and administrative expenses.

- 17. One: Executive Summary 5 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Table 1-1 Medical Device Excise Tax Payment of Selected Industry Leaders, 2013 Company Payment Johnson & Johnson $200 million Boston Scientific $73 million Covidien $60 million Smith & Nephew $24 million Hill-Rom $12.3 million Source: Kalorama Information Clearly, the amount of money being paid is substantial. The initial feeling within the industry was that this level of taxation would deny manufacturers opportunities to invest in R&D, to make capital investments, and to increase staffing. The reality of the tax is reflected in a survey by the Emergo Group, in which 45% of senior managers indicated that the tax has had a "very" or "somewhat negative" impact on their business in 2013, while 34% indicated that it had "no impact." Though the growth of small players in the market is likely hurt by the tax, Kalorama Information estimates that the tax impact was 20 to 30% less than the projections of industry commentators and corporate reports. Bipartisan support for repeal of the tax is building in both the House of Representatives and the Senate, according to the Medical Imaging & Technology Alliance (MITA). In the House and Senate, bipartisan majorities support repeal of the device tax. In March, a coalition of 79 Senators reached across the aisle in a vote to adopt an amendment to the Fiscal Year 2014 Senate Budget Resolution repealing the medical device tax. Reps. Erik Paulsen (R-MN) and Ron Kind

- 18. One: Executive Summary 6 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. (D-WI) introduced in the House the “Protect Medical Innovation Act,” which garnered a bipartisan response that has increased to 253 co-sponsors. SCOPE AND METHODOLOGY There are many estimates of the medical device market as a whole that have been published using various methodologies; export and import sales, unit estimates and price averaging, but Kalorama Information considers estimates of manufacturer revenues the most important and valid methodology for business planning. In many of the largest device markets, Kalorama Information has already conducted studies and has examined manufacturer revenue estimates, rendering the total market visible. This report was assembled using data from Kalorama Information's previous medical device reports. Primary and secondary research was used. Research into company annual reports, trade publications, government and medical literature was used as a foundation. Interviews with executives at medical device companies were conducted and are the key source of estimates. CONCLUSIONS The following are the major conclusions of the report: The global market for medical devices was billion dollars in 2013. With average growth, this should grow to $ billion in 2018. A majority of companies in Kalorama’s Bellwether index of medical device companies increased research and developing spending as a percentage of revenue. For most device companies, migration from US sales continues. On a revenue basis, companies earned of their total revenues from United States customers. The average of our device company index was a % increase in non-US sales, though some companies were well beyond this average. The “Rest of World” market (all areas outside of the US, Europe and Asia) represents % of the world device market. Growth in healthcare spending in

- 19. One: Executive Summary 7 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. countries such as Brazil, Turkey, South Africa, Chile, Mexico and others drove the market. Expect more device companies to focus on these import-heavy markets. Respiratory Equipment, Catheters, Patient Monitoring and Dental Equipment are the largest categories of medical devices. IOLs, stents, molecular tests, and cosmetic products were the most common categories of new devices approved last year.

- 20. C H A P T E R T W O Introduction DEFINITION Medical devices include any instrument, apparatus, appliance, machine, contrivance, implant, in-vitro device as well as any accessories or related components that facilitate any or some of the following functions pertaining to a disease, injury, or condition of handicap: diagnosis, prevention or monitoring, treatment. The following conditions apply to our definition. It should be regulated by a state regulatory authority. It should be intended for application in the prevention, diagnosis, and/or cure of disease or other conditions such as an injury or a handicap. It should not achieve any of the above intended applications by chemical action and/or metabolism activity within or on the body. REGULATION IN THE US Classification of Medical Devices Medical devices are typically classified into three classes based on the risk associated with them. This classification was originally provided by the US Food and Drug Administration (US FDA), and similar classifications are followed by major Asian countries such as Japan and China. These classifications signify the level of control required to ensure the safety and effectiveness of the device. Consequently, manufacturers of the different classes need to adhere

- 21. Two: Introduction 9 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. to different levels of regulations and norms, i.e., stringent regulations for higher class of medical devices: Class I: This class includes medical devices that pose minimum risk to a patient and are simpler in design as compared to Class II and Class III medical devices. Class I devices are classified in the ‘general controls’ category, as specified by the US FDA, and include devices such as tongue depressors, bedpans, elastic bandages, examination gloves, hand-held surgical instruments and X-ray film. The manufacturing and distribution of medical device products in this class generally requires: Class II: According to the US FDA, Class III devices are subject to ‘special controls’ in addition to ‘general controls’. These devices require a higher level of safety assurance in terms of potential injury or other harm to the patient. Devices in this class include X-ray machines, powered wheelchairs, infusion pumps, surgical drapes and ultrasonic diagnostic devices. In addition to Class I requirements, the manufacturing and distribution of medical device products in this class generally entails the following: Special labeling requirements Compliance with performance standards Post-market surveillance Pre-market approval may be required Class III: Devices in this class require the highest level of safety and effectiveness assurance as the potential threat to the patient is highest in their case. Information availability regarding the safety aspect of these devices is generally limited as compared to Class I and Class II devices; and these, therefore, require additional safety measures after ‘general controls’ and ‘special controls’. Medical devices in this category include life-supporting or life-sustaining devices, such as replacement heart valves, implanted cerebellar stimulators, implantable pacemaker pulse generators, endosseous (intra-bone) implants, etc. In addition to Class I and Class II requirements, the manufacture and supply of these devices entails the following: A scientific review to ensure the safety and effectiveness of a device Pre-market approval (mandatory) In some countries, a device-tracking system to maintain and update information about the recipients of the device is necessary for certain Class III devices such as implantable pacemakers.

- 22. Two: Introduction 10 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. In the United States, the Food and Drug Administration (FDA) requires manufacturers of clinical devices that may have a negative consequence on the patients’ health with improper use to prove both the device is safe and it is effective prior to sale. However, some policymakers and device manufacturers have labeled U.S. device regulation as slow, risk-averse, and expensive. FDA's Center for Devices and Radiological Health (CDRH) is responsible for regulating firms who manufacture, repackage, relabel, and/or import medical devices sold in the United States. In addition, CDRH regulates radiation-emitting electronic products (medical and non- medical) such as lasers, x-ray systems, ultrasound equipment, microwave ovens and color televisions. Manufacturers (both domestic and foreign) and initial distributors (importers) of medical devices must register their establishments with the FDA. All establishment registrations must be submitted electronically unless a waiver has been granted by FDA. All registration information must be verified annually between October 1st and December 31st of each year. In addition to registration, foreign manufacturers must also designate a U.S. Agent. Most class I devices, such as blood pressure monitors are low level-risk and subject only to “general controls,” Class II devices meet general controls as well as “special controls,” such as additional labeling requirements. These moderate-risk devices generally pass through the 510(k) review pathway, which refers to the section of the Food, Drug, and Cosmetic Act dealing with premarket notification. In this process, the FDA and the manufacturer rely on similarities between the device at issue and a previously cleared device. Products requiring PMAs are Class III devices are high risk devices that pose a significant risk of illness or injury, or devices found not substantially equivalent to Class I and II predicate through the 510(k) process. The PMA process is more involved and includes the submission of clinical data to support claims made for the device. An investigational device exemption (IDE) allows the investigational device to be used in a clinical study in order to collect safety and effectiveness data required to support a Premarket Approval (PMA) application or a Premarket Notification 510(k) submission to FDA. Clinical studies with devices of significant risk must be approved by FDA and by an Institutional Review Board (IRB) before the study can begin. Studies with devices of nonsignificant risk must be approved by the IRB only before the study can begin. The following table provides information on recent FDA device approvals. Stents, IOLs and molecular testing were among the larger categories of newly approved devices.

- 23. Two: Introduction 11 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Table 2-1 2013 FDA Device Approvals Device Name Category Date Therapy™ Cool Flex™ Ablation Catheter and IBI 1500T9-CP v.1.7 Cardiac Ablation Generator - P110016/S0081 Catheter 12/18/2013 GORE® VIABAHN® Endoprosthesis, GORE® VIABAHN® Endoprosthesis with Heparin BioActive Surface - P1300062 Stent 12/5/2013 RNS® System - P1000263 Epilepsy 11/14/2013 MitraClip Clip Delivery System – P1000094 Heart Valve Device 10/24/2013 Juvéderm Voluma XC - P1100335 Implant 10/22/2013 Nidek EC-5000 Excimer Laser System - P970053/S0116 LASIK 9/30/2013 Wavelight ALLEGRETTO WAVE® Eye-Q Excimer Laser - P020050/S0127 LASIK 9/27/2013 DIAMONDBACK 360® Coronary Orbital Atherectomy System - P1300058 Stent Delivery System 10/21/2013 Liposorber® LA-15 System - H1200059 Blood Processing 10/10/2013 MiniMed 530G System - P12001010 Glucose Monitor/Insulin Delivery 9/26/2013 Complete® SE Vascular Stent System - P11004011 Stent 9/19/2013 GORE TAG Thoracic Endoprosthesis - P040043/S05112 Endovascular Stent Graft 9/10/2013 Mobi-C® Cervical Disc Prosthesis (two-level) - P11000913 Cervical Disc Prosthesis 8/23/2013 Parascript® AccuDetect® 6.1.0 - P12000414 Computer-Aided Detection (CAD) Software 8/22/2013 Nit-Occlud® PDA - P12000915 Occluder 8/16/2013 Mobi-C® Cervical Disc Prosthesis – P11000216 Cervical Disc Prosthesis 8/7/2013 therascreen® EGFR RGQ PCR Kit - P12002217 Molecular Assay 7/12/2013 Abbott RealTime HCV Genotype II; Abbott RealTime HCV Genotype II Control Kit; and Uracil-N-Glycosylase (UNG) - P12001218 Lab Test 6/20/2013 MemoryShape Breast Implants - P06002819 Breast Implant 6/14/2013 THxID™ -BRAF Kit for use on the ABI 7500 Fast Dx Real- Time PCR Instrument - P12001420 Molecular Assay 5/29/2013 Trulign Toric Posterior Chamber Intraocular Lens and Trulign Toric IOL Calculator - P030002/S02721 Intraocular Lens (IOL) 5/20/2013 Selenia Dimensions 3D System - P080003/S00122 Mammography Device 5/16/2013 cobas® EGFR Mutation Test - P12001923 Lab Test 5/14/2013 SEDASYS® Computer-Assisted Personalized Sedation System - P08000924 Sedation 5/3/2013

- 24. Two: Introduction 28 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. 0 1000 2000 3000 4000 5000 6000 7000 8000 1975 1980 1990 1995 2000 2007 2011 7156 6965 6649 6291 5810 5708 5724 HOSPITAL MARKET UPDATE Community hospitals include nonfederal, short-term general, state specialty hospitals. Excluded are hospitals not accessible by the general public such as prison hospitals or college infirmaries. Large US-based hospitals benefit from economies of scale. They have lower costs per patient or per procedure because of volume discounts in purchases and other similar factors. Therefore, it has been observed that many hospitals have been merging to form a bigger group. Merged hospitals often find it easier to borrow money and make greater profits because of decreased competition. Figure 2-2: Number of Hospitals in the US, 1975-2011

- 25. Five: Bellwether Companies 60 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. US VERSUS INTERNATIONAL SALES For the past few years bellwether companies have seen a decline in US sales as they focus on international markets, especially the emerging BRIC nations. 2012 represented a slight stay of this trend as the US economy rebounded slightly and European nations began unusually large healthcare cuts that impacted the industry. 2013 demonstrated that this is a longstanding trend; US markets declined and most companies continued to seek outside the US markets. Table 5-3 Percent of Sales from US, 2013 and 2012 2013 2012 Johnson and Johnson GE Healthcare Medtronic Philips Boston Scientific Becton Dickinson Stryker St. Jude Medical B. Braun Siemens Hill-Rom Smith and Nephew Covidien CareFusion Fresenius Medical On a revenue basis, companies earned of their total revenues % US vs. US) from United States customers.

- 26. Five: Bellwether Companies 62 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Table 5-5 Research and Development Spending as a Percentage of Revenues, Bellwether Companies 2013 2012 Johnson and Johnson GE Healthcare Medtronic Philips Boston Scientific Becton Dickinson Stryker St. Jude Medical B. Braun Siemens Hill-Rom 4.1 4.0 Smith and Nephew 5.3 4.2 Covidien 1.9 1.7 CareFusion 4.8 4.5 *

- 27. Seven: Company Profiles 116 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. TERUMO CORPORATION Location: Shibuya, Tokyo, Japan Website: www.terumo.com Revenues 2013: Revenues 2012: ($ billions) Company Overview Terumo Corporation is a Japanese company founded in 1921 to design and make superior thermometers. Terumo today is broadly engaged in the manufacture and sales of medical products and equipment, its product lines including pharmaceuticals, nutritional food supplement, blood bags, disposable medical devices, cardiovascular systems, vascular grafts, peritoneal dialysis, blood glucose monitoring system, and medical electronic and digital thermometers. In addition to Japan, the company has established subsidiaries in numerous regions, including the US, India, China, and many European countries. The company’s revenues were approximately billion in 2013, an increase of 4% over 2012. In the cardiac & vascular segment, net sales increased by 5.7%; in the blood management segment, net sales increased by 4.1%; in the general hospital segment, net sales increased by 2.3%. In the area of coronary stents, Terumo Corporation markets the Nobori drugeluting stent, a version of Biosensors International’s BioMatrix stent, through a licensing agreement between the two companies. In October of 2012, Biosensors and Terumo extended the original licensing agreement for territories outside of Japan until December 2014. NOBORI 2 is the largest real- life registry of the Nobori® stent. The 3 year clinical results of the NOBORI 2 study show consistently low occurrence of clinical events throughout the trial. Given the NOBORI 2 three year results; the more than 20.000 patients studied in the NOBORI clinical program supports the safety and efficacy of the Nobori® stent. Endovascular coiling now accounts for fully 50% of neuroendovascular aneurysm treatments in Western countries. Some 30% of cases in Japan are treated by coiling, a share that continues to increase. Terumo figures prominently in this market.

- 28. Seven: Company Profiles 117 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. CARDINAL HEALTH Location: Dublin, OH Website: www.cardinal.com Revenues 2013: Revenues 2012: ($ millions) Company Overview Cardinal Health is a Fortune 19 healthcare services company specializing in the distribution of pharmaceuticals and medical products. Based in Dublin, Ohio, this company employs more than 30,000 people worldwide. Cardinal also manufactures medical and surgical products for ambulatory care centers, physician offices, clinical laboratories and hospitals. The company reported fiscal year 2013 revenues of $101 billion. The Cardinal Health medical segment manufactures high-volume replenishable products such as gloves, gowns, surgical drapes, scrubs, and fluid management product. They support the diagnostic industry by supplying surgical and procedural kitting operations that assemble single- use products and apparel for specific procedures in one kit. Among the products offered: Acquisitions Cardinal Health has announced the completion of the acquisition of AccessClosure, a leading manufacturer and distributor of extravascular closure devices in the United States. The $320 million acquisition was an all-cash transaction. - DuraBlue™ sterilization wrap is double-layered, with a securely bonded seal on three sides, and made with non-woven 100% polypropylene SMS technology for superior strength and microbial protection. - The Pulse Wave® laparoscopic suction/irrigation system is lightweight and disposable and designed to enhance speed, efficiency and ease of use during surgery. - The Protexis™ brand of surgical gloves designed to enable natural hand movement. - The Medi–Vac® portfolio of products suction and fluid collection products.

- 29. Seven: Company Profiles 118 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. BIOMET Location: Warsaw, IN Website: www.biomet.com Revenues 2013: Revenues 2012: ($ billions) Company Overview In May of 2014, Biomet’s Boards of Directors approved a definitive agreement under which Zimmer will acquire Biomet for $ billion. The transaction, which is subject to customary closing conditions and regulatory approvals, is expected to close in the first quarter of 2015. The merger of Zimmer and Biomet will position the combined company as a leader in the $ billion musculoskeletal. Biomet, established in 1977 and located in Warsaw, Indiana, is one of the world’s leading medical device manufacturers. The company specializes in reconstructive products for hips, knees and shoulders, fixation devices, orthopedic support devices, dental implants, spinal implants and operating room supplies. In 2013, the company’s revenues approached $3.1 billion. During 2013, E1® Antioxidant Infused Technology Tibial Bearings continued to receive strong market acceptance. The E1® technology provides Vitamin E infused highly cross-linked polyethylene, which is designed to offer strength and oxidative stability for implant longevity, helping Biomet to remain a market leader for products accommodating minimally-invasive knee techniques. The Oxford® Partial Knee, which was introduced in the United States during 2005 and has been commercially available in Europe for 35 years, is currently the only free-floating meniscal bearing unicompartmental knee system approved by the FDA. Biomet’s offering of minimally-invasive partial knee systems also includes the Alpina™ Unicompartmental Knee (which is not currently available in the United States); the Vanguard M™ Series Unicompartmental Knee System, a modified version of the Oxford® Partial Knee that incorporates a fixed-bearing tibial component as opposed to a free-floating tibial bearing; and the Repicci II® Resurfacing Knee System.

- 30. Seven: Company Profiles 119 Copyright © 2014 Kalorama Information, LLC. Reproduction without prior written permission, in any media now in existence or hereafter developed, in whole or in any part, is strictly prohibited. Acquisition Prior to its acquisition by Zimmer, Biomet was active in acquisitions in 2013. In October, Biomet announced agreement to acquire Lanx, Inc, a full service spine company and a leader in minimally invasive techniques and technologies. This expands Biomet Spine’s technology portfolio through the addition of innovative products currently offered by Lanx, including the Timberline® Lateral Approach Fusion System, and the Aspen® Minimally Invasive Fusion System. These products are complementary to Biomet Spine’s comprehensive offering of products, including the Lineum® OCT Spine System, MaxAn® Anterior Cervical Plate System, Cellentra™ VCBM and the Polaris™ Translation™ Screw System. Product Launches The first clinical use of the Signature™ Patient-Specific glenoid instrumentation in the United States took place in 2013. The Signature™ Glenoid System had been introduced in Europe in February 2013, and is used in conjunction with Biomet's Comprehensive® shoulder system, the market-leading shoulder replacement system in the United States. Signature™ glenoid guides utilize CT data and a proprietary algorithm to match each patient's anatomy and facilitate proper positioning of the glenoid component. The Signature™ Glenoid System is viewed as a significant advance in shoulder arthroplasty. Biomet launched in July of 2013 the ePAK™ Single-Use Delivery System, the latest in innovative technology for internal fracture fixation. The system is a pre-sterilized, single-use procedure pack that addresses distal radius fractures and features the DVR® Crosslock implant and instrumentation.