The document discusses concerns that led to the Fundamental Review of the Trading Book (FRTB). It summarizes that pre-FRTB there was unclear classification between banking and trading books allowing regulatory capital arbitrage. Risk measures also failed to fully capture risks like procyclicality, model risk for complex products, and comprehensive risks. The FRTB aims to address these issues with changes like standardized approaches, constraints on modeling, and convergence of prudential and accounting rules. It signals a strategic shift towards limiting internal modeling and preventing methodology arbitrage.

(INDIRA) Call Girl Mumbai Call Now 8250077686 Mumbai Escorts 24x7

CH&Cie - Fundamental Review of the Trading Book

1. Arbitrage opportunity Banking book vs Trading book

• The classification of assets between the banking book and trading book

was unclear allowing arbitrage opportunity for RWA optimization

• For instance, the credit risk component in the banking book is more

demanding in terms of RWA in comparison to the trading book

Volatility of capital assigned for trading positions

• Pro-cyclicality of market risk measures has been revealed in the past

few years, especially for banks using the advanced approach

• As a consequence, the volatility in capital assigned for trading positions

is a concern not in line with regulatory expectations

Model risk for structured and complex products

• The models used as well as the underlying assumptions were unable to

capture embedded risks in complex products

• Whether related to the use of historical data or the nature of the

products itself, model risk has been looked upon very closely

Comprehensive risks coverage

• Both regulatory constraints and internal processes failed to ensure a

comprehensive coverage of all embedded risks in trading positions

• The liquidity component of the trades had not been captured nor the

increasing credit risk components embedded in credit derivatives

Granularity, data quality and aggregation

• The level of granularity on which risk factors were monitored seemed

insufficient to fully capture real trends in the trading portfolios

• The aggregation of data (and its quality) introduced imperfections and

myopia in risk measures

Market Risk RWA Variability

• Following investigations led by the Basel Committee market risk RWA

vary significantly across jurisdictions and portfolios

• These variability could be explained (partially) by discrepancies by

modeling methodologies as well as the approaches (STD vs Adv.)

Multiple concerns behind the scenes that led to the FRTB

Obviously the past few years reshaped the convictions that were commonly acknowledged across the industry.

Besides these convictions, some new loopholes were brought to light by the extreme conditions, deemed

impossible, of the past crisis.

The trading book and the underlying instruments of trading portfolios have been subject to multiple

investigations in order to assess “what went wrong” (as mentioned by the Basel Committee).

The Fundamental review of the Trading Book opens a new era on regulatory perception of the embedded risks

in trading positions. More importantly, it shows a strategic reversal and the willingness of regulators for a

convergence between risk measurement methods (standardized approach vs advanced approach), an

integrated assessment of risk types (from a silo risk assessment to a more comprehensive risk identification)

and an alignment between prudential and accounting rules.

Fundamental Review of the

Trading Book

The purpose of the FRTB is to cover the shortcomings that

both regulatory constraints as well as internal risk processes

failed to capture during the crisis

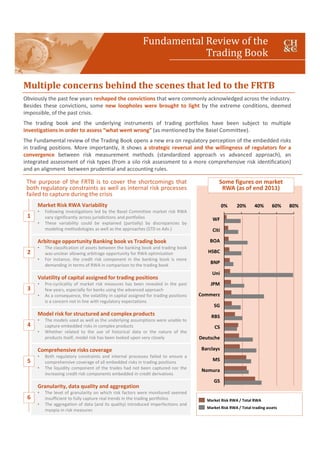

Market Risk RWA / Total RWA

Market Risk RWA / Total trading assets

1

2

3

4

5

6

40%20%

GS

0%

MS

Nomura

CS

Deutsche

Barclays

RBS

60% 80%

JPM

Commerz

SG

Uni

BNP

HSBC

BOA

Citi

WF

Some figures on market

RWA (as of end 2011)

2. These concerns are to be addressed by a redesign of the

trading portfolios and the risk measures…

The Fundamental Review of the Trading Book presents extensive reshape of the treatment of market

risk. Its redesign is multi-dimensional and ranges from operational implementation, to measurement

and methodologies, to documentation and clarifications…

Trading

book vs

banking

book

• Boundary and classification | The FRTB provides a clarification

on instruments classification and assignment between the banking and

the trading book. Besides providing a pre-defined list of instruments to

be assigned, institutions should provide operational criteria on the

intent of the instrument

Description Impact

• Rigidity of the classification:

once assigned the

reclassification is limited

• Operational constraints to

justify the classification

• Alignment between the books| The FRTB shows a clear

intention of a convergence between the treatment of the two books in

both directions. The treatment of default risk in the trading book is to

get closer to the banking book whereas interest rate risk in the banking

is to be measured in Pillar I (on-going) using a fair value measurement

of the balance sheet

• The intention is to

segregate the two books

while homogenizing the

treatment of risks

Risk

measurem

ent

• Standardized approach| Introduces a higher level of granularity

and bucket differentiation. Each bucket is assigned to a specific

formula. The diversification and hedging positions are better captured

via a revised correlation factor. Design of a method to better capture

various risks (interest rate, FX, equity, …). To be used as a floor

• Higher complexity that the

initial method

• However, it enhances the

transparency in measuring

risks at more granular levels

• Advanced approach| Using internal methods will be definied on a

more granular level via a P&L attribution method,etc… Risk

measurement is consequently done desk by desk. The methodology

relies on the Expected Shortfall (to replace the VaR) with a 97.5%

confidence level (vs 99% for the VaR). Calibration of risks in stress

conditions.

• Complexity in comparing

results related to the

attribution of methods by

desk. Some are eligible

other not eligible

• ES models can be complex

(use of EVT,…)

Framing

and

constraints

• Framing | Securitization positions are no more eligible to the

advanced approach. The Basel Committee imposes the use of the

standardized approach for all securitized positions

• Higher transparency at the

cost of higher RWA

• Constraints | Constraints are provided by the FRTB. A methodology

will be provided for choosing the stressed period. Correlation

parameters in the IDR charge might be constrained as well whereas

the horizons for VaR calculation ( 10 ൈ 1 െ ݀ܽ ܴܸܽ ݕ vs 10 െ

݀ܽ) ܴܸܽ ݕ are subject to similar types of guidance and constraints

• Higher impact on RWA

• Limits arbitrage related to

methodology and methods

This reveals a new tendency in regulatory requirements and the reversal in terms of limiting the ability

for banks in using internal approaches as well as framing methodology arbitrage

• Will this tendency be generalized

because of some discrepancies

that still exist between these

regulations ?

• Under this framework, what is

the relevance of using advanced

approaches?

• Are regulators pushing

(indirectly) for the use of the STD

approach?

• What about overlaps between

the various regulations?

• Are we heading for an over-

coverage of risks?

Convergence between

prudential and accounting rules

Integrated risk assessment

framework

Convergence between the

Standardized and the advanced

approach

Fundamental Review of the

Trading Book

3. Our expertise in the field can help you in various ways

CH&Co dedicated team is constituted of a balanced team of experts in Risk Modeling as well as

regulatory and accounting interpretation. The ability to both interpret the regulation (via benchmarks

and lobbying among the industry participants) and dispatch resources that can assist in quantifying

risks, allows to achieve quick results while being in line and compliant with regulatory requirements.

Our team can deliver the following:

1

2

3

4

5

6

Regulatory Watch & Interpretation

CH&Co has invested in dedicated to both follow-up on regulations and

their evolutions as well as to interpret them and provide our clients

with clear guidelines designed for in-house purposes to measure the

impact on banks’ organization, models, processes and businesses

Model Design

CH&Co Global Research & Analytics (GRA) team is constituted of

dedicated experts in risk modeling and quantification. They can support

in-house teams by both providing a higher workforce as well as

feedback on market best practices

Model Validation

We can assist as well on model validation. Our 15-year expertise in the

field allows providing our clients with added-value in terms of

regulators expectations on tests to be performed, standards to be

achieved and documentation to be put in place

Benchmark

CH&Co contributes to discussions across the industry around regulatory

evolutions and their impact on banks’ business models. CH&Co is also

active in responding to QIS as well as EBA discussions papers (for

instance “Future of the IRB Approach). Plus, CH&Co can deliver

benchmarks on the market best practices

Optimization

CH&Co has led multiple assignments and discussions on optimizing

RWAs in an environment with high pressure on ROEs and capital. The

areas for optimization are important but can’t be achieved without

difficulty. Therefore, managing risks in an integrated way (vs silo) is key

Support in strategic decisions

Multiple institutions are adapting their strategies to the evolutions in

regulations and the financial sector. CH&Co can provide decision-

making solutions by simulating impacts, projecting strategic and

business related items and facilitate communication with Senior

Management

CH&Co is also

active in publishing

articles and White

Papers. Our teams

try to answer

questions among

market participants

as well as work on

Research to

continually

enhance risk

measurement

methodologies.

Check out our

publications and

white papers on

our website:

http://www.chapp

uishalder.com/publ

ications/

Stéphane Eyraud, Partner & CEO

Tel UK: + 44 78 34 55 03 98

Tel FR: + 33 6 12 41 64 06

seyraud@chappuishalder.com

Benoit Genest, Partner & head of GRA

Tel FR: + 33 7 87 68 81 77

bgenest@chappuishalder.com

Ziad Fares, Manager GRA, R&D

Tel FR: + 33 6 62 96 25 00

zfares@chappuishalder.com

Fundamental Review of the

Trading Book