Ifrs 1 case study with q & a

•

3 j'aime•1,988 vues

1. The document provides reconciliation of equity and total comprehensive income from previous GAAP to IFRS as of April 1, 2010 and for the year ended March 31, 2011 for XYZ Ltd. 2. Significant adjustments include higher property, plant, and equipment, recognition of intangible assets and financial assets at fair value, inclusion of overhead in inventory, and recognition of pension liabilities and deferred taxes. 3. Total equity increased by Rs. 538 lakhs and total comprehensive income decreased by Rs. 111 lakhs primarily due to the above adjustments.

Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

En vedette (20)

Similaire à Ifrs 1 case study with q & a

Similaire à Ifrs 1 case study with q & a (20)

Plus de Hyderabad Chapter of ICWAI

Plus de Hyderabad Chapter of ICWAI (20)

Dernier

Dernier (20)

Ifrs 1 case study with q & a

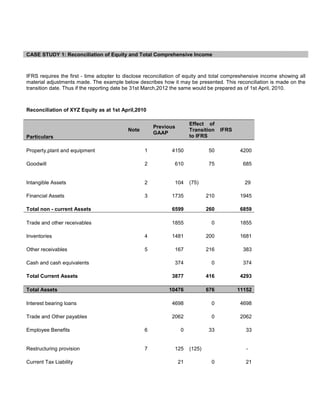

- 1. CASE STUDY 1: Reconciliation of Equity and Total Comprehensive Income IFRS requires the first - time adopter to disclose reconciliation of equity and total compreshensive income showing all material adjustments made. The example below describes how it may be presented. This reconciliation is made on the transition date. Thus if the reporting date be 31st March,2012 the same would be prepared as of 1st April, 2010. Reconciliation of XYZ Equity as at 1st April,2010 Effect of Previous Note Transition IFRS GAAP Particulars to IFRS Property,plant and equipment 1 4150 50 4200 Goodwill 2 610 75 685 Intangible Assets 2 104 (75) 29 Financial Assets 3 1735 210 1945 Total non - current Assets 6599 260 6859 Trade and other receivables 1855 0 1855 Inventories 4 1481 200 1681 Other receivables 5 167 216 383 Cash and cash equivalents 374 0 374 Total Current Assets 3877 416 4293 Total Assets 10476 676 11152 Interest bearing loans 4698 0 4698 Trade and Other payables 2062 0 2062 Employee Benefits 6 0 33 33 Restructuring provision 7 125 (125) - Current Tax Liability 21 0 21

- 2. Deferred tax liability 8 290 230 520 Total Liabilities 7196 138 7334 Total Assets less total liabilities 3280 538 3818 Issued Capital 750 0 750 Revaluation Surplus 3 0 147 147 Hedging Reserve 5 0 151 151 Retained Earnings 9 2530 240 2770 Total Equity 3280 538 3818 Notes: 1. Depreciation was influenced by tax requiremens under the previous accounting standards but under IFRS represents the useful life of assets. The cumulative adjustment increasing the carrying amount of plant, property and equipment by 50. 2.Intangible assets under previous accounting standards included 75 for items that are transferred to goodwill because they do not qualify under the IFRS to be recognised as Intangibles. 3.Financial assets are all classified as available - for - sale under IFRS and are carried at their fair value of 1945. The resulting gains 147(210, less deferred tax of 63) are included in the revaluation surplus. 4.Inventories include fixed and variable production overhead of 200 under IFRS which was excluded under the previous accounting standards. 5.Unrealised gains of 216 on un - matured forward foreign exchange contracts are recognised under IFRS. The resulting gain of 151(216 less related deferred tax of 65) are included in hedging reserve. 6. A pension liability of 33 is recognised under IFRS which was not recognised under the previous accounting standards where it was recognised on cash basis. 7.A restructuring provision of 125 relating to head office activities was recognised under previous accounting standards but does not qualify for recognition under the IFRS. 8. The above changes increased the deferred tax liability as follows: Gross Tax Net a. Revaluation reserve 210 63 147 b. Hedging reserve 216 65 151 c. Retained Earnings 342 103 239 Increase in deferred tax liability : 230 9. Adjustments to retained earnings are as follows: a. Depreciation (note 1) : 50 b. Produciton overhead (note 4) : 200 c. Pension liability (note 6): (33) d. Restructuring provision (note 7) : 125 342

- 3. e. Tax effect of the above 103 Total Adjustment to retained earnings 239 Reconciliation of Total Comprehensive Income of XYZ Ltd. for year ended 31st March, 2011 Effect of Previous Transition IFRS GAAP Particulars Note to IFRS Revenue 10455 - 10455 Cost of Sales 1,2,3 (7,642) (48) (7,690) Gross Profit 2,813 (48) 2,765 Distribution Costs 1 (953) (15) (968) Administrative expenses 1,4 (1,421) (150) (1,571) Finance Income 723 - 723 Finance Costs (951) - (951) Profit before tax 211 (213) (2) Tax expense 5 (79) 64 (15) Profit(Loss) for the year 132 (149) (17) Available for sale financial assets 6 - 75 75 Cash flow hedges 7 - (20) (20) Tax relating to other comprehensive income 8 - (17) (17) Other Comprehensive Income - 38.5 38.5 Total Comprehensive Income 132 (111) 22

- 4. Note to reconciliation of total comprehensive income 1. A pension liability is recognised under IFRS, but was not recognised under accounting standards. The pension liability increased by 65 during the year which caused increases in the cost of sales(25), distribution costs(15), and administrative expenses(25). 2.Cost of Sales is higher by 23 under IFRSs because inventories include fixed and variable production overhead under IFRSs but not under earlier accounting standards. 3.Depreciation was influenced by tax requirements under previous accounting standards, but reflects the useful life of the assets under IFRS. The effect on profit for the year is not material. 4. A restructuring provision of 125 was recognised in the previous accounting standard on 1st April 2010 but did not qualify for recognition under IFRS until the year ended 31st March 2011. The increases administrative expenses for the year 2010-11 under IFRS. 5. Adjustments 1-4 result in a reduction of 64 in deferred tax expense. 6. Available for sale financial assets carried at fair value under IFRS increased in value by 90 in the year 2010-11. The entity sold these assets during the year realising a gain of 20 in the profit and loss. On the realised gain 15 had been included in the revaluation reserve as at 1st April,2010 and is reclassified from revaluation reserve to profit and loss. 7. The fair value of forward foreign exchange contracts that are effective hedges of forecast transactions decreases by 20 in the year 2010-11. 8. Adjustment 6-7 lead fo an increase in 17in deferred tax expenses. ADJUSTMENT NO 5 Increase in Deductible Expenses 1 Pension Liability 65 2 Cost of Sales 23 3 Restructuring Provision 125 213 Applying a tax rate of 30% on above 64 ADJUSTMENT NO 8 Available for Sale Financial Assets 75 Cash flow hedges -20 55 Applying a tax rate of 30% on above 16.5