1. F l o r i d a S t a t e U n i v e r s i t y P a g e | 1

Bloomin’

Brands

NYSE: BLMN,

BLMN US

Sector: Service

Industry: Restaurant (Casual)

Decision: Buy

Current Price: 25.09

Price Target: 27.88 (11.12% increase)

Bloomin’ Inc. is an attractive stock due to an improving domestic business, strong international strategic

direction and recent divestitures promising solid 2015 operating margins amid changing commodity

costs.

Business description:

Bloomin’ Brands Inc. is one of the largest casual

dining restaurant companies in the world and is

comprised of four primary business segments –

Outback Steakhouse, Carrabba’s Italian Grill,

Bonefish Grill and Fleming’s Prime Steakhouse

and Wine Bar – for a total of 1349 owned and

operated restaurants and another 162 franchises

(as of end 3Q14). The business resides in 48 states,

21 countries and several territories (Puerto Rico

and Quam).

Bloomin’ Brands tries to appeal to different

consumer with their different concepts of

restaurants (see Appendix: Figure-1). In this

industry to create a successful competitive position

and advantage over competition a company needs

to create a comprehensive campaign. Their

campaign consists in a menu & price campaign

with an improvement in the customer experience.

Bloomin’ Brands changed their menu while

adding different priced dishes to create a “barbell

menu” in which the customer will not be limited.

Bloomin’ Brands have also implemented

campaigns to improve customer service such as

scorecard rating while remodeling the restaurants

to create more pleasant and unique experience

while dining in (see Appendix: Figure-2).

Brief History & Management:

Predecessor OSI Restaurant Partners Inc. opened

the first Outback Streakhouse in 1988. By 1996,

the successful Outback brand was expanding

internationally. Bloomin’ Brands Inc. was

incorporated by Bain Capital Partners LLC and

Catterton Management Company LLC in 2006

and soon acquired OSI Restaurants through a

merger. In 2012, Bloomin’ Inc. participated in an

IPO and is now controlled by one founder and a

handful of sponsoring investor groups.

$0

$5

$10

$15

$20

$25

$30

Aug-12

Oct-12

Dec-12

Feb-13

Apr-13

Jun-13

Aug-13

Oct-13

Dec-13

Feb-14

Apr-14

Jun-14

Aug-14

Oct-14

Dec-14

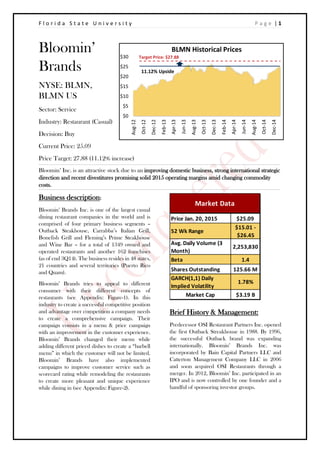

BLMN Historical Prices

Target Price: $27.88

11.12% Upside

Price Jan. 20, 2015 $25.09

52 Wk Range

$15.01 -

$26.45

Avg. Daily Volume (3

Month)

2,253,830

Beta 1.4

Shares Outstanding 125.66 M

GARCH(1,1) Daily

Implied Volatility

1.78%

Market Cap $3.19 B

Market Data

2. F l o r i d a S t a t e U n i v e r s i t y P a g e | 2

The decision by BLMN to host their first analyst day since their IPO may be prudent in the long run as

Chairman and CEO of the Board, Elizabeth Smith, revisited their Revitalization Plan (introduced Q4 2009)

offering specific guidance and focus on targeted international growth, operational productivity, and overall

organizational effectiveness. Elizabeth Smith has been at BLMN since November 2009, and leads the Brand

Presidents who together combine extensive food & beverage operational experience with proven industry

leadership ability. Strategic changes in hiring a new Outback International President, Pat Murtha, as well as

Digital and Chief Information Officer, Donagh Herilhy, Chief Development Officer Suk Singh, and Chief

Global Supply Chain Officer, Juan Guerro, to target international expansion and margin protection through

stronger supply chain management, could aid in meeting 2015 guidelines and estimates. Recognized as only

one of two Casual Dinning Restaurant’s on Fortune 500’s Most Admired Companies, BLMN will look to

leverage its experienced field team and entrepreneurial regional management culture in order to grow comp

profitability and scale.

Industry Overview & Competitive Positioning

Competing in an industry with $683.4 billion

dollar in sales Bloomin’ Brands has approximately

.64% of the market share. The restaurant industry

relies heavily on location and the ability to have

presence in every geographical market without

cannibalizing sales. The industry is fragmented and

mature which affects the margins of the firms

competing. There are 990,000 restaurant locations in

the United States. Customer loyalty is very hard to

acquire and creating brand image and differentiation is

difficult in an industry primarily driven by prices. For

2014, sales of the casual dining segment grew .8% in

comparison to a negative growth of .1% in 2013. 2014

was a successful year for the industry.

Main competitors similar to Bloomin’ Brands

in size are Darden Restaurants with sales of 6.4B,

Brinker International with sales of 2.9B, The

cheesecake Factory with sales of 1.95B and Buffalo

Wild Wings with sales of 1.45B. Besides these big

competitors there are smaller cap firms and locally

owned restaurants that compete for the local markets.

Larger firms take advantage of economies of scale for

cheaper products, centralized supply chains and also

centralized oversight and management. Locally owned

restaurants offer more specialized menus. Due to

changing consumer patterns, consumers are looking

for locally sourced meats and seafood and locally

grown produce. Small owner restaurants can satisfy

these trends better.

Sales are dependent on the state of the

economy and consumer trends. The state of the

economy is very important for the restaurant industry

since the demand for the services is highly elastic. On

average a household spends $2,678 per year at

restaurants. Income is the No.1 driver of household

spending since households that earn $70,000+ account

for 1/3rd

of all U.S households, but more than ½ of total

restaurant spending. According to the Restaurant Performance Index, which tracks the health of the restaurant

Quick

Service

27%

Casual

Dining

32%

Other

41%

Food-Service Market

Breakdown

$43 $120 $239 $397

$587 $683

1

Restaurant Industry Sales

In billions of current

dollars

1970 1980 1990 2000 2010 2014

3. F l o r i d a S t a t e U n i v e r s i t y P a g e | 3

industry, the industry is healthy and future outlooks are positive. In December 2014 the index was in 103.

Regarding this index, anything above 100 shows industry expansion.

Investment Summary

Signs of strength

We issue a BUY recommendation on Bloomin’ Brands, Inc. with a year-end 2015 target price of $27.88, with

upside potential towards our bull case price of $37.08, giving investors potential upside return of 11.12% and 47.79%,

respectively.

Reasons for Upside Potential:

Significant margin improvement opportunities. A 100 basis point improvement from productivity and

efficiency gains in COGS throughout the projection period increases the stock price in our base case model

to $32.51, a 16.6% increase.

Potential for high same-store sales in Brazil to capture a larger percentage of the total revenues, which

currently are 86% domestically driven.

Geographically diversified source of cash flows, potentially decreasing the risk profile of BLMN.

BLMN is concentrated in strong hands with 98% of shares held by institutions, of which Bain Capital is

the largest shareholder at 30% of float held.

Improving capital structure allowing fiscal flexibility, and improvements in risk management.

BLMN Improving Domestically

After poor 2Q14 growth, management’s focus on their core competencies resulted in 3Q14 comps of 4.8%, 4.8%

and 2.6% at Outback, Flemings, and Bonefish, respectively. Increasing levels of domestic discretionary income

(fueled in part by reduced gas prices) promise to further boost customer traffic and industry-wide sales. Many

economists believe that even though during the 2014 holiday season a reduction in oil prices did not evolve into

more spending, it is a matter of time until consumer start spending their oil savings in other services.

BLMN Displaying Technology & Innovation

According to the National Restaurant Association, most restaurants will begin using technology to reach out to

clients. The use of social media will be beneficial for companies. Many brands have been trying to implement the

use of technology to enhance the consumer experience. A successful application of technology is expected to

improve consumer satisfaction and sales.

Bloomin’ Brands through their R&D division have established a 12 month pipeline of new menus. Bloomin’ Brands

can successfully and quickly introduce new items and menus to satisfy consumer trends. For example Bloomin’

Brands have introduced under 600 calories items which respond to the trend of healthier eating and lifestyles.

BLMN Rolling Out the Lunch Menu

Outback and Carrabba’s now offer weekday lunches, a growing revenue stream, in 59% and 54% of their domestic

locations, respectively. These figures are up from 56% and 51% (2Q14) and 26% and 28% (3Q13). In 2Q2015

Outback Steakhouse is expected to roll out their brand new lunch menu. Bloomin’ Brands tested the new menu by

offering the options only on weekends. The menu options were directed at minimizing the impact of sale

cannibalization. The upcoming launch is expected to increase sales and improve restaurant comps. Bloomin’ Brands

plans to launch a media campaign and service model along with the new menu.

BLMN Relocating and Remodeling

One of the keys for customer loyalty is geographic location. With the new relocation programs through the software

Bloomin’ Brands acquired, the company expects to lift sales of the dinner menu and introduce at the same time the

lunch menu. Around 100 restaurants will be relocated in the upcoming year to reduce cannibalization and increase

sales/geographic reach. All brands will also undergo remodeling phases - Bloomin’ Brands has pledged to renovate

10% of locations annually. Outback already internally remodeled all locations and is now working to remodel the

exteriors. We feel that the reinvestment of capital into existing stores while maintaining strategic expansion plans is

a sign of healthy business operations.

4. F l o r i d a S t a t e U n i v e r s i t y P a g e | 4

BLMN Expanding Bonefish

The main way for food service brands to increase growth is by opening new locations. Bloomin’ Brands new

expansion campaign will have Bonefish Grill as their flagship Brands. Currently there are 201 locations of Bonefish

and Bloomin’ Brands goal is 300 nationally. This will be a key growth opportunity for Bloomin’ Brands since the

company will be able to reach out to many different markets.

BLMN Moving Globally with a Strong Strategic Direction

A highly competitive U.S. market has driven the attention of the big firms internationally. Bloomin’ Brands has

Outback Steakhouse locations in China, South Kore, Brazil and Mexico.

CEO Elizabeth Smith stated that Korean restaurants are in an “aggressive battle for market share with an increased

reliance on discounting”. Accordingly, out of the 36 locations that Bloomin’ Inc. closed/are closing in 4Q14/1Q15,

34 are in South Korea. We applaud this decision, as many of the restaurants selected to close have continued to

provide negative or limited cash flows. This divestment will free management’s time and capital to pursue expansion

in more attractive economies.

Bloomin’ Brand also has a position in Brazil and is one of the pioneers in entering the Brazilian market. Sixteen

locations are planned to open in Brazil in early 2015 (adding to a base of 48). Sao Paulo is the second largest pizza

consumer in the world after New York. Pizza, pasta and steak/seafood are 3 of the top 5 most popular menu items

for this city.

.

BLMN Divesting/Portfolio Optimization

As an additional precaution, Bloomin’ Inc. has recently sold both corporate jets and has divested itself of the Roy’s

brands. We see these actions as indicative of a healthy management desire to cut unnecessary operating costs. We

also foresee an additional possible upside in out years as a result of real estate monetization (Bloomin’ Inc. plans on

leasing all property going forward). Leasing stores will weigh on store level margins, but if management can sell its

real estate and either pay down debt or buyback stock, they may boost shareholder value.

Valuation Summary

In order to arrive at our base case target price of $27.88,

we used a Discounted Cash Flow model utilizing a Free

Cash Flow to the Firm approach.

Unlevered FCFF DCF with Bear, Base, and Bull

Case.

Dynamic WACC using a bottom up CAPM and

bottom up Beta approach.

Terminal Value Calculated using Exit Multiple

Method and Perpetuity Growth Method.

Our bull case target price of $37.08 is based on higher

than expected sales from BLMN’s international capital

investment in Brazil and China as well as relocations of

many domestic stores for optimization of sales. Sales grow

at almost double the rate of the base case for each of the

forecast years, except for the terminal year in which sales

grow at 3%, the same as in the base case.

Recommendation Criteria Price Range

Jan. 20, 2015 Price $25.09

10%+ Upside Price

Above

$27.60

BUY

10% Downside to 10%

Upside Price

$22.58-

$27.60

HOLD

10%+ Downside Price

Below

$22.58

SELL

Base Case $27.88 $5,105.80

Bear Case $16.79 $3,960.50

Valuation DCF

Bull Case $37.08

EV

$6,295.70

5. F l o r i d a S t a t e U n i v e r s i t y P a g e | 5

Our bear case target price of $16.79 assumes the

downside of 0% sales growth in every year of the

projection period. This is based on the potential for

emerging market recessions in China and inflationary

pressures in Brazil that could cause a systemic market

crisis in both of BLMN’s main expansionary target

markets. We assume that the negative growth in these

countries will be offset by growth domestically, thereby

arriving at 0% sales growth.

Taxes in all three models are set to the marginal US

corporate tax rate of 39.1%, assuming all firms will

eventually have to remit earnings to their home country.

Free Cash Flow to Firm Model

We evaluated BLMN using a 3-Stage Discounted Cash

Flow Analysis. A Free Cash Flow to the Firm (FCFF)

model was chosen for a few reasons. First the firm is

highly levered with market value of debt totaling more

than $2.5 Billion (including PV of Capital Leases and

Purchase Obligations). This high leverage is not

expected to continue ad infinitum and thus we chose

the target Market Value of Debt-to-Equity for the

industry of 28% as a guiding point as to what the firm’s

capital structure will look like in the future. Currently

BLMN has a Market Value of Debt to Market Value of

Equity of 82.1%. Management has made it clear in the

most recent 10-Q and First Analyst Investor Day that

they plan to reduce their debt structure going forward

and to fund expansion CapEx through FFO. The main

drivers of this model are EBITDA Margin, growth in

sales, reduction in COGS margin, and the dynamic

WACC structure, driven by decreasing future leverage,

which decreases the levered beta and the CAPM

portion in calculating the Cost of Capital.

Revenue

Revenues were forecasted using a 3-Stage model. In the

first stage sales growth was estimated at 7% for the next

2 years.

7% growth was derived from a combination of analyst

expectations, management expectations, and the strong

adherence towards international expansion. Growth

from 2011 to 2013 was in the 3%-4% range. 2014 was a

year of exceptional historical growth relatively speaking,

due mostly to the new units opened in Brazil, and a

revitalization of domestic units through relocations,

menu revamps, and the introduction of lunch menus at

some locations. The initial high growth period is

supported by our expected growth for Outback in Brazil and the introduction of a second concept (Carrabbas)

in Sorocaba, Brazil during 1H 2015. Sales from 2017-2019 will decrease on average by approximately 125

0%

2%

4%

6%

8%

2012 2013 2014 2015 2016 2017 2018 2019

Sales Growth Forecast

7.10%

7.20%

7.30%

7.40%

7.50%

7.60%

7.70%

2014 2015 2016 2017 2018 2019

WACC

7.50%

8.00%

8.50%

9.00%

9.50%

10.00%

10.50%

2014 2015 2016 2017 2018 2019

CAPM

$0.00

$10.00

$20.00

$30.00

$40.00

BLMN Potential Price

Range

$37.08

(+48%)

$27.88

(+11%)

$16.79

(-33%)

6. F l o r i d a S t a t e U n i v e r s i t y P a g e | 6

basis points a year to end at 3% growth in 2019. Growth

will decrease to this level by 2019 due to loss of market

share and competition.

Depreciation

We assume that BLMN will continue to depreciate its

assets similar to rates in the historical estimation period

from 2011 to 2013. Depreciation in these years was 4%,

3.89%, and 3.97% of sales, respectively. In the

forecasted period deprecation remains an average of the

historical estimation period of 4%.

Margins

Historical Gross Profit margins hover in the 39-40%

range. Gross profit will continue to be driven by

productivity increases, subdued commodity inflation,

and lower labor expenses in foreign countries such as

Brazil and China. BLMN’s Management forecast

commodity inflation to be in the 4-6% range for 2015,

which will be slightly offset by increased sales growth.

Therefore, we have kept Gross Profit margin in the

forecast period at 40%, a slight increase over the average

historical due to decreasing labor costs and productivity

gains outweighing commodity price inflation. Our

metric for Gross Profit differs from what is reported in

the 10K because we include Labor expenses as part of

Cost of Sales, whereas BLMN does not include Labor

expenses as part of cost of sales to calculate gross profit.

EBITDA margins are one of the more important

drivers for the firm as a whole, due to the fact this metric

really shows the value employees add to the operation,

as it is free of debt and before interest, taxes,

depreciation, and amortization. EBITDA margin in the

historical period of 2011-2013 grew at a CAGR of 6.2%.

We expect EBITDA to grow at a CAGR of 3.5% in the

forecast period; 2015-2019 and EBITDA margins to

stay relatively flat at 9.2% of sales.

Selling, General & Administrative (SG&A) Expense Growth

Currently, SG&A is held constant at 30.8% of sales, slightly higher than 2013 due to increased advertising

expenses from a new rollout of a lunch menu as well as new product rollouts.

Interest Expenses

As per the amended credit agreement in the most recent 10Q, OSI has two securitized loans with a revolving

credit facility on Term loan A. The total amount authorized is $1.125 billion, of which $940 million has been

used. Interest for Term Loan A is set at 75 to 125 basis points over base rate which is the highest of 3 separate

proxy rates. Currently, this rate is at 2.16%. Term Loan B is set at 3.50%. Other related interest from CMBS

loans totaling $473.5 million have varying rates. The first mortgage loan has five fixed-rate components and a

floating rate component. The fixed rate component bears interest from 2.37% to 6.81% annually. The floating

rate component is equal to the 30-day LIBOR plus 2.37%. The First Mezzanine Loan totaling $85.4 million

bears interest at 9.00% per annum, and the Second Mezzanine Loan totaling $86.2 million bears interest at

11.25% per annum.

9.00%

11.25%

Collaterlized Term Loan B

First Mortgage Loan

Floating Rate Component

of CMBS

3.50%

4.07%

30-Day LIBOR

+ 2.37%

Fixed Rate Component of

CMBS

2.37% - 6.81%

First Mezzanine Loan

Second Mezzanine Loan

BLMN Debt Financing

Loan Type

Synthetic Cost of Debt

Collateralized Term Loan A

6.22%

Rate

2.16%

0%

2%

4%

6%

8%

10%

12% 2011

2012

2013

2014E

2015E

2016E

2017E

2018E

2019E

EBITDA MARGIN

7. F l o r i d a S t a t e U n i v e r s i t y P a g e | 7

Cost of Capital

Cost of Capital was estimated at a target rate of 7.57% by 2019. We used a dynamic WACC in estimating the

hurdle rate due to the fact that the capital structure should change significantly towards the industry average

during the forecasting period. WACC was 7.43%, 7.51%, 7.56%, 7.58%, and 7.57%, during 2015-2019,

respectively. Cost of debt was estimated synthetically through a country and company default premium. To

estimate country default risk, we calculated the proportion sales in respective foreign countries, then multiplied

that by the default premium in excess of the mature market Equity Risk Premium of 5% (United States). This

ended up adding 22 basis points to the total cost of debt of 6.22%. We then added company default spread of

1.30% which was found through the interest coverage ratio of 3.04. Another approach is to just use the interest

coverage ratio, which hovers between 2 and 3. We then compare that to its respective credit rating level, which

tends to be in the BB range, which has a spread of 4% in excess of the risk free rate. The average unlevered

Beta for the 67 firms in the Restaurant sample space was 0.94.

We calculated the Equity Beta for 2015 to be 1.41. Interestingly, if we run a regression on BLMN using

4,000+ firms in the CRSP index, the stock trades closer to its unlevered Beta at 1.01. This means the market

is not as concerned with the debt and is likely supported by investor expectations of stability in future Operating

Income and free cash flow to service debt and other expenses.

Dividend Policy

BLMN announced on December 16, 2014 that they would implement a 24-cent per share dividend in 2015.

This would yield about 1% per annum at current share prices and cost the company $30 million. We do not

include dividends in the calculation of share price in our DCF as management can reinvest the announced

dividends if it decides to do so.

Capital Expenditures (CAPEX)

Capital Expenditures will mainly be driven by unit store

growth both domestically and internationally.

Financial Analysis

Future Earnings and Volatility

While BLMN just posted negative quarterly net

income of $11.44 million, it should stabilize in the

coming year. BLMN has grown net income in 2010

from $52.97 million to $208 million in 2013. We

expect earnings to increase as revenues rise as BLMN

is in the middle of expanding into higher growth

emerging markets and committed to a domestic

revitalization campaign. Due to a strong historical

presence in Brazil and the entrance of another concept,

we expect to see net income stabilize in the coming

year. We expect earnings margin to average 3.06% in

the 2015-2019 forecast period. We’ve therefore

estimated an EPS of $1.25 for 2015, which slowly rises

to $1.91 by 2019; an 11.11% CAGR.

Furthermore, as can be witnessed in the above daily

Exponentially Weighted Moving Average (EWMA),

using a lambda (JPMorgan RiskMetrics decay factor of

.94), we find that the price history is quite sensitive to

6.59%

0%

2%

4%

6%

8%

1

37

73

109

145

181

217

253

289

325

361

397

433

469

Constant vs EWMA

Volatility

Constant Volatility

EWMA-Volatility

53%

25%

9%

13%

2014 Estimate Capital

Expenditure Breakdown

Development/

relocations

Remodels

IT

Maintenance/

Other

8. F l o r i d a S t a t e U n i v e r s i t y P a g e | 8

earnings announcements. The EWMA chart above on

page 7 displays the most recent 504 trading days as of

Jan 16, 2015. The 6.85% spike on August 5, 2015 was

an earnings report that came in 2 cents below

expectations of 29 cents. A 3.2% CAGR expected

continual growth rate across core domestic AUVs,

continued out-performance of over 2% comp sales

over the Knapp index, and a targeted +10% increase

in their respective lunch platforms were drivers stated

at Q3 2014 Investor Conference that will lead to long-

term sustainable growth. We believe these core areas

will provide our basis for long term unit growth and

same store sales expectations.

Margin Improvement is Fundamental

COGS Margin and which drives Gross Profit margin is

what will make or break this stock. A 100 basis point

improvement in COGS (including labor cost from the

balance sheet) during the projection period from 60%

to 59% will cause our base case price to rise from $27.88

to $32.51, a 16.6% increase in share price. However,

with that said the historical period averages between 15

and 40 basis points above 60%. We assume that

efficiencies will decrease COGS to a flat rate of 60% for

the projection period.

Profitability and Value Metrics

We estimate the return on invested capital to average

7.84%. Furthermore, we estimate the Cost of Capital to

average 7.53% over the projection period. This is a key

signal that BLMN will need to invest wisely in its expansionary capital investment. So far, BLMN is downsizing

in one foreign country, South Korea. This is not a good signal, but with BLMN’s management engaged and

highly experienced in the market it plans to expand the most in (Brazil) in addition to introducing a second

concept internationally for the first time, we expect sales growth to remain as strong as 2014.

On an EV to EBITDA basis, BLMN trades at a multiple of 12x, which trades slightly below the 67 restaurants

in the industry of 12.96; therefore suggesting BLMN could be slightly undervalued.

7.0%

7.5%

8.0%

8.5%

2014 2015 2016 2017 2018 2019 2020

Profitability

Return on Capital Cost of Capital

0%

1%

2%

3%

4%

5%

6%

7%

2013 2012 2011

Capex as % Rev

Annual

Historical Period CAGR Projection Period

2011 2012 2013 ('11 - '13) 2014 2015 2016 2017 2018 2019

EBIT 213.456 181.137 225.357 6.25% 259 246.6562 261.4555 275.8356 286.869 295.4751

(Implied Interest) -83.38 -86.64 -74.77 -83.49 -70.78 -58.07 -45.37 -32.66 -19.95

130.076 94.495 150.584 175.5099 175.874 203.3813 230.4693 254.2107 275.5247

1- Effective Tax Rate 83% 83% 83% 83% 83% 83% 83% 83% 83%

Net Income 107.96 78.43 124.98 145.67 145.98 168.81 191.29 210.99 228.69

% margin 2.81% 1.97% 3.03% 3.30% 3.12% 3.40% 3.65% 3.87% 4.07%

Shares Outstanding 106 114 125.66 126 124 124 124 124 124

CAGR

EPS $1.02 $0.69 $0.99 $1.10 $1.18 $1.36 $1.54 $1.70 $1.84 11.88%

Price $25.32 $25.32 $25.32 $25.32 $25.32 $25.32 $25.32 $25.32 $25.32

Earnings Yield 4.02% 2.72% 3.93% 4.34% 4.65% 5.38% 6.09% 6.72% 7.28%

BLMN EPS

is expected

to increase.

9. F l o r i d a S t a t e U n i v e r s i t y P a g e | 9

BLMN margins are below the Industry Average

Understanding BLMN’s Primary Cost Drivers

Investment Risks

However, the following risks remain present when considering the company:

Carrabba’s may continue to lose money.

The only underperforming segment (again), with 3Q14 comps of -1.2%, was Carrabba’s. Management admits

that their 2014 menu revamp fell short and tells us to expect limited-time-offers until a new 2H15 menu.

However, there is a strong possibility that until a major segment re-haul, Carrabba’s will continue to offsetting

the positive cash flows from other business segments. Due to the continuing underperformance, we suggest

minimizing Carrabba’s’ domestic capital investments without changing the current international expansion

plans.

Lunch offerings may cannibalize dinner traffic.

Despite year-over-year increases in lunch traffic and management’s acknowledgment that some degree of

dinner traffic “cannibalization” is inevitable, they insist that it is not a major issue. We mostly agree, especially

since Carrabba’s needs as much foot traffic as possible.

Rising competition from other industries, such as grocery markets.

Carrabba’s management admits that major potential competition to the entire restaurant industry are grocery-

stores. The rising popularity of prepared grocery-store meals will likely continue to take business away from

Misc

Food

24%

Produce

12%

Breads &

Oils

7%

Dairy &

Cheese

8%

Shell &

Seafood

11%

Other

Meats

5%

Chicken

5%

Beef

28%

Food and Beverage Break-

down

Marketing

4%

G&A/Other

10%

Occupancy

13%

Utilities

3%

Fixed

Labor

18%

Restaurant,

Operating

Costs

7%

Restaurant,

Labor

12%

Food and

Beverage

33%

Cost Structure Break-down

Company Ticker Market Cap LTM EBITDA EV LTM EV/EBITDA LTM EBITDA/Sales

Bloomin' Brands BLMN 3.14B 425,870.00$ 4.41B 10.4 9.72%

Texas Roadhouse, Inc TXRH 2.42B 186,250.00$ 2.41B 12.9 12.02%

Darden Restaurants, Inc DRI 7.94B 642,600.00$ 8.83B 13.7 10.01%

Brinker International, Inc EAT 3.86B 431,460.00$ 4.69B 10.9 14.73%

Ruth's Hospitality Group RUTH 498.83M 49,470.00$ 525.35M 10.6 11.84%

Buffalo Wild Wings Inc BWLD 3.52B 235,770.00$ 3.42B 14.5 16.26%

The Cheesecake Factory Incorporated CAKE 2.49B 233,360.00$ 2.57B 11.0 11.97%

Famous Dave's of Ameirca DAVE 192.43M 19,140.00$ 203.66M 10.6 12.68%

Bravo Brio Restaurant Group, Inc BBRG 238.24M 39,120.00$ 252.31M 6.4 9.59%

Del Frisco's Restaurant Group, Inc DFRG 541.87M 41,090.00$ 546.77M 13.3 14.00%

BJ's Restaurant, Inc BJRI 1.27B 84,260.00$ 1.28B 15.2 10.13%

Mean 2.373 217,126.36$ 11.8 12.09%

Median 2.42 186,250.00$ 11.0 11.97%

10. F l o r i d a S t a t e U n i v e r s i t y P a g e | 10

casual restaurants (an estimated 7 million visits since 2009, or about 2% per year). Due to modern consumer

convenience preferences, this rate is expected to continue to rise.

Rising labor costs as a result of domestic minimum wage hikes.

This New Year saw more minimum wage hikes than ever before, with 20 states increasing their tipped-wage

rate on New Year’s Day, including Florida and California (Bloomin’ Brands’ biggest locations). Several major

west-coast cities such as Seattle and San Francisco have proposed legislation approaching $15/hr. Whether

these increases will materially affect long-term operating margins remains to be seen.

Risks associated with the South Korean economy.

The number of casual dining restaurants built in Korea has shot up by 88% over the last six years, and sales in

Korea’s over-saturated casual dining market dropped by more than 20% in 2Q14 alone.

Risks associated with the Brazilian economy.

Many analysts do not think Brazil’s short-term prospects are favorable. GDP grew a measly .1% in 3Q14,

following the 2Q14 contraction of .6% and 1Q14 contraction of .2% as a result of structural weaknesses,

ineffective expansionary policies and a new political cycle. Temporary jobs will continue being cancelled as the

re-elected government begins to implement fiscal adjustments, imposing additional pressures on the labor

market. However, Bloomin’ Inc. management remains confident amid these statistics due to low

unemployment and a culture which is focused on regularly eating at restaurants.

Beef prices, along with other commodity prices, may rise and squeeze operating margins.

Due to a severe drought three years ago, U.S beef prices have increased significantly over the past several years.

However, beef prices have started (and we predict will continue) to fall as the result of increasing wheat prices.

We calculate 1-year and 2-year correlations of -.82 and -.79, respectively, between beef and wheat prices and

argue that farmers slaughter more cattle during times of rising cattle food prices, causing beef prices to fall (see

Appendix: Figure-5).

Uncertainty Regarding Legal Disputes

Near end 4Q14, a federal court certified a nation-wide class action lawsuit affecting over 100K employees. The

suit addresses potential minimum wage and overtime payment violations. Proceedings such as class action

lawsuits are costly, consume management’s attention, and carry the possibility of large settlement costs.

Risks associated with a high debt capital structure.

BLMN has had a historically high debt capital structure which is more than double the debt capital structure

relative to industry peers (45.1% Market Value of Debt to MV of Capital versus the industry average of

21.7%) . This is often a cause for concern to investors and the firm. However, investors are not as concerned

as can be witnessed by the regression equity beta of 1.01 (highly significant at the 1% level) versus the current

bottom-up equity beta in our DCF of 1.41. The highly levered nature of Bloomin’ has increased debt

servicing and somewhat hindered their profitability in the past. In addition, the high leverage increases the

cost of equity, thereby making the hurdle rate for equity investors higher and less attainable. Despite the high

debt servicing relative to industry peers, S&P has rated Bloomin’ at a BB rating, implying a default spread of

4% in excess of the Risk Free 10-year treasury. Furthermore, management has consistently downsized its long

term debt in the last 4 years, showing their commitment towards the eventual industry average capital

structure, which will not only decrease earnings volatility and unpredictability, but give investors confidence

that management is behaving rationally.

11. F l o r i d a S t a t e U n i v e r s i t y P a g e | 11

Appendix

Figure-1: Diversified Brand Portfolio & Company Timeline

(International

locations)

Source: BLMN Investor Reports

Figure-2: LTM Sales by Concept

Source: BLMN Investor Reports

Figure-3: Customer Value Cycle

Source: BLMN Investor Reports

Brand Locations Position in Market

66 #4

227 #1/#2

753 #1

244 #2

201 #2

August

1987:

Outback

Steakhou

se Inc.

founded

and

incorpor

ated

June

1988:

First

Outback

retail

location

opens in

Florida

October

2006:

Bloomin'

Brands

founded

by Bain

Capital

and

others

June

2007:

Bloomin'

Brands

buys OSI

through

a

leverage

d buy

out

August

2012:

Bloomin'

Brands

goes

public

through

an Initial

Public

Offering

12. F l o r i d a S t a t e U n i v e r s i t y P a g e | 12

Figure-4: Porter Analysis

Threats of New Entrants (medium)

- Considerable initial investment for new market participants. Not only the

location will need a considerable amount of capital but also the marketing

strategy needs it.

- Brand recognition is an important liability for new participants

- Very easy access to distribution channels

- Government health regulations have to be met

- No legal barriers

- New firms will face economies of scale from big participants

Threat of Substitutes (high)

- Studies have shown that consumer decisions are based partly on

the location of the restaurant

- Many competitors with similar products and menus

- Brand differentiation is hard to accomplish

- Low Customer loyalty

- Consumer trends change extremely fast

- Home cooked meals and grocery store ready to eat menus

Competitive Rivalry (high)

- No dominant firm

- Many big size firms

- Hard to create

differentiation

- Profitability margins vary

due to heavy competition

Buyer Power

(medium)

- Switching to

other products

is simple

- Industry with

very elastic

demand

- Many small

buyers since

every household

close to a

location may be

considered a

potential client

- Low importance

and necessity as

a product for

buyers

Supplier Power (low)

- Supplier power

will depend

entirely on the

size of the

business they

work with

- Bigger firms will

be able to enact

economies of

scale and

centralized

supply chains

which greatly

reduce supplier

influence

13. F l o r i d a S t a t e U n i v e r s i t y P a g e | 13

Figure-5: Relationship Between Beef and Wheat Prices

Source: Indexmundi.com

Figure-6: Changing Costs, Expenses and Income

Source: BLMN 10-K

-10.00%

-5.00%

0.00%

5.00%

10.00%

15.00%

20.00%

Dec-12

Feb-13

Apr-13

Jun-13

Aug-13

Oct-13

Dec-13

Feb-14

Apr-14

Jun-14

Aug-14

Oct-14

Dec-14

Changes in Beef and

Wheat Price Over Time

Change in Wheat Change in Beef

150

200

250

300

350

Dec-12

Feb-13

Apr-13

Jun-13

Aug-13

Oct-13

Dec-13

Feb-14

Apr-14

Jun-14

Aug-14

Oct-14

Dec-14

Beef and Wheat Price Over

Time

Wheat Price

Beef Price

2 per. Mov. Avg. (Wheat Price)

2 per. Mov. Avg. (Beef Price)

(dollars in millions):

% of Restaurant sales % % 0.1 % % % 0.3 % % % 0.2 %

(dollars in millions):

% of Restaurant sales % % 0.0 % % % -0.5 % % % 0.0 %

(in millions):

General and administrative $ 268.9 $ 326.5 $ 326.5 $ 291.1 $ 291 $ 253

(dollars in millions):

Income from operations $ 225.4 $ 181.1 $ 181.1 $ 213.5 $ 213.5 $ 168.9

% of Total revenues % % 1 % % % -1 % % % 1 %

Cost of sales

2012 2011 Change 2011 2010 Change

YEARS ENDED YEARS ENDED

DECEMBER 31, DECEMBER 31,

Cost of sales $ 1,281.00$ 1,281.00

YEARS ENDED

32.5 32.2 32.2 32

$ 1,226.10 $ 1,152.00$ 1,226.10

2012 2011 Change 2011 2010 Change

YEARS ENDED YEARS ENDED

DECEMBER 31, DECEMBER 31,

Labor and other related $ 1,117.60$ 1,157.60

YEARS ENDED

12% 15%

DECEMBER 31,

2013 2012

28.3 28.8 28.8 28.8

$ 1,094.10 $ 1,034.40$ 1,094.10

4.5 5.6 5.6 4.7

-15%

DECEMBER 31, DECEMBER 31,

2012 2011 Change 2011 2010 Change

DECEMBER 31,

2013 2012

$ 1,333.80

26%

Labor and other related expenses

General and administrative expenses

Income from operations

2012 2011 Change 2011 2010 Change

YEARS ENDED

DECEMBER 31, DECEMBER 31,

YEARS ENDED

YEARS ENDED

DECEMBER 31,

2013 2012 Change

5.5 4.5

YEARS ENDED

DECEMBER 31,

2013 2012

YEARS ENDED

$ 1,117.60

28.3 28.3

32.6 32.5

YEARS ENDED

Change

24%

Change

-18%

Change

14. F l o r i d a S t a t e U n i v e r s i t y P a g e | 14

Figure-7: Base DCF Model/Sensitivity Analysis

Operating Scenario Base

1 Year 1 Year 2 Year 3 Year 4 Year 5

Mid-Year Convention Y Historical Period CAGR CAGR

2011 2012 2013 ('11 - '13) 2014 2015 2016 2017 2018 2019 ('15 - '19)

Sales $3,841.3 $3,987.8 $4,129.2 3.7% $4,420.0 $4,729.4 $5,060.5 $5,364.1 $5,578.6 $5,746.0 5.4%

% growth NA 3.8% 3.5% 7.0% 7.0% 7.0% 6.0% 4.0% 3.0%

Cost of Goods Sold 2,320.1 2,398.7 2,491.6 2,652.0 2,837.6 3,036.3 3,218.5 3,347.2 3,447.6

Gross Profit $1,521.1 $1,589.1 $1,637.7 3.8% $1,768.0 $1,891.8 $2,024.2 $2,145.6 $2,231.5 $2,298.4 5.4%

% margin 39.6% 39.9% 39.7% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0%

Expenses Before Depreciation 1,162.3 1,284.9 1,232.6 1,360.4 1,455.6 1,557.5 1,650.9 1,717.0 1,768.5

EBITDA $358.8 $304.2 $405.0 6.2% $446.0 $436.2 $466.7 $494.7 $514.5 $529.9 3.5%

% margin 9.3% 7.6% 9.8% 10.09% 9.2% 9.2% 9.2% 9.2% 9.2%

Depreciation & Amortization 153.7 155.5 164.1 187.0 187.2 200.3 212.3 220.8 227.4

EBIT $205.1 $148.7 $240.9 8.4% $259.0 $249.0 $266.4 $282.4 $293.7 $302.5 3.2%

% margin 5.3% 3.7% 5.8% 5.9% 5.3% 5.3% 5.3% 5.3% 5.3%

Taxes 80.2 58.1 94.2 101.3 97.4 104.2 110.4 114.8 118.3

EBIAT $124.9 $90.6 $146.7 8.4% $157.7 $151.6 $162.2 $172.0 $178.9 $184.2 3.2%

Plus: Depreciation & Amortization 153.7 155.5 164.1 187.0 187.2 200.3 212.3 220.8 227.4

Less: Capital Expenditures (120.9) (178.7) (237.2) (253.9) (278.7) (298.2) (316.1) (250.0) (257.5)

% margin 3.1% 4.5% 5.7% 5.9% 5.9% 5.9% 4.5% 4.5%

Less: Inc./(Dec.) in Net Working Capital 94.1 41.0 37.6 26.6 20.7

Unlevered Free Cash Flow Free Cash Flow $154.3 $105.4 $105.9 $176.3 $174.9

$27.9 Dividends $30.0 $30.0 $30.0 $30.0 $30.0

Target WACC 7.57% 0.0% Dynamic WACC 7.43% 7.51% 7.56% 7.58% 7.57% 7.5%

Discount Period 0.5 1.5 2.5 3.5 4.5

Discount Factor 0.96 0.90 0.83 0.77 0.72

Present Value of Free Cash Flow $148.9 $94.6 $88.2 $136.5 $125.9

Enterprise Value Implied Perpetuity Growth Rate

Cumulative Present Value of FCF $594.1 Enterprise Value $5,361.4 Terminal Year Free Cash Flow (2019E) $174.9

Less: Total Debt (2,256.6) WACC 7.6%

Terminal Value Less: Preferred Stock - Terminal Value $6,867.9

Terminal Year EBITDA (2019E) $529.9 Less: Noncontrolling Interest -

Exit Multiple Method 12.96x Plus: Cash and Cash Equivalents 463.4 Implied Perpetuity Growth Rate 4.8%

Terminal Value $6,867.9

Discount Factor 0.69 Implied Equity Value $3,568.2 Implied EV/EBITDA

Present Value of Terminal Value $4,767.3 Enterprise Value $5,361.4

% of Enterprise Value 88.9% Fully Diluted Shares Outstanding 128.0 LTM 9/30/2013 EBITDA 446.0

Enterprise Value $5,361.4 Implied Share Price $27.88 Implied EV/EBITDA 12.0x

Enterprise Value Implied Perpetuity Growth Rate

Exit Multiple Exit Multiple

5,361.4 12.0x 12.5x 12.96x 13.5x 14.0x 0.0 12.0x 12.5x 12.96x 13.5x 14.0x

6.6% 5,204 5,397 5,589 5,782 5,975 6.6% 3.6% 3.7% 3.8% 3.9% 4.0%

7.1% 5,097 5,285 5,474 5,662 5,850 7.1% 4.1% 4.2% 4.3% 4.4% 4.5%

7.6% 4,994 5,177 $5,361 5,545 5,729 7.6% 4.6% 4.7% 4.8% 4.9% 5.0%

8.1% 4,893 5,072 5,252 5,432 5,612 8.1% 5.1% 5.2% 5.3% 5.4% 5.5%

8.6% 4,795 4,970 5,146 5,321 5,497 8.6% 5.5% 5.7% 5.8% 5.9% 6.0%

Assumptions

Sales (% growth) NA 3.8% 3.5% 7.0% 7.0% 7.0% 6.0% 4.0% 3.0%

COGS (% sales) 60.4% 60.2% 60.3% 60.0% 60.0% 60.0% 60.0% 60.0% 60.0%

Exp Before Deprec (% of sales) 30.3% 32.2% 29.9% 30.8% 30.8% 30.8% 30.8% 30.8% 30.8%

Depreciation & Amortization (% sales) 4.0% 3.9% 4.0% 4.2% 4.0% 4.0% 4.0% 4.0% 4.0%

Capital Expenditures (% sales) 3.1% 4.5% 5.7% 5.7% 5.9% 5.9% 5.9% 4.5% 4.5%

Tax Rate 39.1% 39.1% 39.1% 39.1% 39.1% 39.1% 39.1% 39.1% 39.1%

Working Capital (% sales) (12.4%) (12.4%) (12.4%) (12.4%) (12.4%)

Bloomin' Brands Inc

Sensitivity Analysis

($ in millions, fiscal year ending December 31)

Enterprise Value Implied Equity Value

Exit Multiple Exit Multiple

5,361.4 -1.0x -0.5x 0.0x 0.5x 1.0x 3,568.2 12.0x 12.5x 13.0x 13.5x 14.0x

-1.0% 37 315 594 873 1,151 5.4% 3,685 3,889 4,092 4,296 4,499

-0.5% 51 322 594 866 1,137 5.9% 3,571 3,770 3,968 4,167 4,366

0.0% 64 329 $594 859 1,124 6.4% 3,460 3,654 $3,848 4,042 4,236

0.5% 77 336 594 853 1,111 6.9% 3,352 3,542 3,731 3,921 4,110

1.0% 90 342 594 846 1,098 7.4% 3,247 3,432 3,617 3,803 3,988

Implied Perpetuity Growth Rate

Exit Multiple Exit Multiple

0.0 -1.0x -0.5x 0.0x 0.5x 1.0x 12.0 6.5x 7.0x 13.0x 13.5x 14.0x

-1.0% 47.4% 188.5% -100.0% -40.2% -25.5% -1.0% 9.5x 10.1x 10.1x 10.7x 12.0x

-0.5% 48.3% 191.4% -100.0% -40.0% -25.1% -0.5% 9.3x 9.9x 9.9x 10.5x 11.7x

0.0% 49.3% 194.3% -100.0% -39.8% -24.8% 0.0% 9.1x 9.6x 9.6x 10.2x 11.4x

0.5% 50.2% 197.2% -100.0% -39.5% -24.5% 0.5% 8.9x 9.4x 9.4x 10.0x 11.2x

1.0% 51.1% 200.1% -100.0% -39.3% -24.2% 1.0% 8.7x 9.2x 9.2x 9.8x 10.9x

PV of Terminal Value % of Enterprise Value

Exit Multiple

0.9 6.5x 7.0x 7.5x 8.0x 8.5x

6.6% 80.8% 82.0% 83.0% 83.8% 84.6%

7.1% 81.2% 82.3% 83.3% 84.2% 85.0%

7.6% 81.2% 82.3% 83.3% 84.2% 85.0%

8.1% 80.8% 82.0% 83.0% 83.8% 84.6%

8.6% 80.1% 81.3% 82.3% 83.2% 84.0%

WACC

WACC

WACC

Implied Enterprise Value / LTM EBITDA

WACC

WACC

WACC

WACC

Bloomin' Brands Inc

Discounted Cash Flow Analysis

($ in millions, fiscal year ending December 31)

Projection Period

Implied Equity Value and Share Price

15. F l o r i d a S t a t e U n i v e r s i t y P a g e | 15

Figure-8: Bull DCF Model/Sensitivity Analysis

Operating Scenario Base

1 Year 1 Year 2 Year 3 Year 4 Year 5

Mid-Year Convention Y Historical Period CAGR CAGR

2011 2012 2013 ('11 - '13) 2014 2015 2016 2017 2018 2019 ('15 - '19)

Sales $3,841.3 $3,987.8 $4,129.2 3.7% $4,420.0 $4,950.4 $5,544.4 $6,154.3 $6,646.7 $6,846.1 9.1%

% growth NA 3.8% 3.5% 7.0% 12.0% 12.0% 11.0% 8.0% 3.0%

Cost of Goods Sold 2,320.1 2,398.7 2,491.6 2,652.0 2,970.2 3,326.7 3,692.6 3,988.0 4,107.7

Gross Profit $1,521.1 $1,589.1 $1,637.7 3.8% $1,768.0 $1,980.2 $2,217.8 $2,461.7 $2,658.7 $2,738.4 9.1%

% margin 39.6% 39.9% 39.7% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0%

Expenses Before Depreciation 1,162.3 1,284.9 1,232.6 1,360.4 1,523.6 1,706.4 1,894.1 2,045.7 2,107.1

EBITDA $358.8 $304.2 $405.0 6.2% $446.0 $456.6 $511.3 $567.6 $613.0 $631.4 7.2%

% margin 9.3% 7.6% 9.8% 10.09% 9.2% 9.2% 9.2% 9.2% 9.2%

Depreciation & Amortization 153.7 155.5 164.1 187.0 195.9 219.4 243.6 263.1 271.0

EBIT $205.1 $148.7 $240.9 8.4% $259.0 $260.6 $291.9 $324.0 $349.9 $360.4 6.8%

% margin 5.3% 3.7% 5.8% 5.9% 5.3% 5.3% 5.3% 5.3% 5.3%

Taxes 80.2 58.1 94.2 101.3 101.9 114.1 126.7 136.8 140.9

EBIAT $124.9 $90.6 $146.7 8.4% $157.7 $158.7 $177.8 $197.3 $213.1 $219.5 6.8%

Plus: Depreciation & Amortization 153.7 155.5 164.1 187.0 195.9 219.4 243.6 263.1 271.0

Less: Capital Expenditures (120.9) (178.7) (237.2) (253.9) (291.7) (326.7) (362.7) (297.9) (306.8)

% margin 3.1% 4.5% 5.7% 5.9% 5.9% 5.9% 4.5% 4.5%

Less: Inc./(Dec.) in Net Working Capital 121.5 73.6 75.6 61.0 24.7

Unlevered Free Cash Flow FCFF $184.5 $144.2 $153.9 $239.4 $208.4

Dividends $30.0 $30.0 $30.0 $30.0 $30.0

Target WACC 7.57% Dynamic WACC 7.43% 7.51% 7.56% 7.58% 7.57% 7.5%

Discount Period 0.5 1.5 2.5 3.5 4.5

Discount Factor 0.96 0.90 0.83 0.77 0.72

Present Value of Free Cash Flow $178.0 $129.3 $128.2 $185.3 $150.0

Enterprise Value Implied Perpetuity Growth Rate

Cumulative Present Value of FCF $771.0 Enterprise Value $6,450.9 Terminal Year Free Cash Flow (2019E) $208.4

Less: Total Debt (2,256.6) WACC 7.6%

Terminal Value Less: Preferred Stock - Terminal Value $8,182.7

Terminal Year EBITDA (2019E) $631.4 Less: Noncontrolling Interest -

EMM Method 12.96x Plus: Cash and Cash Equivalents 552.1 Implied Perpetuity Growth Rate 4.8%

Terminal Value $8,182.7

Discount Factor 0.69 Implied Equity Value $4,746.4 Implied EV/EBITDA

Present Value of Terminal Value $5,679.9 Enterprise Value $6,450.9

% of Enterprise Value 88.0% Fully Diluted Shares Outstanding 128.0 LTM 9/30/2012 EBITDA 446.0

Enterprise Value $6,450.9 Implied Share Price $37.08 Implied EV/EBITDA 14.5x

Enterprise Value Implied Perpetuity Growth Rate

Exit Multiple Exit Multiple

6,450.9 12.0x 12.5x 12.96x 13.5x 14.0x 0.0 12.0x 12.5x 12.96x 13.5x 14.0x

6.6% 6,264 6,494 6,724 6,953 7,183 6.6% 3.6% 3.7% 3.8% 3.9% 4.0%

7.1% 6,137 6,362 6,586 6,810 7,035 7.1% 4.1% 4.2% 4.3% 4.4% 4.5%

7.6% 6,014 6,233 $6,452 6,671 6,891 7.6% 4.6% 4.7% 4.8% 4.9% 5.0%

8.1% 5,894 6,108 6,322 6,536 6,750 8.1% 5.1% 5.2% 5.3% 5.4% 5.5%

8.6% 5,777 5,986 6,195 6,405 6,614 8.6% 5.5% 5.7% 5.8% 5.9% 6.0%

Assumptions

Sales (% growth) NA 3.8% 3.5% 7.0% 12.0% 12.0% 11.0% 8.0% 3.0%

COGS (% sales) 60.4% 60.2% 60.3% 60.0% 60.0% 60.0% 60.0% 60.0% 60.0%

Exp Before Deprec (% of sales) 30.3% 32.2% 29.9% 30.8% 30.8% 30.8% 30.8% 30.8% 30.8%

Depreciation & Amortization (% sales) 4.0% 3.9% 4.0% 4.2% 4.0% 4.0% 4.0% 4.0% 4.0%

Capital Expenditures (% sales) 3.1% 4.5% 5.7% 5.7% 5.9% 5.9% 5.9% 4.5% 4.5%

Tax Rate 39.1% 39.1% 39.1% 39.1% 39.1% 39.1% 39.1% 39.1% 39.1%

Working Capital (% sales) (12.4%) (12.4%) (12.4%) (12.4%) (12.4%)

Bloomin' Brands Inc

Sensitivity Analysis

($ in millions, fiscal year ending December 31)

Enterprise Value Implied Equity Value

Exit Multiple Exit Multiple

6,450.9 -1.0x -0.5x 0.0x 0.5x 1.0x 4,746.4 12.0x 12.5x 12.96x 13.5x 14.0x

-1.0% 107 439 771 1,103 1,435 5.8% 4,766 5,004 5,242 5,480 5,719

-0.5% 124 447 771 1,095 1,418 6.3% 4,633 4,865 5,098 5,331 5,564

0.0% 140 455 $771 1,087 1,402 6.8% 4,504 4,731 $4,958 5,186 5,413

0.5% 155 463 771 1,079 1,387 7.3% 4,378 4,600 4,822 5,044 5,266

1.0% 170 471 771 1,071 1,372 7.8% 4,256 4,473 4,690 4,907 5,124

Implied Perpetuity Growth Rate Implied Enterprise Value / LTM EBITDA

Exit Multiple Exit Multiple

0.0 -1.0x -0.5x 0.0x 0.5x 1.0x 14.5 6.5x 7.0x 12.96x 13.5x 14.0x

-1.0% 47.4% 188.5% -100.0% -40.2% -25.5% 5.8% 8.7x 9.2x 15.6x 16.1x 16.6x

-0.5% 48.3% 191.4% -100.0% -40.0% -25.1% 6.3% 8.5x 9.0x 15.3x 15.8x 16.3x

0.0% 49.3% 194.2% -100.0% -39.8% -24.8% 6.79% 8.4x 8.9x 14.9x 15.4x 16.0x

0.5% 50.2% 197.2% -100.0% -39.5% -24.5% 7.3% 8.2x 8.7x 14.6x 15.1x 15.6x

1.0% 51.1% 200.1% -100.0% -39.3% -24.2% 7.8% 8.1x 8.5x 14.3x 14.8x 15.3x

PV of Terminal Value % of Enterprise Value

Exit Multiple

0.9 12.0x 12.5x 13.0x 13.5x 14.0x

5.8% 88.1% 88.5% 88.9% 89.3% 89.6%

6.3% 87.8% 88.3% 88.7% 89.0% 89.4%

6.8% 87.6% 88.0% 88.4% 88.8% 89.2%

7.3% 87.3% 87.8% 88.2% 88.6% 88.9%

7.8% 87.1% 87.5% 87.9% 88.3% 88.7%

WACC

WACC

WACC

WACC

WACC

WACC

WACC

Bloomin' Brands Inc

Discounted Cash Flow Analysis

($ in millions, fiscal year ending December 31)

Projection Period

Implied Equity Value and Share Price

16. F l o r i d a S t a t e U n i v e r s i t y P a g e | 16

Figure-9: Bear DCF Model/Sensitivity Analysis

Operating Scenario Base

1 Year 1 Year 2 Year 3 Year 4 Year 5

Mid-Year Convention Y Historical Period CAGR CAGR

2011 2012 2013 ('11 - '13) 2014 2015 2016 2017 2018 2019 ('15 - '19)

Sales $3,841.3 $3,987.8 $4,129.2 3.7% $4,420.0 $4,420.0 $4,420.0 $4,420.0 $4,420.0 $4,420.0 0.0%

% growth NA 3.8% 3.5% 7.0% - - - - -

Cost of Goods Sold 2,320.1 2,398.7 2,491.6 2,652.0 2,652.0 2,652.0 2,652.0 2,652.0 2,652.0

Gross Profit $1,521.1 $1,589.1 $1,637.7 3.8% $1,768.0 $1,768.0 $1,768.0 $1,768.0 $1,768.0 $1,768.0 0.0%

% margin 39.6% 39.9% 39.7% 40.0% 40.0% 40.0% 40.0% 40.0% 40.0%

Expenses Before Depreciation 1,162.3 1,284.9 1,232.6 1,360.4 1,360.4 1,360.4 1,360.4 1,360.4 1,360.4

EBITDA $358.8 $304.2 $405.0 6.2% $446.0 $407.6 $407.6 $407.6 $407.6 $407.6 -1.8%

% margin 9.3% 7.6% 9.8% 10.09% 9.2% 9.2% 9.2% 9.2% 9.2%

Depreciation & Amortization 153.7 155.5 164.1 187.0 174.9 174.9 174.9 174.9 174.9

EBIT $205.1 $148.7 $240.9 8.4% $259.0 $232.7 $232.7 $232.7 $232.7 $232.7 -2.1%

% margin 5.3% 3.7% 5.8% 5.9% 5.3% 5.3% 5.3% 5.3% 5.3%

Taxes 80.2 58.1 94.2 101.3 91.0 91.0 91.0 91.0 91.0

EBIAT $124.9 $90.6 $146.7 8.4% $157.7 $141.7 $141.7 $141.7 $141.7 $141.7 -2.1%

Plus: Depreciation & Amortization 153.7 155.5 164.1 187.0 174.9 174.9 174.9 174.9 174.9

Less: Capital Expenditures (120.9) (178.7) (237.2) (253.9) (260.5) (260.5) (260.5) (198.1) (198.1)

% margin 3.1% 4.5% 5.7% 5.9% 5.9% 5.9% 4.5% 4.5%

Less: Inc./(Dec.) in Net Working Capital 55.8 (4.4) 4.4 - -

Unlevered Free Cash Flow FCFF $112.0 $51.8 $60.7 $118.6 $118.6

Dividends $30.0 $30.0 $30.0 $30.0 $30.0

Target WACC 7.57% Dynamic WACC 7.43% 7.51% 7.56% 7.58% 7.57% 7.5%

Discount Period 0.5 1.5 2.5 3.5 4.5

Discount Factor 0.96 0.90 0.83 0.77 0.72

Present Value of Free Cash Flow $108.1 $46.5 $50.5 $91.8 $85.4

Enterprise Value Implied Perpetuity Growth Rate

Cumulative Present Value of FCF $382.4 Enterprise Value $4,049.5 Terminal Year Free Cash Flow (2019E) $118.6

Less: Total Debt (2,256.6) WACC 7.6%

Terminal Value Less: Preferred Stock - Terminal Value $5,283.0

Terminal Year EBITDA (2019E) $407.6 Less: Noncontrolling Interest -

EMM Method 12.96x Plus: Cash and Cash Equivalents 356.5 Implied Perpetuity Growth Rate 5.1%

Terminal Value $5,283.0

Discount Factor 0.69 Implied Equity Value $2,149.3 Implied EV/EBITDA

Present Value of Terminal Value $3,667.1 Enterprise Value $4,049.5

% of Enterprise Value 90.6% Fully Diluted Shares Outstanding 128.0 LTM 9/30/2012 EBITDA 446.0

Enterprise Value $4,049.5 Implied Share Price $16.79 Implied EV/EBITDA 9.1x

Enterprise Value Implied Perpetuity Growth Rate

Exit Multiple Exit Multiple

4,049.5 12.0x 12.5x 12.96x 13.5x 14.0x 0.1 12.0x 12.5x 12.96x 13.5x 14.0x

6.6% 3,929 4,077 4,226 4,374 4,522 6.6% 4.0% 4.1% 4.2% 4.2% 4.3%

7.1% 3,847 3,992 4,137 4,282 4,426 7.1% 4.4% 4.5% 4.6% 4.7% 4.8%

7.6% 3,767 3,909 $4,050 4,192 4,333 7.6% 4.9% 5.0% 5.1% 5.2% 5.3%

8.1% 3,690 3,828 3,966 4,104 4,243 8.1% 5.4% 5.5% 5.6% 5.7% 5.8%

8.6% 3,614 3,749 3,884 4,020 4,155 8.6% 5.9% 6.0% 6.1% 6.2% 6.3%

Assumptions

Sales (% growth) NA 3.8% 3.5% 7.0% - % - % - % - % - %

COGS (% sales) 60.4% 60.2% 60.3% 60.0% 60.0% 60.0% 60.0% 60.0% 60.0%

Exp Before Deprec (% of sales) 30.3% 32.2% 29.9% 30.8% 30.8% 30.8% 30.8% 30.8% 30.8%

Depreciation & Amortization (% sales) 4.0% 3.9% 4.0% 4.2% 4.0% 4.0% 4.0% 4.0% 4.0%

Capital Expenditures (% sales) 3.1% 4.5% 5.7% 5.7% 5.9% 5.9% 5.9% 4.5% 4.5%

Tax Rate 39.1% 39.1% 39.1% 39.1% 39.1% 39.1% 39.1% 39.1% 39.1%

Working Capital (% sales) (12.4%) (12.3%) (12.4%) (12.4%) (12.4%)

Bloomin' Brands Inc

Sensitivity Analysis

($ in millions, fiscal year ending December 31)

Enterprise Value Implied Equity Value

Exit Multiple Exit Multiple

4,049.5 -1.0x -0.5x 0.0x 0.5x 1.0x 2,149.3 12.0x 12.5x 13.0x 13.5x 14.0x

-1.0% (46) 168 382 597 811 5.4% 2,239 2,396 2,552 2,709 2,865

-0.5% (36) 173 382 591 800 5.9% 2,151 2,304 2,457 2,610 2,763

0.0% (25) 179 $382 586 790 6.4% 2,066 2,215 $2,365 2,514 2,663

0.5% (15) 184 382 581 780 6.9% 1,983 2,129 2,275 2,421 2,566

1.0% (5) 188 382 576 770 7.4% 1,902 2,045 2,187 2,330 2,472

Implied Perpetuity Growth Rate Implied Enterprise Value / LTM EBITDA

Exit Multiple Exit Multiple

0.1 -1.0x -0.5x 0.0x 0.5x 1.0x 9.1 6.5x 7.0x 13.0x 13.5x 14.0x

-1.0% 39.3% 135.2% -100.0% -37.3% -23.2% -1.0% 7.1x 7.6x 7.6x 8.1x 9.0x

-0.5% 40.2% 137.2% -100.0% -37.0% -22.9% -0.5% 6.9x 7.4x 7.4x 7.9x 8.8x

0.0% 41.0% 139.2% -100.0% -36.8% -22.5% 0.0% 6.8x 7.3x 7.3x 7.7x 8.6x

0.5% 41.9% 141.2% -100.0% -36.5% -22.2% 0.5% 6.7x 7.1x 7.1x 7.5x 8.4x

1.0% 42.7% 143.3% -100.0% -36.3% -21.9% 1.0% 6.5x 6.9x 6.9x 7.4x 8.2x

PV of Terminal Value % of Enterprise Value

Exit Multiple

0.9 6.5x 7.0x 7.5x 8.0x 8.5x

6.6% 83.4% 84.4% 85.3% 86.1% 86.8%

7.1% 83.8% 84.7% 85.6% 86.4% 87.1%

7.6% 83.8% 84.7% 85.6% 86.4% 87.1%

8.1% 83.4% 84.4% 85.3% 86.1% 86.8%

8.6% 82.8% 83.8% 84.7% 85.5% 86.3%

WACC

WACC

WACC

WACC

WACC

WACC

WACC

Bloomin' Brands Inc

Discounted Cash Flow Analysis

($ in millions, fiscal year ending December 31)

Projection Period

Implied Equity Value and Share Price

17. F l o r i d a S t a t e U n i v e r s i t y P a g e | 17

Figure-10: Capex Break-down

Figure-11: Sequential Capex Analysis

Capex by Division

in millions 2011 2012 2013 2014E

Development/relocations 14 70-75 105-120 130-135

Remodels 49 60-65 60-65 60-65

IT 12 20-25 20-25 20-25

Maintenance/Other 46 50-55 35-40 30-35

Total Guided 121 200-220 220-250 215-235

Actual/Estimate 121 178 237 220

For the Fiscal Period Ending 12/31/2014 9/28/2014 6/29/2014 3/30/2014 12/31/2013 12/31/2013 9/30/2013 6/30/2013 3/31/2013 12/31/2012 12/31/2012 9/30/2012 6/30/2012 3/30/2012 12/31/2011

Capital expenditures (Total) (174,432) (97,619) (39,313) (237,214) (71,060) (166,154) (97,150) (40,950) (178,720) (44,554) (134,166) (79,743) (34,019) (120,906)

for the period (76,813) (58,306) (39,313) (237,214) (71,060) (69,004) (56,200) (40,950) (178,720) (44,554) (54,423) (45,724) (34,019) (120,906)

Revenues 1,065,454 1,110,912 1,157,859 4,129,230 1,050,555 967,569 1,018,856 1,092,250 3,987,795 998,387 952,916 980,866 1,055,626 3,841,264

CapEx as % of Rev 16.37% 8.79% 3.40% 5.74% 6.76% 17.17% 9.54% 3.75% 4.48% 4.46% 14.08% 8.13% 3.22% 3.15%

12%

40%

10%

38%

2011 Capital

Expenditure

Breakdown

Development/relocations

Remodels

IT

Maintenance/Other

34%

30%

11%

25%

2012 Capital

Expenditure

Breakdown

Development/relocations

Remodels

IT

Maintenance/Other

53%

25%

9%

13%

2014 Est. Capital

Expenditure

Breakdown

Development/relocations

Remodels

IT

Maintenance/Other

0.00%

20.00%

40.00%

50,000

100,000

150,000

200,000

250,000

1/1/2012 1/1/2013 1/1/2014

$ofCapExinthousands

Annual Capex Analysis

Capital Expenditures capex % rev

Capex ytd rate of change Revenue ytd growth

18. F l o r i d a S t a t e U n i v e r s i t y P a g e | 18

Figure-12: Balance Sheet

Balance Sheet

Balance sheet as of: 12/31/2014 9/28/2014 6/29/2014 3/30/2014 12/31/2013 12/31/2012

Assets

Cash and cash equivalents 144,671$ 155,843$ 172,604$ 209,871$ 261,690$

Current restricted cash equivalents 4,542 3,822 2,859 3,364 4,846

Inventories 64,748 65,337 66,799 80,613 78,181

Deferred income taxes 70,137 70,033 69,994 70,802 39,774

Assets held for sale 26,713

Other current assets, net 140,648 132,879 119,008 119,381 103,321

Total Current Assets 451,459 427,914 431,264 484,031 487,812

Restriced cash 26,265 25,892 25,042 25,055 15,243

PPE 1,640,198 1,652,326 1,626,988 1,634,130 1,506,035

Goodwill 359,167 353,086 346,424 346,253 270,972

Intangible assets 600,132 610,782 611,294 617,133 551,779

Deferred income tax assets 3,341 3,372 2,790 2,392 2,532

Other assets, net 153,750 160,707 164,988 165,180 182,180

Total Assets 3,234,312$ 3,234,079$ 3,208,790$ 3,274,174$ 3,016,553$

Liabilities

Accounts payable 200,268$ 188,278$ 176,911$ 164,619$ 131,814$

Accrued and other current liabilities 206,242 190,982 197,276 194,346 192,284

Partner obligations 10,670 9,268 10,174 12,548 14,771

Unearned revenue 226,914 249,322 261,251 359,443 329,518

Current long-term debt 40,751 22,328 11,997 13,546 22,991

Total Current Liabilities 684,845 660,178 657,609 744,502 691,378

Partner deposits and obligations 71,347 75,780 74,863 78,116 85,762

Deffered rent 118,299 114,743 108,098 105,963 87,641

Deffered tax liabilites 142,548 144,805 142,703 150,582 195,874

Long term debt 1,372,341 1,382,161 1,393,136 1,405,597 1,471,449

Other long-term liabiliies 250,495 253,896 280,104 284,721 264,244

Total Liabilities 2,639,875 2,631,563 2,656,513 2,769,481 2,796,348

Redeamable noncontrolling interests 24,525 23,043 22,101 21,984 -

Common stock 1,256 1,256 1,255 1,248 1,211

APIC 1,076,847 1,071,389 1,066,959 1,068,705 1,000,963

Retained earnings (497,342) (485,829) (511,902) (565,154) (773,085)

Accumulated other comprehensive income (15,935) (12,695) (31,783) (26,418) (14,801)

Noncontroling interests 5,086 5,352 5,647 4,328 5,917

Total shareholders equity 569,912 579,473 530,176 482,709 220,205

Total Liabilities and Equity 3,234,312$ 3,234,079$ 3,208,790$ 3,274,174$ 3,016,553$

19. F l o r i d a S t a t e U n i v e r s i t y P a g e | 19

Figure-13: Cash Flow Statement

Cash Flow

For the Fiscal Period Ending 12/31/2014 9/28/2014 6/29/2014 3/30/2014 12/31/2013 12/31/2012 12/31/2011

Net income 71,992$ 82,822$ 55,100$ 214,568$ 61,304$ 109,179$

Depreciation and amortization 143,542 94,792 46,165 164,094 155,482 153,689

Amortization of deferred financing fees 2,378 1,640 848 3,574 8,222 12,297

Amortization of capitalized gift card sales commissions 20,144 14,829 8,792 23,826 21,136 18,058

Depreciation & Amort, total 166,064$ 111,261$ 55,805$ 191,494$ 184,840$ 184,044$

Provision for impaired assets and restaurant closings 36,170 7,089 6,064 22,838 13,005 14,039

Accretion on debt discounts 1,589 1,097 568 2,451 880 663

Stock-based and other non-cash compensation expense 14,546 9,672 2,357 21,589 44,778 39,228

Income from operations of unconsolidated affiliates - - - (7,730) (5,450) (8,109)

Deferred income tax benefit (1,687) (372) (876) (83,603) (7,442) (175)

Loss on disposal of property, fixtures and equipment 1,548 1,077 436 1,441 2,141 1,987

Gain on life insurance and restricted cash investments (1,305) (1,732) (362) (5,284) (5,150) (126)

Loss on extinguishment and modification of debt 11,092 11,092 14,586 20,957 -

Other gains relating to sale of business (36,608) (3,500) (28,819)

Deferred gain on sale-leaseback (1,605) (1,070) (535) (2,135) (1,610) -

Excess tax benefits from stock-based compensation (1,067) (1,095) (1,221) (4,363) - -

Change in assets and liabilities:

Decrease in inventories 14,707 15,724 13,788 3,768 (8,577) (10,525)

Increase in other current assets (34,489) (25,212) (7,463) (28,336) (13,746) (60,858)

Decrease (increase) in other assets 6,141 5,320 2,591 (259) 4,034 8,209

Decrease in accounts payable and current liab (2,059) (11,440) 11,957 10,192 4,687 32,875

Increase in deferred rent 14,969 8,482 2,080 20,618 17,064 12,510

Decrease in unearned revenue (134,545) (110,392) (98,214) 29,634 29,621 30,623

Decrease in other long-term liabilities (2,513) (5,077) (2,248) 12,403 2,255 (2,295)

Cash from Operations 159,548 97,246 39,827 377,264 340,091 322,450

Capital expenditures (174,432) (97,619) (39,313) (237,214) (178,720) (120,906)

Purchases of life insurance policies (1,682) 627 627 (4,159) (6,451) (2,027)

Sale of life insurance policies 627 562 105 1,239 - 2,638

Proceeds from PPE 4,070 (3,063) (3,063) 3,223 4,529 2,150

Sale-leaseback transaction - 192,886 -

Acquisition of business, net of cash acquired (3,063) (1,040) (520) (100,319) 3,500 1,572

Decrease in restricted cash 19,612 13,556 5,514 29,210 84,270 86,579

Increase in restricted cash (21,150) (14,192) (5,105) (38,117) (80,070) (83,148)

Cash from Investing (176,018)$ (101,169)$ (41,755)$ (346,137)$ 19,944$ (113,142)$

Proceeds Loan B & CMBS 1,485,186$

Senior secured Term loan A 297,088$ 297,088$

Extinguishment an of senior secured term loan (700,000) (700,000) - (1,004,575) -

Repayments of long-term debt (25,159) (18,090) (14,578)$ (80,805) (46,868) (25,189)

Proceeds from borrowings on revolving credit facilities 474,500 415,000 100,000 111,000 33,000

Repayments of borrowings on revolving credit facilities (59,500) (15,000) (100,000) (144,000) (78,072)

Financing fees (4,492) (4,492) (12,519) (18,983) (2,222)

Proceeds from the exercise of stock options 7,042 6,476 5,974 27,786 884 -

Distributions to noncontrolling interests (3,331) (2,470) (1,167) (8,059) (13,977) (13,088)

Purchase of limited partnership interests (17,211) (17,211) (17,211) - (40,582) -

Partner deposits and accrued partner obligations (17,603) (13,909) (7,388) (23,286) (25,397) (35,950)

Repayments of notes receivable due from stockholders - - - - (587) (1,082)

Repurchase of common stock (869) (799) (481) (436) - -

Excess tax benefits from stock-based compensation 1,067 1,095 1,221 4,363 - -

Tax withholding on performance-based share units (400) (364) (324)

Other proceeds/extinguish from initial offering and debt, net 5,829 (888,320) 33,303

Cash from Financing (48,868) (52,676) (33,954) (87,127) (586,219) (89,300)

Forex rate changes on cash 138 2,571 (1,385) 4,181 5,790 (3,460)

Net Change in Cash (65,200) (54,028) (37,267) (51,819) (220,394) 116,548

FCF1 (CFO-Capex) (14,884)$ 96,206$ 39,307$ 276,945$ 343,591$ 324,022$

FCF2 (NI+ D&A - CapEX 63,624$ 193,043$ 110,385$ 305,743$ 249,644$ 294,795$

20. F l o r i d a S t a t e U n i v e r s i t y P a g e | 20

Figure-14: Free Cash Flows

Source: Bloomin’ Q3 Investor Conference

Figure-15: Updated Q3 Results

Source: Bloomin’ Q3 Investor Conference

Figure-16: Margin Improvement

Source: Bloomin’ Q3 Investor Conference

21. F l o r i d a S t a t e U n i v e r s i t y P a g e | 21

Figure-17: Operational Growth

Source: Bloomin’ Q3 Investor Conference

Figure-18: Comp Sales vs. KNAPP Track

Source: Bloomin’ Q3 Investor Conference

22. F l o r i d a S t a t e U n i v e r s i t y P a g e | 22

Figure-19: Growth in Comp Sales & Profitability vs. KNAPP

Source: Bloomin’ Q3 Investor Conference

Figure-20: Growth in Comp Sales: Lunch

Source: Bloomin’ Q3 Investor Conference