2017 Flexible Consumption Impact Survey

•

2 j'aime•4,748 vues

Deloitte's 2017 Flexible Consumption Impact Survey results are here! Explore pain points and potential improvements to enhance customer experience, drive retention and operate in an evolving market here: http://www2.deloitte.com/us/en/pages/technology-media-and-telecommunications/articles/enterprise-it-offerings-flexible-consumption-survey.html?id=us:2sm:3ss:flexsurvey:eng:cons:061217

Recommandé

Recommandé

Contenu connexe

Plus de Deloitte United States

Plus de Deloitte United States (20)

Dernier

Dernier (20)

2017 Flexible Consumption Impact Survey

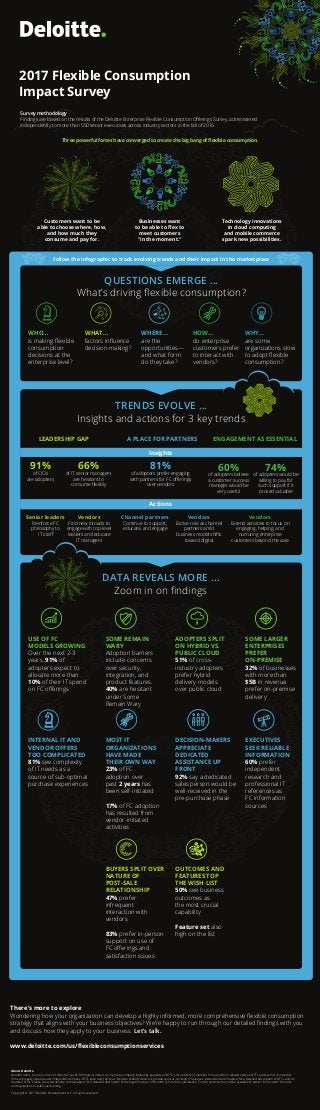

- 1. Customers want to be able to choose where, how, and how much they consume and pay for. Businesses want to be able to flex to meet customers "in the moment." Technology innovations in cloud computing and mobile commerce spark new possibilities. About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting. Copyright © 2017 Deloitte Development LLC. All rights reserved. Follow the infographic to track evolving trends and their impact in the marketplace QUESTIONS EMERGE ... What’s driving flexible consumption? TRENDS EVOLVE ... Insights and actions for 3 key trends DATA REVEALS MORE ... Zoom in on findings WHY… are some organizations slow to adopt flexible consumption? WHO… is making flexible consumption decisions at the enterprise level? WHAT… factors influence decision-making? WHERE… are the opportunities— and what form do they take? ENGAGEMENT AS ESSENTIALLEADERSHIP GAP A PLACE FOR PARTNERS HOW… do enterprise customers prefer to interact with vendors? USE OF FC MODELS GROWING Over the next 2-3 years, 91% of adopters expect to allocate more than 10% of their IT spend on FC offerings SOME REMAIN WARY Adoption barriers include concerns over security, integration, and product features. 40% are hesitant under Some Remain Wary ADOPTERS SPLIT ON HYBRID VS. PUBLIC CLOUD 51% of cross- industry adopters prefer hybrid delivery models over public cloud SOME LARGER ENTERPRISES PREFER ON-PREMISE 32% of businesses with more than $5B in revenue prefer on-premise delivery INTERNAL IT AND VENDOR OFFERS TOO COMPLICATED 81% see complexity of IT needs as a source of sub-optimal purchase experiences MOST IT ORGANIZATIONS HAVE MADE THEIR OWN WAY 23% of FC adoption over past 2 years has been self-initiated 17% of FC adoption has resulted from vendor-initiated activities DECISION-MAKERS APPRECIATE DEDICATED ASSISTANCE UP FRONT 92% say a dedicated sales person would be well-received in the pre-purchase phase EXECUTIVES SEEK RELIABLE INFORMATION 60% prefer independent research and professional IT references as FC information sources BUYERS SPLIT OVER NATURE OF POST-SALE RELATIONSHIP 47% prefer infrequent interaction with vendors 83% prefer in-person support on use of FC offerings and satisfaction issues OUTCOMES AND FEATURES TOP THE WISH LIST 50% see business outcomes as the most crucial capability Feature set also high on the list 91% of CIOs are adopters 66% of IT senior managers are hesitant to consume flexibly 81% of adopters prefer engaging with partners for FC offerings over vendors 60% of adopters believe a customer success manager would be very useful 74% of adopters would be willing to pay for such support if it proved valuable Senior leaders Reinforce FC philosophy to IT staff Vendors Find new inroads to engage with top-level leaders and educate IT managers Vendors Evolve role as channel partners amid business model shifts toward digital Vendors Extend activities to focus on engaging, helping, and nurturing enterprise customers beyond the sale Channel partners Continue to support, educate, and engage There’s more to explore Wondering how your organization can develop a highly informed, more comprehensive flexible consumption strategy that aligns with your business objectives? We’re happy to run through our detailed findings with you and discuss how they apply to your business. Let's talk. www.deloitte.com/us/flexibleconsumptionservices Insights Actions 2017 Flexible Consumption Impact Survey Survey methodology Findings are based on the results of the Deloitte Enterprise Flexible Consumption Offerings Survey, administered independently to more than 550 senior executives across industry sectors in the fall of 2016. Three powerful forces have converged to create the big bang of flexible consumption.