1. IR Department e: ir@ferrovial.com - +34 915862730 1

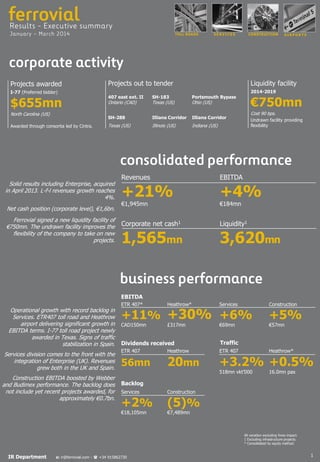

Projects awarded

I-77 (Preferred bidder)

$655mn

North Carolina (US)

Awarded through consortia led by Cintra.

A I R P O R T SCONSTRUCTIONS E R V I C E STOLL ROADS

Dividends received

ETR 407

56mn

Heathrow

20mn

Backlog

ETR 407*

+11%

CAD150mn

Services

+6%

€69mn

Heathrow*

+30%

£317mn

Construction

+5%

€57mn

EBITDA

Revenues

+21%

€1,945mn

EBITDA

+4%

€184mn

Corporate net cash1

1,565mn

Operational growth with record backlog in

Services. ETR407 toll road and Heathrow

airport delivering significant growth in

EBITDA terms. I-77 toll road project newly

awarded in Texas. Signs of traffic

stabilization in Spain.

Services division comes to the front with the

integration of Enterprise (UK). Revenues

grew both in the UK and Spain.

Construction EBITDA boosted by Webber

and Budimex performance. The backlog does

not include yet recent projects awarded, for

approximately €0.7bn.

Solid results including Enterprise, acquired

in April 2013. L-f-l revenues growth reaches

4%.

Net cash position (corporate level), €1,6bn.

Ferrovial signed a new liquidity facility of

€750mn. The undrawn facility improves the

flexibility of the company to take on new

projects.

Liquidity1

3,620mn

Traffic

ETR 407

+3.2%

518mn vkt’000

Heathrow*

+0.5%

16.0mn pax

All variation excluding forex impact.

1 Excluding infrastructure projects.

* Consolidated by equity method.

Services

+2%

€18,105mn

Construction

(5)%

€7,489mn

Projects out to tender

407 east ext. II SH-183 Portsmouth Bypass

Ontario (CAD) Texas (US) Ohio (US)

SH-288 Illiana Corridor Illiana Corridor

Texas (US) Illinois (US) Indiana (US)

Liquidity facility

2014-2019

€750mn

Cost 90 bps.

Undrawn facility providing

flexibility

2. 2

Enterprise acquisition is progressing as expected, with the

necessary actions to achieve synergies in procurement and

supply areas, plus cross-selling between activities.

Revenues

+45.7%

1,033mn

Spain.- Growth in revenues

supported by new contracts. Lower

margins in EBITDA due to costs

related with start up contracts &

integration. Profitability expected to

increase through the year.

EBITDA

+6.1%

69mn/6.7%

UK.- Figures reflect the Enterprise

acquisition (April ‘13). The drop in

profitability is due to lower margins

in Enterprise, expected to increase

trough the year.

Backlog

+1.5%

18,105mn

International.- This division

includes Chile (10mn), Portugal (5mn)

and Poland (2mn).

P&L affected by a provision reversal in 2013 (€7mn).

Excluding this impact, performance would be positive.

Slight improvement in European traffic, although affected

by the Easter timing (April ´14 vs March´13).

Revenues

(5.3)%

91mn

EBITDA

(2.1)%

55mn/60.3%

Positive performance due to the tariff increase and higher

passengers traffic volume.

EBITDA 2014 will be affected by the increase in operating

costs related to the opening of Terminal 2 (June´14).

Revenues

+10.4%

£614mn

EBITDA

+28.0%

£319mn/51.9%

Chicago Skyway

Stake 55%

(5.2)%

32,514

1.1mn

Indiana*

Stake 50%

(3.1)%

21,917

+2.4%

34mn

2.8mn

Ausol **

Stake 80%

(0.4)%

11,867

(5.8)%

7mn

0.4mn

M4

Stake 66%

+4.2%

24,177

+4.4%

5mn

0.1mn

407ETR*

Stake 43%

+3.2%

518mn VKT

+11.2%

122mn

3.8mn

Traffic Revenues EBITDA Net debt

Ferrovial controls 25% of HAH

Consolidated by equity method

Debt

6.8bn

Others

Heathrow +0.5%

16mn

+10.5%

576mn

Traffic Revenues EBITDA

+30.3%

317mn/55.0%

+6.2%

2.5mn

+6.2%

39mn

+16.4%

9mn/24.2%

(2.7)%

12mn

0.9%

24mn/70.1%

(3.7)%

5mn/73.5%

+6.0%

4mn/69.7%

+11.0%

99mn/81.1%

(4.2)%

10mn/83.5%

INVESTOR RELATIONS DEPARTMENT

C/ Príncipe de Vergara, 135 - 28002 MADRID (Spain) Tlf: +34 91 586 27 30 Fax: +34 91 586 28 69

e-mail: ir@ferrovial.es website: www.ferrovial.com

Debt

£12.8bn

RAB £14.9bn

* Consolidated by equity method

** Ausol II traffic

EBITDA growth thanks to better margins at Budimex and

Webber. Backlog does not include recently awarded

projects (I-77 North Carolina, power plant in Poland and a

highway in Australia).

Poland

Budimex.- High level of

contracting activity, based on new

polish government road plan 2014-

2020.

Revenues

0.7%

795mn

US

Webber.-Performance affected

by weather conditions, besides the

lower activity in NTE and LBJ, which

are almost completed.

EBITDA

+4.7%

57mn/7.1%

Backlog

(4.7)%

7,489mn

RoW

F. Agroman.- Important

number of new works contracted

after the end of the quarter, around

€0.9bn. Those new contracts provide

visibility on future growth.

+81.8%

640mn

+49.7%

17mn

(13.8)%

0.4mn/2.1%

+8.8%

375mn

(17.9)%

39mn/10.3%

Revenues EBITDA Backlog

+58.8%

30mn/4.7%

(1.4)%

228mn

(1.1)%

6,264mn

+3.0%

11,613mn

Revenues EBITDA Backlog

(8.9)%

138mn

+25.1%

8mn/6.1%

(10.0)%

986mn

+3.2%

485mn

(0.6)%

41mn/8.5%

(5.4)%

5,413mn

+2.4%

172mn

+18.3%

7mn/4.0%

+4.6%

1,090mn

New regulatory period (Q6) started on 1st April 2014 until

31th December 2018. Maximum allowable yield per

passenger will be RPI minus 1.5%.

2014 tariff increase has been deferred from April to July.

3. Fixed

Assets

17.3bn

Current

Assets

5.6bn

22.9bn

Total

Equity

6.0bn

Non current

Liabilities & others

12.0bn

Current

Liabilities

4.9bn

Gross cash 2.7bn

total

1.6bn

Gross debt 1.1bn

Corporate (1.6)bn

Projects 7.1bn

corporate

53mn

2014

38mn

2015

20mn

2016

11mn

2017

Total cash

2.7bn

Total liquidity 3.6bn

Undrawn lines

0.9bn

1.0bn

2018+

Strong balance sheet and high liquidity position to

face future opportunities.

At the end of March´14, Ferrovial’s net cash

position, excluding infrastructure projects,

amounted to EUR1,565mn.

Standard & Poor’s

BBB / stable

Fitch

BBB- / stable

IR Department e: ir@ferrovial.com - +34 915862730 3

86%

Bonds

4. 4

Women in the company

28,2%

Women in management positions

14%

Spain

55%

America

7%

UK

28%

Poland

6%

RoW

4%

Employees worldwide

66,088

2013

52mn

Investment

In infrastructure &

technologies to reduce

environment impact

2010 - 2013

Lower energy

consumption

2010 2011 2012 2013

311

270

6,900

6,200

2009 - 2013

-31.9%

Reduction of

carbon footprint

Power supply

(,000 Mvh)

-11.6%

Fuels

(,000 Gj)

-8.7%

Risk management

and environment

responsibility

Management of

new business

oportunities

PrioritiesThe combination of talent and commitment made by

Ferrovial’s professionals is one of the pillars of its success

and future sustainability. Professional development,

transversal management of talent and the increasing

internationalisation are among the company’s strategic

priorities, in an environment that guarantees equal

opportunities on the basis of merit.

INVESTOR RELATIONS DEPARTMENT

C/ Príncipe de Vergara, 135 - 28002 MADRID (Spain)

Tlf: +34 91 586 27 30 Fax: +34 91 586 28 69

e-mail: ir@ferrovial.es website: www.ferrovial.com

2013: balanced contribution between fix,

variable and long term incentives:

Metrics of The Long Term Incentive Grant 2013 are a mix of: EBITDA / Net Productive Asset , Cash Flow , TSR *

in comparison with 16 international listed companies:

*ACS, OHL, FCC, Abertis, Paris CdG, Fraport, Serco, Carilion, Bilfinger Berger, Vinci, Strabag, Eiffage, Balfour Beatty, Transurban, SNC Lavalin.

22%

Fix

39%

Variable

39%

Long Term

incentives

2010 Grant

Ferrovial compares with IBEX35 and is in the

average compensation of that group.

Euros

0 200,000 400,000

Percentile

75

0-25%il

25-50%il

50-75%il

75-90%il

Percentile

25

Percentile

90

Mean

Media

Board remuneration non executive

President & CEO remuneration

Source: Towers Watson