Under the lens-audio_slides-08-24-11-stealth_qeiii

•Télécharger en tant que PPTX, PDF•

0 j'aime•745 vues

Recommandé

Recommandé

Contenu connexe

Plus de GordonTLong.com

Plus de GordonTLong.com (20)

Dernier

Dernier (20)

Under the lens-audio_slides-08-24-11-stealth_qeiii

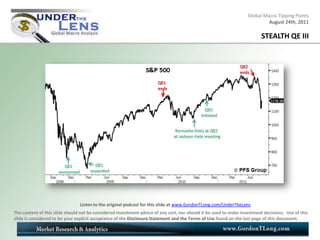

- 1. Global Macro Tipping PointsAugust 24th, 2011 STEALTH QE III Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens The content of this slide should not be considered investment advice of any sort, nor should it be used to make investment decisions. Use of this slide is considered to be your explicit acceptance of the Disclosure Statement and the Terms of Use found on the last page of this document.

- 2. Global Macro Tipping PointsAugust 24th, 2011 STEALTH QE III Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens The content of this slide should not be considered investment advice of any sort, nor should it be used to make investment decisions. Use of this slide is considered to be your explicit acceptance of the Disclosure Statement and the Terms of Use found on the last page of this document.

- 3. Global Macro Tipping PointsAugust 24th, 2011 STEALTH QE III DEFINTIONS NON BORROWED RESERVES (NBR) The NBRs represent the excess capital owned by the commercial banks, which have not been drawn down for use as the capital base for the expansion of bank credit. They currently stand at about $1.76 trillion while in normal circumstances NBRs would be no more than a few tens of billions. High levels of NBRs reflect the reluctance of banks to lend and bankable borrowers to borrow: they are symptomatic of an economy that refuses to expand. REPURCHASE AGREEMENT (Repo) Government Agrees to Buy Back Security for a fixed amount within a specific period of time. REVERSE REPURCHASE AGREEMENT (Reverse Repo) THE BUYER of government securities conducts a reverse repurchase agreement, or a reverse repo. THE INVESTOR in a reverse repo buys securities with an agreement to sell them back to the seller at a fixed price at a future date. For the seller of the securities, the deal is defined as a simple repurchase agreement and is the mirror-image of the reverse repo. If the cost of financing a reverse repo is profitable then the transaction can be highly geared to give a substantial return on the underlying capital. By encouraging this market for short-term government debt, the Fed can exercise tight control over short-maturity government bond yields with benefits extending to medium maturities, irrespective of the quantity issued. CONTINGENT LIABILITY Liability or Debt obligation is contingent on a contractual term. By the nature of a Repo Agreement it is a Contingent Liability with zero effect to the balance sheet. Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens The content of this slide should not be considered investment advice of any sort, nor should it be used to make investment decisions. Use of this slide is considered to be your explicit acceptance of the Disclosure Statement and the Terms of Use found on the last page of this document.

- 4. Global Macro Tipping PointsAugust 24th, 2011 STEALTH QE III Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens The content of this slide should not be considered investment advice of any sort, nor should it be used to make investment decisions. Use of this slide is considered to be your explicit acceptance of the Disclosure Statement and the Terms of Use found on the last page of this document.

- 5. Global Macro Tipping PointsAugust 24th, 2011 JULY 27th – FANNIE & FREDDIR ADDED Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens The content of this slide should not be considered investment advice of any sort, nor should it be used to make investment decisions. Use of this slide is considered to be your explicit acceptance of the Disclosure Statement and the Terms of Use found on the last page of this document.

- 6. Global Macro Tipping PointsAugust 24th, 2011 AUGUST 12TH “OPERATIONAL READINESS” STATEMENT Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens The content of this slide should not be considered investment advice of any sort, nor should it be used to make investment decisions. Use of this slide is considered to be your explicit acceptance of the Disclosure Statement and the Terms of Use found on the last page of this document.

- 7. Global Macro Tipping PointsAugust 24th, 2011 STEALTH QE III Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens The content of this slide should not be considered investment advice of any sort, nor should it be used to make investment decisions. Use of this slide is considered to be your explicit acceptance of the Disclosure Statement and the Terms of Use found on the last page of this document.

- 8. Global Macro Tipping PointsAugust 24th, 2011 STEALTH QE III Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens The content of this slide should not be considered investment advice of any sort, nor should it be used to make investment decisions. Use of this slide is considered to be your explicit acceptance of the Disclosure Statement and the Terms of Use found on the last page of this document.

- 9. Global Macro Tipping PointsAugust 24th, 2011 STEALTH QE III Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens The content of this slide should not be considered investment advice of any sort, nor should it be used to make investment decisions. Use of this slide is considered to be your explicit acceptance of the Disclosure Statement and the Terms of Use found on the last page of this document.

- 10. Global Macro Tipping PointsAugust 24th, 2011 STEALTH QE III Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens The content of this slide should not be considered investment advice of any sort, nor should it be used to make investment decisions. Use of this slide is considered to be your explicit acceptance of the Disclosure Statement and the Terms of Use found on the last page of this document.

- 11. DISCLOSURE STATEMENT AND TERMS OF USE THE CONTENT OF THIS SLIDE PRESENTATION AND ITS ACCOMPANYING RECORDED AUDIO DISCUSSION ARE INTENDED FOR EDUCATIONAL PURPOSES ONLY.This slide presentation and its accompanying recorded audio discussion are not a solicitation to trade or invest, and any analysis is the opinion of the author and is not to be used or relied upon as investment advice. Trading and investing can involve substantial risk of loss. Past performance is no guarantee of future returns/results. Commentary is only the opinions of the authors and should not to be used for investment decisions. You must carefully examine the risks associated with investing of any sort and whether investment programs are suitable for you. You should never invest or consider investments without a complete set of disclosure documents, and should consider the risks prior to investing. This slide presentation and its accompanying recorded audio discussion are not in any way a substitution for disclosure. Suitability of investing decisions rests solely with the investor. Your acknowledgement of this Disclosure and Term of Use Statement is a condition of access to it. Furthermore, any investments you may make are your sole responsibility. THERE IS RISK OF LOSS IN TRADING AND INVESTING OF ANY KIND. PAST PERFORMANCE IS NOT INDICATIVE OF FUTURE RESULTS. Listen to the original podcast for this slide at www.GordonTLong.com/UnderTheLens

Notes de l'éditeur

- Though the media is talking about the Fed needing to do something in reaction to falling equity markets – the Fed would make a serious mistake by announcing a QE III. Dollar would collapse, further inflation cost push from imports would result – and not the least would be a likely further drop in the equity markets.What the Fed is concerned about is the 30 Year Bond just fell through the 2010 crisis lowThe 2-10 Year Spread is fast approaching 175 basis points which marked Japan falling into a protracted Deflationary RecessionWe were as low as 185 but this AM are about 25 bps above this threshold that the credit markets are glued toThe 5 & 10 year TIPs have gone negative.Though narrow and broad money supply is expanding significantly – Money Velocity is rolling over.The Fed just can’t get any traction on Money Velocity!The issue is nominal GDP is no where near the 6-7% required and is below 4% with =20% government expenditure.There are a whole range of solutions out there from Kenneth Rogoff to Larry Summers to use Inflation Targeting to help with thisREMEMBER; Since the Fed froze short rates at 25bps until 2013 there has been a made scramble to borrow at 25 and buy the long end of the treasury – this has drive prices up dramatically and yields below 2% on the 10 year.SO what is to be done.The first thing do do is make sure the $1.7T deficit is going to be financed because Japan and China aren’t going to do it.THEY MUST GET THE BANKS TO DO SOMETHING WITH THEIR 1.76T they have on deposit with the FED (What I will refer to as Non Borrowed Reserves – or NBRs)

- Expect the Fed to reduce interest rates on the Reserves to noticably below that of treasury bills.DO NOT EXPECT THE FED TO MAKE ANY KIND OF BIG DEAL ON THIS – IT MUST BE QUIET AND SUBTLE!!!!!!However, it must send a message to those who are expected to take full advantage of what is being made available to them!!!

- As noted in the October 19, 2009, Statement Regarding Reverse Repurchase Agreements, the Federal Reserve Bank of New York has been working internally and with market participants on operational aspects of TRIPARTY reverse repurchase agreements to ensure that this tool will be ready if the Federal Open Market Committee decides it should be used. Beginning Monday, August 15, the New York Fed intends to conduct another series of small-scale reverse repurchase (repo) transactions using ALL ELLIGIBE COLLATERAL TYPES. The first operation will be conducted using only the expanded reverse repo counterparties announced on July 27, 2011. Subsequent operations in this series will be open to all eligible reverse repo counterparties.Going forward, the Federal Reserve plans to conduct a series of small-scale reverse repurchase transactions about every two months, which will bring the frequency of these operational exercises in line with that of the Term Deposit Facility exercises.Like the earlier operational readiness exercises, this work is a matter of prudent advance planning by the Federal Reserve. The operations have been designed to have no material impact on the availability of reserves or on market rates. Specifically, the aggregate amount of outstanding reverse repo transactions will be very small relative to the level of excess reserves, and the transactions will be conducted at current market rates. These operations do not represent a change in the stance of monetary policy, and no inference should be drawn about the timing of any change in the stance of monetary policy in the future.The results of these operations will be posted on the public website of the Federal Reserve Bank of New York, together with the results for other temporary open market operations. The outstanding amounts of reverse repos are reported as a factor absorbing reserves in Table 1 in the Federal Reserve's H.4.1 statistical release and as liability items in Tables 8 and 9 of that release.