Understanding SAR (Suspicious Activity Reporting)

•

1 j'aime•583 vues

To successfully identify the parties involved in any suspicious activity or money laundering/fraud processes, timely identification and reporting of the same is crucial. The Financial Crimes Enforcement Network (‘FinCEN’) has instituted various changes and updates to the requirements to enhance the process. We will take a look at SAR requirements and challenges for financial institutions and focus on the solutions that can be enacted to stay compliant.

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

Similaire à Understanding SAR (Suspicious Activity Reporting)

Similaire à Understanding SAR (Suspicious Activity Reporting) (20)

Plus de HEXANIKA

Plus de HEXANIKA (15)

Dernier

Dernier (20)

Understanding SAR (Suspicious Activity Reporting)

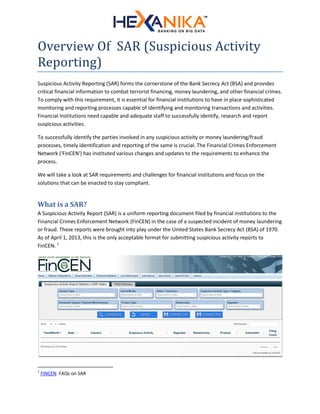

- 1. Overview Of SAR (Suspicious Activity Reporting) Suspicious Activity Reporting (SAR) forms the cornerstone of the Bank Secrecy Act (BSA) and provides critical financial information to combat terrorist financing, money laundering, and other financial crimes. To comply with this requirement, it is essential for financial institutions to have in place sophisticated monitoring and reporting processes capable of identifying and monitoring transactions and activities. Financial Institutions need capable and adequate staff to successfully identify, research and report suspicious activities. To successfully identify the parties involved in any suspicious activity or money laundering/fraud processes, timely identification and reporting of the same is crucial. The Financial Crimes Enforcement Network ('FinCEN') has instituted various changes and updates to the requirements to enhance the process. We will take a look at SAR requirements and challenges for financial institutions and focus on the solutions that can be enacted to stay compliant. What is a SAR? A Suspicious Activity Report (SAR) is a uniform reporting document filed by financial institutions to the Financial Crimes Enforcement Network (FinCEN) in the case of a suspected incident of money laundering or fraud. These reports were brought into play under the United States Bank Secrecy Act (BSA) of 1970. As of April 1, 2013, this is the only acceptable format for submitting suspicious activity reports to FinCEN. 1 1 FINCEN: FAQs on SAR

- 2. Screenshot of FINCEN SAR Report Generator A SAR must be filed within 30 days after the date of initial detection of the suspicious activity. Financial institutions are required to keep a copy of the SAR and the original business record of any supporting documentation for five years. Federal law requires that financial institution and its directors, officers, employees and agents who report suspected activities or known violations are strictly banned from disclosing any information to the person involved in the transaction about that transaction being reported.2 A transaction includes a deposit; a withdrawal; a transfer between accounts; an exchange of currency; an extension of credit; a purchase or sale of any stock, bond, certificate of deposit, or other monetary instrument or investment security; or any other payment, transfer, or delivery by, though, or to a bank. Since February 24, 2012, the FinCEN regulatory body made extensions and exemptions to allow FinCEN reports to be filed electronically. This step was taken in an effort to improve efficiency, reduce government and industry costs, and enhance the ability of investigators, analysts, and examiners to gain better and timely access to important financial information.3 Challenges for SAR Financial institutions and their employees face civil and criminal penalties for failing to properly file suspicious activity reports, including large fines or added regulatory restrictions. Total monetary settlements levied for money laundering, sanctions and tax evasion by the regulators and law enforcement agencies surpassed $13.4 billion for the year 2014. Four international banks paid U.S. authorities more than $300 million each, with some paying out significantly more.4 Suspicious activity monitoring and reporting are critical internal controls, which require enhanced systems to ensure proper surveillance (automation), transaction identification and matching, or a combination of these. Banks should also employ sufficient resources keeping in mind their overall risk profile and transaction volume. Meticulous Identification and Monitoring Requirements A transaction monitoring system typically targets specific types of transactions, prominently those targeting large amounts of cash and/or those from foreign geographies, and includes a manual review of various reports in order to identify unusual activities. These include currency activity reports, funds transfers reports, monetary instrument sales reports, significant balance change reports, ATM transaction reports, nonsufficient funds (NFS) reports and more. The process involves review of daily reports or reports that cover a particular timespan or a combination of both. This creates various challenges: 2 TechTarget: Suspicious Activity Report (SAR) 3 FinCEN: FinCEN Reports Going Paperless 4 Kaufmann Rossin: Regulators Issued Fewer AML Fines in 2014, But Packed a Bigger Punch

- 3. 1. Handling large data volumes: Most legacy systems are incapable of analysis and storage of large data volumes. 2. Updates to identification rules: Banks deploy a certain set of filters or rules to help identify certain behavior that it deems ‘suspicious’. As the definition of "suspicious" keeps being updated, the process of updating the system with new rules can be time consuming and complex. 3. Innumerable data sources: For creation of reports, the system refers to data from disparate sources, requiring frequent backtracking and cross checking. When dealing with large quantities of data, data lineage and linkage issues might crop up, eventually leading to the next challenge. 4. Data Accuracy: Reviewers need to constantly crosscheck the data source and match the data fetched in reports to ensure that the data is accurate. As SAR requires suspicious activities to be reported within a particular timeframe, ensuring data quality becomes even more critical. 5. Frequent Report Generation and Updating: Although FinCEN has provided sufficient streamlining in the reporting format requirement, bank generated reports need to be update from time to time to remain up to date. The Components for SAR Compliance The five key components to an effective monitoring and reporting system are: 1. Identification or alert of unusual activity (which may include: employee identification, law enforcement inquiries, other referrals, and transaction and surveillance monitoring system output). 2. Managing alerts. 3. SAR decision making. 4. SAR completion and filing. 5. Monitoring and SAR filing on continuing activity. These components are present in banks of all sizes. However, the structure and formality of the components may vary. Larger banks will typically have greater differentiation and distinction between functions, and may devote entire departments to the completion of each component. Smaller banks may use one or more employees to complete several tasks (e.g., review of monitoring reports, research activity, and completion of the actual SAR).5 Hexanika: Innovation via Automation Hexanika is a FinTech Big Data software company, which has developed an end to end solution for financial institutions to address data sourcing and reporting challenges for regulatory compliance. The challenges of SAR for financial institutions are to implement sophisticated mechanisms required to identify suspicious transactions and activities and generate proper reports in a timely and concise 5 FFIEC: Suspicious Activity Reporting—Overview

- 4. manner. Hexanika helps establish a compliance platform that streamlines the process of data integration, analytics and reporting. Our software platform can develop and clean data to be sourced for reporting and automation, simplifying the processes of data governance and generating timely and accurate reports to be submitted to regulators in the correct formats. To know more about our products and solutions, read: http://hexanika.com/company-profile/ Contact Us USA 249 East 48 Street, New York, NY 10017 Tel: +1 646.733.6636 INDIA Krupa Bungalow 1187/10, Shivaji Nagar, Pune 411005 Tel: +91 9850686861 Email: info@hexanika.com Follow Us