EAI Checklist

•

0 j'aime•551 vues

Checklist created for EAI illustrating Backoffice, Compliance, Anti-money Laundering and Commission topics.

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (15)

Similaire à EAI Checklist

Similaire à EAI Checklist (20)

Plus de Ideba

Plus de Ideba (20)

Dernier

Dernier (20)

EAI Checklist

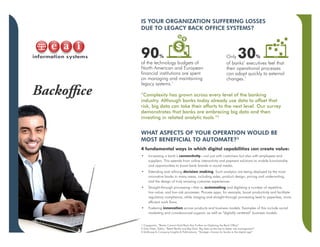

- 1. Backoffice IS YOUR ORGANIZATION SUFFERING LOSSES DUE TO LEGACY BACK OFFICE SYSTEMS? WHAT ASPECTS OF YOUR OPERATION WOULD BE MOST BENEFICIAL TO AUTOMATE?3 4 fundamental ways in which digital capabilities can create value: • Increasing a bank’s connectivity—not just with customers but also with employees and suppliers. This extends from online interactivity and payment solutions to mobile functionality and opportunities to boost bank brands in social media. • Extending and refining decision making. Such analytics are being deployed by the most innovative banks in many areas, including sales, product design, pricing and underwriting, and the design of truly amazing customer experiences. • Straight-through processing—that is, automating and digitizing a number of repetitive, low-value, and low-risk processes. Process apps, for example, boost productivity and facilitate regulatory compliance, while imaging and straight-through processing lead to paperless, more efficient work flows. • Fostering innovation across products and business models. Examples of this include social marketing and crowdsourced support, as well as “digitally centered” business models. 90% of the technology budgets of North American and European financial institutions are spent on managing and maintaining legacy systems.1 Only 30% of banks’ executives feel that their operational processes can adapt quickly to external changes.1 “Complexity has grown across every level of the banking industry. Although banks today already use data to offset that risk, big data can take their efforts to the next level. Our survey demonstrates that banks are embracing big data and then investing in related analytic tools.”2 1 Capgemini, “Banks Cannot Hold Back Any Further on Digitizing the Back Office” 2 Erika Klein, Editor, “Retail Banks and Big Data: Big data as the key to better risk management” 3 McKinsey & Company Insights & Publications, “Strategic choices for banks in the digital age”

- 2. Compliance IS YOUR COMPLIANCE DATA SUFFICIENTLY ACCURATE AND COMPREHENSIVE? 51% of banking executives cite insufficient data as greatest obstacle to better risk management.1 Only 42% of banks have faith that they have the right big data tools to integrate structured and unstructured data.1 TOP REGULATORY COMPLIANCE CONCERNS IN FINANCIAL SERVICES3 • USA Patriot Act Anti-money laundering and provisions to detect and prevent financing of terrorism • Comprehensive Capital Analysis and Review (CCAR) Federal Reserve assessment of adequate capitalization • Financial Industry Regulatory Authority (FINRA) Multiple rules to ensure transparency • Consumer Financial Protection Bureau (CFPB) Part of Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 • Office of the Comptroller of Currency (OCC) Regulations for national banks, federally chartered savings associations, federal branches of foreign banks, and institution-affiliated parties 1 The Economist Intelligence Unit, “Retail Banks and Big Data: Big data as the key to better risk management,” 2014 2 Becca Lipman, “Where Are We Now? The Era of Trade Surveillance Automation,” Information Week WallStreet & Technology, June 13, 2004 3 Robert Half Management Resources, “5 Top Regulatory Compliance Concerns in Financial Services,” April 15, 2015 “...when you look at the ultimate intelligent trading compliance approach, it is going to be able monitor, store, and retrieve trade data, order data, and market data, as well as all relevant communications from all the disparate systems, both internally and externally, and then match these things appropriately.”2

- 3. Anti-Money Laundering ARE YOU CONFIDENT THAT YOU ARE MEETING ALL ANTI-MONEY LAUNDERING REQUIREMENTS? “…the superintendent of the New York Department of Financial Services, Benjamin Lawsky, announced recently that his agency is about to propose a requirement that senior banking executives personally ‘sign off’ on the ‘adequacy and robustness’ of the anti-money laundering (AML) compliance programs that their firms use to spot suspicious customer financial transactions. This requirement would represent a major escalation of pressure on firms to prevent the types of serious financial crimes and abuses that have recently received significant attention.”1 – Robert Appleton, Partner, Day Pitney LLP, former Supervisory Assistant U.S. Attorney AN EFFECTIVE ANTI-MONEY LAUNDERING PROGRAM MUST BE ROBUST AND COMMENSURATE WITH THE SIZE AND COMPLEXITY OF THE INSTITUTION2 An effective program requires: • Ongoing and updated training on BSA/AML and sanctions compliance for all employees tailored to their specific roles. • The roles and responsibilities of each employee and the compliance departments clearly defined and communicated. • Electronic monitoring integrated, constantly updated with client information, and supervised by trained staff. • Periodic independent testing and reviews of the compliance regime and its effectiveness. • Performing and updating detailed customer due diligence for our increasingly mobile and complex financial system. 1 Law 360, “Anti-Money Laundering Compliance is About to Get Personal,” March 10, 2015 2 Financier Worldwide, “Risk, Governance & Compliance for Financial Institutions in 2015”

- 4. Commissions CAN MANUAL PROCESSES PROVIDE THE EFFICIENCY, VISIBILITY AND PREDICTABILITY YOU NEED? “For any given transaction, there are a number of factors that impact the calculation of payouts, including the rep and what he/she is paid, the product type, how the deal is executed, the cost per ticket, the client, and so on... Using software to automate these functions has kept the accounting processes from becoming prohibitively labor intensive.”1 “From a management standpoint, keeping up with the details of so many producers’ activities becomes an equally challenging and tedious task. Using the software, on any given day … management can see where the company stands in relation to revenues, payouts, and what its brokers are doing.”1 “Firms are seeking platforms that can track complex and/or non-revenue compensation metrics. Firms are integrating platforms across units to support the holistic client experience.” Ernst & Young, “Financial advisor compensation: the changing approach to advisor incentives,” 2014 1 Robert A. Bonelli, President and CEO Northeast Securities, Inc., “Managing Complex Sales Compensation Plans,” The Entrepreneur’s Resource