Are all so rs created equal how sors hunt dark liquidity

•

0 j'aime•325 vues

Smart Order Routing

Recommandé

Contenu connexe

Dernier

Dernier (20)

En vedette

En vedette (20)

Are all so rs created equal how sors hunt dark liquidity

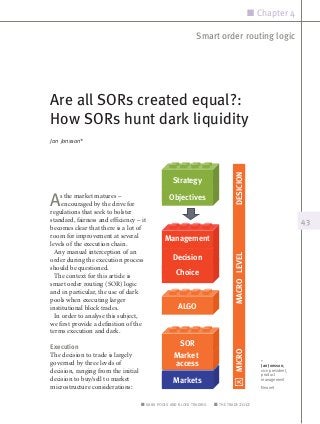

- 1. n Chapter 4 Smart order routing logic Are all SORs created equal?: How SORs hunt dark liquidity Jan Jonsson* DESICION Strategy A s the market matures – encouraged by the drive for regulations that seek to bolster Objectives standard, fairness and efficiency – it 43 becomes clear that there is a lot of room for improvement at several Management levels of the execution chain. Any manual interception of an MACRO LEVEL order during the execution process Decision should be questioned. The context for this article is Choice smart order routing (SOR) logic and in particular, the use of dark pools when executing larger institutional block trades. ALGO In order to analyse this subject, we first provide a definition of the terms execution and dark. Execution SOR MICRO The decision to trade is largely Market governed by three levels of DMA access * Jan Jonsson, decision, ranging from the initial vice president, product decision to buy/sell to market Markets management microstructure considerations: Neonet n dark pools and block trading n the trade 2012

- 2. n Chapter 4 Smart order routing logic Decision (Portfolio/Fund manager) Grey pools The strategic decision made by (Broker crossing networks) a portfolio manager to move Investors are most likely willing to in to or out of a position leads pay a premium price to complete to macro level instructions of the order at once with no risk-in- what instruments to buy/sell, time or price impact. Some dark quantities, etc. pools match on order price and volume limits only without using a Macro Level (Trader, Algorithm) reference price such as the primary The large order is then divided mid/bid/ask used by dark MTFs. into smaller, more manageable However, these are not parts using a certain algorithm that transparent, and harder to reflects the desired strategy. Each benchmark – you need to trust smaller part is then transmitted to the provider is not seeking to the micro level of execution. profit from both commission and spreads. These venues are often Micro Level (SOR, Market access) referred to as ‘grey pools’ and may 44 The micro level focuses on the face problems in the future as optimal execution strategy for each regulators show increasing interest individual slice of the larger order in tightening the regulation of these in the best possible way using all venues. Fair, equal, and predictable available markets and execution behavior is on top of the agenda channels. today – pushing for more automation and standardisation. Dark multilateral trading facilities How SORs hunt dark liquidity Dark multilateral trading facilities Dark is used differently at the (MTFs) are matching engines micro level compared to the that don’t display any pre-trade macro level and it is important to information of resting orders to optimise the use of dark in both anyone and are regulated under channels. However, a common MiFID with equal access and mistake is to focus on only one part rules for everyone. To ensure a of the full chain as we will describe fair price discovery mechanism, later on. dark pools base their execution prices on the primary exchanges’ The use of dark pools at macro mid, bid or ask price. Execution level (Algorithmic execution) is transparent and easy to As described, executing a large benchmark. block order typically involves n dark pools and block trading n the trade 2012

- 3. n Chapter 4 Smart order routing logic dividing it into smaller parts another type of dark execution – (slices) that are executed over one which attempts to save half a a period of time, for instance spread in a mid-point dark pool through using an algorithm. before hitting the lit markets – is Only a small portion of the total used. order (one slice) is active in the lit The spread in Europe is market, while the bulk of the order somewhere between five and 20 ‘rests’ in the algorithm. bps, so this equals savings between This is where dark in its first form 2.5 bps to 10 bps compared to enters the scene. losing the entire spread by being At the macro level, dark is a term aggressive. We can trade at the for the part of an order a broker mid price to save spread, but bid/ executes by trying to find a match ask price points are also interesting, for the order among its customer since there may be more volume base, without causing market available at the offer price in the impact. dark compared to lit. This enables The hunt for efficiency, investors to beat the weighted combined with the trend towards EBBO (European best bid and 45 standardised, transparent and offer when volume is taken into equal treatment of customers via account). new regulations, has led to an automation of this process through Are all SOR created equal? the use of electronically operated As expected, routers comes in dark pools. various shapes and sizes and are The part of the order that is not different based on a number of traded in the lit market is usually factors: allowed to sweep a number of dark pools, carefully selected to avoid The creator/owner unwanted information leakage and Some routers are created by in conjunction with anti-gaming the buy side for their own use, strategies. but more commonly a SOR is provided by the sell-side for its The use of dark pools at the customers, internal prop flow micro level (SOR) or a combination of the two. When the algorithm is executing SORs are also offered by agency slices that are considerably smaller brokers that serve many sell- than the big chunk at the macro and buy-side customers that level, it may decide to send an have different needs. There are aggressive order to the SOR. Here also technology providers that n dark pools and block trading n the trade 2012

- 4. n Chapter 4 Smart order routing logic sell standard products or offer Vertical integration routing customisation. Depending Does the SOR provider control on the provider, the SOR will reference data, gateways to market, have different objectives and market data, network and the functionality. full chain up to the SOR level, or do they only focus on the The SOR maturity development of the SOR? This is An early-generation SOR will critical to the provider’s control be more blunt and static. Later and understanding of the whole versions tend to be more dynamic process. and comprehensive, cleverly combining lit and dark volumes Business/price model as well as preventing gaming The result and focus of attempts. This development never management and the entire ends, not even with advanced organisation will be widely mathematical chaos theories different if the SOR provider makes predicting cause and effect. money on consulting hours, basis 46 point commission on flow they get Degree of specialisation for providing research, or ideally Is execution the key consideration if they are paid for the actual that the SOR provider focuses on, benchmarked performance of their or is it just an enabler of another execution. business? At a specialised firm, Depending on the model chosen, even top management will be the focus may turn to lower involved in the design and quality internal costs – internalising of a router and frequently monitor flow (to make money on scale SOR benchmarks. and possibly make money on spreads), or hopefully a transparent Scale good execution that is well Both an increase in, and benchmarked. diversification of, flow will speed A commission model may create up the learning curve for SOR a principal versus agency problem providers. It will also provide a where a customer wants best larger set of data to analyse in order execution at the cheapest cost and to further develop and optimise the the provider has to lower cost to SOR logic. get a decent margin. Since cost is easy to measure and quality is hard, n dark pools and block trading n the trade 2012

- 5. n Chapter 4 Smart order routing logic a cost focus is common, which is essential to know who you are compromises execution quality. trading with, and their execution Full transparency would require the intentions. The important thing SOR provider to report the actual is to make a well-informed cost of routing to each customer decision with the least amount plus a totally visible margin. of tradeoffs possible. Dark pools are rapidly increasing in Benchmark numbers as institutions fight to The selection of a benchmark keep internalising flow despite has the same dramatic impact as impending regulations. At the business model. At a micro level, same time, huge orders face have a the focus is around beating the harder time in finding each other. EBBO, offering price improvement Pegging executions at the mid/ and spread capture. At the macro bid/ask is an easy, well working level, benchmarks usually include mechanism; but an opportunity implementation shortfall, VWAP, to trade is missed since big and other market impact measures. investors are likely willing to pay One extremely important aspect a premium price if more volume 47 is the criteria needed to include can be done at once. But no one or exclude venues in different has yet managed to implement benchmarks. this with trust, transparency and efficiency. As pure agency brokers, Summary we are waiting for ‘the pure and We have explained that all SORs transparent agency large in scale are certainly not created equal order matching’ – that would bring and the underlying factors that down the cost for execution to a contribute to their differences. It fraction of today. n n dark pools and block trading n the trade 2012