Internal Procurement Audit

This document discusses strategies for auditing procurement processes in the oil and gas industry. It outlines the importance of procurement for acquiring necessary capital goods and materials, as well as the high risks of collusion and corruption. The summary provides: 1) Internal auditors must understand an organization's culture, relationships, and strategies to identify corruption risks in procurement. This includes identifying any "cartels" manipulating the process. 2) A "firewall" defense strategy is recommended to prevent fraud, such as rejecting questionable procurements and substantively testing bidding processes. 3) Continuous review of payments against procurement documents can also limit irregularities, upholding the internal auditor's role in ensuring integrity.

Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

En vedette (15)

Similaire à Internal Procurement Audit

Similaire à Internal Procurement Audit (20)

Dernier

Dernier (20)

Internal Procurement Audit

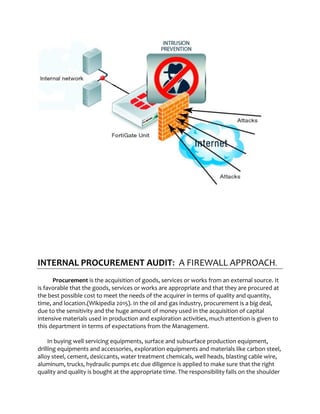

- 1. INTERNAL PROCUREMENT AUDIT: A FIREWALL APPROACH. Procurement is the acquisition of goods, services or works from an external source. It is favorable that the goods, services or works are appropriate and that they are procured at the best possible cost to meet the needs of the acquirer in terms of quality and quantity, time, and location.(Wikipedia 2015). In the oil and gas industry, procurement is a big deal, due to the sensitivity and the huge amount of money used in the acquisition of capital intensive materials used in production and exploration activities, much attention is given to this department in terms of expectations from the Management. In buying well servicing equipments, surface and subsurface production equipment, drilling equipments and accessories, exploration equipments and materials like carbon steel, alloy steel, cement, desiccants, water treatment chemicals, well heads, blasting cable wire, aluminum, trucks, hydraulic pumps etc due diligence is applied to make sure that the right quality and quality is bought at the appropriate time. The responsibility falls on the shoulder

- 2. of the Internal audit to monitor, supervise the procurement through its stages and to make sure that the company gets the value for every dollar spent on the procurement of these materials by certifying the appropriateness of the items bought in quality ,quantity and timing. The job is not as easy as it seems. Procurement is a high risk area which harbors the greatest collusions and contractual cartels in any organization, especially in the oil and gas industry. The internal auditor has to understand the terrain, the sociology and the psychology of people in the organization in order to make an impact in limiting the rate of financial losses inherent in procurement processes. Any attempt to use a haphazard approach in procurement can lead to risk of life, risk of the job itself and risk of personal relationship with your colleagues in other departments of the Organization you work with. Therefore, you must understand the following concepts with respect to your Organization 1. The Corporate Culture of the Organization 2. The underlying relationships, if any, between members of your internal audit team and personnel of the Procurement department, this is necessary for information security. 3. Identify the strategies employed by the Procurement officers, managers to get undue economic advantages with respect to contracts and Procurements. 4. Is there existence of a Cartel, responsible for that? Identify the individuals and their powers within the Organization. 5. Apply the Firewall defense strategy to stop them.

- 3. THE CORPORATE CULTURE: The vision, mission of the organization, the ethical orientation and how friendly or strict the work environment is, is very paramount. I cannot overemphasize the importance of the reward and punishment approach of the Organization. The existing technology i.e the software ERP packages used by the Organization is key as it determines how those procurements are made, online or normal procurements. The Companies policies on procurement, its approved vendors, preferred vendors and why they are preferred and all you need to know about the company that is vital to the course. UNDERLYING RELATIONSHIPS: This is very vital especially for a newly employed internal Auditor sent on assignment to monitor procurements. It is important to be very smart, you have to find someone to attach to, who knows the terrain well as you carefully watch what he does and how he goes about it. You are not supposed to divulge every information you have to the team or blatantly say your opinion. You have to think like the Mafia and act like a lamb, but always remember to ask too many questions; it will get you somewhere…It will help you understand the personal relationship between the members of your team and the entire organization.

- 4. IDENTIFY THE STRATEGIES USED BY THE PROCUREMENT DEPARTMENT: The Procurement Managers know the game, the game has a goal, the goal is manipulating and masterminding procurement processes so economic benefits will flow into the private pockets of a particular staff or group of staff (cartel) who are aware and stimulate the process at the detriment of the Company. How does it work? They have their preferred vendors, they do their bargain, they have someone in Accounts of finance responsible for the disbursement of cash preferably the Accounts Payable Line Manager in the Organization and another corrupt big boss who understands the system and regularly collects his share when a deal is sealed, this makes a perfect team. As an Internal Auditor, two activities should be on your mind: The Procurement and the disbursement (Payment) for the procured goods. Let’s look at the risk areas in Procurement and things that must certainly go wrong for the Auditor to know they are on rampage 1. Purchase order may be incorrect 2. Unauthorized purchases may be made 3. Abuse of purchasing system, some staffs may order things for personal use. 4. Duplicate payments may be made 5. Inadequate division of responsibilities between purchasing, receiving and payment. 6. Purchasing may not meet companies need in quality and quantity. 7. Frequent unusual demands from some user departments of goods. 8. Goods may not be accounted for on timely basis. 9. Adjustments on vendor accounts may not be properly authorized. 10. Inflated quotations Once you get these red flags, next step is to search for your verifiable evidence. You do that using the following documents: (1)Purchase order (2) Purchase manual (3) Vendor List (4)Purchase file (5) Receiving document (6)Request for price quotation (7)Request for Proposal (8)Advertisement and solicitations (9) Vendor Proposals (10)Vendor Catalogue (11) History File (12)Adjustments and write-offs (13)Procurement file totals.

- 5. IDENTIFY THE CARTEL: Once you have this evidence at your disposal and you are trying to monitor or find out what transpired in a particular transaction, it will automatically lead you to the Cartels. Here is it. You have to start moving round strategically, asking some salient questions on this particular transaction you are monitoring and naturally you will receive replies, some annoying ones, some evasive ones, some implicating ones. Once there is divergence and incoherence in answers that are supposed to be uniform the truth will begin to surface, at this stage you will know exactly who the cartels are, though not all involved will want to talk to you or respond in a way to drag them to the dance floor. But one lesson learned, now you know the Cartel and who they are, if you move further you may receive a call from a colleague or the Head of your Department telling you to retreat, this means that a big boss is in the game. FIREWALL DEFENSE STRATEGY Having known who you are up against, it becomes a little bit easy to face them squarely, not in an attack minded manner, but defense of the Companies resources. Let’s look at what Cartels and procurement personnel do to gain undue economic benefit from Procurements and Contracts.

- 6. 1. Bribes and Kickbacks 2. Collusive bidding 3. Change order abuse 4. Co mingling of contracts 5. Excluding qualified bidders 6. False, inflated, duplicate invoices. 7. False statements and claims 8. Hind –Bargaining with vendors 9. Leaking of bid information 10. Manipulation of bids 11. Rigged specification 12. Purchases for personal use 13. Split purchases 14. Unbalanced bidding etc. Firewall defense strategy in Procurement Audit is a strategy that has been designed to work like the computer software firewall” to prevent the frauds of every manner against the company from yielding expected fruits as planned by its perpetrators. The Internal Audit department can implement Firewall approach in Procurement by getting a grip of two vital departments in the Organization: The Procurements and the Accounts Payable. All payments for procurements must pass through the internal audit for approval, therefore the Internal Audit should simply reject any procurement transaction that is questionable or that exhibit any trait of questionability in relevance, purpose and specification. It is a common sense game; just say NO, we are constrained to authorize this procurement that is the firewall approach. Then, immediately begin substantive testing on the bidding process, desired qualification of bidders; ask questions on the rationale behind the selection of a particular vendor. If the job has been done and you are called upon to investigate, then do these: 1. Compare purchase orders with vendor catalogues, if there are significant variances, it should be investigated. 2. Sort payment file by vendor amount and number 3. Probe for favored vendors, accumulate and rank frequency of vendor order. 4. Validate adequate segregation of duties 5. Check compliance to procedures, check the particular requestor has authorization to order for the product. 6. Check the vendor invoice for clerical accuracy, proper dates, and appropriateness of purchase. 7. Do your purchase needs audit and close the case.

- 7. If the particular transaction passes these tests, it’s a good deal you move for approval. It looks rigorous but an auditor can be smart too, get it done in minutes and keep the work moving especially if we are using software to help. The next stronghold is the Accounts payable; the department must have the stipulated criteria for a procurement to pass before it is verified for payments. Since the internal; auditor cannot sit permanently with the accounts payable officer to monitor all payments made with respect to procurements, the best approach is to do a weekly review of payments made with respect to procurement, review prices and all that need to be reviewed. Asking relevant questions that will unveil any attempted financial irregularity perpetrated by interested parties. By sticking to the above guidelines, you are not been difficult, but are just doing the job you are paid for. You have be civil but brave, technical and smart and mostly remember as a regulator, you are adjudged to be incorruptible per se, if you loosen up your belt, they will hang you in the gallows. This is Internal Audit and Integrity is the key, once lost is irrecoverable. Thanks Egege Justice +2348065122244 Lekki,Lagos Nigeria.