Recommandé

Contenu connexe

Similaire à The Economic Forecasts - The Coming Hyper-Inflation Apocalypse

Similaire à The Economic Forecasts - The Coming Hyper-Inflation Apocalypse (18)

Dernier

Dernier (20)

The Economic Forecasts - The Coming Hyper-Inflation Apocalypse

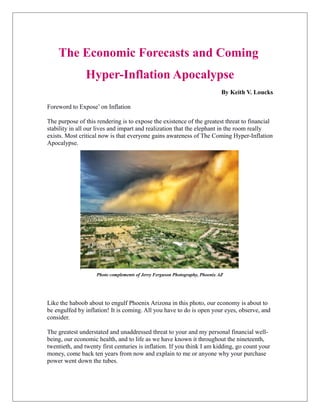

- 1. The Economic Forecasts and Coming Hyper-Inflation Apocalypse By Keith V. Loucks Foreword to Expose’ on Inflation The purpose of this rendering is to expose the existence of the greatest threat to financial stability in all our lives and impart and realization that the elephant in the room really exists. Most critical now is that everyone gains awareness of The Coming Hyper-Inflation Apocalypse. Photo complements of Jerry Ferguson Photography, Phoenix AZ Like the haboob about to engulf Phoenix Arizona in this photo, our economy is about to be engulfed by inflation! It is coming. All you have to do is open your eyes, observe, and consider. The greatest understated and unaddressed threat to your and my personal financial well- being, our economic health, and to life as we have known it throughout the nineteenth, twentieth, and twenty first centuries is inflation. If you think I am kidding, go count your money, come back ten years from now and explain to me or anyone why your purchase power went down the tubes. The Coming Hyper-Inflation

- 2. There is indisputable proof, yes evidence that inflation is planned by the “powers that be”. Why is the Washington establishment giving lip service to how bad defecate spending is and yet are making little attempt to stem the free flow of the force fed cash injection in to the economy? Why are the lawmakers and administration spending trillions of dollars with little or no concern about the size of the defeatist? If you have not been aware of this situation, now you have been enlightened. Now, stay tuned here. An explanation is provided in this eBook “The Coming Hyper-Inflation Apocalypse”. This logical explanation is presented now so all can see what is happening behind the blinds in the Capitol City metaphorical smoky backrooms. The practical definition of inflation is “more money chasing the same amount of goods and services”. Think about it. In a closed economic cell where there are no additional goods and no additional funds to increase the price of those goods, equilibrium in price is reached. By introducing more money into that closed cell, the price of the goods rise as there is more money to apply to the purchase of goods and services. That is inflation. Do you have the picture yet? How many times has the FED printed money to bolster the overdraft spending of the Federal Government? Understand the FED (US Federal Reserve Bank) is internationally owned and not US. It is a privately owned corporation not “Federal” and not a government agency. The FED has no reserves and is not a bank. The US Congress simply authorizes the FED to provide influx of funds that are pumped into the economy to cover deficit spending. It obligates us the citizens to pay the huge debts for funds they advance into our economy. If you are a person who believes in written Biblical scripture, then, know “The borrower is the slave to the lender”. Each of us need to determine how and what action we necessarily need to take to counteract the scourge of inflation. The action your friend or neighbor may take may or may not be the correct action for you to take. Do you want to store gold, gems, hoard food, stockpile guns, or ammo? Do you want to be debt free with a fat savings account? Do you need to rent or own your abode? Are you better off to have that dwelling paid off or financed to the hilt? Surprisingly, being fully paid off may or may not be the correct financial position for you to take. Now that you are aware that a problem is looming, you must act. If you believe that the coming apocalypse is real, you will be compelled to act. Now is a good time for you to address some of these questions. As time goes on, answers and undeclared viewpoints are being offered here to assist you in deciding your best avenue of action, your plan of attack. You do have one, don’t you? Is gold better to possess than real estate? Is being debt free better than having little or no equity? If so, what debt to value ratio is optimal? Should I allow someone to hold my gold in trust or have it in my own hot little hand? Are equities and annuities a consideration or is my financial value under threat? What percentage of my assets should I commit to my economic defense? 2

- 3. There are many questions. There are many combinations of answers. Not all is right for every one person and if a broker/dealer is pushing a product or item, consider if the benefit to you outweighs the benefit of fees and commissions collected by the broker/dealer. A case will be presented at the end of “The Coming Hyper-Inflation Apocalypse” as to why you should not be concerned about any of these matters. Many believe their destiny is predetermined and so to be concerned with maters such as these is an exercise of futility. The eBook, “The Coming Hyper-Inflation Apocalypse” will address these questions and concepts in depth. Most critical currently is that everyone, all become aware of The Coming Hyper-Inflation Apocalypse. If you believe the scenarios therein are correct, tell your friends about this eBook. If you believe the ideas are incorrect and a waste of time, tell your enemies. Tell everyone you know and those who do not! Table of Contents 1. Chapter 1 Knowing The Basics May Save Your Bacon. 2. Chapter 2 What Should I Use For A Hedge? a. Option # 1, Precious Metals. b. Option # 2, Real Estate. c. Option # 3, Gemstones. d. Option # 4, Stocks. e. Option # 5, Bonds. f. Option # 6, Bank CD's and Savings. g. Option # 7, Annuities. h. Option # 8, Foreign Currency. i. Option # 9, Collectables. j. Option # 10, Armaments and Ammunition. k. Option # 11, Tools and Skills. 3. Chapter 3 How Do I Counter The Coming Disaster You Ask? 4. Chapter 4 Is Real Estate A Special Consideration? 5. Chapter 5 To What Purpose? Purpose of protecting against hyperinflation 6. Chapter 6 Do You Need Further Proof? 3

- 4. The Coming Hyper-Inflation Apocalypse Chapter 1 Knowing The Basics May Save Your Bacon. You should commend yourself for taking the first steps to preserving your estate, assets, and valuables. At some time in the future, having made that move will be looked back upon as one of the best finical moves you ever made. Understand, we are not talking of hording assets. Hording should not be the goal, but the preservation of your purchasing power should be by positioning of assets appropriately. Now is the time to expand your understanding of and study the coming hyperinflation, the financial apocalypse that will manifest its self in ways we could never imagine. Look at the cost of medical care. Not only has cost of your local doctor increased, just go to the local hospital for serious illness. You will see or likely already have observed a huge increase in prices. This not only comes from the increase of technology but, form the cost of new, better, and more efficient state of the art equipment and facilities. Have you received your medical insurance premium increase yet? All this to say that, these increase in expenses are simply symptoms of the problem, hyperinflation, a coming era in lives, which will be affected by the increased cost of manufacturing, education and training, and building facility costs. Now that you recognize the symptoms in one industry, you can predict and plan for the coming catastrophic financial and economic collapse. I wish here not to be a doomsayer but consider myself a forecaster willing to speak out saying, “the King has no clothes”. There are many definitions of inflation. Inflation is the growing or swelling of an idea, concept or object. For our purposes, we are going to address inflation as it relates to your money and welfare. Why should you care? Guaranteed if you don’t, you will become the victim of the “Greatest Wealth Transfer In History”. The definition of inflation we address here: “More money applied to purchasing the same amount of goods and/or services.” As a simplified example, if in a closed society, there are only ten loaves of bread for sale and there are no other sources for bread available, and if there are only ten dollars available in this closed society to buy that bread, a loaf should be worth one dollar each. New wrinkle, for whatever reason, ten additional dollars are now introduced into our closed society but there still has been no additional loaves of bread created. All other things being equal, the cost of the bread has now doubled to two dollars per loaf. Another way to say it is, I have more money now so, I am willing to pay twice as much for a loaf of bread. That is inflation. 4

- 5. In real life over the last ten to twenty years, how much has the price of that loaf you purchase increased. It is not thirty-three cents per loaf any more as it was in 1994. If you had thirty-three cents in 1994, according to the CPI calculator it would take fifty- two cents to buy the same item as in 2014. Come on now. If you believe that, I know a man selling swampland in the south, a man selling a bridge in Brooklyn, and a government touting the Consumer Price Index legitimacy. Can you really buy a thirty- three cent loaf of bread for fifty-two cents these days? More like two dollars and fifty- two cents wouldn’t you think? Now, why should you or I care? What is a few measly dollars for a loaf of bread? Well, let us draw a picture. Let us apply this concept to bigger ticket items like, say, the average home price in 1994 of $154,500 as compared to the average home price in 2010 of $272,900.1 The CPI shows the inflated value for that period should only be $227,326. Surprise, understated by $45,574, do you suppose the CPI computations understate the real rate of inflation all around? When I first became involved in the financial planning industry in the early nineteen seventies, the CPI included the cost of petroleum products in the computations of inflation. Shortly after in the late seventies, petroleum related product values were removed from the measure of inflation. Just think, what in our modern lives is not touched and affected by its relationship to the cost of petroleum? Without the influence of the obvious, gasoline, heating oil, goods, transportation, building materials, packaging, medicines, clothing, automobiles, and others, the CPI rate was trimmed in a major way so real inflation was not shown. Had they left the influence of petroleum in the mix, inflation would have measured beyond terrifying levels. What is real? Not the CPI as presented and we now recognize it. Did you buy a steak twenty years ago? What would you pay for that same steak today? Knowing this information, you will reap the consequences of your choices and so should you choose not to act, then….. On the other side of the coin, if you choose to act the worst that can happen is that you were prepared and will have value accumulated for your effort. This is why you should care. If you have your life savings tied up in stored dollar assets anywhere and you have ten, twenty, or thirty years to retire, then you need to preserve the purchase power of your thirty-three cents starting today, right now! 1http://www.census.gov/const/uspriceann.pdf US Census data 5

- 6. Chapter 2 What Should I Use For A Hedge? There are a number of options. Precious metals, real estate, gemstones, stocks, bonds, Bank CD's and savings, annuities, foreign currency, collectables, arms and ammunition. Some of these make as much sense as burring your money in the back yard in a tin can. The following are in no particular order of importance. Option # 1, Precious metals. First, precious metals like gold, silver, copper, platinum, and platinum are a reasonable consideration. There are many sub categories to these like bullion, coins, company shares, and others. Precious metals are recognized worldwide as the basic medium of monetary exchange. They are portable and can be easily concealed or stolen. It is valuable enough it will attract thieves. They generally are the gauge by which most credible currencies and monetary values are measured. Minor precious metals like silver, copper, and others have great industrial demand. It has been said, the demand for silver used in electronics will cause the ratio between gold and silver to narrow significantly. Gold has value because it cannot be grown, manufactured, or generated or reproduced. There is a finite supply of gold, most of which is likely to be in the ground still. Because gold is compact and portable, it is convent to transport. Because a small amount has great value, great value can be more readily concealed and/or stored. Gold in the ten year period from 2003 to 2013, jumped from $281.50 to $1405-$1675 per ounce. That works out to a 399% or 596% increase of value for gold as compared to a 27.2% loss for a dollar stored anywhere. Gold is a medium of value recognized worldwide. There is a finite supply of silver as well. Silver is available and is purchased at a smaller cost outlay than gold or platinum. Pre-1965 minted junk silver, US coinage is commonly recognized. A real 90% silver dime should buy two moderately price loaves of bread at any given time. Four silver dollars should pay a day’s labor wage. Whereas a single 1/10 oz. American Gold Eagle will be about one and a half days labor for the same work. Gold and silver jewelry may be considered. As pretty as it might be, this probably is not a preferred way to hedge your buying power even though it may be a fantastic way to hedge a special relationship with your significant other. The cost of precious metal jewelry is mostly derived from the labor to manufacture it. When it comes time to exchange it for valued commodities like food or medical services, it will fetch substantially less for the precious metal value than if it were in a recognizable form like coins or bullion. Just buy a set of earrings or a necklace and take it to the nearest “We 6

- 7. Buy Gold Here” storefront. See what their best offer for it is. You will quickly understand. You should have a good reason for your choice of medium and the subset of that medium. You may want to consider a combination and diversification. Are precious metals better own than real estate? The answer depends upon your circumstances and your outlook for the future. Ultimately, only God knows what the future will reveal. Generally, a person has to be of some means to buy a chunk of land whereas precious metals can be obtained fully owned for a much smaller sum. Option # 2, Real estate. There are many considerations if deciding what kind of real estate might be right for you. Real estate is not as passive an investment as precious metals. Real estate has many advantages and everyone has to have a place to lay their head. Not all residences have to be luxurious. The old slogan “Under all is land.” has never been any more true than now. If you own/control land, you can have a feeling of well being, feeling of self-worth, live on or in, rise food on, barricade, and be less subject to the property owner moving you off. Useful characteristics possessed by real estate are for practical basic needs. It is a place for that subsistence garden, a means of growing food such as squash, carrots, turnips, and chickens, etc. Real estate is not displaced or hidden and the boundaries are readily definable. Wherever you put your foot or lay your head, you are on land. If you are at sea, the port is “land”. If you are in the air, the airport is “land”. If one can grow and store a winter’s food supply on his or her homestead, it may be worth more than an ounce of gold when cold and hunger occur. Believe, it can and most likely will occur. When it comes time to pay the property tax, a need for gold will become apparent. Even though carrots and turnips may be traded to others for needed supplies, they don’t work well as legal tender to pay the property tax. In the late thirties, my grandparents had a full wagon load of good potatoes that they hauled to town in a wagon pulled by a team of horses. They were not able to trade the whole load for a 25 lb. sack of flower. Yet, they never starved. Real estate is important enough that Chapter 4 is dedicated to real property, its intricacies, and ramifications. Option # 3, Gemstones. Gemstones may be something you may want to consider. Gems are not a readily recognizable commodity by the average person. More often than not, they have a relative lightweight and are easy to transport. They can vary from an inexpensive ten-dollar 7

- 8. emerald to a hundred-thousand dollar diamond. They can include diamonds, emeralds, rubies, satires, topaz, garnets, and many other semi-precious stones. To the uneducated person, gemstone quality diamonds look like natural diamonds, but can be faked, i. e. the very real zircon industrial diamond. Like gold and silver jewelry, much of the value is in the cost to produce, cut set, and mount. The mined diamond market is under strict control by international private cartels. The average person will not know how to color grade or discern an inclusion from a crack. The average person would stay away from trading their value for value in gems, the particulars they may not be failures with. Option # 4, Stocks. A certificate of ownership in a company is referred to as a stock. It represents ownership equity of some type in a specific company. There are many forms of stocks. Some give full ownership. Some give conditional ownership after an event occurs. Some come with dividends and some without. Stock trading is highly regulated for good reason. Might I say for one word, “greed”. Think about it, the shysters are steeling for greedy purposes and most people who get taken make themselves vulnerable because they are pursuing a faster easier way to wealth. There have been as many ways to use a good concept for illicit purposes as there are ideas, thus, the creation of regulations for each illicit concept to counter greedy activities. By in large, stock trading regulations do a very good job of protecting the average investor greedy or not. A person can take delivery of a stock certificate that simply means the stock certificate will be delivered into the owner’s hand. A stock certificate may be held in a “in house” account which simply means the certificate is held in trust by the brokerage firm for the benefit of the stock owner. Observation of the stock trading charts and system is an excellent example of how values of all markets fluctuate. It too is the most well-known system as the public observes and is exposed to daily reports on market changes in value like the Dow, S&P 500, and others. All investments medium values ebb and flow. The frequency tends to be quicker with securities more than other investments therefore, it is more readily observable to the average person. As to active involvement in the management of their ownership, most stock owners (shareholders) have little or no effective say in the management of the company they own. Many times, they do not even know what companies they have an ownership in or a piece of. Management is vests in the board of directors and Chief Executive Officer, comptroller, or CEO, not the miner equity holders even though they would likely have a shareholder vote. 8

- 9. There are some correlations between the relationship of stock holding value and inflation. It is a fact that historically when the inflation rates are a moderate 2% to 3%, stock values overall do well. As inflation gets higher, equity values suffer due to economic hard times for many of the companies in business. One can consider stock as a place to store ones purchase power but it is evident when times get tough the values may languish severely. That defeats the whole purpose of hedging against inflation. However if you believe stocks are an avenue for you to partake in, do it using investment clubs where others can have input in the goal helping to reduce the inherent risk of markets investing. Option # 5, Bonds. A bond is simply a promise to repay a debt for money lent. Bonds however are extremely dangerous to the person who does not fully understand the implications of market trends. Bond values are predicated upon the rate of return an investor would reasonably expect to receive on any investment. As expected interest yields increase, the value of any bond with a fixed coupon rate inversely decreases in corresponding ratio. Likewise as expected interest yields decrease, the value of any bond with a fixed coupon rate inversely increases in corresponding ratio. Here is an example. If the investor owns a thousand dollar bond with a coupon yield of 4%, then should the general expected yield on investments increase to 8%, the value of the bond he or she holds would decrease by half to $500.00. i.e. $1000.00 x 4% = $40. Now, if $40 is the yield and the expected return is 8% then, $40 divided by 8% = $500.00 which is the new bond market value. Every time inflation increases, expected yields increase causing the reevaluation of and not the purchase power of any bond decrease. This is true for or any other loan you hold as well. For example, let’s say inflation doubles, what could I expect? There is an expected prevailing return on any investment made and owning a bond is no different. Current yield at any given time generally is expected to keep pace with inflation even though it does lag some. Now, if inflation causes expected yields to double, the $1000.00 bond value devolves to $500.00 because of yield change. However, the purchase value of that $500.00 would be $250.00 because of inflationary loss. In the next seven-year segment even though yield returns may not have changed, purchase value would be $125.00 because if inflation, not expected yield change. The next seven-year segment would deliver a $125.00 purchase value from the original one thousand dollars invested in that $1000.00 bond. Understand, 9

- 10. in this example, the expected interest yields only changed one time, not three. Ongoing inflation is the bug in the ointment. The rule works conversely too. At the stated coupon rate, the yield a bond offers, when expected rates of return decrease, the value of that bond will inversely increase in corresponding ratio. As an example, that same $1,000.00 bond’s stated interest yield is say 5% or $50.00. When expected investment yield decrease by half to 2.5%, then the value of that bond will double to $2,000.00 based upon the then current expected yield of $50.00. Consider me this, in our day, what is the likelihood of the bond now yielding 4% decreasing as much as the chance of it increasing. In addition, in this day and age, there is always a chance of default by the debtor. Oh, I forgot, Government bonds have the full faith and credit of the US Federal Government to back them, with diluted deflated dollars. With inflation looming like a haboob in the desert, do you want to take that chance? If yields rates were as high as they were in the late nineteen seventies and early eighties, then consideration of bonds as a holding or investment might be warranted if you were convinced that hyperinflation weren’t in the offing but again, all things being equal in current times, investigate heavily and seek component counsel before making a lasting commitment. Option # 6, Bank CD's and Savings. Would you put a thousand dollars in a tin can buried in the back yard or under the mattress or in the freezer section of your refrigerator or in a hollowed-out book in the den? Not likely, According to the CPI, each dollar stored lost 27.2 percent of its purchase power between 2000 and 2010. The CPI shows no devaluation from 2013 to 2014, but have you watched the price of bread, steak, or services in the last year. Remember the CPI doesn’t account for the cost of petroleum as it affects other costs. Photo courtesy of PDPoto.org. Storing your purchase power in fiat cash money or equivalents is asking to be reduced systematically. Any place where one stores cash or cash equivalents like tin cans, savings 10

- 11. accounts, CD’s, or mortgage financing is virtually guaranteeing the shrinkage as indicated by past experience. Option # 7, Annuities. An annuity: A fixed amount of money that is paid to someone each year. : an insurance policy or an investment that pays someone a fixed amount of money each year.2 A single premium annuity is simply a loan to financial institution like insurance companies or banks. The operative word here is “fixed”. Placing funds in an annuity is no different than putting your money in a tin can except, it is there and you can’t take it out. Your funds are locked in, period. Your funds are subject to every effect of inflation for as long as it exists. Within the last decade or so, insurance companies have created annuity products that are tied to the stock market fluctuations. These products are referred to Index Annuities. They have the minimum guarantee features of fixed annuities but an appreciation ability that can move in value as the markets rise. At any rate, they are still a fiat cash equivalent storage medium. Annuities are guaranteed by the financial strength of the issuing company and usually by the underpinning authorizing government agency whose jurisdiction the company operates in. Annuities are as safe as any place you can store your funds, if the inflation threat is absent. Oh, yes, I forgot, Social Security is an annuity whose funds the US Congress has misappropriated and transferred to general government operating fund. Yes, those Social Security funds for which we paid into all our working years are being replaced with dollars issued by the FED. Option # 8, Foreign Currency. Consider foreign currency as an option. Do you really want to risk your wealth on some obscure currency like the Iraqi Dinar or the Vietnamese Dong. If the world goes broke, how on earth and at what exchange are you going to cash in? If some dictator starts a coup or completes one, what will happen to that currency’s value? In addition, the Forex markets are a plunge into the unknown for the average person. They have nothing to do with protecting your assets. 2www.merriam-webster.com/dictionary/annuity 11

- 12. Option # 9, Collectables. Art, antiques, stamps, non-gold or silver coins, may be items to consider as value storage items, but when it comes down to push and shove, in tough times, who will give you a sack of flour for some panting or a beanie baby. Option # 10, Armaments and Ammunition. Armament may be of value if the powers that be don’t outlaw them. We are already seeing legislation against the free trade of weapons in Colorado, Massachusetts, Maryland, New York, New Jersey, and Illinois. When civil uncertainty arises, armament and ammunition become valuable as a useful commodity and exchange medium of value. There could be criminal responsibilities if you provide a weapon to a felon or potential criminals. In real bad times, in the right hands, a rifle, bow and arrow, a crossbow, slingshot, a snare or even a fishhook might make the difference between starvation and sustenance. A wild rabbit, wild turkey, or even a dove could make all the difference. How many newsreels have you seen where the refugees in Africa have no means of gathering a meal and the children are starving. Guns are scrutinized by law enforcement and could be subject to confiscation attempts and strict regulation as they are in Illinois, New Jersey, and New York. If you are not intimately failures with their use, storage, and correct utility, then consider other alternatives. Option # 11, Tools and Skills. Quality tools to complete projects and repairs must be a primary consideration. These tools need to be basic and necessarily should not be electronic. Even if you have a generator, fuel may or may not be readily available or affordable at any price. Basic tools might include saws, hammers, hand brace, bits, hand screwdrivers, and any other tool you may deem necessary to complete an average project. Whether usefulness is more important to you than capital preservation must be your decision. An ounce of gold does a person no earthly good if the need at that moment is for a saw to cut heating fuel or a pot to cook one’s meal in. Consideration for basic preparedness must be a given at the time a person is waging war against the coming expectations. Basic trade skills are important. Understanding the way things work mechanically and the process of disassembling for repair can make life much simpler. If you don’t have funds 12

- 13. or trading goods to pay a plumber, electrician, or other professional, you become fully dependent upon the good graces of social generosity. Basic job skills, and production abilities too can be exchanged to assist others that find themselves in the above situation. Your skills may be the resource to provide for your own sustenance. The cash money economy, cash may be king, but it will be the deposed royalty when inflation takes hold. 13

- 14. Chapter 3 How Do I Counter The Coming Disaster You Ask? How, you ask? Utilize some or all the assets in the previous chapter whose value counter acts the devaluation of your dollars. In other words, place your purchasing power in assets that stay abreast of or increase with the cost of living as inflation increases. The characteristics of a wealth holder, a marker of purchase value are important. Durability is critical. You can’t do it by hording bread. Bread isn’t durable. It doesn’t have lasting intrinsic value. Consider items with intrinsic value like precious metals, real estate, Armament, gems, and coinage made from real precious metals. Photo courtesy of PDPoto.org. First, basics needs necessarily to be addressed. In most every circumstance, most people will choose to provide first for the basic needs of water, food, shelter, warmth, and medical. Many however are caught up in the “comfort for now” and “live for the moment” mode so easily that they forget to provide or plan for the future. The proverb, ”Go to the ant, you sluggard; consider its ways and be wise!”3 The ant not only stores for the future, but like the honeybee, it does so in a way that is beneficial to the society as a whole. My point here is, when you adequately provide for your own future, someone else doesn’t have to provide for you later say, in a refugee camp after all has gone south economically. Make sure you provide for the basics of water, food, shelter, warmth, and medical. Everybody provides for them now in one way or another. That is what the largest part of most paychecks are spent for. How, you ask? How do I counteract inflation’s advance? The answer is, change your habits and your thinking. When you think, take captive every thought, consider if you really need to spend your future on that trivial trinket of snack. 3Proverbs 6:5-7 New International Version Bible 14

- 15. In the nearest WalMart we see people spending money they don’t have for things they don’t need. Often if they were to forgo that candy bar and soft drink, that five dollar Starbucks, that extra pair of shoes, or new barbeque grill, they could save enough to purchase a gram of gold. In a year’s time, skipping one latté daily would buy a Gold Eagle or a Maple Leif. If people would pass up those spur of the moment expenditures, they may very well be on the first step to securing their future. Consider the consequences before spending that little dab of money on that new pair of shoes or exotic toy, People make the excuse that a penny here and there would never make a difference. When we made presentations at financial seminars, we would remind people that to be a millionaire you had to have the first penny. To be a millionaire you had to have the last penny. Without either the first or the last penny, you are not a millionaire. The point is, account for your expenditures and your pennies. Photo courtesy of PDPoto.org. Did you know that if you were a millionaire, hid your million in a tin can during the last twenty years, and inflation rate stayed the same as the CPI showed for the last twenty years, according to the CPI your million dollar’s buying value would have been reduced to six hundred thirty four thousand, some less than a million. This represents a loss of over one third in purchase value. Utilize holding mediums that possess the characteristics of limitation (scarcity), utility (usefulness), and is easily recognizable by many people. The most common are precious metals and real estate. Each has attributes to consider. One is portability. Precious metals, gems, bonds, stocks, guns, and cash money are portable. Real Estate is not. A person can sleep on, shelter on, and grow food on real estate while it is difficult to do these on the others. As real estate lacks portability, is not readily dividable, is subject to taxing authorities, is subject to government agency restrictions, is often subject to private covenant regulations controlled by the neighborhood authorities, all of which renders it a limited asset. It still is a major candidate as a viable inflation hedge. Physical characteristics will affect the 15

- 16. cost and value. Access to water for household use and irrigation from reliable water source is critical. Is gold better for you to own than real estate? The answer depends upon your circumstances and your outlook for the future. Ultimately, only God knows what the future will revile. Gold has value because it cannot be grown, manufactured, or generated. There are finite supplies of which much is likely still to be located in the ground. Because it is compact and portable makes it convenient to transport. Because a small amount has great value, great value can be more easily concealed. Gold is a worldwide-recognized medium of value. Watch this Video now, 16

- 17. Chapter 4 Is Real Estate A Special Consideration? Real estate like gold and silver likewise has a limited supply. Contrary to recent popular belief, real estate is subject to market conditions and valuation. Unlike gold and silver, the quality real estate depends greatly upon the amenities such as water, minerals, altitude, and relationships to other geographical features, and many other variables. It has discernible ownership boundaries, and cannot be moved. A person can’t hide it and it will not go away although as with any holding one can be estranged from it. The world is made of real estate. As realized by property owners and contrary to recent popular belief, real estate is subject to market condition fluctuations and valuations as are any other commodity. The greatest lie perpetuated by real property proponents is, “location, location, location”. I do not know how to say how much BS. that platitude is. Every piece of property has a value regardless of location. As a formally licensed real estate veteran broker, I say the proper statement and the truth is “price, price, price”. The most obscure piece of land in the Nevada desert has a value just as a square foot of commercial land on Wall Street. Every parcel of property will sell at a price no matter what its’ location. Free and clear real estate like housing, farmland, residential income property, and commercial buildings can be a good hedge too. Notice I stated “free and clear”. I will discuss the concept of leverage and loans as it applies later. It seemed to be a great surprise to the real estate related industries when the recent downturn occurred. If one looks at gold or stock charting, they will see values fluctuate. It is reasonable to know real estate values will fluctuate too although with not as much frequency. On the other side of the coin, so to speak, are detriments like tax obligations, up-keep, lack of portability, and valuation based upon the properties attributes. Property tax in New York State might be prohibitive as compared to property tax in Alabama. Access to basic amenities like water, power, and temperature conditions all may need consideration. The process of purchasing a personal dwelling, a home serves several purposes. Possessing a home affords a security and feeling of permanents. For the average person, making mortgage payments is a system of quasi-forced accumulation in small increments at a steady rate. Controlling a parcel of land and improvements allows for a certain amount of freedom in planning for near and the long-term future. Purchasing may require a nominal sum for down payment. These days it is often no more than the sums required for first, last and damage deposit if you were to rent or lease. These smaller down payment amounts allow for the start to building equity and a certain amount of self- determination. One can possess a dwelling by leasing or renting. This rent paying condition does not assist in the building of equity. Rent is rent. When it is paid, it buys that space and use of it for a time. When that time has run out, that is all there is. At the end of the lease term one can be put out, which, inhibits making plans for future events at that property. If you 17

- 18. were to plant a garden, you might not get the opportunity to harvest the fruits of your labor. We will now consider rental property from both viewpoints of the owner and the renter. Basic analysis of rental property as a revenue source and an investment is in order. Below is a sample “Rental Property Income Analysis”. Rental Property Income Analysis If you want to evaluate the return on the $180,000 investment, you have to annualized the Net Monthly Income by multiplying it by 12. The next step is to divide that result by the price of the rental dwelling. i.e. $10,796.40 divided by $180,000.00 = 6% annual yield on investment. Important to know is how to work the computations backward. Multiply the price of the investment property by the expected yield or rate of return. i.e. $180,000.00 x .06 = $10,800.00. Now, convert this yield into a monthly income by dividing the $10,800.00 by 12. = $900.00 18

- 19. Reverse Rental Property Income Analysis When renting, your costs as a property owner need to be covered. Ad those to the net monthly income required to return your desired yield on investment. The sum results in the Adjusted Gross Income. The next step is to apply the vacancy rate that applies to property in the location of this property. It may be as high as 50% or as low as 2% or 3%. 50% means that the property is not rented half the time. 2% means that the property could be vacant one week out of a year. To calculate equivalent of vacancy, subtract the rate from 100% and divide into the Adjusted Gross Income Required. i.e. 100% - 5% = 95% or .95 in decimal form. Then in this case, divide the $1260.00 by .95. The result is $1326.32 or the Gross Required Before Vacancy. To obtain the vacancy dollar value, take the difference between the two, or $66.32. Income after the management factor is applied and derived in the same way. If the property is located in an expensive location like New York, New Jersey, California, or a high hazard insurance state, then the numbers will be affected by extreme measures. All things being equal, the system does not change and remains the same. If you live in a high priced state, consider selling that expensive property. Relocate to where you can purchase a property with the same utility for half or less and diversify into other solid inflation countering hedges. Now you know the amount the property should rent for to return 6% on the $180,000 investment. Consider that each property has its own circumstances and conditions. The purchase price may be higher or lower. Tax costs can vary within the same region. Utility costs are different from community to community. Expected rates of return change and will change greatly as time advances. All these factors will affect you as the property owner or you as a renter. Inflation isn’t just the loss 19

- 20. of purchase value, it is the depletion of our economy as price increase builds upon price increase at an ever growing rate. In order to make a rate of return or even just break even, the owner needs to charge the tenant the amount indicated by the Reverse Property Income Analysis. As a renter, one would expect to pay that for a home. As the owner, the costs would be about the same except owner occupants have advantages that allow for equity build up, not being subject to eviction except for non-payment, and assurance of home base security. Inflation and the mortgage. In the “Great American Dream”, having the mortgage burning party is one of the goals to be strived toward. Many of the nationally noted financial advisers highly encourage the homeowner/borrowers to be debt free, which includes paying off the home completely. That is an admiral goal and for most a formidable task. It generally takes most people a lifetime to achieve. When your home is paid off in twenty-five to thirty years, what do you have? That national average $65,000 home in 1983 has inflated to $208,000.00 in 2013. Your loan at an average of 14% interest would have cost you $268,729.00 in total principal and interest costs plus property tax and hazard insurance over 30 years. If you had paid rent for that same period, you would have paid about $288,000.00 not considering the increase in cost of living. By financing, you would have force paid off the original loan of $65,000.00. You could have refinanced in 1988 and saved 5% interest. You would have saved $86,482.00 less refinance charges. All this just for background to provide understanding of how the system functions. At higher rates like the above 14% interest, to be “paid off” is probably golden. However, if the interest rates are 4% with expectations of a simple 10% hyperinflation, what then? Let’s look at paying off your loan or being free and clear verses the financing option. When your home becomes free and clear of debt, twenty-five to thirty years from now at 10% annual inflation, the $208,000.00 home will inflate to an approximate $3,630,000.00. If you finance $200,000.00 at an average of 4% interest, your total cost in total principal and interest paid would be $357,487.00 plus property tax and hazard insurance, which over 30 years you would pay anyway. If you had paid rent for that same period, you would have paid an average of $15,233.00 per month or approximately $5,484,000.00 over that 30 year period. By financing and subsequently buying, you would have force paid the original loan of $200,000.00 in that same period. By purchasing other hedge values with that $200,000.00 borrowed, at 10% inflation, they would grow to $3,489,880.00 less your total principal and interest of $357,487.00. Even though your original $208,000.00 has a huge deflated purchase value, you have nearly doubled your affective purchase value by hedging against inflation. You have used locked-in cheap interest to take advantage of a larger inflation factor. Do you really want 20

- 21. to pay off your home or take advantage of the circumstances? See the comments on leverage further on. I am not advocating for or against either. The intention here is to expose the options. An additional set of real estate inflation hedge ideas are for the senior population. Study closely and seek independent counsel before you choose one of these options. It is that of home-mortgage interest deduction from your taxable income. You should consult your accountant as to how it applies to your situation. Lately we see a movement by government bear cats to reduce or remove this deduction. Consider that when inflation carries you into the 30% or higher tax bracket, you could save a whopping $2160.00 in income tax from a $7200.00 home interest deduction on the $180,000.00 mortgage. Do you really want to make that extra principal payment each year. Maybe or maybe not. Recently created is a newer mortgage phenomena called “Reverse Mortgage” that was put into play by the Reagan Administration. The reverse mortgage is a way to convert home equity into cash money and at the same time retain ownership of one’s home. Reverse mortgage industry is regulated by the US Department of Housing and Urban Development commonly known as HUD. There are rules that are connected to the utilization of the program. The owner/borrower must be age 62 or older. The amount of loan borrowed is based upon a “loan to value” ratio dictated by actuarial demographics. The amount the owner/borrower can receive depends upon the current interest rate, appraised value of the property, and a maximum upper limit. The owner/borrower may be required to initially to have from twenty to forty percent equity in order to obtain the loan. There is mortgage insurance required and the cost or the premium required is figured into the amount to calculate the available borrowable funds. The owner/borrower has options of receiving money in a lump sum, annualized payments for a period certain, or payoff of an existing loan, all without a required monthly payment as in other mortgage loans. Property tax and insurance premiums don’t go away. They still are the responsibility of the owner and have to be paid. Upon the time the owner/borrower ceases to use the property as their primary residence, the loan principal and accumulated interest become due and payable.4 Another way to look at home financing and contrary of many opinions of the nationally known financial gurus who advise to have your home paid for, a reverse mortgage can have benefits when it comes to inflation application. If your property is free and clear, not having payments can be very satisfying. You know real property historically has stayed even with inflation and many times has outpaced inflation even though in part it is one of the factors in computing inflation. Knowing 4http://portal.hud.gov/hudportal/HUD or 21

- 22. property could keep pace with the inflation rate regardless of whether it is encumbered with financing or not opens the discussion about whether to be encumbered or not. If you are 62 years old or older and making payments, consider refinancing with a reverse mortgage, paying off the old mortgage. Your payments go to zero and the money you save on payments can be applied to acquire other inflation hedge products. A drawback is, the amount borrowed grows by the compounded accumulating interest. The value of the property may or may not ever catch up with the principal and interest owing. If you get too old to live in your home, the full amount owed becomes due and payable whether or not the property is worth the amount owed. The loan is insured with mortgage insurance so the lender has very little risk if you can’t pay or the property value falls below the accrued debt owing and you don’t pay. Who is backing that insurance? Could it be the government in one form or another? This is another hint that government powers are not concerned about curtailing inflation. Well, just bail out the reverse mortgage deficits with inflated dollars using rising bracketing tax to cover the debt later. If you are 62 years old or older and own your home with no debt, consider financing with a reverse mortgage, using the resulting cash to acquire other inflation hedge products. The same drawbacks still apply as in the example above. Another way to utilize the reverse mortgage if you are 62 years or older is to purchase a home with the required down payment and finance the balance with a no payment reverse mortgage. Again, the same drawbacks still apply as in the first example above. Utilize the savings you used to pay for rent or other housing payment to hedge inflation. If you are determined to use investment real estate as your means to hedge inflation, consider utilizing a quality complex property search tool to assist. Watch video by clicking on the banner. 22

- 23. Chapter 5 To What Purpose? Purpose of protecting against hyperinflation It is easy to be caught up in and focus on a survivalist mode verses focusing on the mode of counteracting inflation. Depending upon what one’s outlook is will determine the action plan one implements. If you have confidence that life and our society will continue as is, then preparing for strict inflation and monetary collapse may be all you may want to do. If on the other hand, you believe financial collapse of the currency will precipitate the collapse of your economy and way of life, then you may want to consider a deeper and more personal and additional survival positioning. The purpose of “The Coming Hyper-Inflation Apocalypse” is intended to be a general wakeup call about how to survive the impending circumstance. It is not intended to be a personal survival guide although consideration for survival events needs to be touched upon. One of the first laws of investment is the utilization of diversification. Why, because diversification spreads the risk of loss between several investment or preservation mediums you might control. Ideally, when the market value of one medium declines, the others will hold their value. Additionally, the hope is that not all will decline at the same time. The old adage about not “putting all your eggs in one basket” is precisely about this situation. One should consider not only diversifying between types and various anti-inflation mediums, but in how he or she will address the short-term adverse conditions that affect their welfare. Other considerations to review are, should you put all your available assets strictly in the inflation hedge or would basic survival assets be an option. “What assets”, you ask? Will your basic survival needs be met in the event of calamity? If you have been through a hurricane, the artic vortex, tornado, wildfire, riot, earthquake, epidemic, flood, volcano, tsunami, terrorist attack, and your electricity has been off for a week or two, you should have a sense of what I am referring to when I say “calamity”. Consider an emergency plan. You may ask, “should I acquire Gold Eagles or Kugerands”? As part of your hedge and if you are not considering basic survival as part of your plan, would you have a need for smaller denomination forms of precious metals to buy a loaf of bread with? On the other hand, if you have your hedge holdings in smaller denominations like five-dollar gold piece or a one-gram gold bar, exchange for commodities becomes simpler when it comes time to buy that loaf of bread. After a person has developed a plan to achieve their basic survival goals, it is helpful to know the fundamentals for utilizing the laws of finance. Utilizing the laws of finance in and of itself will help mitigate some of the normal losses caused by inflation. 23

- 24. Providing for the basic personal needs of water, food, shelter, and medical is paramount. Everyone should consider his or her dwelling, their home as a first place to start when considering assets for hedging. I have made a strong case for home ownership verses renting. Now that basic needs have been considered, consider provision for future basic needs when an emergency should arise. It is not expensive to be prepared for emergencies, but if you are not prepared when the need arises, the cost can be unmeasurable. Ask those in the Midwest and the East who have been without electricity for a week to ten days in the last three years. There are millions of them. Everyone should have an emergency savings as well as well as emergency stores. These two facets hold the same purpose, to span the gap between good times and destitute times. Emergency funds should not be moneys that are readily available to spend upon a whim, but should be funds that are available and at hand only to obtain and provide the needed basic requirements of, water, food, shelter, and medical, etc. These funds are not funds in a slush fund at a bank somewhere where electricity or marshal law may inhibit access. They are funds you can put your hand on if the electricity and services go out like in Hurricane Sandy. “What are good forms of emergency fund storage and how much do I need?” you may ask. The answer depends upon what you visualize your needs being and what circumstances you believe you may encounter. If you are a person of one or a family of six, your needs are different. A little dab of cash fiat money is good, but destroys easily in wind, fire, and rain. Durable forms of emergency funds are junk silver coins and small denomination gold. We are not talking here of collector coinage, but basic down to earth common coins and bullion bars. If times get really tough, these coins are recognizable by most people. Larger denomination gold may be less satisfactory as the greater value could be hard to deal with, make and receive change for. Precious metal coins will always possess utility or industrial value and should major deflation occur, the coin will retain the greater of the coin face amount or the intrinsic value of the metal. Small denomination pre-1965 dimes, quarters, and half dollars should be considered in addition to the fiat paper money. A 90% pre-65 silver dime still after a hundred years is worth the value of a couple loaves of bread in this day. If needed you can always sell your coins to the local coin dealer for fiat money (paper cash) if physical conditions haven’t shut the dealers down. Again, these are not funds intended for use with instant access. By virtue of not being an instant access item will help in keeping these funds intact. 24

- 25. In addition, diversification of this emergency account is as critical as your other assets and for the same reasons. Include a minor few fiat bucks, more pre-65 silver coins, some gram size gold bars, some $5 and $10 dollar gold coins and then ounce size gold coins. A third medium that you may want to consider for a diversification is armaments and ammunition. In destitute times, a shotgun and shells of a variety may be paramount for acquiring a meal and home protection. Remember there is a great responsibility associated with owning a gun. The caliber you choose will depend upon personal preference. Owning a gun doesn’t have to be expensive or complicated. Personally, I prefer simple weapon construction with as few moving parts to break or repair as possible. If your plan opts for arms and ammo, you should become intimate with your tool, the firearm, its use, storage, and safety measures. Choosing which mediums to diversify into and in what amount is a personal choice. Diversifying may include other items in addition to basic needs preparation of emergency funds, procurement, and protection. As we turn to the next law of finance, we learn another way to take advantage of the natural financial law, “Dollar Cost Averaging”. It is important to understand. The concept works well for those who procure holdings on a regular periodic schedule over time with an equal amount of capitol in equal periods and when buying valued items whose values flux. When the subject product is higher in price, fewer units of the holding are acquired during that buying period. When the prices are lower more units of the holding are acquired during that buying period. The success of this investment style depends fully upon the price being variable while acquisition occurs. It also depends upon the dollar value being consistent and invested at regular intervals. I have observed as much as a 15% growth over natural market values in variable markets by using this strategy. Real estate is not a good candidate for this strategy. The markets do not fluctuate often enough and most do not possess the funds it takes to make those large period investments required to purchase multiple properties. Because of the nature of acquiring real estate by the average person, the average buyer is forced to put down a modest down payment and make periodic payments if they want to remain in possession. By purchasing in this manner, over time, substantial sums may be amassed in equity that tends to stay abreast of inflation. Many national known financial advisers are avid proponents of becoming debt free. There is validity to this concept in some circumstance, but not all. For short-term debt and debt subject to usurers interest rates, everyone should be paid off and the debt should not be renewed. On the other hand, I take issue with the idea of paying your real estate debt off especially if it is your home and especially if you expect significant inflation. Exceptions to home debt are loans with variable interest rates and 25

- 26. debts on income property that don’t carry their own way as well as ultra-high interest rates. If you have funds to pay it off, use those funds to obtain other sound inflation hedges. Consider precious metals in form of junk silver and small denomination gold. You can store large amounts in the safety deposit box at several banks if needed, but not your emergency funds. Keep them at readily at hand. If I owe on my modest home the amount it is worth, i.e. equity to debt ratio of zero, I should gradually be building equity through payments on principal reduction even if the property doesn’t appreciate, or shall we say inflate. If I didn’t own it I still would have rent payments equal to larger than the cost of the mortgage payment, utilities, property tax, and upkeep. See the explanation in the previous chapter on rental property income analysis. All things being equal, owning is better than renting. Now, assume hyperinflation of a simple 10% per year for the next ten years. My $180,000.00 home would be worth $425,743.00 and I still only owe $141,000.00 after making payments for that past ten years. Now understand, the purchase power in the value of my home is not worth any more than before when I purchased it, but the dollar value is in a deflated condition. Likewise, that $180,000 mortgage is being paid with greatly deflated dollars. Let me ask this, when hyperinflation appears like it did in Germany in the 1920’s and in Argentina in the 1980’s, and as it will here, what will happen at 20% or 30% in the home scenario above or in your own housing scenario? It can happen, it already happened 53 other times around the world in the last one hundred years. Now the government could index all debt obligations to any new currency reevaluation. Even then, you would be no worse off than when you first started except fiat cash money would be worthless. Theoretically, you should still have your accumulated equity through self-imposed forced payments. If indexing occurs, all bets are off. In light of government re-indexing, one would want to seriously consider how much real property debt he or she should carry. The Federal Government could confiscate gold too. I quote, “Executive Order 6102 is a United States presidential executive order signed on April 5, 1933, by President Franklin D. Roosevelt "forbidding the Hoarding of gold coin, gold bullion, and gold certificates within the continental United States". The order criminalized the possession of monetary gold by any individual, partnership, association or corporation.5 Too, see the Gold Reserve Act Of 1934. Over reach of government is not a new phenomenon. Gold and Silver is easier to conceal than real estate although most would comply with federal confiscations regulation. In the current politically charged atmosphere, a faction 5From Wikipedia, the free encyclopedia 26

- 27. exists who will defend their right to the death to determine their own destiny without government interference. Another strategy is playing the ratio balance between gold and silver. There is a historical balance, a ratio between gold and silver values that can be taken advantage of. Currently gold to silver ratio is about 65 to 1. It has been 45 to 1 often nearly 100 to 1 historically. This is just another alternative. As an investment strategy, leverage can be used to make a fortune. It can work for the investor like a sling shot but can work against the investor even faster. To double the value of an investment, it has to increase by 100%, but if it only drops by 50%, the value of the investment will be back to the original value. Look at it the other way. If my investment drops by 50%, it has to go up by 100% to get back to the original value. Hold this concept in mind as we discuss leverage. How leverage works. First example, when the investor purchases a property for $100,000.00 in cash paid for in full and that property appreciates in value 10%, the investor makes a 10% profit less acquisition, holding, and disposal costs. Assets now equal $110,000.00. Second example, if the investor borrows 80% of the property value, using the same $100,000.00 as a 20% equity down payment or $20,000.00 down payment on each of five properties, he or she could purchase five times as much property as in the above. The appreciation still being 10%, but now 10% times the five properties now under control will yield five times the appreciation profit as in the one property cash purchase above. i.e 5 properties x 10% = 50% return on the $100,000.00 less of coarse acquisition, holding, and disposal costs. This increases your equity by one third to $150,000.00. That leverage works for real estate, stocks, precious metals and any asset that has appreciation potential. In the case of stocks, there are strict securities regulations that govern how much can be financed. One of the major causes of the stock market crash of 1929 was over financing and low equity to debt ratio. Many stocks were leveraged to the max. The stocks went down in value. Remember the 50% and 100% example above? Nobody says much these days about low equity financing of millions of homes in the US during the early part of the twenty first century. Hmmmm Above the example of the 50% return was demonstrated. Should the investor incur a decrease of value on the first property of 10%, he or she would have a loss. But when the investor owned five of the properties financed as in the second example, wowza! 5 properties x 10% = 50% loss of the original equity. We saw leverage work backwards against many real property investors in the early eighties and again after the turn of the century. 27

- 28. The whole point is, if you are going to leverage your assets with “other people’s money”, understand that it can work against you greater than it will work for you. A 10% appreciation gains you one third more while a 10% decrease looses you not a third, but half your asset value. Be aware of this when contemplating leveraged market plays. A simple financial tool one can use is the “Rule of 72”. If you want to know how long it takes to double your investment, divide the number 72 by the interest rate of return. Conversely, If one wants to know what rate of return would need to be received to double your value in X years, simply divide X years into the number 72. i.e. 7.2% interest will double my value in 10 years. Conversely, if I want to double my money in ten years, divide 10 into 72 and the result will be 7.2 percent. If you want to know how long it will take for your purchase value to be cut by half, simply divide the number 69 by the expected rate of inflation. i.e. 69 divided by 6.9% = 10 years. My $100,000 purchase value today would have to be $200,000.00 to preserve the same purchase value in ten years. Let’s try another. 69 divided by 10% = 6.9 years. Another, 69 divided by 13% inflation = 5.3 years. 13% inflation is not unrealistic. We had 13.58% in 1980 as provided from the CPI. In Germany 1923, prices doubled every two days. Annual inflation in 1989 in Argentina was twelve thousand percent (12,000%). 28

- 29. Chapter 6 Do You Need Further Proof? I have stated before that inflation is premeditated. It is the elephant in the room that is seldom discussed. Let’s start with the graduated income tax brackets. As income increase, tax bracket percentages go up. As you and I need to make a higher income to stay abreast of the cost of living increase, we edge into higher tax brackets. In addition, these days, tax deductions are being eliminated one by one. Let’s consider the cost the home of $180,000.00. To qualify for the mortgage payment, the annual earnings would need to be roughly $50,000.00. If inflation were to rise 10% over the next ten years, we could reasonable expect interest rates to jump two and a half times. The annual earnings at the time to qualify for the mortgage on this same dwelling would have to be $287,000.00. All costs are higher including interest to compensate for the rise in inflation. Property taxes will be higher as well as the cost of maintenance. Income taxes evolve to higher burdens due to tax bracket creep. Is it any wonder government feels deficit spending is ok? Just pay the debt with cheaper devalued dollars later. Would you be interested in some savings bonds? Additional factors as to why my dwelling will inflate in price and not value is, as building materials inflate, costs go up to construct. As costs of living go up, wages for labor need to increase in order to keep up. iiiiiiivv Take the basic steps to survive economic catastrophic collapse. 29

- 30. Prolog All the above applies to inflation and financial matters. Turning to the last, final, and most important aspect of concerns about future events we need to consider where your mind is. Those of us who believe that which is written in the Bible will find the promise that God will provide a way. “do not worry about your life, what you will eat or drink; or about your body, what you will wear. Is not life more than food, and the body more than clothes? Look at the birds of the air; they do not sow or reap or store away in barns, and yet your heavenly Father feeds them. Are you not much more valuable than they?6 worrying is not of God. I believe that God will and does provide. I also believe that the birds of the air also land and pick up tidbits as He made them to do. We like the birds of the air have the ability to reason and plan like the ant. Should we not use those God given gifts? 6Matthew 6:25-34 New International Version Bible 30

- 31. i Published with permission of The Coming Hyper-Inflation Apocalypse By Keith V. Loucks ii http://2b221h37-fre1tbl18o-hf0t7x.hop.clickbank.net/?tid=HYPERINFLATION iii http://IwishIHadanOrange.com Adventure novel about EMP iv http://www.keithloucks.com/kvloucks/AlternativeTreatmentForCancer v http://59a097wgqgli3obxtop719ogzk.hop.clickbank.net/?tid=HYPERINFLATION