Call Girls Koregaon Park Call Me 7737669865 Budget Friendly No Advance Booking

Keynote capitals stock ideas

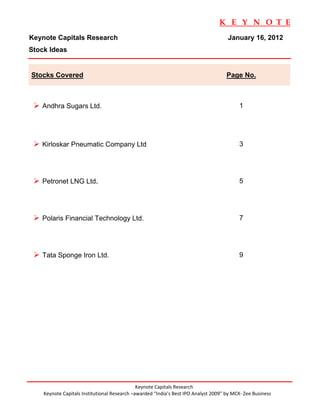

1. K E Y N O T E

Keynote Capitals Research January 16, 2012

Stock Ideas

Stocks Covered Page No.

Andhra Sugars Ltd. 1

Kirloskar Pneumatic Company Ltd 3

Petronet LNG Ltd. 5

Polaris Financial Technology Ltd. 7

Tata Sponge Iron Ltd. 9

Keynote Capitals Research

Keynote Capitals Institutional Research –awarded “India’s Best IPO Analyst 2009” by MCX‐ Zee Business

2. K E Y N O T E

Andhra Sugars Ltd.

Key St

tock Data Andhra SSugars Ltd. (A

ASL) was inco

orporated in A

August, 1947 engaged in m manufacture aand

sale of su

ugar, organic and inorganic chemicals being the ma ones at T

c ajor Tanuku, Kovv vur,

Sector Commod Chemicals

dity Taduvai, Saggonda and Bhimadole in Andhra P

e Pradesh. It is the largest manufacturer of

s r

CMP `116.15 caustic soda in south India. The c

company has three subsid diaries viz. Th Andhra Fa

he arm

52wk H

High/Low `130/ 84.55 Chemical Corporation Ltd. (AFCCL largest man

L) nufacture of h

hydrazine hyd drate (300 TPPA)

Market Cap

t `3.14bn at Kovvu JOCIL at Guntur is in the business of manufac

ur, s cturing fatty a

acids, glycerin

ne,

soaps, etc. and Hindusthan Allied Chemicals Ltd. ASL ha two assoc

d as ciate companies

($61.05mn)

known a Sree Akka

as amamba Tex xtiles and An

ndhra Petroc chemicals Ltd (APL) which

d.

6m Avg daily vol 8923

g. produces oxo-alcohols at Visakha

s apatnam, with technical c

h collaboration from M/s Da avy

BSE Se ensex 16154.62 Mckee of London, usi the latest LP Oxo process technolo

f ing t ogy, designed to produce 2-

e

ethyl hex

xanol or butan

nols.

Reco ‘Buy’

BSE Code 590062 Besides, ASL has in nterests in th power bu

he usiness with investments in the Andh

s hra

NSE C

Code ANDHRSUGA

AR Pradesh Gas Power Corporation Ltd. (APGP PCL), apart from its ow 16 MW c

wn co-

Face V

Value `10 generatio power plan and 11.60 MW of wind f

on nt farm. Power i one of the critical inputs to

is s

manufact ture Caustic S

Soda. Major power require ement for the production o Caustic So

e of oda

is met ou of this sour (APGPCL at an econo

ut rce L) omical rate. T supplemen and to ensu

To nt ure

adequate and continu

e uous availability of power f production purposes non-conventional

for n

Share tern (30th

eholding patt

wind pow is genera

wer ated at Rama agiri in Andhr Pradesh and at Veeran

ra nam in Tirunvveli

Sept, 2011)

district of Tamil Nadu.

f

Publi India is the second largest prod ducer of suga in the wor with 10 to 12% production

ar rld

c & of the world. Acc cording to the sources, till September, 2011 sugar

e , rcane has be een

Othr DIIs planted in 50.93 la hectare a

akh against 49.44 lakh hectares in same per

s riod last year up

45% 1% by 3% ASL has s

%. sugar manufa acturing capac of 5000 T

city TCD at Sugar Unit-I, Tanuku,

r

a 250 TCD capa

00 acity plant at S

Sugar Unit-II, Taduvai, and a 2000 TCD capacity pla

d D ant

Prom at Suugar Unit-III, Bhimadole. The compan produces 30 KL per d

ny day of industrial

oters alcoh from molasses, which is the raw mat

hol s terial for etha

anol (absolute alcohol), ace

e etic

54% acid, acetic anhyddride and ethy acetate.

yl

At present ASL pr roduces ethan on a limite scale. But in the comin years ethanol

nol ed t ng

produuction in the c

country will re

eceive impetu as the GoI proposes to come out with a

us h

policy to make m

y mandatory the blending of ethanol with petrol. This will provide an

e h

Price Performance (%)

) oppoortunity to the company to look into the possibility of expanding th production of

he n

ethannol.

1 Mth 3 Mths 6 Mths 1 Yr

Going forward ASL will also be benefited fro its strategic capacity ex

g e om xpansion plan of

n

4.64 18.46 19

9.68 2.65

Hi-Sttrength Hypo Plant propos to be set at Saggonda to produce Poly Aluminiu

sed a um

Stock Price Performance

k Chlorride extensiv

vely used in water treatm ment plants, aqua culture dairy, text

e, tile,

leather, paper and host of other industries.

d

120

ASL intends to d diversify in p

pharma segm ment and ha purchased a plot at t

as d the

110

Jawaaharlal Nehru Pharmacity, Vishakhapat ttanam. It is i the proces of finalizing a

in ss g

100 suitable product-line to be mannufactured fro this facilit With bette realisations in

om ty. er s

90 sugar, steady dem mand for chloor-alkali products, new pr roduct develo

opments back ked

80 by acctive R&D effo will help A post a de

orts ASL ecent performmance going fforward.

70 ASL’s expansion plan and with cane crush

s hing expected to be highe in the coming

d er

60 seaso expect w

on well for its gro

owth. Althoug production of caustic soda remain

gh n ned

unde pressure ow

er wing to highe imports. To help the do

er o omestic industry, governme

ent

Jan‐11

J 11

Mar‐11

May‐11

Sep‐11

Nov‐11

Jan‐12

Jul‐11

J l 11

has imposed impo duty of bot caustic sod and soda a

ort th da ash.

Andh

hra Sugars

BSE_

_SENSEX

1 Keynote Cap

K pitals Resear

rch

3. K E Y N O T E

Key Financials (`Cr)

Particulars FY07 FY08 FY09 FY10 FY11

Net Revenues 576.12 463.99 571.91 551.59 468.83

EBITDA 146.63 116.09 133.95 156.44 108.47

Net Profit (Adj) 64.15 42.58 45.28 66.76 36.21

Earnings Per Share 22.64 14.96 15.81 23.94 12.58

Price Earnings 3.82 5.46 3.76 5.01 7.01

EBIDTA Margin (%) 25.45% 25.02% 23.42% 28.36% 23.14%

PAT Margin (%) 11.13% 9.18% 7.92% 12.10% 7.72%

RONW (%) 20.53% 10.29% 15.60% 19.80% 10.89%

ROCE (%) 25.37% 9.03% 14.48% 18.98% 9.36%

Sources: Keynote Capitals Ltd.

Quarterly Financials (`Cr)

Particulars Q2FY10 Q3FY10 Q4FY10 Q1FY11 Q2FY11 Q3FY11 Q4FY11 Q1FY12 Q2FY12

Net Sales 132.1 143.61 126.59 103.48 107.22 116.69 142.64 180.32 195.51

Other Income 9.95 5.34 6.89 8.26 13.37 15.89 14.22 9.27 17.58

Total Income 142.05 148.95 133.48 111.74 120.59 132.58 156.86 190.04 217.5

Total Expenditure 104 96.99 101.17 90.87 100.31 111.34 108.63 147.82 161.17

PBIDT 38.05 51.96 32.31 20.87 20.28 21.24 48.23 42.22 56.33

Less: Interest 5.72 4.74 4.39 4.1 3.94 4.73 6.05 6.28 4.35

PBDT 32.33 47.22 27.92 16.77 16.34 16.51 42.18 35.94 51.98

Less: Depreciation 8.68 8.72 8.81 9.17 9.4 9.6 9.79 9.85 9.47

Tax 7.85 12.95 6.5 2.5 1.5 2.3 12.17 7.5 13.3

Profit After Tax 15.8 25.55 12.61 5.1 5.44 4.61 20.22 18.59 29.21

EPS (`) 5.83 9.43 4.65 1.88 2.01 1.7 7.46 6.86 10.78

PBIDTM (%) 28.8 36.18 25.52 20.17 18.91 18.2 33.81 23.41 28.81

PBDTM (%) 24.47 32.88 22.06 16.21 15.24 14.15 29.57 19.93 26.59

PATM (%) 11.96 17.79 9.96 4.93 5.07 3.95 14.18 10.31 14.94

During FY11, ASL posted 45.76% lower net profit (adj) of `36.21Cr on 15% lower net

sales of `468.83Cr. Its EPS was `12.58 and it paid dividend of 55%. For Q2FY12, its net

profit shot up 440% to `29.21Cr from `5.44Cr in Q2FY11 on 82% higher sales of

`195.51Cr and the Q2FY12 EPS stands at `10.78. For H1FY12, was `47.81Cr on 78%

higher net sales of `375.83Cr leading to a H1FY12 EPS of `17.6. Its equity capital stands

at `27.11Cr with reserves of `467Cr and sound debt:equity ratio of 0.7:1.

ASL a six decade old company represents a relatively safe investment option for the

investors. Although its sugar division continues to be a loss making units, the caustic

soda & industrial chemicals divisions are doing extremely well. ASL’s segment wise

revenue is sugar – 26%; caustic soda – 46%; chemicals 17% and others – 11%. At the

current market cap of `314.88Cr and considering ASL’s track record and management

capability indicates a scope for share price appreciation.

Keynote Capitals Research 2

4. K E Y N O T E

Kirloskar Pneumatic Ltd.

Key Stock Data We recommend buying in Kirloskar Pneumatic Company Ltd. (KPCL) as a value

buy.

Sector Capital Goods

Incorporated in 1958, KPCL provides high end integrated solutions using

CMP `451.75

Compression & Transmission Technologies. The company caters to the

52wk High/Low `600 / 375

industries like Petrochemicals, Power, Steel, Cement, Food & Beverage,

Market Cap `5.78bn Defense, Construction & Mining and many more.

($112mn)

6m Avg. daily vol 6,192 KPCL derives 89% of its total revenues out of compression systems products

BSE Sensex 16,154.62 while rest from transmission products. The company generates 60% of

revenues from projects business and balance from equipment supply. The

Reco ‘Buy’ company pioneered CNG Systems, Coal Gasification compression systems etc

in the country. It has supplied refrigeration system for all refineries in the

BSE Code 505283

country. The compressor division has just completed the coal gasification order

NSE Code NA

project. It is the market leader in CNG market with 40-45% share.

Face Value `10

In transmission products, KPCL caters to Gearboxes for Railways and Marine

th

Shareholding pattern (31 industries. The company does not supply to auto industry and therefore it is not

December, 2011) vulnerable to auto industry slowdown. The company has also diversified into

Public wind mill gear boxes, where the company manufacturers 1 MW gear boxes for

15% MW class WTGs. This is the only company apart from Suzlon, which has

Corpo

rate captive gear box production facility that is into manufacture of MW class gear

6% boxes.

Prom

nstitu oter

tions 56% KPCL has completed a revamp program of transmission business for which it

20% Forei made huge investment. The company has demolished its old plant totally to

gn

3% make it suitable for manufacturing large gear boxes. Replaced about 80% of

the old machines with machines with latest technology and is now brand new.

Price Performance % The company received permission from Indian Railways for operating Road

Railer trains in Delhi Chennai corridor. This is different from the roll on & rolls

1 Mth 3 Mths 6 Mths 1 Yr off service currently offered by CONCOR and other players. For example if a

-0.15% -7.27% -4.24% -5.78% car loaded specialised wagon at the Gurgaon Factory of Maruti Udyog will get

offloaded only in the premises of a Dealer in TN or AP without changing the

Stock Price Performance wagons. The specially made bogies/wagons will be decoupled and connected

to truck and taken to dealers. Manufacturing of road railers will start by

120%

115% Q3FY12.

110%

105% The company has over `500Cr order book while the average ticket size ranges

100%

from 006020-100Cr.

95%

90%

85% KPCL is fundamentally strong company with debt to equity of just 0.14x and

80% Return on Equity of 25.2%. The company’s stock price outperformed the

75%

Sensex over a one year period. Its share price dropped 19.3% for last one year

70%

compared to a negative return of 22.5% by the Sensex. Considering the

current inexpensive valuation, 7.7x for FY12 based on annualized EPS `58.76

KPCL BSE_SENSEX (5-year average forward P/e is 12.18x) and reasonable dividend yield of 2.9%,

we expect the downside is limited for the stock and can be considered as a

good value pick.

3 Keynote Capitals Research

5. K E Y N O T E

Key Financials (`Cr)

Particulars FY07 FY08 FY09 FY10 FY11

Net Revenues 353.56 398.75 514.57 453.28 491.73

-

Growth (%) - 12.78% 29.05% 11.91% 8.48%

EBITDA 37.07 37.99 66.67 70.96 72.77

Growth (%) - 2.48% 75.49% 6.43% 2.55%

Net Profit 26.52 29.82 40.74 44.59 42.78

Growth (%) - 12.44% 36.62% 9.45% -4.06%

EPS (`) 33.4 22.05 30.12 35.01 31.93

P/E (x) 22.8 6.2 14.1 14.8 14.1

EBIDTA Margin (%) 10.5% 9.5% 13.0% 15.7% 14.8%

PAT Margin (%) 7.5% 7.5% 7.9% 9.8% 8.7%

RONW (%) 41.1% 36.1% 46.8% 41.2% 36.1%

ROCE (%) 41.8% 32.0% 35.1% 32.9% 25.2%

Source : Company

Keynote Capitals Research 4

6. K E Y N O T E

Petronet LNG Ltd.

Key Stock Data Petronet LNG was incorporated in 1998 as a JV by the Govt. of India to import LNG

and set up LNG terminals in the country. Its promoters are GAIL (India), ONGC, IOCL

Sector Gas Distrib. and BPCL, each having 12.5% stake in Petronet LNG. In addition, GDFI (part of GDF

CMP `156.65 Suez, a French national gas company) holds a 10% stake and is a strategic partner.

52wk High/Low GDF Suez has been the largest LNG importer in Europe for the past 30 years. Asian

`185.85/105.1 Development Bank also has a stake of 5.2% in Petronet LNG.

Market Cap `12198Cr The Dahej LNG terminal was started in 2004 with a capacity of 5 mmtpa. The terminal

($2.36bn) is strategically situated in the biggest gas consuming state in India and is in close

6m Avg. daily vol 23,06,889 proximity to Qatar, the company’s main supplier. In 2009, capacity of Dahej terminal

BSE Sensex 16,154 was increased to 10 mmtpa. Currently, the company has a 25 yr LNG supply contract

for 7.5 mmtpa with Rasgas of Qatar. LNG is transported via three tankers—Disha,

Raahi and Aseem to the Dahej terminal. The company has back-to back off-take

Stock Codes agreements with GAIL, IOCL and BPCL in the ratio of 60:30:10, respectively. The

terminal is well connected with GAIL’s HVJ & DUPL pipelines and GSPL’s network in

Bloomberg Code PLNG IN Gujarat. The company has recently contracted 1.5 mmtpa for 2 yrs and has entered

Reuters Code PLNG.BO into offtake agreements for the same. The company also provides regasification

BSE Code 532522 services wherein companies can use Petronet LNG’s facilities for regasifying their LNG

NSE Code PETRONET cargoes.

Face Value `10

Capacity Expansion: Petronet LNG is expanding its capacity in Dahej by 5 mmtpa

by constructing another jetty and expanding its regas plant facilities to handle

Shareholding Pattern (31st Dec, higher volume of LNG. This expansion is being done at a very competitive capital

2011) cost of `20bn. The company is also constructing a greenfield LNG terminal of 5

mmtpa at Kochi at an investment of `42 bn. The higher capex/ton reflects current

Public & costs of setting up LNG terminals and is in line with other projects scheduled to

Others

27.53% come up in the future. Kochi terminal is expected to be operational by the end of

FY13, thus, contribution to topline and bottomline is expected from FY14. There is

sufficient pent-up demand for natural gas in the Southern region, mainly from the

industrial sector in Mangalore and Kochi. The management is confident of

DII supplying LNG from its Kochi terminal to BPCL’s 9.5 mmt Kochi refinery and MRPL

7.92%

(Capacity: 11.8 mmt). Both these refineries are undergoing capacity expansion to

Promoter 15 mmt, which would require additional volumes of gas.

FII

50%

14.55%

Key Financials

(`Cr)

Price Performance Particulars FY07 FY08 FY09 FY10 FY11

(%)

1 Mth 3 Mths 6 Mths 1 Yr Net Sales 5508.96 6555.31 8428.70 10649.09 13197.29

-0.8% 0.3% 8.5% 26.5% Y-o-Y Growth % 43.6% 19.0% 28.6% 26.3% 23.9%

Total Expenditure 4860.90 5689.18 7527.43 9802.63 11981.02

Stock Price Performance EBITDA 648.06 866.13 901.27 846.46 1216.27

Y-o-Y Growth % 32.8% 33.6% 4.1% -6.1% 43.7%

160

140

Margin 11.8% 13.2% 10.7% 7.9% 9.2%

120

Interest 107.04 102.36 101.21 183.93 193.13

100 Depreciation 102.03 102.18 102.52 160.86 184.67

80 Tax 162.33 240.52 255.60 195.00 286.80

60 PAT 313.25 474.65 518.44 404.50 619.62

Jan-11

Mar-11

May-11

Jun-11

Dec-11

Jan-12

Feb-11

Jul-11

Sep-11

Oct-11

Apr-11

Aug-11

Nov-11

Y-o-Y Growth % 60.7% 51.5% 9.2% -22.0% 53.2%

Margin 5.7% 7.2% 6.2% 3.8% 4.7%

Petronet LNG BSE Sensex

EPS (`) 4.18 6.33 6.91 5.39 8.26

(Source - Keynote Capitals ltd.)

5 Keynote Capitals Research

7. K E Y N O T E

Demand-supply gap of natural gas in India: The Indian market for natural gas has

always suffered from a chronic shortage of supplies. This is due to limited domestic

gas supplies, gas pricing & customer allocation being the prerogative of the Govt.

and inadequate transmission infrastructure in the country. A study by Mercados

shows that natural gas demand is expected to grow at CAGR of 21% from 179

mmscmd in FY11 to 381 mmscmd in FY15. On the other hand, the Directorate

General of Hydrocarbons (DGH) estimates that supply will grow at CAGR of 8.6%

only from 146 mmscmd in FY11 to 203 mmscmd in FY15. Thus, the demand-supply

gap is expected to increase by more than 5 times from 33 mmscmd in FY11 to 178

mmscmd in FY15.

No regulatory threat to regas tariffs: Petronet LNG is perhaps the only player in the

oil & gas industry whose margins / pricing / returns are not subject to any regulations.

The company has reported ROEs in the range of 25-30% historically. This has

created a concern that the regulator may bring LNG terminals and regas tariffs into

its ambit. However, since the regasification tariff accounts for a small portion of the

delivered price, controlling the tariff may not result in any meaningful relief to

regasified liquefied natural gas (RLNG) customers.

First mover advantage at Dahej Terminal: The Dahej terminal is located in Gujarat,

which accounts for 1/3rd of the total gas consumption of India. Gujarat is home to

various refineries, petrochemical, fertilizer & power plants which account for the lion’s

share of R-LNG consumption. The 10 mmtpa LNG terminal at Dahej will continue to

be the base of Petronet LNG’s operations going forward due to its optimal location,

low capital cost translating into competitive regas tariffs and tying up of 75% of its

capacity at favorable long term contracts.

Valuation and Outlook

Demand for natural gas is expected to remain robust in India and domestic supply of

natural gas fails to meet the shortfall, which will boost business prospects for Petronet

LNG. With growing volumes and increasing revenue visibility through capacity

expansions at Dahej and new capacities coming up at Kochi makes Petronet LNG as an

attractive long term investment opportunity. As per the consensus estimates, Petronet

LNG is trading at 12.05x FY12E EPS of `13.0 and `11.85x FY13E EPS of `13.23.

Keynote Capitals Research 6

8. K E Y N O T E

Polaris Financial Technology Ltd.

Polaris FT was founded in 1993. It provides software services and solutions to

Key Stock Data

multinational clients. The Company provides its services to companies in the banking and

Sector IT financial industry, which specialize in retail banking, credit cards, insurance, risk

CMP `137.80 management, investment banking and a variety of telecom related activities. It is chosen

52wk High/Low 214/113 outsourcing partner for 9 of the top 10 global banks and 7 of the 10 top global insurance

Market Cap `1369Cr companies. It is world's first CMMi (Capability Maturity Model Integrated) level 5 certified

($268mn) Company.

6m Avg. daily vol 64829

Revised guidance upward:- Polaris’s management has increased its revenues

BSE Sensex 16154.62

guidance for FY12E at `2014Cr –`2060Cr from `1968Cr – `2014Cr backed by robust

volume growth and strong performance of Intellect. The EPS guidance is revised to

Reco. ‘Buy’ `22.65 – `23.47 from `21.95 – `22.35.

Excellent numbers for the Q2FY12:- The Company has registered strong numbers

BSE Code 532254

for the quarter ending September 2011. The company has crossed `500Cr as

NSE Code POLARIS

revenues in the September quarter ended. A sharp rise of 35% in the consolidated

Face Value `5

revenues to `523.12Cr in Q2FY12 as compared with `387.95Cr in the same quarter

last year. Operating profit moved up to `75.54Cr as compared to `60.24Cr Y-o-Y

basis. Similarly revenues contribution from Top 5 clients increased to 43.03% against

Shareholding pattern (30th

Sep, 2011) 40.81% in the same quarter last year.

Geography-wise revenues contribution:- The company received more than 67%

revenues from US and Europe. The highest revenues come from US (45.43%) as

Prom compared to Europe (22.40%). Revenues contribution from Offshore stood at 59.15%

Other oters

s 29% in Q2FY12 as compared to 56.68% Y-o-Y. It will have positive impact on companies

36%

bottom-line.

Key Financials (`Cr)

DII FII

11% 24% Particulars FY07 FY08 FY09 FY10 FY11

Total Sales 1032.4 1099.3 1377.9 1353.8 1586.3

Y-o-Y Growth % 25.1% 6.5% 25.3% -1.8% 17.2%

Price Performance (%) Total Expenditure 871.8 981.1 1144.4 1131.7 1372.4

1 Mth 3 Mths 6 Mths 1 Yr EBITDA 160.6 118.2 233.5 222.0 213.9

9.9% 7.8% -24.6% -15.8% Y-o-Y Growth % 110.4% -26.4% 97.6% -4.9% -3.7%

Depreciation 48.1 46.0 50.5 35.0 33.7

Stock Price Performance

EBIT 112.5 72.2 183.0 187.0 180.2

Close Price Sensex Other income 9.3 18.1 -31.6 -7.3 59.1

Bse IT Interest paid 0.8 0.8 0.7 0.9 1.1

115

PBT 121.0 89.5 150.7 178.8 238.2

105

Tax 19.9 16.1 20.9 25.5 35.9

95 PAT 101.1 73.4 129.8 153.3 202.3

85 Y-o-Y Growth % 374.3% -27.4% 76.9% 18.1% 32.0%

75 NPAT & Minority 101.2 73.2 130.7 152.8 202.5

EPS(`) 10.2 7.4 13.2 15.4 20.4

65

EBITDA Margin 15.6% 10.8% 16.9% 16.4% 13.5%

55

PAT Margin 9.8% 6.7% 9.4% 11.3% 12.8%

PE 14.7 11.0 8.1 11.2 6.8

Source: Keynote Capitals Research

7 Keynote Capitals Research

9. K E Y N O T E

12 Intellect wins across banking and insurance verticals: - Intellect (The flagship

product of company) suite is a set of most comprehensive pack of solutions designed for

the Corporate, Retail and Investment Banking segments. Intellect is a service-enabled,

component-based core banking system. Polaris is assessed at CMMI Level 5

certification offering highly repeatable, continuous-improvement processes. Intellect

revenues contributed `139.28Cr in the Q2FY12, representing 27.32% of its revenues;

witnessing a jump of 68% y-o-y. Services revenues contributed 72.68% at `370.46Cr to

the revenues; representing a growth of 21% on y-o-y basis. Polaris has recorded 12

intellect wins across banking and insurance verticals during the quarter.

Revenues split by Products and Services `Cr

Particulars Q2FY11 Q1FY12 Q2FY12

Product Revenues 83.0 105.2 139.3

Services Revenues 305.3 344.9 370.5

Source: Company

Quarterly performance `Cr

Particulars Q2FY11 Q3FY11 Q4FY11 Q1FY12 Q2FY12

Total Sales 388.0 411.4 443.0 455.8 523.1

Q-o-Q Growth % 5.0% 6.1% 7.7% 2.9% 14.8%

Total Expenditure 327.7 347.5 384.8 392.3 447.6

EBITDA 60.2 63.9 58.2 63.5 75.5

Q-o-Q Growth % 5.7% 6.1% -9.0% 9.2% 19.0%

Depreciation 8.4 8.7 8.7 9.6 11.2

EBIT 51.8 55.2 49.5 53.9 64.4

Other income 5.4 5.3 17.5 8.0 8.9

Interest paid 0.3 0.3 0.4 0.5 0.6

PBT 56.9 60.2 66.6 61.5 72.7

Tax 9.0 10.1 9.0 16.9 18.9

PAT 47.9 50.2 57.7 44.5 53.8

Q-o-Q Growth % 3.0% 4.7% 15.0% -22.8% 20.9%

Source: Company

Valuation

At current market price of `137.80 stock is trading at 6.8x FY11 and 6.3x Q2FY12 (TTM)

earnings. Which is low as compared its industry PE of 14.3x (From Bloomberg). The

management of Polaris has revised the revenue guidance upward and increasing deal

sizes will lead to outperform going forward. Similarly Rupee depreciated against the

Dollar, which will have positive impact on the company’s EBITDA margin.

Keynote Capitals Research 8

10. K E Y N O T E

Tata Sponge Iron Ltd.

Tata Sponge, which has its manufacturing facility at Bilaipada (in Joda Block of

Key Stock Data

Keonjhar District in Orissa), was initially set up as a joint venture company between

Sector Metals Tata Steel and the Industrial Promotion and Investment Corporation of Orissa Limited

CMP `254.7 (IPICOL). It has a production capacity of 390000tpa of sponge iron. The company has

52wk High/Low 379.0/232.6 also set up 26MW of captive power plants to gain from the waste hot gases released

Market Cap `389.77Cr from its kilns in phases.

($74.9mn)

High Dividend yield: Over the last several years company has consistently paid

6m Avg. daily vol 5235

dividend more than 40% of face value. Last year company paid dividend of Rs8 per

BSE Sensex 16154.6

share translation dividend yield of 2.33%. Average dividend yield for the last 5 years is

Reco ‘Buy’ 2.8% which is reasonably good.

BSE Code 513010 Debt free: The Company is totally debt free and therefore higher cost of capital will not

NSE Code TATASPONGE affect the company’s performance.

Face Value `10

Lower production and sales volume muted by higher realization: Despite

Shareholding pattern (30 th significantly lower production and sales volumes, strong sponge iron realizations are

Sept, 2011) supporting both revenue and margins. Sponge Iron production was significantly lower

in H1FY12 to 143K tons from 193K tons on account of disruption in iron ore supply due

to mining ban in Karnataka and regulatory rigor in the Barbil region has affected supply

of iron ore to the industry. Current sponge iron prices are at a 3-year high in the

Othe Prom domestic market and are expected to be elevated till the ban is not taken back.

rs oters Currently, price of the sponge iron is `24000 per ton as compared to `17200 per ton

42.3 43.7

% during same period previous year.

%

Key Financials (`Cr)

DIIs FIIs

7.3% 6.8% Particulars FY07 FY08 FY09 FY10 FY11

Price Performance (%) Total Income 296.83 480.04 628.28 541.94 694.87

1 Mth 3 Mths 6 Mths 1 Yr Growth (%) 45.2% 61.7% 30.9% -13.7% 28.2%

4.6% 18.5% 19.7% 2.6% Total Expenditure 245.04 311.92 424.16 396.09 526.07

PBIDT 51.79 168.12 204.12 145.85 168.8

Stock Price Performance

Growth (%) 23.5% 224.6% 21.4% -28.5% 15.7%

110%

Interest 5.36 12.03 4.64 0.25 0

100%

PBDT 46.43 156.09 199.48 145.6 168.8

90%

Depreciation 13.49 19.65 18.31 19.38 18.52

80% Tax 2.91 19.48 60.5 46.08 55.6

70% Fringe Benefit Tax 0.2 0.31 0 0.02 0

60% Deferred Tax 8.6 21.12 0 -4.4 -6.66

50% Reported PAT 21.23 95.53 120.67 84.52 101.34

Jan‐11

Mar‐11

May‐11

Sep‐11

Nov‐11

Jan‐12

Jul‐11

Extra-ordinary Items 5.37 3.17 0 0 0

Adj PAT Extra-ordinary item 15.86 92.36 120.67 84.52 101.34

Tata Sponge Metals Growth (%) -28.4% 482.3% 30.7% -30.0% 19.9%

Sensex Source: Company & Keynote Capitals Research

9 Keynote Capitals Research

11. K E Y N O T E

Quarterly performance(`Cr)

Net sales grew 19% Q-o-Q (down 1% Y-o-Y) to `174Cr while realizations increased

23% Q-o-Q to `22397 per ton.

EBITDA decreased 10% Q-o-Q (13% Y-o-Y) to `29.9Cr while EBITDA/ton declined

8% Q-o-Q to `4206.

Radhikapur (East) coal block is on track. Coal production is likely to start in 2013.

`Cr

Particulars Q2FY11 Q3FY11 Q4FY11 Q1FY12 Q2FY12

Net Sales 175.3 168.38 191.64 138.09 168.02

Other Income 3.8 2.89 4.14 4.48 6.22

Other Operating Income 0.09 2.01 3.8 7.6 5.7

Total Income 179.19 173.28 199.58 150.17 179.94

Total Expenditure 159.74 135.53 131.51 112.6 143.86

PBIDT 19.45 37.75 68.07 37.57 36.08

Interest 0 0 0 0 0.06

PBDT 19.45 37.75 68.07 37.57 36.02

Depreciation 4.64 4.64 4.52 4.56 4.62

PBT 14.81 33.11 63.55 33.01 31.4

Tax 4.4 10.91 20.72 10.49 9.67

Reported Profit After Tax 10.41 22.2 42.83 22.52 21.73

EPS (`) 6.76 14.42 27.81 14.62 14.11

PBIDT Margins (%) 11.1% 22.4% 35.5% 27.2% 21.5%

PBDT Margins (%) 11.1% 22.4% 35.5% 27.2% 21.4%

PAT Margins (%) 5.9% 13.2% 22.3% 16.3% 12.9%

TTM Profit & Loss A/C `Cr

Particulars TTM Q208 TTM Q209 TTM Q210 TTM Q211

Net Sales 603.54 492.84 606.09 666.13

Other Income 10.27 9.98 7.96 17.73

Other Operating Income 6.26 9.93 10.84 19.11

Total Income 620.07 512.75 624.89 702.97

Total Expenditure 364.7 415.84 472.23 523.5

PBIDT 255.37 96.91 152.66 179.47

Interest 8.43 1.5 0.25 0.06

PBDT 246.94 95.41 152.41 179.41

Depreciation 17.89 19.2 19.02 18.34

PBT 229.05 76.21 133.39 161.07

Tax 65.75 26.83 43.4 51.79

Reported Profit After Tax 163.3 49.38 89.99 109.28

EPS (`) 106.04 32.06 58.44 70.96

PBIDT Margins (%) 41.2% 18.9% 24.4% 25.5%

PBDT Margins (%) 39.8% 18.6% 24.4% 25.5%

PAT Margins (%) 26.3% 9.6% 14.4% 15.5%

Source: Company & Keynote Capitals Research

Valuations: We expect sponge iron production to be significantly lower due to iron supply

issues. However, this has been factored and the stock is available at the attractive

valuations. At CMP of `254.7, company trades at the TTM PE multiple of 3.59x and P/BV

multiple of 0.71x which are very low as compare to the industry peers of 10.9x and 1.68x

respectively.

Keynote Capitals Research 10

12. K E Y N O T E

KEYNOTE CAPITALS LTD.

Member

Stock Exchange, Mumbai (INB 010930556)

National Stock Exchange of India Ltd. (INB 230930539)

Over the Counter Exchange of India Ltd. (INB 200930535)

Central Depository Services Ltd. (IN-DP-CDSL-152-2001)

4th Floor, Balmer Lawrie Building, 5, J. N. Heredia Marg, Ballard Estate, Mumbai 400 001. INDIA

Tel. : 9122-2269 4322 / 24 / 25 • www.keynotecapitals.com

DISCLAIMER

• This report has been prepared and issued by Keynote Capitals Limited, based solely on public information and sources believed to be reliable.

• Neither the information nor any opinion expressed herein, constitutes an offer, or an invitation to make an offer, to buy or sell any securities or any

options, futures or other derivatives related to such securities and also for the purpose of trading activities.

• Keynote Capitals Limited makes no guarantee, representation or warranty, express or implied and accepts no responsibility or liability as to the

accuracy or completeness or correctness of the information in this report.

• Keynote Capitals and its affiliates and their respective officers, directors and employees may hold positions in any securities mentioned in this

Report (or in any related investment) and may from time to time add to or dispose of any securities or investments.

• Keynote Capitals may also have proprietary trading positions in securities covered in this report or in related instruments.

• An affiliate of Keynote Capitals Limited may also perform or seek to perform broking, investment banking and other banking services for the

company under coverage.

• If ‘Buy’, ‘Sell’, or ‘Hold’ recommendation is made in this Report, such recommendation or view or opinion expressed on investments in this Report

is not intended to constitute investment advice and should not be intended or treated as a substitute for necessary review or validation or any

professional advice. The views expressed in this Report are those of the analyst which are subject to change and do not represent to be an authority

on the subject. Keynote Capitals may or may not subscribe to any and/ or all the views expressed herein.

• The opinions presented herein are liable to change without any notice.

• Though due care has been taken in the preparation of this report, Keynote Capitals limited or any of its directors, officers or employees shall be in

any way be responsible for any loss arising from the use thereof.

• Investors are advised to apply their judgment before acting on the contents of this report.

• This report or any portion hereof may not be reprinted, sold or redistributed without the written consent of Keynote Capitals Limited.

Keynote Capitals Research