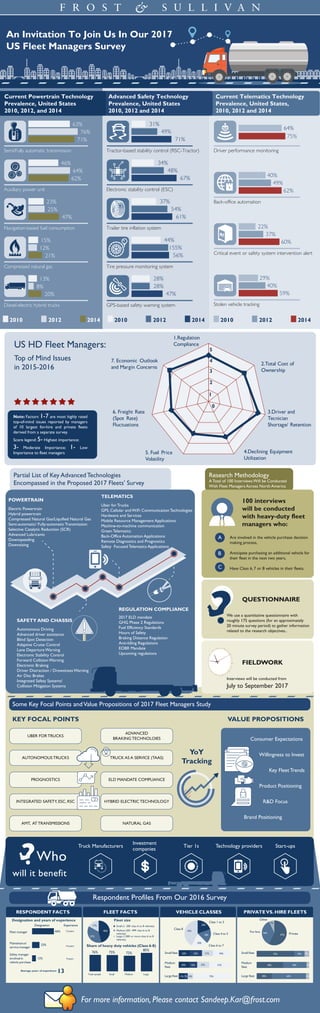

The document summarizes key findings from surveys of US heavy-duty fleet managers conducted in 2010, 2012, and 2014 regarding adoption of advanced vehicle technologies. It also outlines plans to survey 100 fleet managers in 2017 on topics like powertrains, safety, telematics, regulations, and issues of top concern. The 2017 survey aims to gather insights on purchasing decisions, regulations, and technology focus areas from managers of private and for-hire fleets of Class 6-8 vehicles.

Call Girls Hongasandra Just Call 👗 7737669865 👗 Top Class Call Girl Service B...

Frost and Sullivan's 2017 US HD Fleet Managers Survey

1. 31%

49%

71%

Tractor-based stability control (RSC-Tractor)

Advanced Safety Technology

Prevalence, United States

2010, 2012 and 2014

Electronic stability control (ESC)

67%

48%

34%

Trailer tire inflation system

Tire pressure monitoring system

GPS-based safety warning system

61%

47%

54%

28%

37%

28%

63%

76%

71%

Semi/Fully automatic transmission

Current Powertrain Technology

Prevalence, United States

2010, 2012, and 2014

Auxiliary power unit

62%

64%

46%

Navigation-based fuel consumption

Compressed natural gas

Diesel-electric hybrid trucks

47%

21%

20%

25%

12%

8%

23%

15%

13%

56%

155%

44%

Current Telematics Technology

Prevalence, United States,

2010, 2012 and 2014

64%

75%

Driver performance monitoring

Back-office automation

62%

49%

40%

Critical event or safety system intervention alert

60%

37%

22%

Stolen vehicle tracking

59%

40%

29%

Partial List of Key Advanced Technologies

Encompassed in the Proposed 2017 Fleets' Survey

KEY FOCAL POINTS VALUE PROPOSITIONS

Research Methodology

A Total of 100 Interviews Will be Conducted

With Fleet Managers Across North America

POWERTRAIN

TELEMATICS

Autonomous Driving

Advanced driver assistance

Blind Spot Detection

Adaptive Cruise Control

Lane Departure Warning

Electronic Stability Control

Forward Collision Warning

Electronic Braking

Driver Distraction / Drowsiness Warning

Air Disc Brakes

Integrated Safety Systems/

Collision Mitigation Systems

Are involved in the vehicle purchase decision

making process,

Anticipate purchasing an additional vehicle for

their fleet in the next two years,

Have Class 6, 7 or 8 vehicles in their fleets.

We use a quantitative questionnaire with

roughly 175 questions (for an approximately

20 minute survey period) to gather information

related to the research objectives..

Interviews will be conducted from

July to September 2017

Truck Manufacturers Tier 1s Start-ups

Investment

companies

UBER FOR TRUCKS

ADVANCED

BRAKING TECHNOLOIES Consumer Expectations

Willingness to Invest

Key Fleet Trends

Product Positioning

R&D Focus

Brand Positioning

YoY

Tracking

AUTONOMOUS TRUCKS TRUCK AS A SERVICE (TAAS)

PROGNOSTICS ELD MANDATE COMPLIANCE

INTEGRATED SAFETY, ESC, RSC

NATURAL GAS

HYBRID ELECTRIC TECHNOLOGY

AMT, AT TRANSMISSIONS

Technology providers

SAFETY AND CHASSIS

REGULATION COMPLIANCE

2017 ELD mandate

GHG Phase 2 Regulations

Fuel Efficiency Standards

Hours of Safety

Braking Distance Regulation

Anti-Idling Regulations

EOBR Mandate

Upcoming regulations

Electric Powertrain

Hybrid powertrain

Compressed Natural Gas/Liquified Natural Gas

Semi-automatic/ Fully-automatic Transmission

Selective Catalytic Reduction (SCR)

Advanced Lubricants

Downspeeding

Downsizing

Uber for Trucks

GPS, Cellular and WiFi Communication Technologies

Hardware and Services

Mobile Resource Management Applications

Machine-to-machine communication

Green Telematics

Back-Office Automation Applications

Remote Diagnostics and Prognostics

Safety Focused Telematics Applications

A

B

C

100 interviews

will be conducted

with heavy-duty fleet

managers who:

QUESTIONNAIRE

FIELDWORK

VEHICLE CLASSES PRIVATEVS.HIRE FLEETS

20%

18%

20%

43%

57%

36%

7%Class 1 to 3

Class 4 to 5

Class 6 to 7

Class 8

Private

For hire

Other

Small fleet

Medium

fleet

Large fleet

22%

20%

11%

23%

16%

7%

21%

23%

10%

34%

41%

73%

Small fleet

Medium

fleet

Large fleet

72%

50%

29%

19%

45%

65%

9%

5%

6%

RESPONDENT FACTS FLEET FACTS

Designation and years of experience

Designation Experience

Fleet manager 13 years

Maintenance/

service manager 14 years

Safety manager

involved in

vehicle purchase

9 years

66%

23%

12%

Average years of experience 13

Fleet size

46%

37%

17% Small (1 -300 class 6 to 8 vehicles)

Medium (301 -999 class 6 to 8

vehicles)

Large (1,000 or more class 6 to 8

vehicles)

Share of heavy duty vehicles (Class 6-8)

76% 75% 72%

85%

Total sample Small Medium Large

Some Key Focal Points andValue Propositions of 2017 Fleet Managers Study

An Invitation To Join Us In Our 2017

US Fleet Managers Survey

Who

will it benefit

Respondent Profiles From Our 2016 Survey

For more information, Please contact Sandeep.Kar@frost.com

US HD Fleet Managers:

Top of Mind Issues

in 2015-2016

Note: Factors 1-7 are most highly rated

top-of-mind issues reported by managers

of 10 largest for-hire and private fleets

derived from a separate survey.

Score legend: 5- Highest importance;

3- Moderate Importance; 1- Low

Importance to fleet managers

0

1

2

3

4

5

1.Regulation

Compliance

2.Total Cost of

Ownership

3.Driver and

Tecnician

Shortage/ Retention

4.Declining Equipment

Utilization

5. Fuel Price

Volatility

6. Freight Rate

(Spot Rate)

Fluctuations

7. Economic Outlook

and Margin Concerns

2010 2012 2014 2010 2012 2014 2010 2012 2014