Costi di Processo: 4.Report della Produzione

•

0 j'aime•277 vues

Costi di processo https://www.manager.it/default.asp?page=A_contabilita.html

Recommandé

Contenu connexe

Tendances

Tendances (16)

Similaire à Costi di Processo: 4.Report della Produzione

Similaire à Costi di Processo: 4.Report della Produzione (19)

Plus de Manager.it

Plus de Manager.it (20)

Dernier

Dernier (20)

Costi di Processo: 4.Report della Produzione

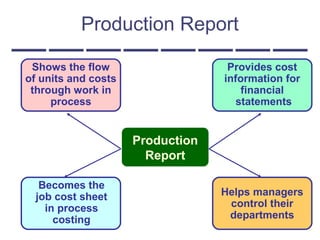

- 1. Production Report Production Report Helps managers control their departments Provides cost information for financial statements Shows the flow of units and costs through work in process Becomes the job cost sheet in process costing

- 2. Production Report A computation of cost per equivalent unit. A computation of cost per equivalent unit. Section 1 Section 2 Section 3 Production Report A quantity schedule showing the flow of units and the computation of equivalent units. A quantity schedule showing the flow of units and the computation of equivalent units.

- 3. Production Report A reconciliation of cost flows for the period, including: Total cost for units completed and transferred from the processing department. Total cost for partially completed units remaining in work in process. A reconciliation of cost flows for the period, including: Total cost for units completed and transferred from the processing department. Total cost for partially completed units remaining in work in process. Section 1 Section 2 Section 3 Production Report

- 4. Double Diamond Skis uses process costing to determine unit costs in its Shaping and Milling Department. Double Diamond uses the weighted average cost procedure. Using the following information for the month of May, let’s prepare a production report for Shaping and Milling. Double Diamond Skis uses process costing to determine unit costs in its Shaping and Milling Department. Double Diamond uses the weighted average cost procedure. Using the following information for the month of May, let’s prepare a production report for Shaping and Milling. Production Report Example

- 5. Work in process, May 1: 200 units Materials: 55% complete. $ 9,600 Conversion: 30% complete. 5,575 Production started during May: 5,000 units Production completed during May: 4,800 units Costs added to production in May Materials cost $ 368,600 Conversion cost 350,900 Work in process, May 31: 400 units Materials 40% complete. Conversion 25% complete. Work in process, May 1: 200 units Materials: 55% complete. $ 9,600 Conversion: 30% complete. 5,575 Production started during May: 5,000 units Production completed during May: 4,800 units Costs added to production in May Materials cost $ 368,600 Conversion cost 350,900 Work in process, May 31: 400 units Materials 40% complete. Conversion 25% complete. Production Report Example

- 6. Section 1: Quantity Schedule with Equivalent Units Production Report Example Units to be accounted for: Work in process, May 1 200 Started into production 5,000 Total units 5,200 Equivalent units Materials Conversion Units accounted for as follows: Completed and transferred 4,800 4,800 4,800 Work in process, May 31 400

- 7. Production Report Example Units to be accounted for: Work in process, May 1 200 Started into production 5,000 Total units 5,200 Equivalent units Materials Conversion Units accounted for as follows: Completed and transferred 4,800 4,800 4,800 Work in process, May 31 400 Materials 40% complete 160 5,200 4,960 Section 1: Quantity Schedule with Equivalent Units

- 8. Production Report Example Units to be accounted for: Work in process, May 1 200 Started into production 5,000 Total units 5,200 Equivalent units Materials Conversion Units accounted for as follows: Completed and transferred 4,800 4,800 4,800 Work in process, May 31 400 Materials 40% complete 160 Conversion 25% complete 100 5,200 4,960 4,900 Section 1: Quantity Schedule with Equivalent Units

- 9. Section 2: Compute cost per equivalent unit Production Report Example Total Cost Materials Conversion Cost to be accounted for: Work in process, May 1 15,175$ 9,600$ 5,575$ Costs added in the Shipping and Milling Department 719,500 368,600 350,900 Total cost 734,675$ 378,200$ 356,475$ Equivalent units 4,960 4,900 Cost per equivalent unit

- 10. Total Cost Materials Conversion Cost to be accounted for: Work in process, May 1 15,175$ 9,600$ 5,575$ Costs added in the Shipping and Milling Department 719,500 368,600 350,900 Total cost 734,675$ 378,200$ 356,475$ Equivalent units 4,960 4,900 Cost per equivalent unit 76.25$ Production Report Example Section 2: Compute cost per equivalent unit $378,200 ÷ 4,960 units = $76.25

- 11. Total Cost Materials Conversion Cost to be accounted for: Work in process, May 1 15,175$ 9,600$ 5,575$ Costs added in the Shipping and Milling Department 719,500 368,600 350,900 Total cost 734,675$ 378,200$ 356,475$ Equivalent units 4,960 4,900 Cost per equivalent unit 76.25$ 72.75$ Total cost per equivalent unit = $76.25 + $72.75 = $149.00 Production Report Example $356,475 ÷ 4,900 units = $72.75 Section 2: Compute cost per equivalent unit

- 12. Section 3: Cost Reconciliation Production Report Example Total Equivalent Units Cost Materials Conversion Cost accounted for as follows: Transferred out during May 4,800 4,800 Work in process, May 31: Materials 160 Conversion 100 Total work in process, May 31 Total cost accounted for

- 13. Total Equivalent Units Cost Materials Conversion Cost accounted for as follows: Transferred out during May 715,200$ 4,800 4,800 Work in process, May 31: Materials 160 Conversion 100 Total work in process, May 31 Total cost accounted for 4,800 units @ $149.00 Production Report Example Section 3: Cost Reconciliation

- 14. Total Equivalent Units Cost Materials Conversion Cost accounted for as follows: Transferred out during May 715,200$ 4,800 4,800 Work in process, May 31: Materials 12,200 160 Conversion 7,275 100 Total work in process, May 31 19,475 Total cost accounted for 734,675$ 160 units @ $76.25 Production Report Example Section 3: Cost Reconciliation All costs accounted for 100 units @ $72.75