Observatorio europeo de salidas a bolsa 2T 2015

•

0 j'aime•441 vues

Nuestro último Observatorio Europeo de Salidas a Bolsa muestras datos sobra las salidas a bolsa del segundo trimestre del año.

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (19)

En vedette

En vedette (13)

Similaire à Observatorio europeo de salidas a bolsa 2T 2015

Similaire à Observatorio europeo de salidas a bolsa 2T 2015 (20)

Plus de PwC España

Plus de PwC España (20)

Dernier

Dernier (20)

Observatorio europeo de salidas a bolsa 2T 2015

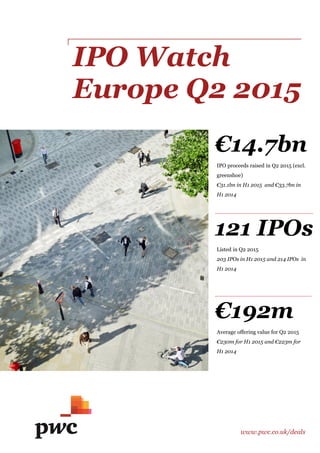

- 1. IPO Watch Europe Q2 2015 www.pwc.co.uk/deals €14.7bn IPO proceeds raised in Q2 2015 (excl. greenshoe) €31.1bn in H1 2015 and €33.7bn in H1 2014 121 IPOs Listed in Q2 2015 203 IPOs in H1 2015 and 214 IPOs in H1 2014 €192m Average offering value for Q2 2015 €230m for H1 2015 and €223m for H1 2014

- 2. 2IPO Watch Europe Survey Q2 2015 | European IPO trends 3 Market volatility and performance 5 Pricing and performance of top 5 European IPOs 6 Top 10 IPOs in Europe 7 Exchange activity by value 8 Exchange activity by volume 9 IPOs by sector 10 UK focus Overview 11 Relative performance of London IPOs 12 Private equity and industry trends 13 US and Hong Kong domestic activity 14 Appendix – IPOs by market 15 Contacts / About IPO Watch Europe 16 Contents Outlook for second half 2015: • Following the Greek No vote, global markets have showed increasing signs of tension albeit without wide-spread panic. We believe July will be key in assessing the extent of the contagion risk and receptiveness of Europe’s markets to the pipeline of IPO candidates. • Barring these factors, the trends observed in the first part of 2015 will continue and we expect continued IPO activity in the second part of the year: - PE driven activity will continue, though at a slower pace as IPO exits compete with trade sales - A number of spin-offs from large listed companies have already been announced, especially in the financial sector - Privatisation programmes will also contribute sizable IPOs throughout Europe, including Italy, Netherlands and Poland • There are other headwinds likely to impact Europe’s markets with volatility likely to be a recurring feature of the coming months, due to the uncertainty on US interest rates and the renewed concerns over the Chinese economy.

- 3. 3IPO Watch Europe Survey Q2 2015 | European IPO trends €14.7bn raised in Q2 2015, down 34% on Q2 2014 following the surge in activity across Europe last year Figure 1: Quarterly European IPO activity by value and volume H1 2014 Q1 2015 Q2 2015 H1 2015 Total European listings comprise those with: Less than $5m raised 53 17 41 58 Greater than $5m raised 161 65 80 145 Total number of listings 214 82 121 203 Money raised excl. greenshoe (€m) 33,730 16,375 14,724 31,099 Exercised greenshoe (€m) 2,157 1,611 699 2,310 Total money raised (€m) 35,887 17,986 15.423 33,409 Average offering value (€m)* 223 276 192 230 * Average offering value has been calculated based on total offering value including greenshoe excluding listings raising less than $5m “We enter a period of uncertainty following the Greek referendum and wider concerns in the US and China may give rise to market turbulence and volatility. In this environment, a number of IPO plans may be derailed or postponed and in the short term we expect the summer holiday months to be relatively quiet. The pipeline for the second half of the year looks solid and we expect IPO activity to pick up towards the end of the third quarter.” Mark Hughes Partner in the UK Capital Markets Group

- 4. 4IPO Watch Europe Survey Q2 2015 | European IPO trends Strong activity levels in both quarters resulted in a good H1 2015, slightly below H1 2014 but far ahead of the five previous years Figure 2: European IPO activity (H1 and full year) since 2007* Figure 3: Quarterly European IPO activity since 2012 VolumeofIPOsVolumeofIPOs 2.4 0.8 0.4 7.7 3.3 5.4 3.0 14.8 11.4 22.3 6.6 9.2 16.4 14.7 61 93 60 74 45 76 52 106 68 145 76 86 82 121 - 20 40 60 80 100 120 140 160 - 5 10 15 20 25 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 ValueofIPOs(€bn) Value €bn Greenshoe €bn IPOs *Excludes greenshoe. Note: Excludes IPOs on Borsa Istanbul, Zagreb Stock Exchange and Bucharest Stock exchange pre 2011 80.5 14.0 7.1 26.3 27.1 11.3 26.5 49.5 31.1 819 295 126 380 459 288 279 375 203 0 100 200 300 400 500 600 700 800 900 - 10 20 30 40 50 60 70 80 90 2007 2008 2009 2010 2011 2012 2013 2014 2015 H1 ValueofIPOs(€bn) H1 value €bn FY value €bn IPOs 2012 2013 2014 2015

- 5. 5IPO Watch Europe Survey Q2 2015 | Market volatility and performance Volatility index has increased significantly towards the end of the quarter reflecting increasing uncertainty over Greece Figure 4: Volatility compared to IPO proceeds Figure 5: Historical performance of major market indices since January 2014 Turmoil in emerging markets Moneyraised€bn VSTOXXindex Money raised €bn VSTOXX index -10% 0% 10% 20% 30% 40% Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun %changesince1Jan2014 DAX 30 CAC 40 FTSE 100 Source: Thomson Reuters as at 30 June 2015 IPO of ISS, Pets at Home and Poundland IPO of AA, B&M and Euronext 2014 2015 IPO of NN, FinecoBank and SSP Declining oil price 2014 2015 QE by ECB IPO of Sunrise, Aena, Elis and GrandVision Greece uncer- tainty 0 2 4 6 8 10 12 14 16 Jan Feb Mar Apr May Jun July Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun 0 5 10 15 20 25 30

- 6. 6IPO Watch Europe Survey Q2 2015 | Pricing and performance of top 5 European IPOs The top 5 IPOs have all outperformed their respective indices Figure 6: Top five IPOs in Q2 2015 Figure 7: Offer price versus initial price range of top five IPOs Cellnex Telecom Woodford Patient Capital Trust Spie Europcar INWIT Exchange BME London Euronext Paris Euronext Paris Borsa Italiana IPO date 7 May 21 April 9 June 26 May 22 June PE backed No No Yes Yes No Money raised (€m) incl. greenshoe 2,141 1,108 939 879 796 Price range €12.00 - €14.00 £1.00 €14.50 - €17.50 €11.50 - €15.00 €3.25 - €3.90 -20% -10% 0% 10% 20% 30% Offer price Price range Figure 8: Performance of top five IPOs Share performance from IPO to 30 Jun 2015 (%) 8.4% -3.5% 13.5% -6.2% 8.2% -1.4% -1.4% -6.4% 11.0% -1.1% Domestic index performance from IPO to 30 Jun 2015 (%) Cellnex Telecom Woodford Patient Capital Trust Spie Europcar INWIT Cellnex Telecom Woodford Patient Capital Trust Spie Europcar INWIT Offer price

- 7. 7IPO Watch Europe Survey Q2 2015 | Ten largest IPOs in Q2 2015 €m (excl. greenshoe) €m (incl. greenshoe) Sector Market Country of origin PE backed Cellnex Telecom 1,946 2,141 Telecommunications BME Spain No Woodford Patient Capital Trust 1,108 1,108 Financials London United Kingdom No Spie 939 939 Industrials Euronext France Yes Europcar Groupe 879 879 Consumer Services Euronext France Yes INWIT 796 796 Telecommunications Borsa Italiana Italy No Pandox 601 601 Financials OMX Sweden No Patentes Talgo 570 570 Industrials BME Spain Yes Sophos Group 495 495 Technology London United Kingdom Yes Cairn Homes 400 440 Consumer Goods London Ireland No Europris 431 431 Consumer Services Oslo Norway Yes Total 8,165 8,641 Ten largest IPOs in Q1 2015 €m (excl. greenshoe) €m (incl. greenshoe) Sector Market Country of origin PE backed Aena 3,875 4,263 Industrials BME Spain No Auto Trader 1,937 2,228 Consumer Services London United Kingdom Yes Sunrise Communications 1,882 2,148 Telecommunications SIX Swiss Switzerland Yes GrandVision 1,020 1,116 Health Care Euronext Netherlands Yes Elis 750 854 Industrials Euronext France Yes Refresco Gerber 548 563 Consumer Goods Euronext Netherlands Yes Tele Columbus 477 510 Technology Deutsche Börse Germany No OVS 414 446 Consumer Goods Borsa Italiana Italy Yes Saeta Yield 435 442 Utilities BME Spain No Wizz Air Holdings 364 419 Consumer Services London Hungary Yes Total 11,702 12,989 Top 10 IPOs in Europe Spain hosted the largest IPO in both quarters so far in 2015 Figure 13: Top ten IPOs Other Top 10 IPOs 45% 55% Figure 12: Top ten IPOs (value) in Q2 2015 “The weather is warm and the window is certainly open in Madrid. A strong start to the year with the Aena IPO has been quickly followed up in Q2, with Cellnex and Patentes Talgo standing out in terms of capital raised, with Euskatel successfully completing its IPO on 1 July. Entering the traditionally quieter summer period, we reflect upon what has been a fantastic year to date for the Spanish IPO market, far surpassing 2014 total proceeds already. With the improving economic indicators, we are hopeful of more positive news to follow for 2015, but also note the elections in November are likely to result in a slower end to the year.” Rocio Fernandez Funcia Partner in the Spanish Capital Markets Group

- 8. 8IPO Watch Europe Survey Q2 2015 | Stock exchange offering value (€m) H1 2014 Q1 2015 Q2 2015 H1 2015 London Stock Exchange 15,867 4,648 4,697 9,345 BME (Spanish Exchange) 3,631 4,310 2,593 6,903 Euronext 6,570 2,637 2,267 4,904 Euronext Paris 4,077 909 1,999 2,908 Euronext Amsterdam 1,767 1,696 - 1,696 Euronext Brussels 596 32 268 300 Euronext Lisbon 130 - - - NASDAQ OMX 3,279 1,416 2,447 3,863 OMX Stockholm 1,714 1,040 2,268 3,308 OMX Helsinki 105 208 114 322 OMX Copenhagen 1,460 168 - 168 OMX Iceland - - 65 65 OMX Vilnius - - - - OMX Talinn - - - - SIX Swiss Exchange 1,073 1,882 - 1,882 Borsa Italiana 1,226 490 993 1,483 Deutsche Börse 857 573 728 1,301 Oslo Børs & Oslo Axess 386 57 587 644 Irish Stock Exchange 483 302 92 394 Warsaw Stock Exchange 107 8 313 321 Zagreb Stock Exchange - 36 - 36 Borsa Istanbul 43 16 7 23 Bucharest Stock Exchange - - - - Wiener Börse 194 - - - Prague Stock Exchange 14 - - - Total 33,730 16,375 14,724 31,099 Figure 10: Top five stock exchanges in Europe in Q2 2015 Figure 9: IPO offering value by stock exchange* *Excludes greenshoe **Excludes listings raising less than $5m BME 5 IPOs raised * €2.6bn Average IPO proceeds ** €712m Largest IPO: Cellnex Telecom €1,946m (€2,141m incl. greenshoe) OMX 37 IPOs raised * €2.4bn Average IPO proceeds ** €121m Largest IPO: Pandox €601m (€691m incl. greenshoe) Euronext 13 IPO raised * €2.3bn Average IPO proceeds ** €239m Spie €939m (€1,033m incl. greenshoe) Borsa Italiana 7 IPOs raised * €1.0bn Average IPO proceeds ** €165m Largest IPO: INWIT €796m (no greenshoe exercised) Exchange activity by value London retained its leading position in H1 2015, however proceeds in Spain almost doubled compared to H1 2014 LSE 28 IPOs raised * €4.7bn Average IPO proceeds ** €200m Largest IPO: Woodford Patient Capital Trust €1,108m (no greenshoe exercised)

- 9. 9IPO Watch Europe Survey Q2 2015 | Exchange activity by volume OMX saw more activity in Q2 2015 than the whole of H1 2014, representing over a quarter of all European Q2 IPOs by volume “After a few quiet years, a positive trend of IPOs on the Italian Stock Exchange began in mid 2014 and has continued through the first half of 2015. The ECB liquidity injection has improved the performance of the Italian equity markets, reducing volatility and improving conditions for companies entering the capital markets for the first time. There is a robust pipeline of Italian corporate and public service entities seeking out an IPO, most of which are monitoring the developments in Greece in order to plan the right time to approach the markets.“ Christian Alessandrini Partner in the Italian Capital Markets Group Figure 11: IPO volume by stock exchange Stock exchange offering volume H1 2014 Q1 2015 Q2 2015 H1 2015 London Stock Exchange 86 27 28 55 NASDAQ OMX 33 18 37 55 OMX Stockholm 27 14 30 44 OMX Helsinki 4 3 3 6 OMX Iceland - - 2 2 OMX Vilnius - - 1 1 OMX Talinn - - 1 1 OMX Copenhagen 2 1 - 1 Euronext 28 13 13 26 Euronext Paris 24 9 10 19 Euronext Brussels 1 1 3 4 Euronext Amsterdam 2 3 - 3 Euronext Lisbon 1 - - - Warsaw Stock Exchange 16 2 16 18 Borsa Italiana 12 6 7 13 Deutsche Börse 7 3 7 10 BME (Spanish Exchange) 6 3 5 8 Oslo Børs & Oslo Axess 7 1 5 6 Borsa Istanbul 8 3 1 4 Bucharest Stock Exchange - 2 - 2 SIX Swiss Exchange 5 1 1 2 Irish Stock Exchange 3 1 1 2 Zagreb Stock Exchange - 2 - 2 Wiener Börse 2 - - - Prague Stock Exchange 1 - - - Total 214 82 121 203

- 10. 10IPO Watch Europe Survey Q2 2015 | IPOs by sector Financials and Consumer services declined significantly compared to H1 2014, partially offset by growth in Telecom, Industrials and Consumer goods *Excludes greenshoe **Excludes listings raising less than $5m Stock exchange offering value (€m) H1 2014 Q1 2015 Q2 2015 H1 2015 variance vs. H1 2014 Industrials 7,112 5,427 2,967 8,394 1,282 Financials 9,976 2,402 4,480 6,882 (3,094) Consumer Services 10,088 3,138 1,998 5,136 (4,952) Telecommunications 2,160 1,887 2,743 4,630 2,470 Consumer Goods 956 1,131 922 2,053 1,097 Health Care 1,096 1,252 709 1,961 865 Technology 989 664 888 1,552 563 Utilities 27 435 5 440 413 Oil & Gas 776 18 11 29 (747) Basic Materials 550 21 1 22 (528) Total 33,730 16,375 14,724 31,099 (2,631) Figure 14: IPO value by sector* Telecom 3 IPOs raised in Q2 €2,743m * Average IPO proceeds ** €1,371m Largest IPO: Cellnex Telecom €1,946m (€2,141m incl. greenshoe) Industrials 23 IPOs raised in Q2 €2,967m * Average IPO proceeds ** €197m Largest IPO: Spie €939m (€1,033m incl. greenshoe) Financials 36 IPOs raised in Q2 €4,480m * Average IPO proceeds ** €172m Largest IPO: Woodford Patient Capital Trust €1,108m (€1,108m incl. greenshoe) “The second quarter has been good for French IPOs, especially PE-backed ones. All transactions raising more $50m were PE backed over the period, reflecting the renewed confidence in economic conditions in France. Investors are also keen to support innovation with healthcare being the most dynamic industry by number of IPOs. The pipeline remains good, although the uncertainty related to European and international geopolitics might hinder the potential level of activity in the coming months.” Philippe Kubisa Partner in the French Capital Markets Group

- 11. 11IPO Watch Europe Survey Q2 2015 | UK focus – Overview A decrease in average deal size combined with an uptick in trade sales led to lower activity in London compared to the buoyant activity in Q2 2014 Figure 15: London IPO trends – value* Figure 16: London IPO trends - volume Proceeds (incl. greenshoe) €m £m Sector Market Country PE backed Woodford Patient Capital Trust 1,108 800 Financials Main United Kingdom No Sophos Group 495 352 Technology Main United Kingdom Yes Cairn Homes 440 325 Consumer Goods Main Ireland No Toro 330 245 Financials Main United Kingdom No Apax Global Alpha 297 218 Financials Main United Kingdom Yes Figure 17: Five largest UK IPOs of Q2 2015 6 4 1 13 7 8 5 15 13 27 7 6 18 14 8 15 13 13 6 17 20 25 19 27 16 22 9 14 - 10 20 30 40 50 60 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 VolumeofIPOs Main AIM and SFM 0.6 0.2 0.0 3.6 1.8 2.3 1.1 7.0 4.6 9.2 1.3 0.8 4.5 3.7 0.1 0.1 0.4 0.0 0.3 0.6 1.2 1.3 0.8 0.6 0.9 0.1 1.0 - 1 2 3 4 5 6 7 8 9 10 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 ValueofIPOs(€bn) Main AIM and SFM 2012 2013 2014 2015 2012 2013 2014 2015 *Excludes greenshoe “After leading the PE-backed trend for the last two years, US PE driven IPOs started to slow down six months ago and we are seeing a similar trend emerge in the UK. In stark contrast, PE exits across continental Europe remain active - whether this continues into the second half of the year remains to be seen due to the continued uncertainty over Greece.” Viv Maclachlan Director in the UK Capital Markets Group

- 12. 12IPO Watch Europe Survey Q2 2015 | UK focus - Relative performance of London IPOs Figure 18: Share price performance of London IPOs relative to the FTSE all share index, from IPO to 30 Jun 2015 Note: Threshold of $5m proceeds | Relative performance based on the FTSE All Share Index for Main Market and SFM listed companies and FTSE AIM All Share index for AIM listed companies Source: Dealogic and Thomson Reuters as of 30 June 2015 64 54 47 40 38 36 34 29 25 20 20 17 15 13 12 12 12 12 12 12 11 11 10 9 9 9 8 8 8 8 6 6 5 5 5 4 3 3 1 -1 -14 -33 -53 -67 -80% -60% -40% -20% 0% 20% 40% 60% 80% Aldermore Group Stride Gaming Drum Income Plus REIT Wizz Air Integrated Diagnostics Sanne Group Auto Trader Shawbrook Group Eurocell RedX Pharma Woodford Patient Capital Trust Curtis Banks Marshall Motor Holdings John Laing Group Lakehouse Miton UK MicroCap Trust Cairn Homes Elegant Hotels Group DFS Furniture Grand Group Investment Ranger Direct Lending Fund Sequoia Economic Infrastructure Income Fund PureTech Health Amedeo Air Four Plus Apax Global Alpha AEW UK REIT Gateley Holdings Verseon Sophos Group Toro Non-Standard Finance Gabelli Value Plus+ Trust VPC Speciality Lending Investments Revolution Bars Group PTSG Zegona Communications MayAir Group Gear4music Adgorithms Puma VCT 11 ScS Group HSS Hire Group Aquatic Foods Group IronRidge Resources 5companies have underperformed the index 39companies have outperformed the index Main Market AIM and SFM

- 13. 13IPO Watch Europe Survey Q2 2015 | UK focus - Private equity and industry trends * UK IPOs raising over $50m, excludes closed-end funds, SPACs, SPVs, Capital Pool companies, Investment Managers, REITs, Royalty Trusts ** Excludes greenshoe Figure 19: PE-backed vs non PE-backed IPO trends in London* Figure 20: Five largest UK PE-backed IPOs of Q2 2015 Stock exchange offering value (€m) H1 2014 Q1 2015 Q2 2015 H1 2015 Financials 4,253 1,466 2,977 4,443 Consumer Services 8,248 2,758 107 2,865 Industrials 1,493 375 345 720 Consumer Goods 173 12 509 521 Technology 366 4 495 499 Health Care 511 20 264 284 Consumer Services 10 13 - 13 Telecommunications 211 - - - Oil & Gas 602 - - - Utilities - - - - Total 15,867 4,648 4,697 9,345 Figure 21: London IPO value by sector ** - 1 2 3 4 5 6 7 8 9 10 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 ValueofIPOs(€bn) Non PE-backed PE-backed 2012 2013 2014 2015 Proceeds (incl. greenshoe) €m £m Sector Market Country Sophos Group 495 352 Technology London United Kingdom Shawbrook Group 342 250 Financials London United Kingdom Integrated Diagnostics 299 216 Health Care London Egypt Apax Global Alpha 297 218 Financials London United Kingdom Elegant Hotels Group 87 63 Industrials London Barbados - - - - 82% 100% 56% 49% 51% 74% 70% 54% 96% 57% “We are now almost two years into the resurgence of PE-driven IPO activity and the backlog of IPO candidates is now naturally slowing. For some time we have seen a large number of these transactions being run as dual track processes and, as we see private and public valuations converge, trade sales become quite attractive, as essentially they provide a one-time exit to existing shareholders.” James Fillingham Deals Partner

- 14. 14IPO Watch Europe Survey Q2 2015 | US and Hong Kong domestic activity The US IPO market was reinvigorated in the second quarter after a slow start to 2015 Hong Kong more than doubled H1 2015 proceeds compared to last year * Excludes greenshoe H1 2014 Q1 2015 Q2 2015 H1 2015 Stock exchange IPOs Offering value (€m)* IPOs Offering value (€m)* IPOs Offering value (€m)* IPOs Offering value (€m)* Europe 214 33,730 82 16,375 121 14,724 203 31,099 US 160 23,648 41 5,411 75 11,757 116 17,168 Hong Kong 52 7,630 28 2,075 46 15,099 74 17,174 • The US IPO market came back to life in the second quarter of 2015, increasing 83 percent in volume and 111 percent in proceeds raised, compared to the first quarter of 2015 which had been a record low. 75 IPOs completed in Q2 2015 raising €11.8bn, a significant increase over the first quarter’s 41 IPOs and €5.4bn in proceeds, despite slowing economic growth forecasts in the US and the uncertain interest rate environment. • The healthcare industry continued to lead IPO market activity with 31 IPOs (41 % of total volume) - the high demand for these smaller biotechnology and biopharmaceutical IPOs showcases the interest among IPO investors for high-growth companies. On a total proceeds basis, Q2 was generally well-diversified, with the energy sector raising the highest proceeds – as energy prices slowly show signs of recovery. • Companies continue to crystalize valuations through spin-off transactions to help create improved corporate clarity and visibility. There were 9 spin-offs that closed in the second quarter of 2015. This brought the total number of completed spin-offs for the year to 14, which already exceeds the total spin-offs in 2012 and is on track to surpass the 18 spin-offs in 2013. • In Hong Kong, the second quarter took off after a slow start of the year with 46 IPOs raising €15.1bn, compared to €2.1bn in Q1 2015. Overall, the half year results more than doubled compared to last year, with €17.2bn raised in H1 2015 against €7.6bn in H1 2014. • The new Shenzhen-Hong Kong Stock Connect program, along with the existing Shanghai-Hong Kong Stock Connect program have fuelled the positive IPO trend and define new growth opportunities and perspectives for companies and investors, reflected in the strong results of this first half-year. Figure 22: US and Hong Kong overview

- 15. 15IPO Watch Europe Survey Q2 2015 | Appendix - IPOs by market * Excludes greenshoe Figure 23: IPOs by market H1 2014 Q1 2015 Q2 2015 H1 2015 Stock exchange IPOs Offering value (€m)* IPOs Offering value (€m)* IPOs Offering value (€m)* IPOs Offering value (€m)* TOTAL London Stock Exchange 86 15,867 27 4,648 28 4,697 55 9,345 BME (Spanish Exchange) 6 3,631 3 4,310 5 2,593 8 6,903 Euronext 28 6,570 13 2,637 13 2,267 26 4,904 NASDAQ OMX 33 3,279 18 1,416 37 2,447 55 3,863 SIX Swiss Exchange 5 1,073 1 1,882 1 - 2 1,882 Borsa Italiana 12 1,226 6 490 7 993 13 1,483 Deutsche Börse 7 857 3 573 7 728 10 1,301 Oslo Børs & Oslo Axess 7 386 1 57 5 587 6 644 Irish Stock Exchange 3 483 1 302 1 92 2 394 Warsaw Stock Exchange 16 107 2 8 16 313 18 321 Zagreb Stock Exchange - - 2 36 - - 2 36 Borsa Istanbul 8 43 3 16 1 7 4 23 Bucharest Stock Exchange - - 2 - - - 2 - Wiener Börse 2 194 - - - - - - Prague Stock Exchange 1 14 - - - - - - Athens Stock Exchange - - - - - - - - Budapest Stock Exchange - - - - - - - - Total 214 33,730 82 16,375 121 14,724 203 31,099 EU-REGULATED London Main 40 13,746 18 4,529 14 3,685 32 8,214 BME (Spanish Exchange) (Main) 5 3,626 2 4,310 3 2,588 5 6,898 Euronext 20 6,523 9 2,587 9 2,250 18 4,837 NASDAQ OMX (Main) 11 2,987 6 1,127 11 2,107 17 3,234 SIX Swiss Exchange 5 1,073 1 1,882 1 - 2 1,882 Borsa Italiana (Main) 2 1,121 2 468 2 924 4 1,392 Deutsche Börse (Prime and General Standard) 5 857 2 573 6 728 8 1,301 Oslo Børs 4 351 - - 2 529 2 529 Irish Stock Exchange (Main) 1 200 1 302 1 92 2 394 Warsaw Stock Exchange (Main) 5 105 1 7 5 308 6 315 Zagreb Stock Exchange - - 2 36 - - 2 36 Wiener Börse 2 194 - - - - - - Prague Stock Exchange 1 14 - - - - - - Bucharest Stock Exchange - - - - - - - - Athens Stock Exchange - - - - - - - - Budapest Stock Exchange - - - - - - - - EU-regulated sub-total 101 30,797 44 15,821 54 13,211 98 29,032 EXCHANGE-REGULATED London AIM and SFM 46 2,121 9 119 14 1,012 23 1,131 NASDAQ OMX (First North) 22 292 12 289 26 340 38 629 Oslo Axess 3 35 1 57 3 58 4 115 Borsa Italiana (AIM) 10 105 4 22 5 69 9 91 Euronext (Alternext) 8 47 4 50 4 17 8 67 Borsa Istanbul 8 43 3 16 1 7 4 23 Warsaw Stock Exchange (NewConnect) 11 2 1 1 11 5 12 6 BME (Spanish Exchange) (MAB) 1 5 1 - 2 5 3 5 Bucharest Stock Exchange (AeRO) - - 2 - - - 2 - Deutsche Börse (Entry Standard) 2 - 1 - 1 - 2 - Irish Stock Exchange (ESM) 2 283 - - - - - - Exchange-regulated sub-total 113 2,933 38 554 67 1,513 105 2,067 Europe total 214 33,730 82 16,375 121 14,724 203 31,099

- 16. This publication has been prepared for general guidance on matters of interest only, and does not constitute professional advice. You should not act upon the information contained in this publication without obtaining specific professional advice. No representation or warranty (express or implied) is given as to the accuracy or completeness of the information contained in this publication, and, to the extent permitted by law, PricewaterhouseCoopers LLP, its members, employees and agents do not accept or assume any liability, responsibility or duty of care for any consequences of you or anyone else acting, or refraining to act, in reliance on the information contained in this publication or for any decision based on it. © 2015 PricewaterhouseCoopers LLP. All rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers LLP which is a member firm of PricewaterhouseCoopers International Limited, each member firm of which is a separate legal entity. Contacts IPO Watch Europe surveys all new primary market equity IPOs on Europe’s principal stock markets and market segments (including exchanges in Austria, Belgium, Croatia, Denmark, France, Germany, Greece, the Netherlands, Ireland, Italy, Luxembourg, Norway, Poland, Portugal, Romania, Spain, Sweden, Switzerland, Turkey and the UK) on a quarterly basis. Movements between markets on the same exchange are excluded. This survey was conducted between 1 April and 30 June 2015 and captures IPOs based on their first trading date. All market data is sourced from the stock markets themselves and has not been independently verified by PricewaterhouseCoopers LLP. About IPO Watch Europe David Jetuah (Press office) +44 (0) 20 7212 1812 david.jetuah@uk.pwc.com Mark Hughes +44 (0) 20 7804 3824 mark.c.hughes@uk.pwc.com Vivienne Maclachlan +44 (0) 20 7804 1097 vivienne.maclachlan@uk.pwc.com 16IPO Watch Europe Survey Q2 2015 |