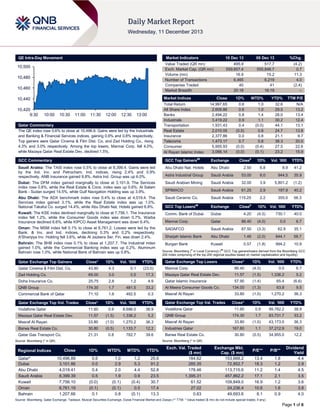

1. QE Intra-Day Movement

Market Indicators

10,500

10,480

10,460

09 Dec 13

%Chg.

495.9

559,607.4

16.9

6,465

40

20:18

517.7

555,846.7

15.2

6,219

41

16:19

(4.2)

0.7

11.3

4.0

(2.4)

–

Market Indices

10,440

10,420

9:30

10 Dec 13

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.6% to close at 10,496.9. Gains were led by the Industrials

and Banking & Financial Services indices, gaining 0.9% and 0.8% respectively.

Top gainers were Qatar Cinema & Film Dist. Co. and Zad Holding Co., rising

4.3% and 3.0% respectively. Among the top losers, Mannai Corp. fell 4.0%,

while Mazaya Qatar Real Estate Dev. declined 1.5%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,997.65

2,609.86

2,494.22

3,419.22

1,931.43

2,010.05

2,377.86

1,473.17

5,955.93

3,066.14

0.6

0.6

0.8

0.9

0.4

(0.5)

0.0

0.7

(0.0)

(0.0)

1.0

1.0

1.4

1.1

(0.0)

0.6

0.8

0.8

(0.4)

(0.1)

32.6

29.5

28.0

30.2

44.1

24.7

21.1

38.3

27.5

23.2

N/A

13.2

13.4

12.4

13.1

13.8

9.7

20.0

22.6

15.9

GCC Commentary

GCC Top Gainers##

Exchange

Close#

1D%

Saudi Arabia: The TASI index rose 0.5% to close at 8,399.4. Gains were led

by the Ind. Inv. and Petrochem. Ind. indices, rising 2.4% and 0.9%

respectively. ANB Insurance gained 9.8%, Astra Ind. Group was up 6.0%.

Abu Dhabi Nat. Hotels

Abu Dhabi

2.50

6.8

8.9

41.2

Astra Industrial Group

Saudi Arabia

53.00

6.0

944.5

35.9

Dubai: The DFM index gained marginally to close at 3,101.9. The Services

index rose 0.8%, while the Real Estate & Cons. index was up 0.6%. Al Salam

Bank - Sudan surged 14.5%, while Gulf Navigation Holding was up 3.9%.

Saudi Arabian Mining

Saudi Arabia

32.00

3.9

5,801.2

(1.2)

SPIMACO

Saudi Arabia

61.25

2.9

197.9

40.2

Abu Dhabi: The ADX benchmark index rose 0.4% to close at 4,019.4. The

Services index gained 3.1%, while the Real Estate index was up 1.0%.

National Takaful Co. surged 14.4%, while Abu Dhabi Nat. Hotels gained 6.8%.

Saudi Ceramic Co.

Saudi Arabia

115.25

2.2

355.0

56.3

GCC Top Losers

Exchange

Kuwait: The KSE index declined marginally to close at 7,756.1. The Insurance

index fell 1.2%, while the Consumer Goods index was down 0.7%. Warba

Insurance declined 6.6%, while KIPCO Asset Management was down 6.4%.

Comm. Bank of Dubai

Dubai

4.20

(4.5)

730.1

40.0

Mannai Corp.

Qatar

86.40

(4.0)

0.0

6.7

Oman: The MSM index fell 0.1% to close at 6,761.2. Losses were led by the

Bank. & Inv. and Ind. indices, declining 0.3% and 0.2% respectively.

A'Sharqiya Inv. Holding fell 3.6%, while Al Jazeera Ser. Fin. was down 2.4%.

SADAFCO

Saudi Arabia

87.50

(3.3)

62.9

35.1

Sharjah Islamic Bank

Abu Dhabi

1.46

(2.0)

844.1

58.7

Burgan Bank

Kuwait

0.57

(1.8)

994.2

10.9

Bahrain: The BHB index rose 0.1% to close at 1,207.7. The Industrial index

gained 1.0%, while the Commercial Banking index was up 0.2%. Aluminum

Bahrain rose 1.0%, while National Bank of Bahrain was up 0.8%.

##

#

Close

Vol. „000

1D% Vol. „000

YTD%

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Gainers

Close*

1D%

Vol. „000

YTD%

Qatar Exchange Top Losers

Close*

1D%

Vol. „000

YTD%

Qatar Cinema & Film Dist. Co.

43.80

4.3

0.1

(23.0)

Mannai Corp.

86.40

(4.0)

0.0

6.7

Mazaya Qatar Real Estate Dev.

11.57

(1.5)

1,336.2

5.2

(6.6)

Zad Holding Co.

69.00

Doha Insurance Co.

3.0

0.5

17.3

25.75

Commercial Bank of Qatar

2.8

1.2

4.9

174.30

QNB Group

1.7

481.5

33.2

71.10

1.6

492.5

0.3

Qatar Islamic Insurance

57.90

65.4

(1.3)

63.8

9.5

(1.0)

1,270.2

36.3

Close*

1D%

Val. „000

YTD%

11.60

0.9

99,782.2

38.9

174.30

Masraf Al Rayan

(1.4)

134.00

33.80

Al Meera Consumer Goods Co.

1.7

83,731.7

33.2

Close*

1D%

Vol. „000

YTD%

Vodafone Qatar

11.60

0.9

8,686.0

38.9

Mazaya Qatar Real Estate Dev.

11.57

(1.5)

1,336.2

5.2

Masraf Al Rayan

33.80

(1.0)

1,270.2

36.3

Masraf Al Rayan

33.80

(1.0)

43,173.0

36.3

Barwa Real Estate Co.

30.80

(0.5)

1,133.7

12.2

Industries Qatar

167.80

1.1

37,212.9

19.0

Qatar Gas Transport Co.

21.31

0.8

782.7

39.6

Barwa Real Estate Co.

30.80

(0.5)

34,955.0

12.2

Qatar Exchange Top Vol. Trades

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Vodafone Qatar

QNB Group

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar Exchange Top Val. Trades

Close

1D%

WTD%

MTD%

YTD%

10,496.89

3,101.86

4,019.41

8,399.39

7,756.10

6,761.19

1,207.66

0.6

0.0

0.4

0.5

(0.0)

(0.1)

0.1

1.0

2.9

2.0

1.9

(0.1)

(0.1)

0.8

1.2

5.3

4.4

0.9

(0.4)

0.5

(0.1)

25.6

91.2

52.8

23.5

30.7

17.4

13.3

Exch. Val. Traded

($ mn)

184.62

285.35

178.46

1,395.31

61.52

27.02

0.83

Exchange Mkt.

Cap. ($ mn)

153,668.2

72,852.7

113,715.6

457,862.2

109,849.0

24,236.4

49,693.6

P/E**

P/B**

13.4

18.3

11.2

17.1

16.9

10.6

8.1

1.8

1.2

1.4

2.1

1.2

1.6

0.9

Dividend

Yield

4.4

2.9

4.5

3.5

3.6

3.8

4.0

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 6

2. Qatar Market Commentary

The QE index rose 0.6% to close at 10,496.9. The Industrials

and Banking & Financial Services indices led the gains. The

index rose on the back of buying support from non-Qatari

shareholders despite selling pressure from Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

63.30%

74.36%

(54,859,825.79)

Non-Qatari

Qatar Cinema & Film Dist. Co. and Zad Holding Co. were the top

gainers, rising 4.3% and 3.0% respectively. Among the top

losers, Mannai Corp. fell 4.0%, while Mazaya Qatar Real Estate

Dev. declined 1.5%.

Buy %*

36.70%

25.63%

54,859,825.79

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Tuesday rose by 11.3% to 16.9mn

from 15.2mn on Monday. Further, as compared to the 30-day

moving average of 12.3mn, volume for the day was 37.1%

higher. Vodafone Qatar and Mazaya Qatar Real Estate Dev.

were the most active stocks, contributing 51.3% and 7.9% to the

total volume respectively.

Ratings, Earnings and Global Economic Data

Ratings Updates

Company

Dubai Islamic Bank

(DIB)

DIB Sukuk Company

Ltd.

Agency

Market

Fitch

Dubai

Fitch

Dubai

Type*

LT IDR/ ST IDR/ VR/

SR/ SR floor

Senior unsecured trust

certificates

Old Rating

New Rating

Rating Change

Outlook

Outlook Change

A/F1/bb/1/A

A/F1/bb/1/A

–

Stable

–

A

A

–

–

–

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC –

Local Currency) (VR – Viability Rating)

Global Economic Data

Date

Market

Source

Indicator

Period

12/10

US

NFIB

NFIB Small Business Optimism

November

12/10

US

US Census Bureau

Wholesale Inventories MoM

October

12/10

US

US Census Bureau

Wholesale Trade Sales MoM

12/10

France

INSEE

Industrial Production MoM

12/10

France

INSEE

12/10

France

INSEE

12/10

France

12/10

Actual

Consensus

Previous

92.5

92.6

91.6

1.40%

0.30%

0.50%

October

1.00%

0.30%

0.80%

October

-0.30%

0.10%

-0.30%

Industrial Production YoY

October

0.00%

0.30%

-0.70%

Manufacturing Production MoM

October

0.40%

0.20%

-0.50%

INSEE

Manufacturing Production YoY

October

0.70%

0.20%

-1.20%

UK

RICS

RICS House Price Balance

November

58%

60%

57%

12/10

UK

ONS

Industrial Production MoM

October

0.40%

0.40%

0.90%

12/10

UK

ONS

Industrial Production YoY

October

3.20%

3.20%

2.20%

12/10

UK

ONS

Manufacturing Production MoM

October

0.40%

0.40%

1.20%

12/10

UK

ONS

Manufacturing Production YoY

October

2.70%

2.90%

0.70%

12/10

UK

ONS

Trade Balance

October

-£2619

-£2800

-£2644

12/10

Italy

ISTAT

Industrial Production MoM

October

0.50%

0.20%

0.20%

12/10

Italy

ISTAT

Industrial Production WDA YoY

October

-0.50%

-2.20%

-2.90%

12/10

Italy

ISTAT

Industrial Production NSA YoY

October

-0.50%

–

0.20%

12/10

Italy

ISTAT

GDP WDA QoQ

3Q2013

0.00%

-0.10%

-0.30%

12/10

Italy

ISTAT

GDP WDA YoY

3Q2013

-1.80%

-1.90%

-2.20%

12/10

China

National Bureau of Stat.

Industrial Production YTD YoY

November

9.70%

9.70%

9.70%

12/10

China

National Bureau of Stat.

Industrial Production YoY

November

10.00%

10.10%

10.30%

12/10

China

National Bureau of Stat.

Retail Sales YTD YoY

November

13.00%

13.10%

13.00%

12/10

China

National Bureau of Stat.

Retail Sales YoY

November

13.70%

13.20%

13.30%

12/10

China

People's Bank of China

Money Supply M0 YoY

November

–

0.081

0.08

12/10

China

People's Bank of China

Money Supply M1 YoY

November

–

0.09

0.089

12/10

China

People's Bank of China

Money Supply M2 YoY

November

–

0.142

0.143

12/10

China

National Bureau of Stat.

New Yuan Loans

November

–

580.0B

506.1B

12/10

Japan

Bank of Japan

Money Stock M2 YoY

November

4.30%

4.20%

4.10%

12/10

Japan

Bank of Japan

Money Stock M3 YoY

November

3.40%

3.50%

3.30%

12/10

Japan

ESRI

Consumer Confidence Index

November

42.5

43.0

41.2

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Page 2 of 6

3. News

Qatar

QCB: Construction sector surged by 9.3% in 2012 –

According to the data released by the Qatar Central Bank

(QCB), Qatar‘s construction sector rose by 9.3% in 2012 to

emerge as one of the fastest growing non-oil sectors. The

construction sector has gained nearly QR2.3bn in 2012 to climb

to a record high in current prices. However, the report showed

that the construction sector‘s share of GDP had edged down to

10.5% in 2012 from 11.2% in 2011. (Bloomberg)

Lasting Iran deal could lead to a Qatar rating upgrade –

According to QNB Group, Qatar, which does not face any

imminent threat from the US shale gas boom, could expect to

get higher ratings if there is a permanent solution for Iran

nuclear crisis. QNB‘s Head of Economics Joannes Mongardini

said that Qatar‘s non-hydrocarbon sector is expected to grow

faster than its oil segment and is expected to witness an

additional inflow of 300,000 workers to fill in 240,000 new jobs

over the next one to two years. (Gulf-Times.com)

QCB issues 3 and 5-year government bonds, sukuk – The

Qatar Central Bank has issued QR4bn worth of government

bonds and sukuk with three-year and five-year durations. (QCB

press release)

Doha metro stations set for completion by 2018 – The

construction work on major underground stations of the Doha

Metro Project, which are progressing as scheduled, are

expected to be accomplished by 2018. Saad Ahmed alMuhannadi, CEO of Qatar Rail Company said that work on the

underground projects is moving along as scheduled and the

Lusail Light Rail Transit (LRT) has reached an advanced stage.

The Lusail LRT underground station is almost complete with

regard to civil engineering works. Other architectural and

technical works would be held in another stage in connection

with other stations. (Gulf-Times.com)

Kahramaa to upgrade services to higher levels – Minister of

Energy and Industry HE Dr Mohamed bin Saleh al-Sada

highlighted the need for the Qatar General Electricity and Water

Corporation (Kahramaa) to upgrade its services to higher levels

in order to meet the expectations of the country‘s residents. He

said that this year‘s theme ―Strategic Transformation in

Performance‖ reflected the corporation‘s response to the goals

and objectives of Qatar National Vision 2030. The QNV has

stressed the importance of economic development, increased

environmental consciousness, cultural development and

capacity building of national human resources. (Gulf-Times.com)

Ooredoo, QNB extends business partnership – Ooredoo and

QNB have extended their pioneering business partnership,

which helps them provide improved services to their customers.

Ooredoo‘s network will ensure continuous availability and uptime for all the banking services covered by QNB‘s extensive

network. This will play a vital role in ensuring QNB‘s customers

never face service disruptions due to connectivity losses

between the bank‘s main office and its branches as well as

ATMs nationwide around the clock. (Gulf-Times.com)

Qatar plans higher health, education outlays in budget –

Qatar will continue to make higher allocations for health and

education in its next budget, in order to reduce its reliance on

the hydrocarbon sector and keep inflation under control. At the

Euromoney Conference, the Prime Minister & Interior Minister

HE Sheikh Abdullah bin Nasser bin Khalifa al-Thani said the

new phase of growth will require the government to focus more

on diversification and expansion in non-oil sectors, which will

boost the economic growth. He also emphasized on the private

sector‘s active participation in Qatar‘s ongoing economic

diversification process. (Gulf-Times.com)

QIF urges QE to tackle liquidity to lure institutional inflow –

According to the Qatar Investment Fund (QIF), factors such as

the MSCI upgrade, mammoth capital expenditure ahead of FIFA

World Cup and a spate of listings augur well for the Qatar

Exchange (QE). However, QE must tackle liquidity problems to

ensure the entry of more foreign institutional investors. At the

Euromoney Conference, QIF chairman Nicholas Wilson said

that QE has witnessed more than 22% growth in its key index

ever since MSCI announced its decision to upgrade Qatar to

‗emerging market‘ from ‗frontier‘ status. (Gulf-Times.com)

RasGas awards EPC contract to Chiyoda Almana for

onshore flow assurance project – The Ras Laffan Liquefied

Natural Gas Company (RasGas) has awarded an engineering,

procurement & construction (EPC) contract to Chiyoda Almana

Engineering for its onshore flow assurance project. This project

consists of onshore storage, pumping and loading facilities for

mono ethylene glycol (MEG), which prevents the formation of

hydrates. This project will include MEG transfer pumps and

facilities to load road tankers that will supply MEG to onshore

facilities of RasGas, Qatargas and Barzan, as well as the

capability to load marine vessels to transport MEG onto offshore

back-up tanks on wellhead platforms. (Bloomberg)

L&T Shipbuilding wins $154mn order from HOSC for

commercial vessels – India-based Larsen & Toubro (L&T)

Shipbuilding has obtained a repeat order worth $154mn from

Halul Offshore Services Company (HOSC) for six specialized

commercial vessels. This order is for the design, construction

and commissioning of four platform supply vessels (PSVs) and

two anchor handling towing, supply & standby vessels

(AHTSSVs) with 150 MT bollard pull. PSVs will be delivered in

1Q2015, while AHTSSVs will be delivered in 4Q2015.

(Bloomberg)

Property deals worth QR868.55mn during December 1-5 –

The Real Estate Registration Department at the Qatar‘s Ministry

of Justice said real estate transactions worth QR868.55mn were

registered during December 1-5, 2013 in Qatar. Properties that

were traded include open plots of land, two-floor villas, annexes,

houses and residential compounds and buildings that are

located in the municipalities of Umm Salal, Al Khor, Doha, Al

Rayyan, Al Shamal, Al Daayen and Al Wakra. (Bloomberg)

GWCS‟ BoD to meet on January 19 – The Gulf Warehousing

Company‘s (GWCS) board of directors will meet on January 19,

2014 to discuss the company‘s financial results ending on

December 31, 2013. (QE)

QA begins 4 weekly flights to Cyprus, could team up with

Emirates – Qatar Airways (QA) has launched four weekly flights

to Larnaca International Airport in Cyprus that will commence

from April 29, 2014. This will be QA‘s first route to Cyprus.

Meanwhile, QA‘s CEO Akbar Al Baker suggested that the airline

could again team up with the Emirates Airline to increase its

leverage when negotiating orders with plane manufacturers.

(Bloomberg)

Page 3 of 6

4. International

US finalizes Volcker rule, curbing Wall Street's risky trades

– US banks will no longer be able to make big trading bets with

their own money after regulators finalized on Tuesday a rule

shutting down what was a hugely profitable business for Wall

Street before the credit crisis. The measure known as the

Volcker rule was a late addition to the 2010 Dodd-Frank Wall

Street reform law and seeks to ensure that banks can't make

speculative trades that are so large and risky that they threaten

individual firms or the wider financial system. Banks had hoped

to substantially soften the rule, but JPMorgan's $6 billion trading

loss in 2012 motivated regulators to devise a tough version.

(Reuters)

US budget deal could usher in new era of cooperation – A

bipartisan budget deal announced in the US Congress on

Tuesday, though modest in its spending cuts, would end three

years of impasse and fiscal instability in Washington that

culminated in October with a partial government shutdown.

However, the agreement faces a challenge from some House

conservatives and will require support of the minority Democrats

to pass. The backing of President Barack Obama should help

round up votes of his fellow Democrats. He urged Congress to

quickly pass it. (Reuters)

Europe edges toward plan to close failing banks – Euro

zone countries edged toward agreeing a plan to tackle ailing

banks on Tuesday but divisions remain about key parts of the

reform that is needed to underpin confidence in the bloc's

lenders. A draft plan, circulated among EU ministers at a

meeting in Brussels, spells out how a new agency may close

failing banks chiefly in the euro zone and, crucially, how the cost

can be shared out among different national funds in the scheme.

Linking these funds will take 10 years, however, and it will fall to

countries to cover the costs in the mean time. The new agency

to shut banks and a fund to pay for the clean-up will form a

second pillar of banking union, as soon as the European Central

Bank starts supervising banks late next year. (Reuters)

IATA: Mideast, Asia-Pacific to drive global passenger

growth – According to the International Air Transport

Association (IATA), emerging economies in the Middle East and

Asia-Pacific will see the strongest international passenger

growth with a CAGR of 6.3% and 5.7% respectively between

2013 and 2017. By 2017, the total number of passengers is

expected to rise to 3.91bn—an increase of 930mn passengers

over 2.98bn passengers carried in 2012. The Asia-Pacific region

is expected to add around 300mn more passengers by the end

of 2017, of which around 75% is expected to be domestic

passengers. (Gulf-Times.com)

Regional

GCC non-hydrocarbon sector growth tops developed

nations “between 1980 and 2009” – According to a research

by three senior IMF economists, the GCC region‘s nonhydrocarbon sector growth performance has been above that of

other oil producers or advanced economies between 1980 and

2009. Growth in Kuwait, Qatar and the UAE during the period

was at par with that of India and China. The sectors that

contributed most to non-hydrocarbon growth (and that increased

their share in the real GDP) were the manufacturing sector in

Bahrain, Oman and Saudi Arabia (driven by petrochemicals),

the construction sector in Oman and Qatar and the

transportation sector in Kuwait, Oman, Qatar and the UAE. The

financial sector also grew strongly in Qatar and the UAE. (GulfTimes.com)

GOIC: Total GCC industrial investment rises to $338bn in

2012 – According to the data released by the Gulf Organization

for Industrial Consulting (GOIC), total industrial investments in

the GCC region rose from $81bn in 1998 to $338bn in 2012.

The number of GCC firms has increased from 7,089 in 1998 to

15,165 in 2012, while the number of workers grew from 559,420

workers in 1998 to 1.34mn workers in 2012. The data showed

that most of these investments were in the segments such as

chemicals, refined petroleum products, base metals, building

materials and food industries. (GulfBase.com)

Bloomberg: Sukuk sales surge to $4.7bn in 3Q2013 –

According to the data compiled by Bloomberg, sukuk sales have

surged to $4.7bn in 3Q2013. The average yield on Shari‘ahcompliant debt from the GCC region fell 10 basis points to

3.78% in 3Q2013. (Bloomberg)

Stéphane Michel appointed President for Total‟s Middle

East, E&P Division – French oil company Total E&P Qatar

Managing Director Stéphane Michel has been appointed as the

President for the Middle East, Exploration & Production Division.

Michel will take on this new assignment in Paris on January 1,

2014 and will be reporting to Arnaud Breuillac, President (E&P)

at Total. (Gulf-Times.com)

OPEC trims output to lowest in 2 years as Saudi Arabia cuts

– OPEC has reduced its crude oil production in November to the

lowest level in two years as the output dropped below the

organization‘s 30mn barrels-per-day ceiling for the third month.

OPEC pumped 29.63mn bpd last month as compared to

29.83mn bpd in October. According to OPEC‘S monthly report,

output from Saudi Arabia fell to a five-month low of 9.63mn bpd

last month from 9.71mn bpd in October. (Gulf-Times.com)

CDSI: Saudi non-oil exports stood at SR17.97bn in October

– According to a report released by the Central Department of

Statistics & Information (CDSI), Saudi non-oil exports stood at

SR17.97bn in October 2013, indicating 12.6% YoY. However,

Saudi imports have declined by 0.2% YoY to SR44.2bn. The

CDSI report showed that petrochemical products have topped

the Kingdom‘s list of exports in October and accounted for

31.74% of non-oil exports valued at SR5.7bn. Plastic products

ranked second among non-oil exports to SR5.36bn, which is

followed by the transport equipment & their parts at 15.02% of

the total value of exports. Meanwhile, the report showed that

equipment, machinery and electrical utensils have captured the

highest value of Saudi imports in October 2013 at SR10.94bn,

followed by transport materials at SR8.28bn and ordinary metals

& their products at SR5.13bn. The report also showed that the

UAE has topped the list of major importers from Saudi Arabia by

14.38% of the total value of exports in October, followed by

China at 13.80% and Singapore at 5.61%. (GulfBase.com)

SAGIA: Kingdom ready to invest in Azerbaijan‟s industry –

Saudi Arabian General Investment Authority‘s (SAGIA) Head

Abdullatif Al Othman said that the Kingdom is ready to invest in

Azerbaijan's petrochemical and refining industry. (Bloomberg)

Kingdom to increase its share in IDB‟s subscribed capital

by SR902.19mn – Saudi Arabia‘s Deputy Premier & Minister of

Defense Crown Prince Salman said that the Kingdom has

decided to increase its share in the Islamic Development Bank‘s

(IDB) subscribed capital by SR902.19mn. This will bring its total

share to SR5.15bn. This new amount will be paid to the bank

over a period of 20 years beginning from 2016. This capital

increase will enable IDB to meet the growing requirements of its

56-member countries. (GulfBase.com)

Rolls-Royce obtains contract from HDEC for ADMA OPCO –

Rolls-Royce has obtained a strategic contract from Korea‘s

Page 4 of 6

5. Hyundai Engineering & Construction (HDEC) to supply the Abu

Dhabi Marine Operating Company (ADMA OPCO) with power

generation equipment and related services. This will help boost

oil & gas processing activities at the Satah Al Razboot offshore

project in the UAE. (Bloomberg)

Kingdom plans SR15bn water storage projects – The

National Water Company‘s (NWC) CEO Luay Al Musallam said

the Kingdom is straining to meet the growing water demand of

its population and is planning to implement SR15bn water

storage projects. Luay Al Musallam said that Jeddah will be the

site for the first storage project that will begin in 2014.

(Bloomberg)

Yansab‟s BoD recommends SR2 dividend for 2H2013 –

Yanbu National Petrochemicals Company‘s (Yansab) board of

directors has recommended a dividend of SR2 per share for

2H2013, which translates to a total dividend of SR3 per share

for 2013. The company expects to increase its annual dividend

to SR3.5 per share in 2014 and SR4 per share in 2015.

(GulfBase.com)

Saudi CMA approves AFG‟s capital decrease request – The

Saudi Capital Market Authority‘s (CMA) board of commissioners

has approved Aldukheil Financial Group‘s (AFG) request to

decrease its capital from SR50mn to SR2mn. (Tadawul)

Saudi CMA approves BNP Paribas‟ amendment its business

profile – The Saudi CMA‘s Board of Commissioners has

approved BNP Paribas Investment Company‘s request to

amend its business profile by including managing investment

funds & advising activities. BNP Paribas will now be authorized

to conduct deals as a principal, agent that manages investment

funds, arranges, advises and handles custody activities.

(Tadawul)

DMCC signs MoU with UAB to facilitate account opening

process for companies – The Dubai Multi Commodities Centre

(DMCC) has entered into a MoU with Sharjah-based United

Arab Bank (UAB) to facilitate the process of opening a bank

account for companies, while they establish themselves in the

DMCC Free Zone. Under this MoU, DMCC and UAB have

agreed to collaborate for creating a streamlined process where

companies can register in the DMCC Free Zone and open a

bank account simultaneously. Meanwhile, UAB has opened a

new branch in DMCC‘s Almas Tower. (GulfBase.com)

7.34mn Indian passengers pass through Dubai in 2012 –

Dubai Airports Company‘s (DAC) Media Relations Manager

Zaigham Ali said that India has emerged as the largest market

served from Dubai with 7.34mn passengers passing through it in

2012. The number of Indian passengers who travel to or through

Dubai International Airport is expected to reach 8.3mn in 2013.

This increase is due to seven Indian and Dubai airlines

operating a total of 185 weekly flights from 20 Indian cities to

Dubai. (Bloomberg)

MEED: Abu Dhabi‟s project spending to cross $100bn in

next seven years – According to MEED, Abu Dhabi‘s project

spending could expand to cross $100bn over the next seven

years as the government ramps up its efforts to sustain

economic gains seen in the last few years. Construction projects

have remained the most active sector with projects worth $30bn

to be awarded over the next seven years. The oil & gas sector

has a project pipeline worth $25bn, while transport & chemicalrelated projects will also see a surge in investments worth

$20bn. Similarly, the industrial as well as power & water sectors

will be busy with contracts valued at $6bn and $5bn

respectively, which will be awarded until 2020. (GulfBase.com)

ADX bets on GIIs, stream of IPOs in 2014 – The Abu Dhabi

Securities Exchange‘s (ADX) CEO Rashed Al Baloushi said that

ADX is betting with UAE‘s upgrade to emerging market status.

He said that an improvement in the Emirate‘s economy will

attract more global institutional investors (GIIs) and prompt a

stream of IPOs in 2014. (Bloomberg)

Abu Dhabi soon to have permanent cruise terminal – The

Abu Dhabi Tourism & Culture Authority‘s (TCA Abu Dhabi)

Director General Mubarak Al Muhairi said that the Emirate is

moving closer to have a permanent cruise terminal built at Mina

Zayed. This cruise terminal will boast of a dedicated cruise

stopover beach and other amenities. (Bloomberg)

IDB begins work to issue industrial licenses for firms – The

Industrial Development & Regulation Bureau (IDB) has begun its

work for issuing licenses to the firms intending to start

manufacturing activities in Abu Dhabi. This agency will also

regulate the Emirate‘s manufacturing sector, which is a key

element in Abu Dhabi‘s economic diversification strategy under

the Abu Dhabi Vision 2030. The agency will also approve

applications for gas connections to industrial consumers and

formulate policies for creating an environment conducive for

setting up of a knowledge-based economy. (GulfBase.com)

Abu Dhabi plans to double its rig count by 2018 – Abu Dhabi

Marine Operating Company‘s (ADMA-OPCO) CEO Ali Al

Jarwan said the Emirate is planning to more than double its rig

count as more oil wells will be developed. The number of rigs

will be increased from 40 rigs to 88 rigs by 2018, which is part of

the Emirate‘s plan to raise its oil output by 35% in 2018.

(GulfBase.com)

Bahrain expects 20,000 trade visitors to attend BIAS –

Bahrain‘s Ministry of Transportation expects 20,000 trade

visitors to attend the Bahrain International Airshow 2014 (BIAS).

These visitors also include around 100 companies and

governmental, military and civil delegations from over 25

countries. (GulfBase.com)

Emaar launches Vida Residence, The Hills – Emaar

Properties has launched Vida Residence, The Hills in Dubai that

will feature 136 serviced apartments. (GulfBase.com)

Depa appoints new independent directors – Depa Ltd. has

appointed Roderick Maciver and Fahad Al Nabet as the

company‘s

independent

non-executive

directors.

(GulfBase.com)

EITC‟s BoD approves new board member –

Integrated Telecommunications Company‘s (EITC)

directors has approved the appointment of Masood

as the new board member who will represent

Development Company. (DFM)

Emirates

board of

Mahmood

Mubadala

Page 5 of 6

6. Rebased Performance

Daily Index Performance

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

150.8

132.8

0.7%

0.5%

0.6%

0.4%

0.1%

120.4

0.0%

0.1%

S&P Pan Arab

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Yen

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

1,262.18

1.8

2.7

(24.7)

DJ Industrial

20.40

2.7

4.6

(32.8)

S&P 500

109.38

(0.0)

(2.0)

(1.6)

4.32

2.6

4.4

0.7

3.2

46.5

136.00

(0.2)

(2.2)

(21.4)

1.38

0.2

0.4

4.3

102.85

(0.4)

(0.1)

1.64

0.1

0.6

1.13

0.3

0.5

RUB

BRL

26.1

131.13

CHF

USD Index

Dubai

Oman

Source: Bloomberg

GBP

AUD

Bahrain

Jul-13

(0.1%)

Abu Dhabi

QE Index

Oct-11 May-12 Dec-12

Kuwait

Aug-10 Mar-11

Qatar

(0.0%)

(0.5%)

Saudi Arabia

Jan-10

1.3%

18.6

NASDAQ 100

STOXX 600

DAX

FTSE 100

CAC 40

Nikkei

Close

1D%

WTD%

YTD%

15,973.13

(0.3)

(0.3)

21.9

1,802.62

(0.3)

(0.1)

26.4

4,060.49

(0.2)

(0.0)

34.5

314.91

(0.7)

(0.5)

12.6

9,114.44

(0.9)

(0.6)

19.7

6,523.31

(0.6)

(0.4)

10.6

4,091.14

(1.0)

(0.9)

12.4

15,611.31

(0.2)

2.0

50.2

1.2

MSCI EM

1,012.32

(0.0)

1.0

(4.1)

3.1

SHANGHAI SE Composite

2,237.49

(0.0)

0.0

(1.4)

HANG SENG

0.92

0.4

0.5

(12.0)

23,744.19

(0.3)

0.0

4.8

79.97

(0.2)

(0.4)

0.2

BSE SENSEX

21,255.26

(0.3)

1.2

9.4

7.2

Bovespa

50,993.02

(0.3)

0.1

(16.3)

1,409.85

(0.2)

1.4

(7.7)

32.72

0.43

(0.1)

0.4

(0.0)

0.9

(11.3)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (―QNBFS‖) a wholly-owned subsidiary of Qatar National Bank (―QNB‖). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6