QNBFS Daily Technical Trader Qatar - September 07, 2023 التحليل الفني اليومي ...

23 July Daily market report

1. Page 1 of 7

QE Intra-Day Movement

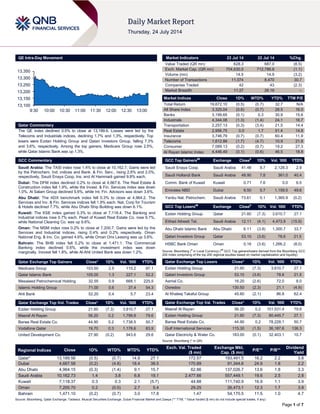

Qatar Commentary

The QE index declined 0.5% to close at 13,189.6. Losses were led by the

Telecoms and Industrials indices, declining 1.7% and 1.3%, respectively. Top

losers were Ezdan Holding Group and Qatari Investors Group, falling 7.3%

and 3.6%, respectively. Among the top gainers, Medicare Group rose 2.5%,

while Qatar Islamic Bank was up 1.3%.

GCC Commentary

Saudi Arabia: The TASI index rose 1.4% to close at 10,162.7. Gains were led

by the Petrochem. Ind. indices and Bank. & Fin. Serv., rising 2.6% and 2.0%,

respectively. Saudi Enaya Coop. Ins. and Al Hammadi gained 9.8% each.

Dubai: The DFM index declined 0.2% to close at 4,667.6. The Real Estate &

Construction index fell 1.9%, while the Invest. & Fin. Services index was down

1.0%. Al Salam Group declined 5.6%, while Int. Fin. Advisors was down 3.6%.

Abu Dhabi: The ADX benchmark index fell 0.3% to close at 4,964.2. The

Services and Inv. & Fin. Services indices fell 1.9% each. Nat. Corp for Tourism

& Hotels declined 7.7%, while Abu Dhabi Ship Building was down 6.1%.

Kuwait: The KSE index gained 0.3% to close at 7,118.4. The Banking and

Industrial indices rose 0.7% each. Pearl of Kuwait Real Estate Co. rose 9.7%,

while National Cleaning Co. was up 9.6%.

Oman: The MSM index rose 0.2% to close at 7,200.7. Gains were led by the

Services and Industrial indices, rising 0.4% and 0.2% respectively. Oman

National Eng. & Inv. Co. gained 4.6%, while Oman Orix Leasing was up 3.6%.

Bahrain: The BHB index fell 0.2% to close at 1,471.1. The Commercial

Banking index declined 0.6%, while the investment index was down

marginally. Inovest fell 1.8%, while Al-Ahli United Bank was down 1.2%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Medicare Group 103.50 2.5 115.2 97.1

Qatar Islamic Bank 105.00 1.3 227.1 52.2

Mesaieed Petrochemical Holding 32.55 0.9 668.1 225.5

Islamic Holding Group 71.00 0.6 37.4 54.3

Ahli Bank 52.20 0.4 5.7 23.4

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 21.60 (7.3) 3,610.7 27.1

Masraf Al Rayan 56.20 0.2 1,799.8 79.6

Barwa Real Estate Co. 44.90 0.2 1,738.5 50.7

Vodafone Qatar 19.70 0.3 1,176.6 83.9

United Development Co. 27.90 (0.2) 943.6 29.6

Market Indicators 23 Jul 14 22 Jul 14 %Chg.

Value Traded (QR mn) 628.3 687.0 (8.5)

Exch. Market Cap. (QR mn) 704,630.5 712,786.8 (1.1)

Volume (mn) 14.5 14.9 (3.2)

Number of Transactions 11,074 8,470 30.7

Companies Traded 42 43 (2.3)

Market Breadth 11:27 26:16 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 19,672.10 (0.5) (0.7) 32.7 N/A

All Share Index 3,325.04 (0.6) (0.7) 28.5 16.0

Banks 3,199.65 (0.1) 0.3 30.9 15.6

Industrials 4,344.08 (1.3) (1.4) 24.1 16.7

Transportation 2,257.13 (0.3) (3.4) 21.5 14.4

Real Estate 2,956.75 0.0 1.7 51.4 14.8

Insurance 3,746.79 (0.7) (0.7) 60.4 11.9

Telecoms 1,612.88 (1.7) (4.7) 10.9 21.8

Consumer 7,089.13 (0.2) (0.7) 19.2 27.3

Al Rayan Islamic Index 4,446.49 (0.1) (0.6) 46.5 18.8

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Saudi Enaya Coop. Saudi Arabia 41.48 9.7 2,128.3 2.9

Saudi Hollandi Bank Saudi Arabia 48.90 7.8 361.0 40.4

Comm. Bank of Kuwait Kuwait 0.71 7.6 0.0 6.5

Emirates NBD Dubai 9.50 5.7 1,159.5 49.6

Yanbu Nat. Petrochem. Saudi Arabia 73.61 5.1 1,365.9 (0.2)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Ezdan Holding Group Qatar 21.60 (7.3) 3,610.7 27.1

Etihad Atheeb Tel. Saudi Arabia 12.11 (4.1) 4,473.9 (15.9)

Abu Dhabi Islamic Bank Abu Dhabi 6.11 (3.8) 1,300.7 33.7

Qatari Investors Group Qatar 53.10 (3.6) 78.6 21.5

HSBC Bank Oman Oman 0.16 (3.6) 1,266.2 (8.0)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 21.60 (7.3) 3,610.7 27.1

Qatari Investors Group 53.10 (3.6) 78.6 21.5

Aamal Co. 16.20 (2.6) 72.0 8.0

Ooredoo 130.50 (2.3) 21.1 (4.9)

Al Khaleej Takaful Group 45.60 (2.1) 86.8 62.4

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Masraf Al Rayan 56.20 0.2 101,531.4 79.6

Ezdan Holding Group 21.60 (7.3) 80,445.7 27.1

Barwa Real Estate Co. 44.90 0.2 78,228.1 50.7

Gulf International Services 115.30 (1.5) 36,187.6 136.3

Qatar Electricity & Water Co. 183.00 (0.1) 32,403.1 10.7

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 13,189.56 (0.5) (0.7) 14.8 27.1 172.57 193,491.5 16.2 2.2 3.8

Dubai 4,667.58 (0.2) (4.8) 18.4 38.5 170.89 91,344.6 24.9 1.8 2.2

Abu Dhabi 4,964.15 (0.3) (1.4) 9.1 15.7 62.86 137,026.7 13.6 1.8 3.3

Saudi Arabia 10,162.73 1.4 3.8 6.8 19.1 2,477.66 557,449.1 19.6 2.5 2.8

Kuwait 7,118.37 0.3 0.3 2.1 (5.7) 44.88 111,740.9 16.9 1.1 3.9

Oman 7,200.70 0.2 (0.0) 2.7 5.4 29.25 26,473.1 12.3 1.7 3.9

Bahrain 1,471.10 (0.2) (0.7) 3.0 17.8 1.47 54,170.5 11.5 1.0 4.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

13,100

13,150

13,200

13,250

13,300

13,350

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 7

Qatar Market Commentary

The QE index declined 0.5% to close at 13,189.6. The Telecoms

and Industrials indices led the losses. The index fell on the back

of selling pressure from Qatari shareholders despite buying

support from non-Qatari shareholders.

Ezdan Holding Group and Qatari Investors Group were the top

losers, falling 7.3% and 3.6% respectively. Among the top

gainers, Medicare Group rose 2.5%, while Qatar Islamic Bank

was up 1.3%.

Volume of shares traded on Wednesday fell by 3.2% to 14.5mn

from 14.9mn on Tuesday. However, as compared to the 30-day

moving average of 14.1mn, volume for the day was 2.7% higher.

Ezdan Holding Group and Masraf Al Rayan were the most active

stocks, contributing 25.0% and 12.4% to the total volume

respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Invest Bank

(INVESTB)

Capital

Intelligence

Abu

Dhabi

FSR/LT FCR/ST

FCR/SR

BBB/BBB/A3/3 BBB/BBB/A3/3 – Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC

– Local Currency)

Earnings Releases

Company Market Currency

Revenue

(mn)1Q2014

% Change

YoY

Operating Profit

(mn) 1Q2014

% Change

YoY

Net Profit (mn)

1Q2014

% Change

YoY

Dunia Finance* Duabi AED – – – – 82.6 48.6%

Deyaar Development Dubai AED 488.3 421.6% 73.4 -28.8% 62.5 129.2%

United Kaipara Diaries Co.* Dubai AED 170.0 16.9% -22.5 NA -20.7 NA

Majid Al Futtaim Holding

(MAF)*

Dubai AED 12800.0 NA – – 0.0 NA

Abu Dhabi Aviation (ADA)* Abu Dhabi AED 734.4 -6.1% 209.1 9.3% 109.7 16.2%

Ras Al Khaimah Poultry &

Feeding Co. (RAPCO)*

Abu Dhabi AED 25.4 NA – – 23.5 564.4%

Kuwait Projects Co. (KIPCO) Kuwait KD – – – – 11.4 NA

Al Mazaya Holding Co. Kuwait KD 5.7 -26.4% – – 1.6 673.5%

Shell Oman Marketing Co.

(SOMS)*

Oman OMR 188.5 -9.7% – – 5.7 -6.1%

Al-Hassan Engineering Co.

(AHEC)*

Oman OMR – – – – -1.8 NA

Sohar Poultry Co. (SPC)** Oman OMR 8.1 7.9% – – 0.6 77.3%

Al Maha Petroleum Products

Marketing Co.*

Oman OMR 174.8 13.9% – – 5.6 7.6%

Bahrain Commercial

Facilities Company (BCFC)

Bahrain BHD – – – – 4.2 35.5%

Source: Company data, DFM, ADX, MSM (** FY2014 results, * 1H2014 results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

07/23 US MBA MBA Mortgage Applications 18 July 2.40% – -3.60%

07/23 EU European Commission Consumer Confidence July -8.4 -7.5 -7.5

07/23 France INSEE Business Survey Overall Demand July -6.0 – 7.0

07/23 France INSEE Production Outlook Indicator July -18.0 – -19.0

07/23 France INSEE Manufacturing Confidence July 97.0 98.0 97.0

07/23 France INSEE Business Confidence July 93.0 92.0 93.0

07/23 UK BBA BBA Loans for House Purchase June 43265 41375 41881

07/23 UK CBI CBI Reported Sales July 21.0 15.0 4.0

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 71.59% 74.09% (15,676,968.37)

Non-Qatari 28.41% 25.91% 15,676,968.37

3. Page 3 of 7

News

Qatar

CBQK 2Q2014 profitability slightly misses estimates on the

back of higher-than-expected provisions. CBQK posted a net

profit of QR489.8mn, slightly below (5.5%) our estimate of

QR518.5mn (Bloomberg & Reuters consensus of QR513mn and

QR512.75mn). Net income declined by 8.3% and 5.5% QoQ

and YoY, respectively. A surge in provisions was the primary

cause of drop in profitability and the miss. The bank posted net

provisions (credit and investment impairments) of QR227.1mn

vs. QR59.3mn in 1Q2014 (2Q2013: QR148.2mn). CBQK

exhibited healthy performance from core banking income.

Net interest income climbed up by 5.1% QoQ (+41.9% YoY;

note YoY comparisons are impacted by Abank’s consolidation)

to QR652.7mn. The bank’s NIM has shown signs of

improvement, improving to 2.7% in 2Q2014 vs. 2.6% in 1Q2014.

Fees & commissions surged by 28.1% QoQ (+64.2% YoY) to

QR271.0mn. On the other hand, FX income was weak at

QR24.3mn (down 42.5% and 39.1% QoQ and YoY,

respectively). Share of profit from associates (QR101.8mn)

displayed positive performance, growing by 11.1% QoQ and

27.7% YoY. Operating expenses marginally increased by 3.6%

QoQ (+62.8% YoY). On the positive side, CBQK’s efficiency

ratio improved from 39.6% in 1Q2014 to 36.3% in 2Q2014

(2Q2013: 38.8%). Loan growth is yet to materialize. CBQK’s

loan book grew by 1.0% QoQ (3.8% YTD), reaching QR69.4bn.

On the other hand, deposits receded by 3.7% QoQ (down 5.6%

YTD) to QR59.8bn. As such, the LDR jumped to 116% in

2Q2014 vs. 111% in 1Q2013 (2013: 105%). Abank contributed

18.2% and 14.7% to overall loans and deposits, respectively.

(QE, QNBFS)

QISI reports QR48.6mn net profit in 1H2014 – Qatar Islamic

Insurance Company’s (QISI) net profit increased to QR48.6mn

in 1H2014 from QR35.8mn in 1H2013. EPS stood at QR3.24 in

1H2014 as compared to QR2.39 in 1H2013. (QE)

ORDS registers 2% YoY decline in 1H2014 net profit –

Ooredoo’s (ORDS) net profit fell by 2% YoY to QR1.7bn in

1H2014. ORDS’ revenue dipped to QR16.5bn in 1H2014, down

3% compared to 1H2013, despite the strong performance in

Qatar, Oman and Algeria that was offset by decline in revenue

in Indonesia, Kuwait and Iraq. ORDS’ EBITDA decreased by

10% YoY to QR6.8bn in 1H2014 (1H2013: QR 7.6bn) with

EBITDA margin decreasing to 42% (1H2013: 45%) due to lower

revenues and the continued investment across the business into

customer acquisition and retention, global brand roll-out, service

launches and customer experience. The company’s customer

base rose 2% YoY to 93.9 mn in 1H2014 backed by its

increasing share across markets. (Peninsula Qatar)

UDCD 1H2014 profit up 34% to QR521mn – United

Development Company (UDCD) posted a 34% increase in net

profit to QR521mn in 1H2014 compared with QR389mn in

1H2013 riding on strong show by group companies. UDCD’ EPS

reached QR1.41 for 1H2014, compared with QR0.92 in 1H2013,

up 53%. The Company’s gross profit stood at QR702mn in

1H2014, compared with QR508mn in 1H2013. (Gulfbase.com)

BRES posts QR222.2mn net profit in 1H2014 – Barwa Real

Estate Company (BRES) reported a net profit of QR222.2mn in

1H2014 as compared to QR199.2mn in 1H2013. The

Company’s EPS amounted to QR0.58 in 1H2014 versus

QR0.52 in 1H2013. (QE)

GDI awards N-KOM contracts worth $110mn – Gulf Drilling

International (GDI) Limited, a subsidiary of Gulf International

Services (GISS), has awarded two contracts worth $110mn to

Nakilat-Keppel Offshore & Marine (N-KOM). N-KOM is a joint

venture shipyard between Nakilat (QNNS) and Singapore’s

Keppel Offshore & Marine (Keppel O&M). The first contract is for

the construction of a self-propelled and self-elevating liftboat,

which is customized for field transit operations in the MENA

region in water depths of up to 65 meters. The liftboat, which will

be completed at the end of 2015, will provide accommodation

and platform support services for customers with operations in

Qatar. N-KOM has also bagged a six-year repair and

maintenance contract for GDI’s existing fleet of jack-up rigs

operating in the Middle East. (QE)

IBB offers UK real estate financing for GCC clients – The

Islamic Bank of Britain (IBB) is offering its UK real estate finance

products to Gulf-based clients this summer. A member of Masraf

Al Rayan Group (MARK), the IBB’s offering is tailored toward

discerning individuals seeking to purchase a property in London

or the UK for investment purposes or as a holiday home. As the

oldest Shariah-compliant retail bank in the UK, IBB is offering a

premium service for clients seeking established local expertise

and insights into the property buying process in the UK. The

bank also offers attractive financing rates and is complemented

by assistance from a dedicated team based in the Knightsbridge

area of London that specializes in assisting GCC nationals with

their property purchase in the UK. MARK intends to build upon

IBB’s excellent foundations and has invested over £100mn to

support its expansion. These include Shari’ah-compliant savings

& property finance products for retail & commercial customers

based locally and for those investing in the UK from the Gulf.

(Gulfbase.com)

MDPS: Monthly Industrial PPI rises by 0.3% month-on-

month (up 3.1% year-on-year) in May – The Ministry of

Development Planning and Statistics (MDPS) has released the

monthly Producer Price Index (PPI) of the industrial sector which

covers mining, electricity & water and manufacturing activities

for May 2014. The PPI for May 2014 stood at 170.3, which

showed an increase of 0.3% month-on-month and a year-on-

year increase of 3.1%. The mining group (with 77% weightage)

PPI increased by 0.1% month-on-month (2.9% year-on-year),

primarily due to the overall price increase seen in the crude

petroleum and natural gas group by the same percentage. The

manufacturing group (with a weight of 21%) PPI showed a rise

of 1.3% month-on-month (4.3% year-on-year). (MDPS)

QCFS to announce results on August 10 – Qatar Cinema and

Film Distribution Company (QCFS) will disclose its financial

reports for the period ending June 30, 2014, on August 10,

2014. (QE)

IQCD to announce results on August 10 – Industries Qatar

(IQCD) will disclose its financial reports for the period ending

June 30, 2014, on August 10, 2014. (QE)

QSTec strikes deal with Qatar Rail to explore solar energy

prospects – Qatar Solar Technologies (QSTec) has signed a

deal with Qatar Railways Company (Qatar Rail) to explore

opportunities that may lead to the installation of up to 80

megawatts (MW) of solar technology within Qatar’s upcoming

rail network. The company is currently building a 150 MW solar

module manufacturing facility and an 8,000-ton polysilicon

manufacturing plant in Qatar. The first stage of the deal will look

at installing ground and rooftop mounted solar PV installations

on the proposed three million square meter rail depot facility that

will be located near the new Sheikh Hamad International Airport.

(Bloomberg)

4. Page 4 of 7

International

IMF cuts US 2014 growth forecast to 1.7% – The International

Monetary Fund expects the US economy to grow 1.7% in 2014,

even more slowly than it predicted a month ago, as weakness in

the first quarter offsets an expected pick-up in the second half of

2014. The IMF, which in June forecasted a 2% growth for the

US in 2014, said US activity should accelerate to 3% to 3.5% in

the remainder of 2014, and grow by 3% in 2015 and 2016. The

IMF said that the drag on growth from the first quarter

contraction will still not be offset. US GDP contracted at an

annual pace of 2.9% in the first three months of 2014, dragged

down by a weak housing market, a slower pace of restocking by

businesses and lower exports. It was the sharpest decline in five

years. The Fund said that the lower growth expectations should

contribute to continued slack in the labor market for the next

three to four years, with the US remaining below full

employment until 2018. The IMF added that the US Federal

Reserve could keep its benchmark interest rates at zero beyond

the middle of 2015, the date implied by policy maker forecasts,

as long as inflation and financial stability concerns remain

subdued. The Fund believed the US central bank could then

raise rates at every other policy meeting, in what would be a

more gradual approach than what the median Fed forecasts

currently suggest. According to the IMF, further US growth could

be disappointing if US interest rates rise too quickly, there is a

broader & concerted slowdown in emerging markets, and

increasing geopolitical tensions in Iraq and Ukraine prompt

higher energy prices and severe financial & trade disruptions.

(Reuters)

MBA: US mortgage applications rise in latest week –

Applications for US home mortgages rose last week as both

purchase and refinancing applications picked up. The Mortgage

Bankers Association said its seasonally adjusted index of

mortgage application activity, which includes both refinancing

and home purchase demand, rose 2.4% in the week ended July

18. The MBA's seasonally adjusted index of refinancing

applications climbed 4.1%, while the gauge of loan requests for

home purchases, a leading indicator of home sales, rose 0.3%.

The fixed 30-year mortgage rates averaged 4.33% in the week,

unchanged from the week before. (Reuters)

Eurozone confidence falls in July, bodes ill for recovery –

According to the European Commission preliminary data,

consumer confidence in the Eurozone deteriorated much more

than expected in July, adding to worries about the health of the

bloc's economic recovery. The 18 countries using the Euro saw

consumer confidence falling to -8.4 in July from a revised -7.5 in

June, showing the worst reading since April, when it stood at -

8.6. Analysts surveyed by Reuters expected the bloc's

consumer confidence to edge down to -7.5 in July from the

originally reported -7.4 in June. IHS Global Insight’s Chief

European economist Howard Archer said a second successive,

and deeper dip in Eurozone consumer confidence in July will

fuel mounting concerns that already weak growth is faltering. He

added while the Eurozone consumer confidence is still clearly

above its long-term average, the recent about-turn in sentiment

is an unwelcome and worrying development. In another sign of

the fragility of the recovery, Eurozone industrial production

dropped sharply in May with only the energy sector thriving. The

confidence is suffering partly because of the conflict in eastern

Ukraine, where separatists backed by Russia are fighting

government forces. As a result, the European Union is

considering economic sanctions against Russia, but such action

would also hurt the Eurozone economy. (Reuters)

China July HSBC flash PMI rises to 18-month high –

According to a preliminary HSBC survey, activities in China's

factory sector expanded at its fastest pace in 18 months in July,

as a raft of government stimulus measures kicked in. The

HSBC/Markit Flash China Manufacturing Purchasing Managers'

Index rose to 52.0 in July from June's final reading of 50.7,

beating a forecast of 51.0 in a Reuters poll. It was the highest

reading since January 2013, and above the 50-point level that

separates growth in activity from contraction for the second

consecutive month. A sub-index measuring new orders, a gauge

of demand at home and abroad, hit a 18-month high of 53.7,

while the sub-index for output also rose to a 16-month high in

June. The final Markit/HSBC manufacturing PMI for July is due

on August 1. China's economy grew slightly faster than

expected in the second quarter as a burst of government

stimulus paid dividends, but analysts said Beijing will likely need

to offer further support to meet its growth target of around 7.5%

for 2014. (Reuters)

Japan trade deficit expands after exports unexpectedly

drop – Japan’s trade deficit was larger than forecast after

exports unexpectedly fell, dragging on an economy squeezed by

a sales-tax increase in April. The finance ministry reported that

the shortfall in June was 822.2bn Yen, surpassing the 643bn

Yen median estimate in a Bloomberg News survey of 32

economists. Exports shrank 2% from a year earlier, while

imports rose 8.4%. The government this week cut its growth

forecast for the year ending March 2015, citing weak foreign

demand and a fall in consumption after the tax rise. With fossil-

fuel imports swelling the trade deficit, now at a record 24

months, a pick-up in exports is needed to help Prime Minister

Shinzo Abe sustain growth in the world’s third-largest economy.

Citigroup’s Chief Economist Kiichi Murashima said that the trade

deficit will remain at the current level through the end of this year

with both exports and imports growing slightly. He said the

export recovery will be sluggish mainly due to structural

reasons, as Japanese companies are producing products

abroad for foreign demand. Exports to the US fell 2.2% from a

year earlier, with automobiles shipments dropping 6.8%. Exports

to Asia were down 3.8%. (Bloomberg)

Regional

Moody’s: Mideast firms face $91bn refinancing needs –

According to a Moody’s report, Middle East investment grade

companies are facing refinancing needs of about $91bn from

bank and bond debt due to mature over the next four years.

Moody’s pointed out that this accounts for about 8% of the total

EMEA bank and debt maturities of $1.17tn. The report analyses

the refinancing needs of its EMEA-based investment grade (IG)

issuers by examining their bond and bank loans maturities on an

annual basis. Among EMEA countries, companies in Germany,

France and the UK represent the greatest amounts of bank and

bond maturities (each at 15%) in the next four years. Moody’s

said refinancing concerns may shift to Russia, which now

constitutes 10% of the total EMEA (11% of European) bank &

bond maturities over the same period. The report stated that the

average investment grade corporate credit quality over the next

four years will be stable to slightly improving, with liquidity

remaining solid supported by the gradual macroeconomic

recovery. The report further added that despite the trillion debt

figure, the investment grade refinancing volumes in EMEA are

manageable within the normal capacity of capital markets.

(GulfBase.com)

Savola signs non-binding MoU to sell Savola Packaging to

Takween – Savola Group (Savola) has signed a non-binding

MoU to sell its entire share capital of Savola Packaging

Company to Takween Advanced Industries Company. The

proposed transaction is subject to various conditions and

approvals including, without limitation, Takween completing

5. Page 5 of 7

detailed due diligence on Savola Packaging to its reasonable

satisfaction, the negotiation & entry by Takween and Savola into

definitive agreements in relation to the proposed transaction, the

approval by each party board of directors as well as any

necessary shareholders and regulatory consents. HSBC Saudi

Arabia is acting as financial advisor to Takween for the

transaction. The MOU will be effective from the date of

signature, with an initial term of up to 16 weeks i.e., up to

November 11, 2014. (Tadawul)

Maaden to start commercial production of aluminum

smelter – Saudi Arabian Mining Company (Maaden) announced

that it will begin the commercial production of the aluminum

smelter at its subsidiary Maaden Aluminum Company (MAC) on

September 1, 2014. MAC is 74.9% owned by Maaden, and

25.1% owned by Alcoa – the aluminum Smelter is designed to

produce 740,000 tons per year. (Tadawul)

DHHC BoD approves expansion plan; to buy land plot for

SR97.5mn – Dallah Healthcare Holding Company’s (DHHC)

board of directors approved the company's expansion plan in its

own lands surrounding Dallah Hospital in Nakheel District,

Riyadh. This initial plan included developing three spots around

Dallah Hospital to include 150 beds, 60 clinics, housing and

services with an initial budgeted cost of SR500mn. On the same

day, the company’s board approved to buy a 6,300 square

meters land plot next to Dallah Hospital for SR97.5mn. The

move is part of the company’s plan to construct medical tower

including clinics, specialized medical centers, medical

commercial center and other facilities to be an extension of the

Dallah Hospital Complex. This project will be financed through

the company's operations and long-term Islamic financing.

(Tadawul)

Sobha Group in talks with banks for AED14.69bn project –

India-based developer Sobha Group is engaged in talks with

local and international banks to secure financing for its

AED14.69bn Sobha Hartland development in Dubai’s

Mohammad Bin Rashid City. The funding for the development

will come from a combination of internal cash and bank

financing. Work has already begun on the site with construction

underway on two schools in the new community. Sobha is

aiming to complete the phase one of the project by 1Q 2017,

while the entire development is scheduled to be completed by

2020. (GulfBase.com)

Damac’s latest project in Akoya sells out in one night –

Damac Properties’ latest project, which offers nearly 300 luxury

apartments in Loretto, located in Downtown Akoya, have been

sold out during a suhoor taking place in six venues across the

UAE in just one evening. More than 300 investors, from as far

as Saudi Arabia, Qatar, Kuwait, India, Pakistan, Russia and the

CIS countries, flocked to venues throughout the country to

capitalize on the strength and future growth of the Dubai real

estate market. The project, which will begin handing over units

in 2015, will be fully completed in 2018 and include hotels, hotel

apartments, a 1.3km outdoor retail strip, private park, schools

and hospitals. (GulfBase.com)

Mashreq Bank profit jumps 40% to AED1.16bn in 1H2014 –

Mashreq Bank reported a 40% increase in its net profit for

1H2014, climbing to AED1.16bn as compared to AED828mn in

1H2013. The net profit increased by 45% to AED585mn in

2Q2014 as compared to AED403mn in 2Q2013. The bank's net

interest income at the end of June 2014 increased by 38.1% to

AED1.44bn as compared to AED1.04bn a year earlier. EPS

strengthened to AED6.86 at the end of June 2014 as compared

to AED4.90 a year earlier. Mashreq’s total assets increased by

15.9% to reach AED103.9bn in June 2014 as compared to

AED89.7bn at the end of 2013. Loans & advances grew by

11.0% during 1H2014 to reach AED56bn, as compared to

AED50.4bn at the end of December 2013. Customer deposits

increased by 20.7%, during the same period to AED70.6bn at

the end of June 2014. (DFM)

DLD: Dubai real estate transactions for 1H2014 top

AED113bn – The Dubai Land Department (DLD) announced

that the total amount of real estate transactions recorded in

Dubai exceeded AED113bn in 1H2014. According to a financial

report issued by Real Estate Research and Studies Department,

sales accounted for 54% of the total transactions over the same

period, numbering 22,096 deals worth AED61.5bn. Sales

relating to land transactions accounted for the major share of

real estate transactions in 1H2014, amounting to AED35bn and

comprising 5,516 deals. Sales relating to units totaled

AED24.7bn for 15,997 transactions. Buildings transactions held

the third place with a figure of AED1.8bn, with the combined

total for all three categories being AED61.5bn. (Bloomberg)

CBRE: Dubai prime office rents surges 25% YoY – According

to the CBRE Group, 2Q 2014 office rents in Dubai’s Central

Business District (CBD) surged 25% YoY while it was up 3%

QoQ amid strong economic growth and rising business

confidence. Occupancy rates within prime CBD offices have

been rising steadily over the past 12 months, with less than 16%

vacancy rate as compared to an average of 40% vacancy for all

Dubai office stock. The supply of offices in Dubai will grow

significantly, with more than 1.8mn square meters to be

completed by the end of 2017. Almost 500,000 square meters of

office space is scheduled for completion in 2014, with more than

30% of that in the Business Bay area. (Bloomberg)

JLL: Abu Dhabi residential property prices up 17% in

1H2014 – According to Jones Lang LaSalle (JLL), sales prices

in Abu Dhabi’s residential property sector have increased by

average 17% in 1H2014. It was also the sixth successive

quarter of increases in sales prices for residential units, with a

7% rise over 2Q2014. Total residential stock in Abu Dhabi is

now around 240,000 units after 1,750 units were completed in

Reem Island, Danet Abu Dhabi and Al Reef during 2Q2014.

Rents in Abu Dhabi have increased following the recent removal

of the rental cap. JLL said that the increase has brought rent

prices in line with the current market levels. The average rent for

a two-bedroom increased by 3% in 2Q2014 to AED150,000,

according to JLL. The vacancy rate in Abu Dhabi office space is

expected to increase past its current rate of 30% due to

additional space scheduled to come online over the next two

years. However, office rental spaces remained unchanged in

2Q2014 with prime space averaging AED1,540 a square meter

and secondary space averaging AED1,180 a square meter. JLL

said the stock remains stable at 3.1mn square meters and there

were no major new deliveries between April and June.

Downward pressure on office rents is expected in 2014 with

130,000 square meters expected to enter the market in 2014.

Average line store retails rents for malls on Abu Dhabi Island

remained stable at AED3,000 a square meter as well as outside

Abu Dhabi at AED1,820 a square meter. The emirate’s total

retail stock is now 2.2mn square meters. Over 400,000 square

meters is expected to enter the market by the end of 2014. Hotel

occupancies year to May 2014 stood at 77% in Abu Dhabi. JLL

said the hotel market is expected to improve in 2H2014.

(GulfBase.com)

NBQ reports net profit of AED186.3mn in 1H2014 – National

Bank of Umm Al-Qaiwain (NBQ) reported a net profit of

AED186.3mn for 1H2014 as compared to AED184.7mn in

1H2013. Net profit for 2Q2014 declined to AED91mn as

compared to AED97mn in 2Q2013. EPS for 1H2014 remained

6. Page 6 of 7

flat at AED0.11 as compared to 1H2013. Net interest income for

1H2014 increased to AED224mn as compared to AED211mn in

1H2013. Total assets stood at AED12.56bn at the end of June

2014 as compared to AED12.54bn at the end of December

2013. Loans & advances stood at AED7.38bn, while customer

deposits amounted to AED7.49bn as of June 30, 2014. (ADX)

DI’s Marmum to export over 1.8mn liters Raha long-life

juices in 2014 – Marmum Dairy Farm (Marmum), a subsidiary

of Dubai Investments (DI), is planning to export over 1.8mn liters

of its Raha long-life juices across the Middle East and Africa in

2014. Marmum has set ambitious growth targets in exports with

plans to touch 3mn liters in exports by 2015 and 10mn liters by

2018. (DFM)

Jet Airways, Etihad unveil plans to reinforce commitment to

growth of India’s aviation industry – India-based Jet Airways

and Etihad have outlined plans to reinforce their long-term

commitment to the growth of India’s economy and aviation

industry, including a major new turnaround strategy for Jet

Airways to return to profitability in three years. Additionally, Jet

Airways mulls selling planes and restructuring its debts as it tries

to find ways to end the losses that have plagued it for years. The

Indian airline has lost a combined $1.3bn in the year to March

2014. (Reuters, Bloomberg)

ADPC: Abu Dhabi cargo shipments surged by 37% in

1H2014 – According to the Abu Dhabi Ports Company (ADPC),

general cargo moving through Abu Dhabi’s commercial ports

surged by 37% in 1H2014. ADPC’s commercial ports (Musaffah,

Khalifa, and Zayed Ports) handled 6.4mn freight tones (FT) of

general cargo in 1H2014 as compared to 4.7mn FT in 1H2013.

The increased volume is attributed to Abu Dhabi’s ongoing

economic growth, as well as ADPC’s work with key customers to

maximize their supply chain efficiencies. The company is

expecting to handle more than 12mn FT by the end 2014 as

compared to 9.5mn FT handled in 2013. (Bloomberg)

Ahli Bank reports net profit of OMR13.1mn in 1H2014 – Ahli

Bank reported a net profit of OMR13.1mn in 1H2014 as

compared to OMR12.5mn in 1H2013, reflecting an increase of

5%. The bank’s total assets have increased by 17% YoY to

OMR1.5bn at the end of June 2014, as compared to OMR1.3bn

at the end of June 2013. Loans & advances and financing

increased by 20% YoY to OMR1.25bn. Customer deposits rose

by 8% YoY to OMR996mn at the end of June 2014. (MSM)

NBK Bahrain reports net profit of $74.1mn in 1H2014 –

National Bank of Kuwait - Bahrain (NBK Bahrain) reported a net

profit of BHD74.1mn for 1H2014 as compared to BHD53.9mn

for 1H2013, indicating a growth of 38% YoY. The bank’s total

assets have increased by 19% to $9.2bn at the end of June

2014 as compared to $7.7bn at the end of December 2013.

Shareholders’ equity increased by 14% to $851.1mn as

compared to $745.6mn at the end of December 2013.

(GulfBase.com)

BHB announces change in GHF paid-up capital – Bahrain

Bourse (BHB) announced that the paid-up capital of Gulf

Finance House (GFH) has been increased due to the issuance

of 112,198,863 shares, pursuant to the approval from the

extraordinary general meeting held on April 14, 2014, and this

will be effective July 24, 2014. The previous total outstanding

shares was 3,161,889,967 & the new outstanding shares is

3,274,088,830, whereas the previous total paid-up capital was

$972.3mn and the new total paid up capital is $1bn. (Bahrain

Bourse)

CBB: Bahrain insurance premiums grow 8% – According to

the Central Bank of Bahrain (CBB), Bahrain’s insurance market

has posted a gross premium increase of 8% to BHD258.41mn in

2013, as compared to 2012. Motor insurance attributed a

significant part of this increase, with BHD68.05mn in 2013, up

10% from 2012. Medical insurance increased from BHD37.17mn

in 2012 to BHD40.83mn in 2013, also rising about 10% and

representing nearly 16% of the total premiums written in the

insurance market. The Takaful industry in Bahrain has

experienced a growth in gross contributions by 7% to

BHD57.22mn in 2013, with the gross contributions representing

around 22% of 2013. The total assets of insurance and takaful

firms in 2013 stood at BHD1,698.33mn as compared to BHD

1,613.28mn in 2012, up 5%. The gross premiums of reinsurance

and retakaful firms reached BHD336.57mn at the end of 2013

as compared to BHD312.12mn in 2012, indicating an increase

of around 8%. (Bloomberg)

7. Contacts

Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian

Head of Research Senior Research Analyst Senior Research Analyst

Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509

saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa

Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC

Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666

Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025

sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

200.0

210.0

Jul-10 Jul-11 Jul-12 Jul-13 Jul-14

QE Index S&P Pan Arab S&P GCC

1.4%

(0.5%)

0.3%

(0.2%)

0.2%

(0.3%) (0.2%)

(0.8%)

0.0%

0.8%

1.6%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,304.63 (0.1) (0.5) 8.2 DJ Industrial 17,086.63 (0.2) (0.1) 3.1

Silver/Ounce 20.92 (0.2) 0.2 7.4 S&P 500 1,987.01 0.2 0.4 7.5

Crude Oil (Brent)/Barrel (FM

Future)

108.03 0.7 0.7 (2.5) NASDAQ 100 4,473.70 0.4 0.9 7.1

Natural Gas (Henry

Hub)/MMBtu

3.79 (0.1) (3.0) (12.7) STOXX 600 342.86 0.1 0.9 4.4

LPG Propane (Arab Gulf)/Ton 104.38 0.4 0.8 (17.5) DAX 9,753.56 0.2 0.3 2.1

LPG Butane (Arab Gulf)/Ton 122.50 0.2 0.4 (9.8) FTSE 100 6,798.15 0.0 0.7 0.7

Euro 1.35 (0.0) (0.4) (2.0) CAC 40 4,376.32 0.2 0.9 1.9

Yen 101.48 0.0 0.1 (3.6) Nikkei 15,328.56 (0.1) 0.7 (5.9)

GBP 1.70 (0.1) (0.3) 2.9 MSCI EM 1,077.70 0.3 1.4 7.5

CHF 1.11 0.0 (0.4) (1.0) SHANGHAI SE Composite 2,078.49 0.1 0.9 (1.8)

AUD 0.95 0.7 0.7 6.0 HANG SENG 23,971.87 0.8 2.2 2.9

USD Index 80.82 0.1 0.4 1.0 BSE SENSEX 26,147.33 0.5 2.0 23.5

RUB 34.84 (0.4) (0.8) 6.0 Bovespa 57,419.96 (1.0) 0.7 11.5

BRL 0.45 (0.3) 0.3 6.5 RTS 1,272.02 0.4 (0.3) (11.8)

189.5

157.4

141.8