Top Rated Pune Call Girls Sinhagad Road ⟟ 6297143586 ⟟ Call Me For Genuine S...

28 January Daily market report

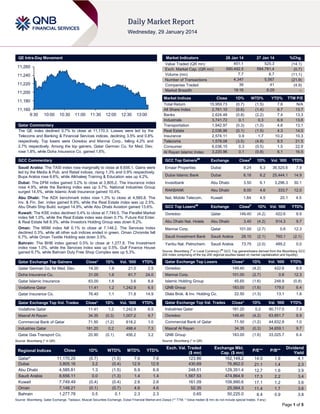

1. QE Intra-Day Movement

Market Indicators

11,260

11,240

11,220

11,200

Market Indices

11,180

11,160

9:30

28 Jan 14

451.1

590,492.5

7.7

4,347

39

19:16

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index declined 0.7% to close at 11,170.3. Losses were led by the

Telecoms and Banking & Financial Services indices, declining 3.5% and 0.8%

respectively. Top losers were Ooredoo and Mannai Corp., falling 4.2% and

2.7% respectively. Among the top gainers, Qatar German Co. for Med. Dev.

rose 1.8%, while Doha Insurance Co. gained 1.6%.

27 Jan 14

525.3

594,781.4

8.7

5,567

41

8:29

%Chg.

(14.1)

(0.7)

(11.1)

(21.9)

(4.9)

–

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

15,959.73

2,761.10

2,624.48

3,741.72

1,942.97

2,036.96

2,574.11

1,578.08

6,036.15

3,220.96

(0.7)

(0.6)

(0.8)

0.1

(0.3)

(0.1)

0.9

(3.5)

0.3

0.1

(1.5)

(1.4)

(2.2)

0.3

(1.0)

(1.5)

1.7

(4.8)

(0.5)

(0.8)

7.6

6.7

7.4

6.9

4.6

4.3

10.2

8.5

1.5

6.1

N/A

13.7

13.3

13.6

13.1

14.0

10.3

21.5

22.9

16.5

GCC Commentary

GCC Top Gainers##

Exchange

Close#

Saudi Arabia: The TASI index rose marginally to close at 8,656.1. Gains were

led by the Media & Pub. and Retail indices, rising 1.3% and 0.9% respectively.

Bupa Arabia rose 6.6%, while Alkhaleej Training & Education was up 4.2%.

Emaar Properties

1D%

Dubai

8.24

6.3

36,525.6

7.9

Dubai Islamic Bank

Dubai

6.16

6.2

25,444.1

14.9

Dubai: The DFM index gained 3.2% to close at 3,805.2. The Insurance index

rose 4.9%, while the Banking index was up 3.7%. National Industries Group

surged 14.5%, while Islamic Arab Insurance gained 10.4%.

Investbank

Abu Dhabi

3.50

6.1

3,296.3

30.1

RAKBANK

Abu Dhabi

8.00

4.6

333.7

12.0

Abu Dhabi: The ADX benchmark index rose 1.3% to close at 4,585.8. The

Inv. & Fin. Ser. index gained 8.9%, while the Real Estate index was up 2.5%.

Abu Dhabi Ship Build. surged 14.9%, while Abu Dhabi Aviation gained 13.6%.

Nat. Mobile Telecom.

Kuwait

1.84

4.5

20.1

4.5

GCC Top Losers

Exchange

Close

1D% Vol. ‘000

Kuwait: The KSE index declined 0.4% to close at 7,749.5. The Parallel Market

index fell 1.0%, while the Real Estate index was down 0.7%. Future Kid Enter.

& Real Estate fell 8.3%, while Investors Holding Group was down 8.2%.

Ooredoo

Qatar

149.40

(4.2)

422.6

8.9

Abu Dhabi Nat. Hotels

Abu Dhabi

3.40

(4.2)

914.3

9.7

Oman: The MSM index fell 0.1% to close at 7,148.2. The Services Index

declined 0.3%, while all other sub indices ended in green. Oman Chromite fell

6.7%, while Oman Textile Holding was down 3.5%.

Mannai Corp.

Qatar

101.00

(2.7)

0.6

12.3

Saudi Investment Bank

Saudi Arabia

28.10

(2.1)

760.1

(2.1)

Yanbu Nat. Petrochem.

Saudi Arabia

73.75

(2.0)

489.2

0.0

Bahrain: The BHB index gained 0.5% to close at 1,277.8. The Investment

index rose 1.0%, while the Services index was up 0.5%. Gulf Finance House

gained 6.7%, while Bahrain Duty Free Shop Complex was up 5.3%.

Qatar Exchange Top Gainers

Qatar German Co. for Med. Dev.

Close*

1D%

Vol. ‘000

YTD%

14.20

1.8

21.0

2.5

##

#

Vol. ‘000

YTD%

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers

Close*

1D%

Vol. ‘000

Ooredoo

149.40

(4.2)

422.6

8.9

Mannai Corp.

101.00

(2.7)

0.6

12.3

Doha Insurance Co.

31.00

1.6

81.7

24.0

Qatar Islamic Insurance

63.00

1.6

3.6

8.8

Islamic Holding Group

Vodafone Qatar

11.41

1.2

1,242.9

6.5

QNB Group

Qatar Insurance Co.

76.40

1.1

71.8

14.9

YTD%

45.65

Dlala Brok. & Inv. Holding Co.

(1.6)

248.9

(0.8)

183.00

(1.6)

179.0

6.4

22.50

(1.3)

13.1

1.8

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

Vodafone Qatar

11.41

1.2

1,242.9

6.5

Industries Qatar

181.20

0.2

90,717.0

7.3

Masraf Al Rayan

34.35

(0.3)

1,007.2

9.7

Ooredoo

149.40

(4.2)

63,851.7

8.9

Commercial Bank of Qatar

71.50

(1.2)

618.2

1.0

Commercial Bank of Qatar

71.50

(1.2)

44,632.8

1.0

181.20

0.2

498.4

7.3

Masraf Al Rayan

34.35

(0.3)

34,659.1

9.7

20.90

(0.1)

456.2

3.2

QNB Group

183.00

(1.6)

33,025.7

6.4

Qatar Exchange Top Vol. Trades

Industries Qatar

Qatar Gas Transport Co.

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Close

1D%

WTD%

MTD%

YTD%

11,170.25

3,805.16

4,585.81

8,656.11

7,749.49

7,148.21

1,277.78

(0.7)

3.2

1.3

0.0

(0.4)

(0.1)

0.5

(1.5)

(0.4)

(1.5)

(1.3)

(0.4)

(0.7)

0.1

7.6

12.9

6.9

1.4

2.6

4.6

2.3

7.6

12.9

6.9

1.4

2.6

4.6

2.3

Exch. Val. Traded

($ mn)

123.86

430.69

248.51

1,567.53

161.09

52.35

0.65

Exchange Mkt.

Cap. ($ mn)

162,149.2

76,862.0

129,351.4

474,864.9

109,990.6

25,564.3

50,225.0

P/E**

P/B**

14.0

21.1

12.7

17.3

17.1

11.4

8.4

1.9

1.4

1.6

2.2

1.2

1.7

0.9

Dividend

Yield

4.1

2.3

3.9

3.4

3.6

3.6

3.8

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 5

2. Qatar Market Commentary

The QE index declined 0.7% to close at 11,170.3. The Telecoms

and Banking & Financial Services indices led the losses. The

index declined on the back of selling pressure from non-Qatari

shareholders despite buying support from Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

49.19%

48.24%

4,313,187.38

Non-Qatari

Ooredoo and Mannai Corp. were the top losers, falling 4.2% and

2.7% respectively. Among the top gainers, Qatar German Co. for

Med. Dev. rose 1.8%, while Doha Insurance Co. gained 1.6%.

Buy %*

50.81%

51.76%

(4,313,187.38)

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Tuesday fell by 11.1% to 7.7mn

from 8.7mn on Monday. Further, as compared to the 30-day

moving average of 10.5mn, volume for the day was 26.1% lower.

Vodafone Qatar and Masraf Al Rayan were the most active

stocks, contributing 16.0% and 13.0% to the total volume

respectively.

Earnings and Global Economic Data

Earnings Releases

Company

Market

Currency

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

Abu Dhabi

AED

516.5

11.8%

–

–

42.2

-16.1%

Al Mazaya Holding Co.*

Al Maha Petroleum Products

Mar *

Shell Oman Marketing Co. *

Kuwait

AED

336.1

NA

–

–

77.6

1942.1%

Oman

OMR

318.5

4.5%

–

–

10.4

3.5%

Oman

OMR

430.6

6.7%

–

–

12.1

-1.6%

Oman Chromite *

Dhofar Beverages Food

Stuff *

Bahrain

Telecommunications Co.

(Batelco) *

Oman

OMR

2.2

9.9%

–

–

0.6

175.9%

Oman

OMR

4.5

3.7%

–

–

0.2

30.1%

Bahrain

BHD

370.6

21.6%

–

–

43.6

-27.7%

Al Ain Ahlia Insurance Co.*

Source: Company data, DFM, ADX, MSM (*FY2013 results)

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

01/28

US

US Census Bureau

Durable Goods Orders

December

-4.30%

1.80%

2.60%

01/28

US

S&P/Case-Shiller

S&P/CS 20 City MoM SA

November

0.88%

0.80%

1.05%

01/28

US

S&P/Case-Shiller

S&P/CS Composite-20 YoY

November

13.71%

13.80%

13.61%

01/28

US

S&P/Case-Shiller

S&P/CaseShiller Home Price Index

November

165.8

165.72

165.9

01/28

US

Conference Board

Consumer Confidence Index

January

80.7

78.0

77.5

01/28

US

Richmond Fed

Richmond Fed Manufact. Index

January

12

13

13

01/28

France

INSEE

Consumer Confidence

January

86

85

85

01/28

Germany

Destatis

Import Price Index MoM

December

0.00%

0.20%

0.10%

01/28

Germany

Destatis

Import Price Index YoY

December

-2.30%

-2.20%

-2.90%

01/28

UK

ONS

GDP QoQ

4Q2013

0.70%

0.70%

0.80%

01/28

UK

ONS

GDP YoY

4Q2013

2.80%

2.80%

1.90%

01/28

UK

ONS

Index of Services MoM

November

0.40%

0.30%

0.10%

01/28

UK

ONS

Index of Services 3M/3M

November

0.80%

0.70%

0.80%

01/28

Spain

INE

Total Mortgage Lending YoY

November

-26.90%

–

-15.50%

01/28

Spain

INE

House Mortgage Approvals YoY

November

-27.40%

–

-23.20%

01/28

Italy

ISTAT

Consumer Confidence Index

January

98.0

96.7

96.4

01/28

China

NBS

Industrial Profits YTD YoY

December

12.20%

–

13.20%

01/28

China

NBS

Leading Index

December

99.48

–

99.46

01/28

Japan

Shoko Chukin Bank

Small Business Confidence

January

51.3

–

51.1

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Page 2 of 5

3. News

Qatar

S&P: Lending growth in Qatar banks to recover in 2014 –

Standard & Poor’s expects lending growth in Qatar’s banking

industry to pick-up this year on the back of accelerated

infrastructure projects. S&P’s report stated that some projects in

Qatar faced administrative delays last year, but as they

accelerate in 2014, credit growth is expected to make a

commensurate recovery. Meanwhile, according to MEED, a

major overhaul of roads and highways is also under way with

Qatar’s Public Works Authority awarding seven contracts worth

QR10.1bn for a series of road projects across the country last

week. Two major contracts valued at $3bn are expected to be

awarded for the tunneling works for the Blue and Gold Lines of

the Doha Metro are expected. The award for the Gold Line is

expected in the first-quarter and the Blue Line around mid-year.

(Gulf-Times.com)

ABQK to rebalance its financing for retail thrust – Ahli Bank

(ABQK) is in the process of restructuring its retail segment and

rationalizing the branch network. Ahli Bank’s Deputy CEO for

Retail Banking Andrew Mckechnie said the bank is

contemplating recapitalizing as well as prospecting for premium

services. (Gulf-Times.com)

GDI, Oxy Qatar sign QR830mn rig deal – Gulf Drilling

International (GDI) has signed a new five-year contract worth

QR830mn with Occidental Petroleum of Qatar (Oxy Qatar). The

contract is for utilizing the jack-up drilling rig “Al Wajba”, which

will take effect on January 1, 2015 when the current contract

expires. (Gulf-Times.com)

QInvest, NBO to support sukuk issuance in Oman – QInvest

and the National Bank of Oman (NBO) will together support

local Omani entities by providing advisory and other solutions in

relation to sukuk issuance in that country. (Gulf-Times.com)

DOHI to hold AGM & EGM on February 17 – Doha Insurance

Company (DOHI) announced that its AGM and EGM are

scheduled to be held on February 17, 2014 at La Cigale Hotel.

In case of lack of quorum, the second meeting will be held on

February 23, 2014. The AGM’s agenda includes the board’s

proposal to distribute cash dividends of 20% from the share par

value, i.e. QR2.00 for each share to its shareholders. The

EGM’s agenda includes increasing the company’s capital by

(94.25%) from QR257mn to QR500mn by issuing 24.26mn

additional shares, constituting 9 shares for each 10 shares of

QR10 for each (nominal value) plus a premium of QR8 for each

share provided that priority is given to the owner of the share on

February 17, 2014. (QE)

gas liquids, LNG, gas-to-liquids products, and in gas cleanup in

upstream petrochemical/fertilizer manufacturing plants. (GulfTimes.com)

Contract awarded for Doha Festival City mall – The QR6bn

Doha Festival City has appointed the joint venture of Gulf

Contracting Company–Alec Qatar as the contractor to

commence foundation construction for the mall. Scheduled for

an opening in 3Q2016, the mall will be house over 550 outlets,

including many international brands that are making their debut

in Qatar. (Gulf-Times.com)

International

UK economy grows at fastest rate in six years in 2013 –

Britain's economy grew at its fastest rate in 2013 since the

global financial crisis. The UK’s Office for National Statistics said

barring construction and oil & gas extraction, all major sectors of

the country’s economy expanded in the final three months of

2013, concluding its best showing since 2007. The economy

grew 0.7% QoQ from October through December, in line with

forecasts. Growth for the full year rose to 1.9%. (Reuters)

Spain upgrades 2014 outlook, sees jobs growth – Spain has

predicted a faster-than-expected economic recovery and a net

job growth in 2014 as it emerges from five years of recession

with a 26% unemployment rate. Economy Minister Luis de

Guindos said Spain’s battered economy would generate jobs

growth next year, a first since a decade-long property bubble

imploded in 2008, ushering in a double-dip recession. De

Guindos said that in 2014, the Spanish economy will not only

grow, but it will also create jobs. He expects the country’s

economy to expand by about 1% in 2014, compared to an

official growth forecast of 0.7%. (Reuters)

India raises rates, says further tightening unlikely – India

has raised interest rates to dampen inflation, saying it is now

better prepared to deal with the risk of major capital outflows

that could harm emerging economies. However, the Reserve

Bank of India said that if retail inflation eases as projected, it

does not foresee further near-term monetary policy tightening.

The RBI raised its policy repo rate by 25 basis-points to 8%

amid market worries over slowing growth in China and the

prospect of further tapering of the US stimulus. (Reuters)

Regional

ORDS’s BoD to meet on March 4 – Ooredoo’s (ORDS) board

of directors will meet on March 4, 2014 to discuss the

company’s financial results ending on December 31, 2013. (QE)

S&P: GCC banks unaffected by US policy due to healthy

funding profiles – Standard & Poor's (S&P) considers banks in

GCC countries well positioned in a scenario where the US

moves to gradually normalize its monetary policy. S&P expects

the region's healthy economic growth prospects for 2014,

supported by high oil prices, to keep demand for bank credit

high and enable local banks to increase their earnings. In S&P’s

view, most banks in the key banking markets in the Gulf region

are likely to have healthy funding profiles with high-quality

capital in 2014. This will enable them to maintain their healthy

credit growth funded by liquid local deposit markets. Although

low interest rates continue to limit Gulf banks' net interest

margins, most banks have seen a gradual decline in loan

losses. S&P expect this to continue to support earnings growth

in 2014, but by less than in previous years. (GulfBase.com)

QP, Honeywell unit in research deal on gas purification –

Qatar Petroleum (QP) and UOP, a Honeywell company, have

signed a joint research agreement on Process Optimization of

carbon dioxide and sulfur components removal from natural

gases. The research’s primary aim is to efficiently utilize the

treated natural gases in further processing operations such as

transporting natural gas in pipelines, production of LPG, natural

Mauritania projects get $856mn investments from Arabs –

Mauritania has attracted funding worth $856mn from Arab

organizations at an international investment forum. These

investments – equivalent to almost a fifth of the country’s

economy – will pump funds into fisheries, agriculture, livestock,

health and roads, while funding imports from Arab countries to

the tune of $145mn. The Government of Mauritania has signed

Alijarah’s AGM & EGM to be held on February 12 – Alijarah

Holding announced that its AGM and EGM will be held on

February 12, 2014 at Regency. In case of lack of quorum,

second meeting will be held on February 17, 2014 at the same

place. The AGM’s agenda includes the board’s proposal for

distributing a cash dividend at the rate of 15% of the share

nominal value, which represents QR1.5 per share. (QE)

Page 3 of 5

4. five investment deals with the Saudi Development Fund, the

Rajihi Banking Group, the Arab Monetary Fund and the Arab

Institution for Agricultural Development. (GulfBase.com)

SFG to raise capital to SR12,000mn through bonus shares –

Samba Financial Group’s (SFG) board of directors has

recommended an increase in the company’s capital through

bonus shares. The company’s capital is to be raised to

SR12,000mn from SR9,000mn, with an increase by 33.33%.

The total number of issued shares will increase from 900mn to

1,200mn by offering 1 bonus share for every 3 shares owned.

The capital increase will be financed from the retained earnings

by transferring SR3,000mn. The bonus shares will be allotted to

registered shareholders at the close of trading on the

extraordinary general assembly day (to be announced).

(Tadawul)

Saudi CMA approves amendment to Swicorp’s business

profile – The Saudi Capital Market Authority (Saudi CMA) has

approved the amendment in the business profile of Swicorp

Company by adding discretionary portfolio management activity.

Swicorp is now authorized to conduct dealing as a principal

underwriting, investment fund management, discretionary

portfolio management, arranging, advising and custodial

activities. (Tadawul)

Emaar to convert $475.7mn bonds into shares – Emaar

Properties has received 75 notices of conversion from its

bondholders during the period from December 19, 2013 to

January 21, 2014. These bonds amount to $475.7mn, which will

be converted into 398,914,594 shares at a conversion price of

AED4.38 per share. As a result of this conversion, Emaar’s

share capital will be increased from AED6.1bn to AED6.51bn.

An application to that effect has been submitted to the Securities

& Commodities Authority, after getting approval from Emaar’s

shareholders. (DFM)

SKAI secures AED737.6mn of funding from ICBC – SKAI

Holdings announced that it has secured AED737.6mn worth

financing for its Viceroy Dubai Palm Jumeirah, which was

arranged by the Industrial & Commercial Bank of China (ICBC).

This ensured that the AED3.75bn project is fully funded. The

main structural works of the luxury residential and hospitality

project are currently underway, and are slated for completion in

2016. When completed, the project will offer 479 spacious

rooms and suites, and 222 signature Viceroy Residences with a

view of the Arabian Sea. (GulfBase.com)

New body DCTCM established to promote trade & tourism –

Dubai’s ruler HH Sheikh Mohammed bin Rashid Al Maktoum

has issued a decree establishing a new body, Dubai Corporation

for Tourism & Commerce Marketing (DCTCM). The new

corporation will be an affiliate of the Dubai Government’s

Department of Tourism & Commerce Marketing, which will be

responsible for the promotion and marketing of the Emirate.

DCTCM will establish effective partnerships with public and

private sector organizations related to tourism and commerce

sectors and work toward fostering trade relations with regional

and international companies in relevant industries. DCTCM will

also establish a new tourist information center in Dubai to

complement the current visitor information centers at Dubai

International Airport and Dubai Cruise Terminal. (GulfBase.com)

Emirates to move to new Dubai airport after 2020 – Emirates

Airlines is expected to move all of its operations to the new Al

Maktoum International Airport in Dubai after 2020. International

carriers have so far not indicated any plans to move to the new

airport, which officially launched passenger services in October

2013. (Reuters)

Technip wins key EPC contract from DPE – Technip has

obtained a contract from Dubai Petroleum Establishment (DPE)

for the engineering, procurement, construction and installation

(EPC) of the Jalilah B field development project. The field is

located 90 kilometers offshore Dubai. Technip’s scope of work

includes the construction and installation of the Jalilah B

platform, a 900-ton deck, a 500-ton jacket, as well as 13 new

risers on existing platforms. It also includes the installation of

110 kilometers of pipelines. This contract will use three of

Technip’s specialized vessels that are designed for work in both

deep and shallow waters. Technip’s operating center in Abu

Dhabi will execute this fast-track project scheduled for

completion in 2H2014. (GulfBase.com)

NBAD posts AED4.7bn net profit in 2013; appoints CFO –

The National Bank of Abu Dhabi (NBAD) has reported a net

profit of AED4.7bn in 2013, up 9.3% YoY. EPS stood at

AED1.04 in 2013 as compared to AED0.95 in 2012. Net profits

were up 4.0% to AED1.1bn in 4Q2013 versus AED1bn in

3Q2013, but were down by 3.9% as compared to 4Q2012. Net

interest income was higher by 6.8% to AED6.51bn in 2013

versus AED6.096bn in 2012. Total assets increased by 8% YoY

to AED325bn. Loans increased by 12% YoY to AED184bn in

2013 and customer deposits increased by 11% YoY to

AED211bn in 2013. Meanwhile, NBAD’s board of directors has

recommended dividend distribution of 40% in cash and 10% in

shares, which will be allotted to shareholders during the AGM

scheduled to be held on March 11, 2014. Meanwhile, sources

stated that NBAD has appointed James Burdett as the group’s

Chief Financial Officer. (GulfBase.com)

ADIB provides AED450mn finance to Al Dhafra – Abu Dhabi

Islamic Bank (ADIB) has granted Islamic finance facilities worth

AED450mn to Al Dhafra Cooperative Society for funding its

working capital and capital expenditure. The financing facility will

help Al Dhafra Cooperative Society implement numerous

projects for boosting economic and social development, in line

with the Abu Dhabi Government’s Western Region 2030

Strategy. (Gulfbase.com)

Gulf Bank posts KD32.16mn net profit in 2013 – Kuwaitbased Gulf Bank has reported a net profit of KD32.16mn,

reflecting 4% rise in 2013 as compared to KD30.89mn in 2012.

The bank would pay a dividend of 5% through an issue of bonus

shares. (Reuters)

Minimum share offer raised for new IWP projects – The

Omani government has raised the minimum percentage of

shares that an independent water and power company (IWP)

has to divest through an IPO on the Muscat Securities Market

from the current 35% to 40%. However, a top-level official of

Oman Power and Water Procurement Company stated that this

is applicable only for new IWP projects that include the

proposed Quriyat independent water project and the second

Salalah independent power venture. (GulfBase.com)

SOMC appoints new chairman – Shell Oman Marketing

Company (SOMC) announced that Chris Breeze has been

appointed as the non-executive Chairman of the Company. He

replaces John Blascos, the Chairman of SOMC, who has taken

up the new role of Vice President in the Shell Group in The

Hague, and has therefore resigned from the Board with effect

from January 28, 2014. (MSM)

PSC signs MoU with KAVEH – Port Services Corporation

(PSC) has signed a MoU with Kaveh Port & Marine Services

(KAVEH) to manage and operate the Port of Khasab in the

Musandam Governorate. (MSM)

Page 4 of 5

5. Rebased Performance

Daily Index Performance

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

138.5

4.0%

3.2%

3.2%

2.4%

1.3%

1.6%

126.3

0.8%

0.5%

0.0%

0.0%

May-13

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,256.88

(0.0)

(1.0)

4.2

DJ Industrial

15,928.56

0.6

0.3

(3.9)

19.58

(0.6)

(1.7)

0.6

S&P 500

1,792.50

0.6

0.1

(3.0)

107.41

0.7

(0.4)

(3.1)

NASDAQ 100

4,097.96

0.4

(0.7)

(1.9)

5.23

(8.2)

0.8

20.3

STOXX 600

324.22

0.7

(0.2)

(1.2)

152.75

1.2

0.8

20.8

DAX

9,406.91

0.6

0.2

(1.5)

154.00

0.3

0.2

13.4

FTSE 100

6,572.33

0.3

(1.4)

(2.6)

1.37

(0.0)

(0.1)

(0.5)

CAC 40

102.94

0.4

0.6

(2.3)

Nikkei

GBP

1.66

(0.0)

0.6

0.1

CHF

1.11

(0.1)

(0.3)

(0.5)

SHANGHAI SE Composite

AUD

0.88

0.5

1.1

(1.5)

USD Index

80.57

0.1

0.1

RUB

34.83

0.3

0.8

BRL

0.41

(0.2)

(1.1)

(2.6)

Yen

Dubai

Oct-12

Abu Dhabi

QE Index

Mar-12

Oman

Aug-11

(0.1%)

(0.4%)

Bahrain

Jan-11

(0.7%)

Qatar

(1.6%)

Kuwait

(0.8%)

Saudi Arabia

Jun-10

160.5

1.0

0.6

(2.6)

(0.2)

(2.7)

(8.0)

934.09

0.3

(1.7)

(6.8)

2,038.51

0.3

(0.8)

(3.7)

HANG SENG

21,960.64

(0.1)

(2.2)

(5.8)

0.7

BSE SENSEX

20,683.51

(0.1)

(2.1)

(2.3)

6.0

Bovespa

47,840.93

0.3

0.1

(7.1)

1,332.51

(1.0)

(2.3)

(7.6)

Source: Bloomberg

MSCI EM

4,185.29

14,980.16

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5