Vip Call US 📞 7738631006 ✅Call Girls In Sakinaka ( Mumbai )

9 March Daily market report

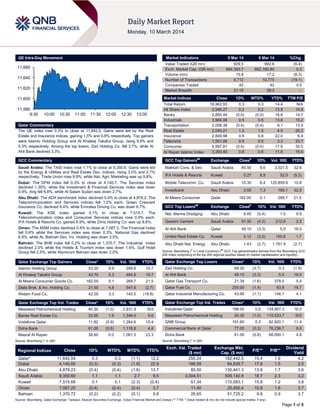

1. QE Intra-Day Movement

Market Indicators

11,660

11,640

11,620

Market Indices

11,600

11,580

9:30

9 Mar 14

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.3% to close at 11,642.0. Gains were led by the Real

Estate and Insurance indices, gaining 1.5% and 0.8% respectively. Top gainers

were Islamic Holding Group and Al Khaleej Takaful Group, rising 9.9% and

5.3% respectively. Among the top losers, Zad Holding Co. fell 3.7%, while Al

Ahli Bank declined 3.3%.

6 Mar 14

%Chg.

929.5

664,393.7

15.8

8,712

42

21:15

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

992.6

662,160.80

17.2

10,775

42

38:3

(6.4)

0.3

(8.3)

(19.1)

0.0

–

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

16,962.93

2,946.27

2,850.44

3,984.08

2,008.39

2,040.21

2,849.98

1,501.06

6,997.81

3,393.40

0.3

0.2

(0.0)

0.5

(0.4)

1.5

0.8

0.5

(0.4)

0.6

0.3

0.2

(0.0)

0.5

(0.4)

1.5

0.8

0.5

(0.4)

0.6

14.4

13.9

16.6

13.8

8.1

4.5

22.0

3.3

17.6

11.8

N/A

14.8

14.7

15.2

13.9

20.2

6.9

20.7

30.5

18.6

GCC Commentary

GCC Top Gainers##

Exchange

Saudi Arabia: The TASI index rose 1.1% to close at 9,350.6. Gains were led

by the Energy & Utilities and Real Estate Dev. indices, rising 3.0% and 2.7%

respectively. Trade Union rose 9.9%, while Nat. Agri. Marketing was up 9.8%.

Makkah Cons. & Dev.

Saudi Arabia

IFA Hotels & Resorts

Kuwait

Dubai: The DFM index fell 0.3% to close at 4,140.7. The Services index

declined 1.35%, while the Investment & Financial Services index was down

0.9%. Arig fell 6.8%, while Al Salam Sudan was down 2.7%.

Mobile Telecomm. Co.

Saudi Arabia

Investbank

Abu Dhabi

Abu Dhabi: The ADX benchmark index declined 0.4% to close at 4,878.2. The

Telecommunication and Services indices fell 1.2% each. Green Crescent

Insurance Co. declined 9.4%, while Emirates Driving Co. was down 6.7%.

Al Meera Consumer

GCC Top Losers

Exchange

Kuwait: The KSE index gained 0.1% to close at 7,515.7. The

Telecommunication index and Consumer Services indices rose 0.9% each.

IFA Hotels & Resorts Co. gained 8.9%, while Zima Holding Co. was up 8.8%.

Nat. Marine Dredging

Abu Dhabi

Qassim Cement

Oman: The MSM index declined 0.4% to close at 7,087.3. The Financial Index

fell 0.6% while the Services index was down 0.3%. National Gas declined

8.9%, while AL Batinah Dev. Inv. Holding was down 3.5%.

Bahrain: The BHB index fell 0.2% to close at 1,370.7. The Industrial Index

declined 2.0% while the Hotels & Tourism index was down 1.6%. Gulf Hotel

Group fell 2.5%, while Aluminum Bahrain was down 2.0%.

##

Close#

9.6

3,021.5

32.6

0.27

8.9

52.5

(5.3)

10.30

8.4

125,859.9

10.8

3.55

7.3

165.1

32.0

162.00

Qatar

1D%

85.50

5.1

268.7

21.5

#

Close

Vol. ‘000

1D% Vol. ‘000

YTD%

YTD%

9.45

(5.4)

1.0

9.9

Saudi Arabia

91.50

(4.2)

212.9

2.2

Al Ahli Bank

Qatar

49.10

(3.3)

5.0

16.0

United Real Estate Co.

Kuwait

0.12

(3.2)

150.8

1.7

Abu Dhabi Nat. Energy

Abu Dhabi

1.43

(2.7)

1,761.9

(2.7)

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Islamic Holding Group

Al Khaleej Takaful Group

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Vol. ‘000

YTD%

53.20

Qatar Exchange Top Gainers

9.9

299.8

15.7

Zad Holding Co.

68.20

(3.7)

0.3

(1.9)

19.7

Al Ahli Bank

49.10

(3.3)

5.0

16.0

43.70

5.3

484.8

Qatar Exchange Top Losers

162.00

5.1

268.7

21.5

Qatar Gas Transport Co.

Dlala Brok. & Inv. Holding Co.

21.50

4.6

547.6

(2.7)

Qatar Fuel Co.

Widam Food Co.

42.00

3.3

140.5

(18.8)

Al Meera Consumer Goods Co.

21.34

(1.6)

378.5

5.4

255.00

(1.4)

83.8

16.7

Qatar Industrial Manufacturing Co.

43.90

(1.1)

146.1

4.1

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

Mesaieed Petrochemical Holding

40.30

(1.0)

2,831.9

303

Industries Qatar

196.00

0.6

134,907.3

16.0

Barwa Real Estate Co.

32.65

1.9

1,349.9

9.6

Mesaieed Petrochemical Holding

40.30

(1.0)

115,533.7

303

Vodafone Qatar

11.82

(0.9)

1,264.6

10.4

191.60

0.3

82,920.1

11.4

Doha Bank

61.00

(0.8)

1,118.8

4.8

Commercial Bank of Qatar

77.00

(0.3)

76,236.7

8.8

Masraf Al Rayan

38.60

0.0

1,061.5

23.3

Doha Bank

61.00

(0.8)

68,090.1

4.8

Qatar Exchange Top Vol. Trades

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

QNB Group

Close

1D%

WTD%

MTD%

YTD%

11,642.04

4,140.65

4,878.23

9,350.60

7,515.68

7,087.25

1,370.72

0.3

(0.3)

(0.4)

1.1

0.1

(0.4)

(0.2)

0.3

(0.3)

(0.4)

1.1

0.1

(0.4)

(0.2)

(1.1)

(1.9)

(1.6)

2.7

(2.3)

(0.4)

(0.1)

12.2

22.9

13.7

9.5

(0.4)

3.7

9.8

Exch. Val. Traded

($ mn)

255.24

166.58

85.50

3,004.51

61.34

11.40

26.65

Exchange Mkt.

Cap. ($ mn)

182,442.5

84,639.7

130,441.3

509,140.9

110,083.1

25,450.4

51,725.2

P/E**

P/B**

15.4

17.8

13.8

18.7

15.8

10.8

9.8

1.9

1.5

1.7

2.3

1.2

1.6

0.9

Dividend

Yield

4.2

2.0

3.6

3.2

3.8

3.7

3.7

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 5

2. Qatar Market Commentary

The QE index rose 0.3% to close at 11,642.0. The Real Estate

and Insurance indices led the gains. The index rose on the back

of buying support from Qatari shareholders despite selling

pressure from non-Qatari shareholders.

Islamic Holding Group and Al Khaleej Takaful Group were the

top gainers, rising 9.9% and 5.3% respectively. Among the top

losers, Zad Holding Co. fell 3.7%, while Al Ahli Bank declined

3.3%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

67.15%

60.96%

57,562,472.78

Non-Qatari

32.85%

39.04%

(57,562,472.78)

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Sunday fell by 8.3% to 15.8mn from

17.2mn on Thursday. However, as compared to the 30-day

moving average of 12.9mn, volume for the day was 22.3%

higher. Mesaieed Petrochemical Holding and Barwa Real Estate

Co. were the most active stocks, contributing 17.9% and 8.5% to

the total volume respectively.

Earnings

Earnings Releases

Company

Gulf Live Stock *

Al Fujairah National

Insurance Co. *

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

AED

50.8

43.9%

–

–

42.9

45.4%

AED

116.7

1.8%

–

–

18.9

1.8%

Market

Currency

Abu Dhabi

Abu Dhabi

Source: Company data, DFM, ADX, MSM (*FY2013 results)

News

Qatar

IMF urges caution on inflation in Qatar – The International

Monetary Fund (IMF) has cautioned that although inflationary

pressures in Qatar appear to be contained at the moment,

policymakers need to remain vigilant. The authorities intend to

phase in investment projects gradually, keeping in mind Qatar's

2006-08 experience with double-digit inflation. However, if signs

of overheating emerge, the authorities need to smoothen out

fiscal spending, and deploy further macro-prudential measures

such as liquidity withdrawal operations in case of excessive

credit growth. IMF said that this strategy can be supplemented

by the authorities' efforts to identify and remove bottlenecks in

the supply chain. (Gulf-Times.com)

Qatar's budget surplus to reach QR40bn – Qatar's budget

surplus is expected to reach QR40bn by the end of the current

fiscal year. According to sources, the surplus stood QR27bn

during the second quarter. The country's GDP is expected to

touch QR200bn for the fourth quarter of the current fiscal year.

In the second and third quarters, it reached QR180bn and

QR185bn, respectively. Oil prices rose to $105 per barrel

against the budget assumption of $65 per barrel, which has led

to the significant surge in the surplus. The Ministry of Finance is

giving final touches to the 2014-15 budget. The ministry has

already received reports from various ministries and government

bodies regarding their projects for the new financial year.

(Peninsula Qatar)

ZHCD’s BoD to meet on March 25 – Zad Holding Company

(ZHCD) has announced that its board will meet on March 25,

2014 to discuss the company’s financial results ending

December 31, 2013. (QE)

MRDS’ BoD to meet on March 23 – Mazaya Qatar Real Estate

Development (MRDS) has announced that its board will meet on

March 23, 2014 to discuss the company’s financial statements

ending December 31, 2013. (QE)

Trading suspension in IQCD’s shares on March 10 – The

Qatar Exchange (QE) has announced suspension in the trading

of Industries Qatar Company’s (IQCD) shares on March 10,

2014 due to the company’s AGM being held on that day. (QE)

Barwa Bank names Subeai as acting CEO – Barwa Bank has

appointed Khalid Yousef al-Subeai as Acting Chief Executive

Officer. Khalid Al Subeai graduated from the University of

Arizona with a BA in Finance and has gone on to hold several

key positions within the finance sector in Qatar. Khalid has been

a Senior Financial Advisor at Qatar Petroleum (QP) for more

than six years. As part of the Project Finance team, he was

directly involved in the execution of over $15bn in landmark debt

capital market transactions for QP, its subsidiaries and the State

of Qatar. Subsequent to this, he moved on to hold the position of

Morgan Stanley Qatar Manager, where he was responsible for

Qatar Client Coverage. Khalid joined The First Investor (TFI) as

Deputy CEO in January 2013, and was then appointed acting

CEO of Barwa Bank Group in March 9, 2014. He brings with him

over nine years of Investment Banking experience with

knowledge of the local and international markets. (Barwa Bank,

Reuters)

MRDS appoints KEMCO to manage Tala Residence –

Mazaya Qatar Real Estate Development (MRDS) has appointed

KEMCO Maintenance & Services to manage their first project,

Tala Residence. The 346-unit Tala Residence housing project

has been developed for the employees of the Qatar National

Convention Centre under a MoU signed between MRDS and

Qatar Foundation for Education, Science & Community

Development. (Peninsula Qatar)

International

Collapse in exports, producer prices threaten China’s

growth target – The biggest drop in China’s exports since 2009

and a deepening factory-gate deflation highlight the challenges

faced by Chinese Premier Li Keqiang in achieving this year’s

economic growth target of 7.5%. Overseas shipments

unexpectedly declined 18.1% in February from a year earlier as

compared to analysts’ median estimate for a 7.5% increase.

Similarly, producer prices fell 2%, the most since July 2013,

extending the longest decline since 1999. Distortions from the

Page 2 of 5

3. Lunar New Year holiday and false invoices that inflated trade

numbers last year, along with a larger-than-projected increase in

imports, make it harder to assess the true picture of the global

and domestic demand for Chinese goods. Slowing consumerprice gains may give leaders more space to support growth as

they gauge the effects of the nation’s first onshore corporatebond default. (Bloomberg)

BIS: Global debt exceeds $100tn as governments binge –

The Bank for International Settlements (BIS) stated that the

amount of debt globally has soared 40% to reach $100tn since

the financial crisis, as governments borrowed to pull their

economies out of recession and companies took advantage of

record low interest rates. According to data compiled by

Bloomberg, the $30tn increase in debt since mid-2007, is in

contrast with a $3.86tn decline in the value of equities to $53.8tn

in the same period. The jump in debt as measured by Swissbased BIS in its quarterly review is almost twice the US' GDP.

Borrowing has soared as central banks suppress benchmark

interest rates to spur growth after the US subprime mortgage

market collapsed and Lehman Brothers Holdings Inc.'s

bankruptcy caused the worst financial crisis since the Great

Depression. As per the Bank of America Merrill Lynch's Global

Broad Market Index, yields on all types of bonds, from

governments to corporate and mortgages, average about 2%,

down from more than 4.8% in 2007. (Bloomberg)

BCC: UK economy to return to pre-recession peak soon –

According to the British Chambers of Commerce (BCC),

Britain's economy should exceed its pre-recession growth peak

in the next few months. BCC upgraded its forecasts for the fullyear GDP growth to reach 2.8% in 2014 and 2.5% in 2015, a

slight upgrade from its December forecasts. Unlike most its

developed economy peers, Britain's economy in 2013 was still

1.4% smaller than its pre-recession peak reached in early 2008.

The BCC said the economy will finally exceed that level in the

second quarter of this year. So far, the UK’s economic recovery

has been led by consumers and the housing market, and the

Bank of England has said business investment and exports

need to pick up for the recovery to be sustained. The BCC

expects 6.6% growth in business investment this year, followed

by 5.7% in 2015, but it warned that growth will remain below

pre-crisis levels for some time. (Reuters)

Japan’s economy expands less than initially estimated in

4Q2013 – Japan’s economy expanded less than estimated in

4Q2013 and its current account deficit widened to a record high

in January, highlighting risks to Abenomics as a sales-tax

increase looms. The Cabinet Office said that GDP grew at an

annualized 0.7% over the previous quarter, less than a

preliminary estimate of 1%. The finance ministry said the current

account deficit widened to $15.4bn, the highest since 1985.

While growth is set to surge this quarter before the bump in the

sales tax next month, Prime Minister Shinzo Abe’s task is to

steer the nation through a projected contraction in April-June

2014. The prime minister is due to publish detailed growth

measures in June, while economists forecast the Bank of Japan

to add to the unprecedented easing to keep the Japan’s

economy on track for a 2% inflation target. According to recent

data, business investment rose 0.8% from the previous quarter,

while onsumer spending increased 0.4%. (Bloomberg)

Regional

GCC insurance growth tops other economies, focus on

profit needed – According to insurance rating agency AM Best,

growth in the GCC insurance industry has outpaced that of other

developed and emerging economies, but insurers ought to focus

on profits than top line. Gross premiums written (GPW) in the

GCC had a CAGR of 21% during 2002-12, the same as Brazil

and China, while Russia was at 18% and India at 16%. AM Best

said a market growth of 21% enables companies to more easily

sustain the shocks associated with emerging markets. Growth in

the GCC will remain higher than in other developed markets but

lower than in the recent past, with a big portion of the premiums

still coming from motor and medical insurance. The rating

agency said that insurers will now have to focus on profitability

rather than top-line growth. (Gulf-Times.com)

DHC signs SR5.8mn deal for constructional excavation in

west Riyadh – Dallah Healthcare Holding Company (DHC) has

signed an agreement worth SR5.8mn for the constructional

excavation in its location in west Riyadh. This constructional

excavation is considered to be the beginning of the construction

of a new hospital in West Riyadh at a total cost of SR508mn.

Started on March 6, 2014, the project is expected to be

completed in two months from the signing of the agreement. The

company expects that construction will be completed, and the

hospital to begin operation in 2Q2016,. (Tadawul)

Almarai purchases farm land in Arizona for SR178.1mn –

Almarai Company has completed the purchase of farm land

spread over 9,834 acres in Vicksburg, in the US state of

Arizona, through its subsidiary Fondomonte, Arizona. The land

composes of 3,604 acres of freehold land, 3,080 acres of

agriculture lease-hold land and 3,150 acres of grazing leasehold land. The total consideration for this transaction amounts to

SR178.1mn, which will be financed from the company's own

resources. The resulting increase in property, plant and

equipment will be reflected in Almarai’s interim consolidated

financial statements for 1Q2014. (Tadawul)

Citymax plans 100 stores in Kingdom by mid-2014 – Citymax

is increasing its investment in the Saudi Arabian market, with the

opening of four stores in the first three months of 2014. Aiming

to have over 100 stores in Saudi Arabia by mid-2014, Citymax’s

investment plans reflect the company's confidence in the Saudi

retail sector. The new Citymax stores will feature the refurbished

Citymax branding with an updated design and interior layout.

The new stores will be located at Qatif & Dammam Corniche,

Abqaiq Mall, Aswak Al Qariah in Dammam, and at Max Yanbu,

Sabt Al Alaya, Red Sea Mall in Jeddah. In addition to the four

brand new stores, three existing stores in Jeddah and Dammam

will be relaunched with the new layout. (GulfBase.com)

Arabtec undertakes $40.23bn housing project in Egypt –

Arabtec Holding has been awarded a contract worth $40.23bn

by the Egyptian army to build 1mn houses across the country.

The project is seen as a major boost to the country of 85mn,

which has been struggling to attract tourists and foreign

investors, amid political turmoil, and saw its foreign reserves

drop to a critical low last year. The housing project to house

lower income individuals will cover 160mn square meters across

13 sites in Egypt. The company said it expects the project work

to start in 3Q2014 and be completed before 2020. (Reuters)

RTA awards AED100mn contract for Al Barsha roads – The

Roads & Transport Authority (RTA) has awarded a contract

worth about AED100mn to construct internal roads at Al Barsha

South 1, and collector roads at Al Barsha South 2. The project is

part of Phase II of the Five-Year Plan (2012-2016) endorsed by

the Ruler of Dubai Sheikh Mohammed bin Rashid Al Maktoum,

for constructing internal roads at several residential districts in

Dubai. The RTA’s Chairman & Executive Director Mattar Al

Tayer explained that the Five-Year Plan for constructing internal

roads in residential communities in Dubai spans across 16

districts where urbanisation rate ranges from 20% to 80%.

(GulfBase.com)

Page 3 of 5

4. Dubai’s trade growth moderates in 2013 – According to Dubai

customs data, Dubai’s non-oil trade expanded 7.6% in 2013,

slowing from 13% growth in 2012, but the Emirate’s trade with

Iran stabilized despite the US economic sanctions. Dubai’s nonoil foreign trade rose to AED1.329tn in 2013, while it exported

small amounts of oil and imported natural gas. Dubai’s non-oil

exports and re-exports climbed 4% to AED518bn, while imports

surged 10% to AED811bn. The Emirate saw its economy pick

up strongly last year as billions of dollars worth of new real

estate projects were announced following a lull after the 20082010 property market crash. Tourist numbers rose 10% to 11mn

people in 2013, while new trade licences recorded an increase

of 12%. The total value of real estate transactions jumped 53%

to AED236bn. (Gulf-Times.com)

Strata increases production in 2013 – Strata Manufacturing, a

subsidiary of Mubadala, increased its production quantity in

2013, albeit without any profit. The aerospace parts

manufacturing company, based in Al Ain, delivered 301 ship

sets to aircraft manufacturers in 2013, a 62.7% rise over 185

ship sets delivered in 2012. The production increase follows last

month’s release of the 2013 financial results where the company

reported revenue of AED20mn as compared to AED110mn in

2012. Strata stated that it invested AED1.2bn in 2013, 28%

more than the previous year, but the increase in revenue and

investment does not correlate to a profit margin. The company's

Chief Executive Badr Al Olama said that Strata has targeted to

be profitable by 2016-2017. For 2014, Strata stated that it is

targeting a revenue “in excess” of AED300mn and is looking to

deliver more than 400 ship sets. (Gulfbase.com)

of deposit (CDs) with an allotted amount of OMR698mn for the

issue No 587. CBO stated that the average interest rate of these

certificates was 0.12%, while the maximum accepted interest

rate was 0.13%. The tenor of these certificates is 28 days and

their maturity date is on April 2. The repo rate during March 5-11

stood at 1%. (GulfBase.com)

NCSI: Oman’s revenue drops 7.9% in January – According

the statistics released by the National Centre for Statistics &

Information (NCSI), the Omani government’s revenues fell by

7.9% at the end of January 2014 to OMR973.3mn against

OMR1,056.9mn recorded in January 2013. The statistics

attributed this to a 10.4% decline in Oman’s net oil revenues,

which stood at OMR829.5mn against OMR926.1mn. Gas

revenues rose by 14.1% to OMR105.5mn in January 2014

against OMR92.5mn in January 2013. Capital revenues

remained unchanged at OMR0.1mn. Similarly, other revenues

stood at OMR38.2mn during January 2014 as compared to

January 2013. (GulfBase.com)

NBAD to boost lending in Latin America by 20% – The

National Bank of Abu Dhabi (NBAD) plans to expand corporate

loans in Latin America by about 20% in 2014. The bank’s Chief

Representative in Brazil Angela Martins said that NBAD will

boost lending and offer other types of financial products to Latin

American companies that do business in countries that are

considered a priority, including those in the Far East, and the

MENA region. Martins said loans linked to Latin America are

expected to cross $720mn by the end of 2014. NBAD’s business

includes hedging, providing exchange-rate transactions for

currencies with low trading volume and distributing Latin

American loans and bonds in the Middle East. (Bloomberg)

Masirah Oil strikes oil at second well – Masirah Oil, an

associate of Malaysia-based Hibiscus Petroleum, said its

second exploration well has achieved a light oil flow rate of up to

3,000bpd in the Block 50 offshore concession area east of

Oman. Masirah Oil said that during a 48-hour test, hydrocarbons

flowed up to the surface and the well achieved oil flow with any

water production. The company said the test flow rates were

quite encouraging and that this was the first offshore oil

discovery in the east of Oman after more than 30 years of

exploration. (GulfBase.com)

KOTC gets delivery of two new tankers – Kuwait Oil Tankers

Company (KOTC) has received the delivery of two new oil

tankers as part of its revamping plan for its current fleet. The

delivery of the new tankers “Fintas” and “Burgan” fulfills the

company's third phase toward having a new fleet of at least nine

new tankers. Al-Fintas is the first of five tankers delivered by the

South Korean company Daewoo Shipbuilding & Marine

Engineering. The new tanker has a capacity of 2.2mn barrels of

oil, whereas Burgan’s capacity is approximately 340,000 barrels.

With the addition of the two new tankers, KOTC’s total fleet size

stands at 23. (GulfBase.com)

CBO declares result of OMR698mn CDs – The Central Bank

of Oman (CBO) has declared results of the tender for certificates

Page 4 of 5

5. Rebased Performance

Daily Index Performance

180.0

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

167.3

145.8

1.1%

0.8%

0.3%

0.4%

0.1%

132.7

0.0%

May-13

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

1,339.98

0.0

0.0

11.1

20.91

0.0

0.0

7.4

109.00

0.0

0.0

(1.6)

4.77

0.0

0.0

9.9

109.00

0.0

0.0

(13.7)

128.63

0.0

0.0

(5.8)

Global Indices Performance

Close

1D%

WTD%

YTD%

16,452.72

0.0

0.0

(0.7)

S&P 500

1,878.04

0.0

0.0

1.6

NASDAQ 100

4,336.22

0.0

0.0

3.8

333.06

0.0

0.0

1.5

DAX

9,350.75

0.0

0.0

(2.1)

FTSE 100

6,712.67

0.0

0.0

(0.5)

DJ Industrial

STOXX 600

1.39

0.0

0.0

1.0

103.28

0.0

0.0

(1.9)

GBP

1.67

0.0

0.0

0.9

MSCI EM

CHF

1.14

0.0

0.0

1.7

SHANGHAI SE Composite

AUD

0.91

0.0

0.0

1.7

USD Index

79.72

0.0

0.0

RUB

36.45

0.0

0.0

BRL

0.43

0.0

0.0

1.0

Yen

Dubai

Oct-12

Abu Dhabi

QE Index

Mar-12

(0.3%)

(0.4%) (0.4%)

Oman

Aug-11

Kuwait

Jan-11

Qatar

(0.8%)

Bahrain

(0.2%)

(0.4%)

Saudi Arabia

Jun-10

1.2%

CAC 40

Nikkei

4,366.42

0.0

0.0

1.6

15,274.07

0.0

0.0

(6.2)

966.72

0.0

0.0

(3.6)

2,057.91

0.0

0.0

(2.7)

HANG SENG

22,660.49

0.0

0.0

(2.8)

(0.4)

BSE SENSEX

21,919.79

0.0

0.0

3.5

10.9

Bovespa

46,244.07

0.0

0.0

(10.2)

1,158.87

0.0

0.0

(19.7)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5