QNBFS Daily Market Report November 28, 2018

•

0 j'aime•129 vues

The QSE Index declined marginally to close at 10,355.7

Recommandé

Recommandé

Contenu connexe

Plus de QNB Group

Plus de QNB Group (20)

Dernier

Dernier (20)

QNBFS Daily Market Report November 28, 2018

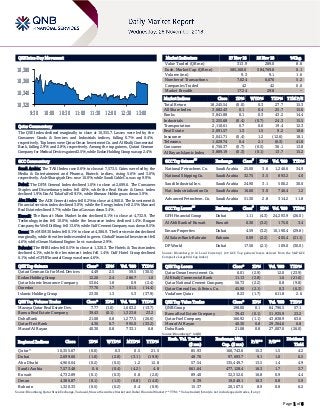

- 1. Page 1 of 6 QSE Intra-Day Movement Qatar Commentary The QSE Index declined marginally to close at 10,355.7. Losses were led by the Consumer Goods & Services and Industrials indices, falling 0.7% and 0.4%, respectively. Top losers were Qatar Oman Investment Co. and Al Khalij Commercial Bank, falling 2.9% and 2.8%, respectively. Among the top gainers, Qatari German Company for Medical Devices gained 2.5%, while Ezdan Holding Group was up 2.4%. GCC Commentary Saudi Arabia: The TASI Index rose 0.6% to close at 7,573.5. Gains were led by the Media & Entertainment and Pharma, Biotech. indices, rising 5.6% and 3.0%, respectively. Ash-Sharqiyah Dev. rose 10.0%, while Saudi Cable Co. was up 9.9%. Dubai: The DFM General Index declined 1.0% to close at 2,699.6. The Consumer Staples and Discretionary index fell 4.0%, while the Real Estate & Const. index declined 1.9%. Dar Al Takaful fell 9.1%, while Ithmaar Holding was down 5.9%. Abu Dhabi: The ADX General index fell 0.2% to close at 4,960.0. The Investment & Financial services index declined 3.0%, while the Energy index fell 2.5%. Manazel Real Estate declined 3.7%, while Dana Gas was down 3.4%. Kuwait: The Kuwait Main Market Index declined 0.1% to close at 4,732.9. The Technology index fell 10.0%, while the Insurance index declined 1.4%. Burgan Company for Well Drilling. fell 13.6%, while Gulf Cement Company was down 8.5%. Oman: The MSM 30 Index fell 0.1% to close at 4,386.9. The Services index declined marginally, while the other indices ended in green. Global Financial Investment fell 4.6%, while Oman National Engine. Invt. was down 2.9%. Bahrain: The BHB Index fell 0.5% to close at 1,320.3. The Hotels & Tourism index declined 4.1%, while the Investment index fell 1.4%. Gulf Hotel Group declined 6.1%, while GFH Financial Group was down 4.6%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Qatari German Co for Med. Devices 4.49 2.5 59.5 (30.5) Ezdan Holding Group 12.20 2.4 286.7 1.0 Qatar Islamic Insurance Company 53.64 1.8 0.9 (2.4) Ooredoo 77.70 1.7 101.5 (14.4) Islamic Holding Group 23.30 1.3 5.3 (37.9) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Mazaya Qatar Real Estate Dev. 7.77 (1.0) 1,603.2 (13.7) Barwa Real Estate Company 39.43 (0.1) 1,323.8 23.2 Doha Bank 21.08 0.8 1,277.5 (26.0) Qatar First Bank 4.36 0.7 995.0 (33.2) Masraf Al Rayan 40.30 0.8 733.1 6.8 Market Indicators 27 Nov 18 26 Nov 18 %Chg. Value Traded (QR mn) 313.9 289.0 8.6 Exch. Market Cap. (QR mn) 585,160.6 584,769.6 0.1 Volume (mn) 9.3 9.1 1.6 Number of Transactions 7,024 6,676 5.2 Companies Traded 42 42 0.0 Market Breadth 17:24 29:8 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 18,245.54 (0.0) 0.3 27.7 15.3 All Share Index 3,082.43 0.1 0.4 25.7 15.6 Banks 3,841.88 0.1 0.3 43.2 14.4 Industrials 3,255.68 (0.4) (0.7) 24.3 15.5 Transportation 2,110.61 0.7 0.6 19.4 12.3 Real Estate 2,091.57 1.3 1.5 9.2 18.8 Insurance 3,041.71 (0.4) 1.2 (12.6) 18.1 Telecoms 1,029.74 0.4 2.1 (6.3) 41.8 Consumer 6,756.37 (0.7) (0.5) 36.1 13.8 Al Rayan Islamic Index 3,889.19 (0.3) (0.1) 13.7 15.2 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% National Petrochem. Co. Saudi Arabia 25.00 3.6 1,246.6 34.9 National Shipping Co. Saudi Arabia 32.75 3.5 893.2 4.0 Saudi Industrial Inv. Saudi Arabia 24.90 3.1 506.2 30.0 Nat. Industrialization Co Saudi Arabia 16.60 3.0 746.4 1.2 Advanced Petrochem. Co. Saudi Arabia 51.30 2.8 314.2 11.8 GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% GFH Financial Group Dubai 1.11 (4.3) 24,293.9 (26.0) Al Ahli Bank of Kuwait Kuwait 0.30 (3.2) 175.0 3.4 Emaar Properties Dubai 4.59 (3.2) 10,190.4 (29.8) Al Salam Bank-Bahrain Bahrain 0.09 (2.2) 405.4 (21.1) DP World Dubai 17.50 (2.1) 109.0 (30.0) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Qatar Oman Investment Co. 6.01 (2.9) 12.0 (23.9) Al Khalij Commercial Bank 11.13 (2.8) 1.6 (21.6) Qatar National Cement Company 56.73 (2.2) 0.8 (9.8) Qatar General Ins. & Reins. Co. 45.90 (2.1) 0.3 (6.3) Vodafone Qatar 8.23 (1.7) 611.8 2.6 QSE Top Value Trades Close* 1D% Val. ‘000 YTD% QNB Group 198.00 0.1 64,796.5 57.1 Barwa Real Estate Company 39.43 (0.1) 51,935.9 23.2 Qatar Fuel Company 166.92 (1.1) 43,838.9 63.6 Masraf Al Rayan 40.30 0.8 29,364.6 6.8 Doha Bank 21.08 0.8 27,007.0 (26.0) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 10,355.67 (0.0) 0.3 0.5 21.5 85.93 160,743.6 15.3 1.5 4.2 Dubai 2,699.60 (1.0) (2.0) (3.1) (19.9) 48.76 97,693.7 9.1 1.0 6.5 Abu Dhabi 4,960.04 (0.2) (0.5) 1.2 12.8 57.54 135,449.7 13.5 1.4 4.9 Saudi Arabia 7,573.48 0.6 (0.4) (4.2) 4.8 661.64 477,128.4 16.3 1.7 3.7 Kuwait 4,732.89 (0.1) (0.3) 0.8 (2.0) 89.40 32,352.6 16.8 0.9 4.4 Oman 4,386.87 (0.1) (1.5) (0.8) (14.0) 6.39 19,048.1 10.3 0.8 5.9 Bahrain 1,320.33 (0.5) (0.2) 0.4 (0.9) 15.37 20,107.5 8.9 0.8 6.2 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any) 10,320 10,340 10,360 10,380 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 6 Qatar Market Commentary The QSE Index declined marginally to close at 10,355.7. The Consumer Goods & Services and Industrials indices led the losses. The index fell on the back of selling pressure from Qatari and GCC shareholders despite buying support from non-Qatari shareholders. Qatar Oman Investment Company and Al Khalij Commercial Bank were the top losers, falling 2.9% and 2.8%, respectively. Among the top gainers, Qatari German Company for Medical Devices gained 2.5%, while Ezdan Holding Group was up 2.4%. Volume of shares traded on Tuesday rose by 1.6% to 9.3mn from 9.1mn on Monday. Further, as compared to the 30-day moving average of 5.8mn, volume for the day was 60.3% higher. Mazaya Qatar Real Estate Development and Barwa Real Estate Company were the most active stocks, contributing 17.3% and 14.3% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 11/27 France INSEE National Statistics Office Consumer Confidence November 92 94 95 11/27 Japan Bank of Japan PPI Services YoY October 1.3% 1.2% 1.1% 11/27 China National Bureau of Statistics Industrial Profits YoY October 3.6% – 4.1% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar Qatar’s trade surplus rises to QR18.99bn YoY in October – Robust rise in the shipments of crude and non-crude helped Qatar more than double its trade surplus YoY to QR18.99bn in October 2018, according to official figures. The country's trade surplus registered a healthy 22.9% increase on monthly basis, showed the figures released by the Ministry of Development Planning and Statistics. In absolute terms, South Korea, Japan, India, China and Singapore were among the largest export markets of Qatar. Imports mainly came from the US, China, the UK, Germany and India in the review period. The exports of non-crude shot up 71% YoY to QR2.44bn, petroleum gases and other gaseous hydrocarbons rose by 48% to QR17.8bn, petroleum oils and oils obtained from bituminous minerals rose by 10.5% to QR4.56bn and other commodities increased by 3.8% to QR3.01bn. (Gulf-Times.com) GWCS well positioned to meet expectations of every demand – Gulf Warehousing Company (GWCS) has put forward every effort possible in order to provide logistics, supply chain services and solutions that serve every industrial and economic sector of Qatari economy. The company proactively enhanced its services and efficiency, especially after the blockade, to serve its clients better and more effectively. “GWCS is in-step with the needs and requirements of the market and its clients, and prides itself on its client focus and readiness to respond to any new opportunity or service gap. It accomplishes this through its widespread bespoke infrastructure that offers the end-to-end supply chain solutions and the technological foundation to meet and exceed the expectations of every demand”, GWCS’ CEO, Ranjeev Menon said. (Peninsula Qatar) QTerminals gets approval for Phase II expansion of Hamad Port – QTerminals announced that it has received approval to design, develop and operate Phase II (Container Terminal 2) of Hamad Port. The announcement comes as a major boost for the expansion of Hamad Port, which has become Qatar’s gateway to the world trade in a short span of time. QTerminals is a terminal operating company jointly established by Qatar Ports Management Company (Mwani) and Qatar Navigation (Milaha). The company provides container, general cargo, RORO (roll-on rolloff), livestock and offshore supply services in Phase 1 of Hamad Port. (Peninsula Qatar) Qatar Chamber signs agreement for report on the country’s energy business environment – Qatar Chamber has signed a strategic partnership with The Oil & Gas Year (TOGY) to launch the ‘TOGYiN’ platform report on Qatar’s attractive business environment in the field of energy and the local industry’s expansion plans. Both sides will partner for the upcoming ‘TOGY Qatar 2019’ edition, which will provide a thorough and comprehensive overview of Qatar’s hydrocarbon industry and related sectors. In a statement, Qatar Chamber stated it is honored to partner with TOGY in producing the ‘TOGY Qatar 2019’ edition, which gathers the opinions and views of the oil and gas elite in Qatar, as well as private-sector leaders. It noted that the report will promote Qatar as an oil and gas hub and an attractive investment destination worldwide, underscoring that the edition will have a vast readership of energy industry executives, decision makers and investors. Qatar Chamber added that the report aims to showcase the wealth of opportunities available in Qatar by featuring its friendly investment climate, economic strategies, and mega-projects and industries. (Gulf-Times.com) Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 26.74% 38.21% (36,027,772.51) Qatari Institutions 8.74% 25.09% (51,322,643.46) Qatari 35.48% 63.30% (87,350,415.97) GCC Individuals 0.36% 0.59% (714,788.77) GCC Institutions 0.15% 0.74% (1,836,189.41) GCC 0.51% 1.33% (2,550,978.18) Non-Qatari Individuals 6.13% 4.60% 4,800,536.70 Non-Qatari Institutions 57.88% 30.77% 85,100,857.45 Non-Qatari 64.01% 35.37% 89,901,394.15

- 3. Page 3 of 6 NTC to promote Qatar in Australian, Scandinavian markets – The National Tourism Council (NTC) is planning to promote Qatar in Australia and Scandinavian countries including Denmark, Finland, Iceland, Norway and Sweden by next year, as its next prospective target markets. NTC’s representative, Rashed Al Qurese mentioned the plan, while speaking at the official launch of ‘Qatar.Qurated for you’ — Qatar’s first global destination campaign, in which he underlined achievements in promoting Qatar since the easing of visa policies and the launch of ‘The Next Chapter of the National Tourism Sector Strategy’ last year. “After the launch of the strategy in 2017 we opened three of the world’s most important markets including China, India, and Russia. Next year we are going to work with our partners in order to venture in the Australian and Scandinavian markets,” Al Qurese said. Granting visa-free entry to citizens of more than 80 countries had made Qatar one of the most open countries in the Middle East and eighth worldwide according to UNWTO, which two-thirds of world population can visit visa- free, he stressed. (Peninsula Qatar) Malaysia offers Qatar opportunities in food processing, healthcare – Malaysia, which is expanding its halal industry, wants Qatar to participate in investment opportunities in the Southeast Asian country’s food processing sector, according to Deputy Prime Minister, Dato' Seri Dr Wan Azizah binti Wan Ismail. Ismail made the announcement during a high-level meeting organized by the Qatari Businessmen Association (QBA), where she and her accompanying delegation met with QBA’s Chairman, HE Sheikh Fasial bin Qassim Al-Thani and Qatar Chamber’s first Vice Chairman, Mohamed bin Towar Al- Kuwari, as well as other QBA officials and members. Aside from food processing, Ismail also encouraged Qatar to participate in the Southeast Asian country’s projects in the tourism and hospitality, aerospace, agriculture, healthcare, and industrial and manufacturing sectors. (Gulf-Times.com) SBCQ becomes official Chamber of Commerce of Spain in Qatar – An Extraordinary Assembly of the Spanish Business Council in Qatar (SBCQ) was convened at Doha Exhibition and Convention Center (DECC) in the past week to vote the approval of the changes in its Articles of Association to be established as the official Chamber of Commerce of Spain in Qatar. The Assembly was chaired by SBCQ’s Chairman, Jose Vicente and Ambassador of Spain to Qatar, Belen Alfaro Hernandez (Honorary Member). SBCQ was founded in 2009 with 7 Members. On the edge of its 10th birthday, the association has 56 members representing a wide spectrum of sectors including engineering Water Treatment companies, construction companies, naval construction, geotechnical works, facilities management and maintenance, management consultancy services, trading and contracting, law firms, and education, among others. It is now registered under the Qatar Financial Centre (QFC) umbrella. Although SBCQ has already been making incredible progress over years in promoting its business members and stretching ties between Spain and Qatar, a more powerful platform to keep on doing it was needed. On this regard Belen Alfaro pointed that “the SBCQ was now in position to be recognized as a Chamber of Commerce.” (Peninsula Qatar) International IEA: Global LNG trade projected to grow double in size by 2030 – Natural gas is set to become the second-largest fuel in the global energy mix, overtaking coal in 2030. Industrial consumers are expected to make the largest contribution to a 45% increase in worldwide gas use. Trade in liquefied natural gas (LNG) is expected to more than double in response to rising demand from developing economies, led by China. The ‘World Energy Outlook 2018’ released by International Energy Agency (IEA) noted the movement towards a more interconnected global gas market, as a result of growing trade in LNG, will intensify competition among suppliers while changing the way that countries need to think about managing potential shortfalls in supply. In the new policies scenario, rising incomes and an extra 1.7bn people, mostly added to urban areas in developing economies, will push up global energy demand by more than a quarter to 2040. The increase would be around twice as large if it were not for continued improvements in energy efficiency, a powerful policy tool to address energy security and sustainability concerns. All the growth is expected to come from developing economies, led by India. (Peninsula Qatar) UK’s retail sales improve in November – British retail sales perked up in November by more than expected, but stores’ confidence for the coming months deteriorated ahead of Brexit, an industry survey showed. The Confederation of British Industry’s (CBI) monthly retail sales balance rose to +19 from +5 in October. A Reuters poll of economists had pointed to a reading of +10. The survey was conducted before last week’s Black Friday promotions. While November’s pick-up was stronger than expected, other parts of the survey were less promising. Business expectations for the next three months cooled to their lowest level since May 2017. (Reuters) The UK government, BoE to spell out no-deal Brexit risks for economy – The British government and the Bank of England (BoE) are likely to step up their warnings of a hit to the economy from a no-deal Brexit, potentially helping Prime Minister, Theresa May to tackle deep opposition to her plan. Barely four months before Britain is due to leave the European Union (EU), May has failed to get much of her own Conservative Party behind the agreement sealed with EU leaders, leaving open the possibility of a no-deal Brexit. BoE’s Governor, Mark Carney and Finance Minister, Philip Hammond have both previously stressed the importance of a transition period, as included in May’s plan, to ease Britain out of its four- decade membership of the EU. (Reuters) French consumer confidence falls in November to lowest since February 2015 – French consumer confidence fell in November to its lowest level since February 2015, according to data from the official statistics agency, INSEE, another sign of sluggishness in the Eurozone’s second-biggest economy. The November reading for consumer confidence fell to 92 points from 95 in October. A Reuters poll of 8 economists had an average forecast of 94 points for the November level. (Reuters) Regional Islamic finance sees mixed growth, buoyed by capital market – The Islamic finance industry grew 11% YoY in 2017 and is set to sustain double-digit growth buoyed by capital market products and the adoption of financial technology, according to a

- 4. Page 4 of 6 Thomson Reuters study. The industry is now represented in 56 countries by 1,389 Shari’ah-compliant financial firms, worth a combined $2.4tn in assets, the study estimated. Islamic banks still retain the lion’s share of the industry, accounting for 71% of total assets, but their growth remained muted at 5%, with consolidation pressures mounting in its core markets of the Gulf and Southeast Asia. In contrast, capital market products such as Islamic bonds and investment funds fared better, posting 9% and 16% growth, respectively. (Reuters) Bloomberg survey: OPEC expected to cut production despite pressure from Trump – OPEC and its allies will announce production cuts to check a slump in oil prices when they meet next week, defying pressure from US President, Donald Trump, according to a Bloomberg survey. Thirty-one of 36 analysts and traders in a global poll predicted that the coalition of producers known as OPEC+, led by Saudi Arabia and Russia, will announce output curbs when it gathers on December 6 to 7. The average estimate for the size of the cut was 1.1mn bpd. Oil prices have collapsed 30% in less than two months on concern that booming US shale production and faltering demand - combined with unprecedented output from Saudi Arabia and Russia - will trigger a new surplus next year. (Gulf-Times.com) EY: MENA corporates seen cautious amid revenue, liquidity concerns and market uncertainties – A modest growth in revenues and a drop in liquidity position, driven largely by ongoing regional market uncertainties, led the Middle East and North African (MENA) corporates to adopt a cautious approach, according to Ernst and Young (EY). “While deal values are higher than 2017, the results of the latest EY Capital Confidence Barometer (CCB) show that one-third (33%) of MENA companies expect to pursue M&A (Mergers and Acquisitions) in the next 12 months, a 32% -point drop from a year ago. In the coming year we may see subdued deal activity and values,” MENA Transaction Advisory Services Leader, EY, Phil Gandier said. The value of the announced deals with disclosed value in the MENA region more than doubled YoY to $10bn in 3Q2018, according to the EY 3Q Mena M&A report. Deal value remained consistent; 107 deals were announced in 3Q2018 against 110 deals in 3Q2017, a decrease of 3%. The GCC deals represented 79% ($7.9bn) of the total MENA’s deal value, and 73% of the deal volume. (Gulf-Times.com) Saudi Aramco aims to become gas exporter with $150bn investment drive – Saudi Aramco’s gas expansion strategy needs $150bn worth of investments over the next decade as the company plans to increase output and become an exporter, its CEO, Amin Nasser said. Saudi Aramco is pushing ahead with its conventional and unconventional gas exploration and production program to feed its fast growing industries, freeing up more crude oil to export or turn into chemicals. Saudi Aramco plans to boost its gas production to 23bn standard cubic feet (scf) a day from 14bn scf now, he said. (Reuters) SABIC has team scouting for M&A deals – Saudi Basic Industries Corporation (SABIC) is targeting acquisitions and partnerships with oil majors as the petrochemicals giant seeks to expand in faster-growing markets such as China and India, according to CEO, Yousef Abdullah Al Benyan. The CEO has a team scouting for potential M&A targets and SABIC is regularly in talks with companies such as Royal Dutch Shell Plc about investing in joint ventures, he said in an interview. The plan builds on SABIC’s acquisition of 25% stake in Switzerland’s Clariant AG earlier this year, and Al Benyan plans to use the alliance to further develop a portfolio of specialty chemicals. The CEO said, “This is just the beginning, we want to be one of the top five specialty companies in order for us to maintain truly very strong competitive positions. We looked at different options. We cannot grow it just organically; we have to go through M&A activity.” (Bloomberg) Saudi Aramco sees chemicals deals beyond $70bn SABIC’s stake – Saudi Aramco will seek more acquisitions to speed its expansion in refining and petrochemicals as Saudi Arabia pushes ahead with plans to diversify its economy from reliance on sales of crude. The purchases will be in addition to Saudi Aramco’s planned purchase of government-controlled chemicals producer SABIC, according to Saudi Aramco’s CEO, Amin Nasser. The deal to buy the chemicals producer, known as SABIC, from the Saudi sovereign wealth fund (PIF) could be valued at about $70bn. “Saudi Aramco will make the most of those prospects with global investments in the chemicals space of roughly $100bn over the next 10 years in addition to prospective acquisitions,” Nasser said. The SABIC deal will help fund the project of creation of jobs by shifting funds from Saudi Aramco to the wealth fund. Nasser added, “The talk now is about 2021, more or less. You need to at least have one year of financial performance with SABIC shares reflected in our financial statements before we can go to the market to list Saudi Aramco.” (Bloomberg) Saudi Arabia raises SR4.78bn from three-tranche Sukuk sale – Saudi Arabia’s Ministry of Finance (MOF) completed a second tap offering of 2017-10 issuance under the Saudi Arabian Government Saudi Riyal-denominated Sukuk program. The MOF received SR10.33bn in bids for the Sukuk; it covered 216% of the total issue size. The Sukuk has been issued in three- tranches. The size of the first tranche was SR2.4bn maturing in 2022, the second tranche has been issued with a size of SR1.8bn maturing in 2024 and the third tranche has been issued with an issue size of SR475mn maturing in 2027. (Bloomberg) Almarai delays debut Dollar bond on Khashoggi fallout – Saudi Arabian dairy company Almarai has postponed a sale of international Islamic bonds because it faced having to pay a higher interest rate after the murder of Saudi journalist Jamal Khashoggi, according to sources. Almarai had hired banks to arrange the issue, but the deal, which would have marked Almarai’s debut in international debt markets, has been delayed to next year. The company was planning to issue a benchmark bond, which generally means upwards of $500mn, sources told Reuters. (Reuters) Banks in UAE look outside of their home turf to boost loan deals – Some of the UAE’s biggest banks are looking outside of their home turf to make up for relatively slow loan growth in the Gulf nation. First Abu Dhabi Bank, has participated in 51 syndicated loan deals overseas this year. Most of them were in Asia, where the bank is ranked 13th among foreign currency loan book runners, according to Bloomberg League Tables, up 10 places from this time last year. Lending by banks in the UAE, the second-biggest Arab economy after Saudi Arabia, has risen

- 5. Page 5 of 6 4.2% in the 10 months through October as the country recovers from two years of slowing economic growth. (Bloomberg) UAE’s rail project back on track with financing sealed – Etihad Rail, the developer and operator of the UAE’s national rail network, stated that the government has agreed financing for phase two of the project which was put on hold in 2016. The financing deal signals that the project is back on track after delays partly due to bureaucracy, technical difficulties and financing issues as the government slowed spending due to low oil prices. State-owned Etihad Rail had suspended the tendering process for phase two of the project in 2016, stating that it was reviewing options for the timing and delivery. Etihad Rail stated that the UAE Ministry of Finance and the Abu Dhabi Department of Finance signed the agreement to finance the second stage. The new railway will increase the volume of goods transported to more than 50mn tons from 7mn tons, it stated. (Reuters) Moody's: Sharjah's credit profile supported by UAE membership and low but rising debt burden – Sharjah's credit profile is supported by the Emirate's membership of the UAE’s, and its relatively high GDP per capita, as well as its low but rising government debt burden, modest fiscal deficits and low levels of wider public sector debt, Moody's Investors Service (Moody's) stated in a report. Its key credit challenges include the rise in government debt since the rating was assigned in 2014 and limited policy and data transparency. The narrow government revenue base is also a credit weakness, while the small size of Sharjah’s economy and close linkages with the rest of the UAE, particularly Dubai, exposes the Emirate to fluctuations in regional demand. (Bloomberg) Emaar Properties to divest stake in 5 hotels to Abu Dhabi National Hotels – Dubai’s Emaar Properties signed an accord to divest its interest in 5 Dubai hotels to Abu Dhabi National Hotels (ADNH). The transaction is expected to close in late 2018 or early 2019, Emaar Properties stated. It did not provide a value for the deal. As part of the accord, Abu Dhabi National Hotels will enter into long-term management agreements with Emaar Hospitality Group to continue operating the assets under its Address Hotels + Resorts and Vida Hotels & Resorts brands. The portfolio consists of Address Dubai Mall, Address Boulevard, Address Dubai Marina, Vida Downtown and Manzil Downtown. (Bloomberg) Emaar Properties picks Standard Chartered to advise on sale of hotel assets – Standard Chartered has been appointed as financial advisor by Emaar Properties on the sale of its hotel assets, the British lender stated. “The deal helps achieve strategic priorities and unlocks shareholder value for both Emaar and ADNH,” CEO of Standard Chartered Bank UAE, Rola Abu Manneh said. (Reuters) Dubai Aerospace authorized to buy back $300mn in bonds – Dubai Aerospace Enterprise (DAE) stated that its board and shareholders have authorized the repurchase of an additional $300mn of its bonds through open market transactions. “The current trading levels of our bonds are not consistent with our current credit ratings, strong financial performance or our projected ratings trajectory,” DAE’s CEO, Firoz Tarapore said. DAE stated it had already bought back $295mn of principal amount of its public bonds under a previous limit of $300mn. (Reuters) Brookfield to be in talks to invest in Dubai's Meraas Holding – Brookfield Asset Management Inc. (Brookfield) is in early talks for an investment in Dubai property developer Meraas Holding, according to sources. The Canadian firm is weighing options that would give it control of some retail properties from Meraas Holding, including entering into a joint venture for those developments. Brookfield is considering taking a stake in the state-run conglomerate as part of such a deal. The discussions are in preliminary stages and may not result in an accord. (Bloomberg) Honghua Group signs around $30mn land drilling rig contract with Kuwait Drilling Company – Honghua Group Ltd, a leading global land drilling rig manufacturer, announced that Honghua Golden Coast Equipment FZE (GCE), a wholly-owned subsidiary of the company, and Kuwait Drilling Company officially signed around $30mn sales contract for land drilling rigs with certain specifications. This contract is an additional sales contract between Honghua Golden Coast and Kuwait Drilling Company for land drilling rigs after 2016. At present, Honghua's number of rigs in the Kuwaiti market has increased to 23 sets. The cooperation reflects that Honghua's products have gained great recognition from clients and the market, which will benefit the company in expanding market share in Kuwait and consolidating the Group's leading position in the Middle East market. (Bloomberg) Oman sells OMR71mn 28-day bills at a yield of 2.283%; bid- cover at 1.07x – Oman sold OMR71mn of bills due December 26 on November 26. Investors offered to buy 1.07 times the amount of securities sold. The bills were sold at a price of 99.825, have a yield of 2.283% and will settle on November 28. (Bloomberg) Bahrain central bank considers new guidance for Islamic banks – Bahrain’s central bank is considering guidance covering Islamic windows, investment accounts and whether to develop a benchmark rate for use by Islamic banks, according to a senior executive. Bahrain’s regulator was the first to issue rules covering Shari’ah-compliant banking and insurance, and its efforts are often followed by other jurisdictions seeking to promote the sector. Bahrain’s central bank has already tightened governance rules for Islamic banks, requiring them to undergo independent external audits, and introduced a more stringent framework for the Shari’ah boards that vet their activities. (Reuters) Bahrain drilling two onshore wells in new gas discovery – Bahrain’s’ Oil Minister, Mohammed bin Khalifa Al Khalifa said, “Bahrain sees good prospects at natural gas find.” He added Bahrain is now drilling two onshore wells in new gas discovery. (Bloomberg) Ahli United Bank says talks still ongoing on merger with Kuwait Finance House – Bahrain-based Ahli United Bank stated to Kuwait Stock Exchange that talks are going on with respect to its merger with Kuwait Finance House (KFH). There have been no significant developments and consultations are still underway regarding valuation results of studies prepared by HSBC and Credit Suisse, the bank stated. (Bloomberg)

- 6. Contacts Saugata Sarkar, CFA, CAIA Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa QNB Financial Services Co. W.L.L. Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 6 of 6 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 45.0 70.0 95.0 120.0 Oct-14 Oct-15 Oct-16 Oct-17 Oct-18 QSE Index S&P Pan Arab S&P GCC 0.6% (0.0%) (0.1%) (0.5%) (0.1%) (0.2%) (1.0%)(1.4%) (0.7%) 0.0% 0.7% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,215.00 (0.6) (0.7) (6.8) MSCI World Index 2,000.07 0.0 1.3 (4.9) Silver/Ounce 14.14 (0.6) (1.0) (16.5) DJ Industrial 24,748.73 0.4 1.9 0.1 Crude Oil (Brent)/Barrel (FM Future) 60.21 (0.4) 2.4 (10.0) S&P 500 2,682.17 0.3 1.9 0.3 Crude Oil (WTI)/Barrel (FM Future) 51.56 (0.1) 2.3 (14.7) NASDAQ 100 7,082.70 0.0 2.1 2.6 Natural Gas (Henry Hub)/MMBtu 4.41 3.0 (6.2) 42.7 STOXX 600 357.40 (0.7) 0.5 (13.8) LPG Propane (Arab Gulf)/Ton 68.00 (1.4) (7.5) (31.3) DAX 11,309.11 (0.9) 0.6 (17.8) LPG Butane (Arab Gulf)/Ton 67.25 (4.6) (11.2) (38.0) FTSE 100 7,016.85 (0.9) 0.3 (14.1) Euro 1.13 (0.3) (0.4) (6.0) CAC 40 4,983.15 (0.7) 0.3 (12.0) Yen 113.79 0.2 0.7 1.0 Nikkei 21,952.40 0.4 0.7 (4.6) GBP 1.27 (0.6) (0.5) (5.7) MSCI EM 980.16 0.4 1.1 (15.4) CHF 1.00 (0.1) (0.1) (2.4) SHANGHAI SE Composite 2,574.68 (0.2) (0.2) (27.1) AUD 0.72 0.1 (0.1) (7.5) HANG SENG 26,331.96 (0.2) 1.5 (12.2) USD Index 97.37 0.3 0.5 5.7 BSE SENSEX 35,513.14 0.2 1.7 (6.1) RUB 67.09 (0.0) 1.3 16.4 Bovespa 87,891.18 3.1 (0.1) (2.3) BRL 0.26 1.7 (1.2) (14.5) RTS 1,098.59 1.3 (1.3) (4.8) 75.9 75.3 73.2