1.

Weekly Commentary

QNB Economics

economics@qnb.com.qa

25 August 2013

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report.

Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend on the individual

circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a complimentary basis. It may not be

reproduced in whole or in part without permission from QNB Group.

How to Get the Indian Tiger to Roar Again, According

to QNB Group

The rapid decline in India’s Rupee requires

structural reforms to sustain economic growth,

according to the QNB Group. India’s role as one of

the world’s growth engines is waning as the Rupee

declines rapidly and its economy shows increasing

signs of slowing down. The Indian Rupee has been

the worst-‐performing emerging market currency

since May 2013 against the backdrop of deepening

concerns over the authorities’ policies. Higher

interest rates and a liquidity squeeze, together

with the tightening of gold imports and capital

restrictions to reduce foreign exchange outflows,

have not stemmed the Rupee decline. According to

the QNB Group, such a policy response is merely

undermining the growth momentum in the

economy. A more appropriate response would be

to expedite the process of structural reforms that

could sustain economic growth over the medium

term. This would be similar to the first wave of

liberalization in the early 1990s engineered by

then Finance Minister Singh that led to two

decades of higher growth and lower poverty for

the Indian economy.

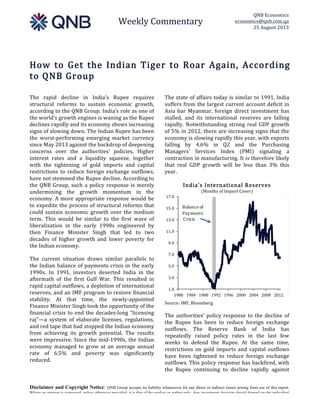

The current situation draws similar parallels to

the Indian balance of payments crisis in the early

1990s. In 1991, investors deserted India in the

aftermath of the first Gulf War. This resulted in

rapid capital outflows, a depletion of international

reserves, and an IMF program to restore financial

stability. At that time, the newly-‐appointed

Finance Minister Singh took the opportunity of the

financial crisis to end the decades-‐long “licensing

raj”—a system of elaborate licenses, regulations,

and red tape that had stopped the Indian economy

from achieving its growth potential. The results

were impressive. Since the mid-‐1990s, the Indian

economy managed to grow at an average annual

rate of 6.5% and poverty was significantly

reduced.

The state of affairs today is similar to 1991. India

suffers from the largest current account deficit in

Asia bar Myanmar, foreign direct investment has

stalled, and its international reserves are falling

rapidly. Notwithstanding strong real GDP growth

of 5% in 2012, there are increasing signs that the

economy is slowing rapidly this year, with exports

falling by 4.6% in Q2 and the Purchasing

Managers’ Services Index (PMI) signaling a

contraction in manufacturing. It is therefore likely

that real GDP growth will be less than 3% this

year.

India’s International Reserves

(Months of Import Cover)

Source: IMF, Bloomberg

The authorities’ policy response to the decline of

the Rupee has been to reduce foreign exchange

outflows. The Reserve Bank of India has

repeatedly raised policy rates in the last few

weeks to defend the Rupee. At the same time,

restrictions on gold imports and capital outflows

have been tightened to reduce foreign exchange

outflows. This policy response has backfired, with

the Rupee continuing to decline rapidly against

1.0

3.0

5.0

7.0

9.0

11.0

13.0

15.0

17.0

1980 1984 1988 1992 1996 2000 2004 2008 2012

Balance of

Payments

Crisis

2.

Weekly Commentary

QNB Economics

economics@qnb.com.qa

25 August 2013

Disclaimer and Copyright Notice: QNB Group accepts no liability whatsoever for any direct or indirect losses arising from use of this report.

Where an opinion is expressed, unless otherwise provided, it is that of the analyst or author only. Any investment decision should depend on the individual

circumstances of the investor and be based on specifically engaged investment advice. The report is distributed on a complimentary basis. It may not be

reproduced in whole or in part without permission from QNB Group.

the US dollar notwithstanding the highest yield on

Indian 10-‐yr bonds since 2008. Clearly, short-‐term

measures of this kind are not going to be enough

to restore confidence.

According to QNB Group, the origin of the rapid

decline in the Rupee is the ever-‐growing Indian

current account deficit over the last 10 years. The

widening deficit reflects a structural weakness in

Indian exports, which have stagnated since 2011,

while imports continue to grow at a rapid pace on

the back of higher domestic demand. This ever-‐

growing current account deficit was financed up

to April 2013 through higher capital inflows to

emerging markets (EM), which kept the Indian

Rupee relatively stable. Since then, however, there

has been a significant withdrawal of EM capital

flows reflecting concerns about the impact of a

possible tapering of Quantitative Easing in the US.

For India, this has exposed the underlying

unsustainable weakness of its current account

deficit, which can only be addressed through a

significant decline in the value of the Rupee. Such

a decline has already resulted in a jump in exports

in July. However, further declines will be

necessary in order to bring the current account

back to a sustainable level.

The underlying problem of the Indian economy is

therefore rooted in an uncompetitive export

sector, according to QNB Group. Only structural

reforms aimed at liberalizing the domestic

economy and reducing India’s still relatively high

cost of doing business can therefore restore

competitiveness and bring about higher economic

growth. This requires another wave of economic

liberalization as in 1991. Without such reforms,

the Indian tiger is unlikely to roar again.