QNBFS Daily Market Report November 27, 2016

•

1 j'aime•288 vues

The QSE Index declined 0.2% to close at 9,714.9.

Recommandé

Contenu connexe

En vedette

En vedette (8)

Plus de QNB Group

Plus de QNB Group (20)

Dernier

Dernier (20)

QNBFS Daily Market Report November 27, 2016

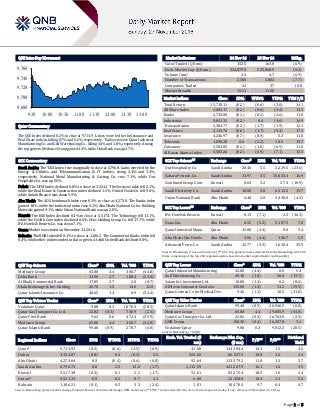

- 1. Page 1 of 5 QSE Intra-Day Movement Qatar Commentary The QSE Index declined 0.2% to close at 9,714.9. Losses were led by the Insurance and Real Estate indices, falling 0.7% and 0.6%, respectively. Top losers were Qatar Industrial Manufacturing Co. and Gulf Warehousing Co., falling 4.4% and 1.8%, respectively. Among the top gainers, Medicare Group gained 4.4%, while Doha Bank was up 2.7%. GCC Commentary Saudi Arabia: The TASI Index rose marginally to close at 6,796.8. Gains were led by the Energy & Utilities and Telecommunication & IT indices, rising 2.4% and 1.4%, respectively. National Metal Manufacturing & Casting Co. rose 7.1%, while Dur Hospitality Co. was up 5.5%. Dubai: The DFM Index declined 0.8% to close at 3,324.1. The Services index fell 2.1%, while the Real Estate & Construction index declined 1.2%. United Foods Co. fell 9.6%, while Amlak Finance was down 5.9%. Abu Dhabi: The ADX benchmark index rose 0.3% to close at 4,273.0. The Banks index gained 1.0%, while the Industrial index rose 0.2%. Abu Dhabi National Co. for Building Materials gained 9.1%, while Union National Bank was up 2.8%. Kuwait: The KSE Index declined 0.3% to close at 5,517.4. The Technology fell 13.1%, while the Health Care index declined 0.6%. Osos Holding Group Co. fell 17.7%, while IFA Hotels & Resorts Co. was down 7.1%. Oman: Market was closed on November 24, 2016. Bahrain: The BHB Index fell 0.1% to close at 1,186.2. The Commercial Banks index fell 0.4%, while other indices ended in flat or green. Al-Ahli United Bank declined 0.8%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Medicare Group 65.80 4.4 300.7 (44.8) Doha Bank 33.90 2.7 188.4 (23.8) Al Khalij Commercial Bank 17.85 2.7 2.0 (0.7) Dlala Brokerage & Inv. Holding 20.70 1.5 14.8 12.0 Qatar Islamic Insurance Co. 48.65 1.4 0.9 (32.4) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Vodafone Qatar 9.08 0.3 1,076.3 (28.5) Qatar Gas Transport Co. Ltd. 22.82 (0.3) 730.9 (2.3) Qatar First Bank 9.62 0.6 472.4 (35.9) Medicare Group 65.80 4.4 300.7 (44.8) Qatar Islamic Bank 99.40 (0.9) 270.7 (6.8) Market Indicators 24 Nov 16 23 Nov 16 %Chg. Value Traded (QR mn) 152.5 163.8 (6.9) Exch. Market Cap. (QR mn) 524,879.5 525,868.9 (0.2) Volume (mn) 4.3 4.7 (6.9) Number of Transactions 2,586 2,802 (7.7) Companies Traded 41 37 10.8 Market Breadth 15:21 11:20 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 15,718.11 (0.2) (0.6) (3.0) 14.1 All Share Index 2,683.17 (0.2) (0.6) (3.4) 13.2 Banks 2,733.08 (0.1) (0.2) (2.6) 11.8 Industrials 3,041.32 (0.2) 0.4 (4.6) 16.9 Transportation 2,384.77 (0.3) (1.7) (1.9) 12.2 Real Estate 2,115.70 (0.6) (1.7) (9.3) 17.3 Insurance 4,246.97 (0.7) (0.9) 5.3 11.0 Telecoms 1,090.28 0.6 (2.2) 10.5 19.7 Consumer 5,584.85 (0.2) (1.0) (6.9) 11.0 Al Rayan Islamic Index 3,583.26 (0.2) (0.9) (7.1) 15.5 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Dur Hospitality Co. Saudi Arabia 20.46 5.5 2,229.5 (23.6) Sahara Petroch. Co. Saudi Arabia 11.97 3.5 15,033.4 16.9 Combined Group Cont. Kuwait 0.64 3.2 27.4 (10.9) Saudi Electricity Co. Saudi Arabia 18.80 2.8 6,213.2 19.7 Union National Bank Abu Dhabi 4.48 2.8 4,338.0 (4.3) GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% IFA Hotels & Resorts Kuwait 0.13 (7.1) 2.5 (36.3) Dana Gas Abu Dhabi 0.55 (5.2) 5,107.9 7.8 Qatar Industrial Manu. Qatar 42.00 (4.4) 0.0 5.4 Abu Dhabi Nat. Hotels Abu Dhabi 3.06 (4.4) 106.7 5.5 Advanced Petro. Co. Saudi Arabia 42.77 (3.9) 1,030.4 35.9 Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Qatar Industrial Manufacturing 42.00 (4.4) 0.0 5.4 Gulf Warehousing Co. 49.10 (1.8) 50.4 (13.7) Salam Int. Investment Ltd. 10.80 (1.4) 6.2 (8.6) Al Meera Consumer Goods Co. 155.00 (1.3) 11.2 (29.5) Qatar German Co for Medical Dev. 9.46 (1.3) 10.5 (31.0) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Qatar Islamic Bank 99.40 (0.9) 26,946.5 (6.8) Medicare Group 65.80 4.4 19,805.9 (44.8) Qatar Gas Transport Co. Ltd. 22.82 (0.3) 16,763.8 (2.3) QNB Group 150.30 (0.4) 16,257.8 3.1 Vodafone Qatar 9.08 0.3 9,812.2 (28.5) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 9,714.93 (0.2) (0.6) (4.5) (6.9) 41.88 144,184.4 14.1 1.5 4.2 Dubai 3,324.07 (0.8) 0.4 (0.3) 5.5 324.65 86,527.5 10.8 1.2 4.1 Abu Dhabi 4,273.04 0.3 (0.4) (0.6) (0.8) 92.64 113,379.2 11.0 1.3 5.7 Saudi Arabia 6,796.75 0.0 2.5 13.0 (1.7) 2,112.59 423,267.9 16.1 1.6 3.5 Kuwait 5,517.38 (0.3) 0.1 2.2 (1.7) 52.01 83,275.4 18.5 1.0 4.4 Oman# 5,521.29 0.5 0.5 0.7 2.1 6.68 22,450.8 10.4 1.1 5.2 Bahrain 1,186.21 (0.1) 0.5 3.3 (2.4) 1.01 18,470.4 9.7 0.4 4.7 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, DFM and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any; #Data as of November 22, 2016.) 9,680 9,700 9,720 9,740 9,760 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 5 Qatar Market Commentary The QSE Index declined 0.2% to close at 9,714.9. The Insurance and Real Estate indices led the losses. The index fell on the back of selling pressure from Qatari and non-Qatari shareholders despite buying support from GCC shareholders. Qatar Industrial Manufacturing Co. and Gulf Warehousing Co. were the top losers, falling 4.4% and 1.8%, respectively. Among the top gainers, Medicare Group gained 4.4%, while Doha Bank was up 2.7%. Volume of shares traded on Thursday fell by 6.9% to 4.3mn from 4.7mn on Wednesday. Further, as compared to the 30-day moving average of 6.8mn, volume for the day was 36.5% lower. Vodafone Qatar and Qatar Gas Transport Co. Ltd. were the most active stocks, contributing 24.8% and 16.8% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings Releases and Global Economic Data Earnings Releases Company Market Currency Revenue (mn) 3Q2016 % Change YoY Operating Profit (mn) 3Q2016 % Change YoY Net Profit (mn) 3Q2016 % Change YoY International Financial Advisors Kuwait KD 8.0 61.3% – – -0.5 N/A Source: Company data, DFM, ADX, MSM Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 11/25 UK UK Office for National Statistics GDP QoQ 3Q2016 0.5% 0.5% 0.5% 11/25 UK UK Office for National Statistics GDP YoY 3Q2016 2.3% 2.3% 2.3% 11/25 UK UK Office for National Statistics Exports QoQ 3Q2016 0.7% 1.0% -1.0% 11/25 UK UK Office for National Statistics Imports QoQ 3Q2016 -1.5% -0.1% 1.3% 11/24 Germany German Federal Statistical Office Exports QoQ 3Q2016 -0.4% -0.3% 1.2% 11/24 Germany German Federal Statistical Office Imports QoQ 3Q2016 0.1% 0.3% -0.1% 11/24 Germany German Federal Statistical Office Government Spending QoQ 3Q2016 1.2% 0.6% 0.6% 11/24 France INSEE Manufacturing Confidence November 103.0 102.0 102.0 11/24 France French Labor Office Jobseekers Net Change October -11.7 -12.8 -66.3 11/25 France INSEE Consumer Confidence November 98.0 98.0 98.0 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar Qatar enjoys high hotel occupancy rates – Despite the addition of several hundred new hotel rooms over the last one year, Qatar’s hotel market occupancy rate is forecast to close at 66% in 2016, which is still higher compared to the occupancy rates in some GCC cities that are also heavy reliant on the corporate segment. According to a quarterly report titled: ‘Doha Q3 2016 Review’ released by Colliers International, a leading global real estate services company, the market performance of serviced apartments have remained relatively stable showing strong resilience during tough times when compared to the hotel segment. The country has witnessed an influx of more than 1,500 keys over the last one year, primarily in the 5-star segment. However, no new supply was introduced into the Doha market in Q32016. (Peninsula Qatar) Qatar’s $35bn foreign reserves to cover more than a year of imports – BMI Research said Qatar’s foreign reserves, currently estimated at $35bn, cover more than a year of imports and noted that the country’s current account deficit in 2016 poses little risk to its economic stability, with the deficit financed through its reserves and debt issuance. The Fitch Group company said in a report that Qatar’s current account will return to surplus in 2017, after posting its first deficit since 1998, estimated at 3% of GDP in 2016. The country will benefit from the recovery in hydrocarbon prices. Nonetheless, the surpluses will be modest over the coming years, given low energy prices by historical standards, strong demand for imported goods in the lead-up to the 2022 FIFA World Cup, and continuing remittances outflows. (Gulf-Times.com) Spain envoy sees signing of $1bn joint investment fund with Qatar in 2017 – Ambassador Ignacio Escobar said plans are underway for a high-level visit to Qatar by Spanish officials in 2017 where discussions would include strengthening of bilateral relations and the possible signing of a $1bn Spanish-Qatari joint investment fund. The ambassador said, “We have a number of deals that are in the pipeline. We are just waiting for an important bilateral visit to take place. We will have agreements on cooperation in defense, legal and judiciary, education, youth and sports, Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 25.58% 32.70% (10,862,966.46) Qatari Institutions 30.18% 32.85% (4,071,894.71) Qatari 55.76% 65.55% (14,934,861.17) GCC Individuals 0.90% 0.73% 266,615.90 GCC Institutions 12.59% 2.78% 14,951,615.17 GCC 13.49% 3.51% 15,218,231.07 Non-Qatari Individuals 11.24% 11.48% (354,566.43) Non-Qatari Institutions 19.51% 19.47% 71,196.53 Non-Qatari 30.75% 30.95% (283,369.90)

- 3. Page 3 of 5 telecommunications, media, and other sectors.” (Gulf- Times.com)Page-1 Oracle can help boost Qatari SMEs tech infrastructure – According to Group Vice President, Cloud Applications, Europe Middle East Africa and Latin America, Rajan Krishnan Qatar has one of the highest Internet penetration rates in the world. The country has 209 million Internet users with penetration rate of 91% and 1.7mn active social media users with a penetration rate of 70%. Qatar also has 4.73mn mobile phone users with Internet penetration rate of a whopping 209% with 66% of them being active social media users. Krishnan added that as Qatar is heading to FIFA World Cup 2022, there are many components where Oracle could offer technical services to develop the sectors, including transportation, logistics, events management and securities. Krishnan said Oracle has a long-standing history in Qatar and in the region, providing complete solutions that integrate all digital technologies including cloud, mobile, social, big data and Internet of Things with applications like middleware, database, analytics, and engineered systems. (Qatar Tribune) International UK firms show no Brexit vote hit in 3Q2016 as investment grows – British companies brushed off the uncertainty over Brexit in the three months after June's referendum and increased their investment, helping to drive solid growth in the economy. The Office for National Statistics said that business investment expanded at a quarterly rate of 0.9% in 3Q2016 beating expectations for a 0.6% rise in a Reuters poll of economists. Britain's economy overall grew by 0.5% in the third quarter, helped by a rebound in exports and robust household spending. A separate survey showed retail sales growing at the fastest pace in more than a year in November and suggested strong consumer spending will continue to drive the economy in 4Q2016. (Reuters) CBI: UK retail sales grow at fastest rate in over a year in November – A survey by the Confederation of British Industry showed that British retail sales grew at their fastest rate in more than a year earlier this month as colder weather continued to boost clothing sales. The CBI distributive trades survey's retail sales balance rose to +26 in November from October's reading of +21, its highest since September 2015 and far stronger than economists' expectations of a fall to +12 in a Reuters poll. British shoppers have shown little sign of retrenching spending since June's vote to leave the European Union, despite a sharp fall in sterling that looks set to push up prices early 2017. The CBI's expected sales balance for December also rose, while a broader quarterly measure of retailers' business situation was its healthiest since February. (Reuters) BBA: UK consumer credit grows at fastest pace in nearly 10 years – British consumer credit expanded last month at the fastest pace in nearly 10 years and mortgage approvals hit a five-month high. The British Bankers' Association figures underlined the strength of consumer demand since Britain voted to leave the European Union in June, although rising inflation and a slowing economy are expected to weigh on households in 2017. The BBA said that consumer credit increased at an annual rate of more than 7% in October, marking the strongest growth since November 2006. British banks approved 40,851 mortgages for house purchases last month, up from 38,690 in September and the biggest number since May. (Reuters) Japan’s CPI falls again, extending longest streak since 2011 – Japan’s consumer prices fell for an eighth straight month, the longest streak of declines since 2009-2011, underlining how distant the nation is from achieving its 2% inflation target. Consumer prices excluding fresh food, the Bank of Japan’s primary gauge of inflation, dropped 0.4% YoY in October. Overall consumer prices rose 0.1% with a spike in fresh food prices compensating for continued falls in energy costs. Consumer prices excluding food and energy rose 0.2 %. The continued fall in prices underscores the struggle to break a cycle that’s reinforced by weak gains in wages, poor consumer sentiment and retailers who compete fiercely through discounting. Even after Governor Haruhiko Kuroda pledged to overshoot the inflation target, households and companies have yet to fully shake off their deflationary mindset. (Bloomberg) Brazil to keep slow pace of rate cuts amid political turmoil – A Reuters poll showed that Brazil's central bank probably will continue cutting interest rates at a glacial pace next week despite a deepening recession as a new political scandal weakened the currency and cast doubts on austerity measures. All but 10 of the 61 economists surveyed by Reuters expect the central bank in its second consecutive meeting to trim the benchmark Selic rate by 25 basis points to 13.75%. The remainder forecast a 50-point cut. Data probably will show Brazil's historic recession deepened between July and September with a 0.8% seasonally adjusted drop. Economists said Brazil's currency slump to near five-month lows probably will discourage the central bank to cut interest rates faster, which would help rekindle growth. (Reuters) Regional Middle East tech companies pitch for $10mn as part of ‘cloud 10’ program – Seven young technology companies from the GCC region travelled to London, UK, last week to pitch for $10mn in front of a panel of investors as part of the Cloud 10 technology accelerator programmed or Escalator, powered by Amazon Web Services (AWS). The companies pitched to a panel of high profile international investors that included: Atkins Global, HSBC Private Bank, Standard Chartered Private Bank, C5 Family Offices and C5 Cloud Partners. (GulfBase.com) Saudi Arabia mining expands as Kingdom chases growth beyond Oil – Saudi Arabian Mining Co. plans to double gold production by 2020 and is increasing output of other commodities from aluminum to ammonia as the world’s biggest crude oil exporter seeks to diversify its economy. Chief Executive Officer Khaled Al Mudaifer said that gold output will be 500,000 ounces by 2020 from about 200,000 ounces in 2016. Aluminum production through a joint venture with Alcoa Corp. in the US has potential to increase to 1mn metric tons from 760,000 tons in 2016, through the use of recycled metal parts. Saudi Arabia wants to spur growth in the mining industry as it plans to create more jobs away from oil and increase revenue under the Saudi Vision 2030 program. According to the Vision 2030 document, the government aims for mining to contribute SR97bn to its economy by 2020 and create 90,000 jobs as a result. (Bloomberg) New regulations to facilitate growth in Saudi Arabia insurance sector – According to professional services organization EY, the insurance sector in the Kingdom of Saudi Arabia will find new opportunities for growth through the National Transformation Plan 2020 and Vision 2030 while simultaneously balancing business and profitability challenges. At the recent EY Jeddah Insurance Seminar held by the MENA insurance practice, EY experts discussed the opportunities and challenges facing the KSA insurance sector, along with the upcoming regulatory changes. (Bloomberg) Saudi Arabia banking sector liquidity improves after sovereign bond issue – The successful $17.5bn sovereign bond issue by Saudi Arabia in October has contributed to easier liquidity condition in the domestic banking system. While the monetary survey data for October is not yet available, it seems likely that at least a portion of the bond proceeds have been transferred to the domestic banking system, with both government and private sector deposits likely to

- 4. Page 4 of 5 have increased over the last few weeks. The government has also started paying contractors; with local press reporting around SR40bn of outstanding payments had been made by November 20, 2016. Another SR100bn of delayed payments is expected to be made by 2016. (Bloomberg) Saudi Arabia sinks Russia oil talks as OPEC deal hangs in the balance – Saudi Arabia pulled out of planned talks with non-OPEC nations including Russia as disagreements about how to share the burden of supply cuts stood in the way of a deal to boost prices just days before a make-or-break meeting in Vienna. OPEC officials were scheduled to meet with non-members including Russia tomorrow before a ministerial meeting in Vienna two days later. The meeting was later cancelled entirely after the Saudi Arabia‘s decided not to take part. According to the sources, instead, the group called another internal meeting to try to resolve its own differences, particularly the question of whether Iran and Iraq are willing to cut production. Saudi Arabia wants an OPEC deal in place before conversations with other producers such as Russia. (Gulf- Times.com) Mobily launches 30GB promo offer for SR300 – MOBILY provided a heavy Internet offer on (Connect 4G) packages, to meet customers’ need that have high rate of data usage. Under the new offer, all Connect 3 & 6 months subscribers will get 100GB data for SR300 and SR575. This offer will cover new and current subscribers to give them the flexibility of benefiting from this great offer. (GulfBase.com) Waha Capital sells key stake in New York firm – Waha Capital, a leading Abu Dhabi-based investment company, said it has extended collar hedges on 18.89mn shares for up to 43 months and also sold 4mn shares in New York-listed AerCap Holdings. AerCap’s share price was $45.46 at close of New York trading on November 22, 2016. These shares were acquired at an average price of $36.51 in an open market share purchase program announced in January. Top official said that the transactions serve to continue Waha Capital’s strategy of hedging its equity market exposure, while generating cash to pursue its growth strategy. (GulfBase.com) ADX CEO: VAT expected to benefit UAE bourses – According to a top spokesman from the Abu Dhabi bourse, the implementation of Value-Added Tax (VAT) in the UAE in 2018 is expected to benefit the country’s financial markets by boosting the earnings of publicly-listed companies. Rashed Al Beloushi, Chief Executive Officer of Abu Dhabi Securities Exchange (ADX), told reporters he was bullish on the impact of VAT on the UAE’s overall economy and on financial markets. (Bloomberg) Batelco launches Sophos security solutions – Bahrain-based Batelco, a top ICT business solutions provider and Sophos, a global leader in network and endpoint security, recently launched Sophos Security Solutions at an IT security workshop in the Kingdom. (GulfBase.com)

- 5. Contacts Saugata Sarkar Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa QNB Financial Services Co. WLL One Person Company Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. WLL One Person Company (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 5 of 5 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg (#Data as of November 22, 2016) Source: Bloomberg (#Market closed on November 25, 2016) Source: Bloomberg (*$ adjusted returns) 80.0 100.0 120.0 140.0 160.0 180.0 Oct-12 Oct-13 Oct-14 Oct-15 Oct-16 QSEI ndex S& PPanA r ab S& PGCC 0.0% (0.2%) (0.3%) (0.1%) 0.5% 0.3% (0.8%) (1.4%) (0.7%) 0.0% 0.7% SaudiArabia Qatar Kuwait Bahrain Oman# AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,183.90 (0.0) (2.0) 11.5 MSCI World Index 1,720.84 0.4 1.4 3.5 Silver/Ounce 16.53 1.3 (0.2) 19.3 DJ Industrial 19,152.14 0.4 1.5 9.9 Crude Oil (Brent)/Barrel (FM Future) 47.24 (3.6) 0.8 26.7 S&P 500 2,213.35 0.4 1.4 8.3 Crude Oil (WTI)/Barrel (FM Future) 46.06 (4.0) 0.8 24.4 NASDAQ 100 5,398.92 0.3 1.5 7.8 Natural Gas (Henry Hub)/MMBtu# 2.74 0.0 6.1 18.5 STOXX 600 342.45 0.5 1.0 (8.7) LPG Propane (Arab Gulf)/Ton# 54.13 0.0 3.3 41.0 DAX 10,699.27 0.5 0.4 (3.3) LPG Butane (Arab Gulf)/Ton# 74.00 0.0 6.3 34.3 FTSE 100 6,840.75 0.1 1.9 (7.4) Euro 1.06 0.3 0.0 (2.5) CAC 40 4,550.27 0.5 1.1 (4.3) Yen 113.22 (0.1) 2.1 (5.8) Nikkei 18,381.22 0.4 0.1 2.9 GBP 1.25 0.2 1.1 (15.3) MSCI EM 855.78 0.4 1.3 7.8 CHF 0.99 0.2 (0.5) (1.2) SHANGHAI SE Composite 3,261.94 0.8 1.8 (13.5) AUD 0.74 0.5 1.4 2.2 HANG SENG 22,723.45 0.5 1.7 3.6 USD Index 101.49 (0.2) 0.3 2.9 BSE SENSEX 26,316.34 2.0 (0.0) (2.7) RUB 64.83 0.5 (0.2) (10.6) Bovespa 61,559.08 (0.4) 1.7 64.3 BRL 0.29 (0.9) (1.2) 15.7 RTS 1,018.51 (1.0) 2.8 34.5 114.0 100.7 96.7