Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à Panama Canal Expansion & its Huge Significance for US Trade, Ports, Railways, Supply Chains, Cities & Investors

Similaire à Panama Canal Expansion & its Huge Significance for US Trade, Ports, Railways, Supply Chains, Cities & Investors (20)

Dernier

Dernier (20)

Panama Canal Expansion & its Huge Significance for US Trade, Ports, Railways, Supply Chains, Cities & Investors

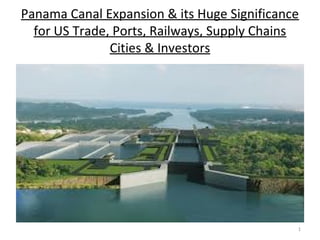

- 1. Panama Canal Expansion & its Huge Significance for US Trade, Ports, Railways, Supply Chains Cities & Investors 1

- 3. LEGAL DISCLAIMER • THISISNOT AN OFFERING OR THE SOLICITATION OF AN OFFER TO PURCHASE AN INTEREST IN GENESISHOUSING FUND, L.P. (THE “FUND”). ANY SUCH OFFER OR SOLICITATION WILL ONLY BE MADE TO QUALIFIED INVESTORSBY MEANSOF A CONFIDENTIAL PRIVATE PLACEMENT MEMORANDUM (THE “MEMORANDUM”) AND ONLY IN THOSE JURISDICTIONSWHERE PERMITTED BY LAW. AN INVESTMENT SHOULD ONLY BE MADE AFTER CAREFUL REVIEW OF THE FUND’SMEMORANDUM. THE INFORMATION HEREIN ISQUALIFIED IN ITSENTIRETY BY THE INFORMATION IN THE MEMORANDUM. • AN INVESTMENT IN THE FUND ISSPECULATIVE AND INVOLVESA HIGH DEGREE OF RISK. OPPORTUNITIESFOR WITHDRAWAL, REDEMPTION AND TRANSFERABILITY OF INTERESTS ARE RESTRICTED, SO INVESTORSMAY NOT HAVE ACCESSTO CAPITAL WHEN IT IS NEEDED. THERE ISNO SECONDARY MARKET FOR THE INTERESTSAND NONE IS EXPECTED TO DEVELOP. NO ASSURANCE CAN BE GIVEN THAT THE INVESTMENT OBJECTIVE WILL BE ACHIEVED OR THAT AN INVESTOR WILL RECEIVE A RETURN OF ALL OR ANY PORTION OF HISOR HER INVESTMENT IN THE FUND. INVESTMENT RESULTSMAY VARY SUBSTANTIALLY OVER ANY GIVEN TIME PERIOD. • CERTAIN DATA CONTAINED HEREIN ISBASED ON INFORMATION OBTAINED FROM SOURCESBELIEVED TO BE ACCURATE, BUT WE CANNOT GUARANTEE THE ACCURACY OF SUCH INFORMATION. • REFERENCESTO SPECIFIC GEOGRAPHIC LOCATIONSAND PROPERTIESLOCATED THEREIN ARE PRESENTED TO ILLUSTRATE THE APPLICATION OF OUR INVESTMENT PHILOSOPHY ONLY AND ARE NOT INTENDED TO BE CONSIDERED RECOMMENDATIONSBY SHYAM REAL ESTATE, LLC. THE SPECIFIC LOCATIONSAND PROPERTIESIDENTIFIED AND DESCRIBED IN THISPRESENTATION DO NOT REPRESENT PROPERTIESACTUALLY PURCHASED, SOLD OR RECOMMENDED FOR THE FUND, AND IT SHOULD NOT BE ASSUMED THAT INVESTMENTSIN THE PROPERTIESIDENTIFIED WILL BE PROFITABLE. 3

- 4. Panama Canal Expansion • Panama Canal $5.2bn expansion project to be completed end 14/ early 15 • Currently 14,000 ships pass the Panama Canal transiting 275m tons, annual throughput capacity to increase to 600m tons post Expansion • Currently Panamax Ships with capacity limit of 4,800 TEU (20 ft container units) can pass the Panama Canal’s current locks • After expansion Post & Super Post Panamax Ships up to 12,500 TEU will be able to pass, 160% increase in capacity of ships that can pass the Canal. Hugely Significant for Global Freight, Global Trade Routes, US Ports, US Supply Chains, US Cities, Warehousing, Distribution Centers, Manufacturing bases, Industrial & Residential Real Estate, Railways, Truckers… 4

- 5. 5

- 6. Panama Canal Expansion Huge increase in ships that can travel through expanded Panama Canal: 1) Post Panamax Container ships which represent 50% of world’s total container shipping capacity 2) Crude Oil Tankers that represent up to 40% of world’s capacity 3) LNG tankers that represent 90% of global capacity 4) Dry Bulk Carriers that represent 80% of global capacity Expansion plays into trend of larger container ships displacing smaller ships Note in 2000 Average Ship Size was 2,900 TEU, in 2012 was 6,100. With 50% of ships on order 10,000 TEU+ this is set to continue due to large Economies of scale available in using larger ships 6

- 7. Implications for US • Expansion will open up Gulf and East Coast Ports to significantly more trade & accelerate traffic growth given that larger vessels & a larger proportion of global shipping fleet will be able to transit the Canal. • Currently 80% of Asian Imports into the US come via West Coast ports ; set to change significantly given accessibility of larger ships to the Gulf / East Coast Ports & Population Centers. • Efficiency Gains & Costs Savings will be available by shipping directly to East coast and Gulf ports to access Mid-West and East Coast population centers. • Shippers will be able to bypass often congested West Coast ports to ship directly to Gulf & East coast region 7

- 8. 8

- 9. 9

- 10. Implications for US • Average Freight Transit Times: Asia to West Coast US 12.3 days by ship, Transit time from West Coast to East Coast via US intermodal system another 6 days so 18.3 days in total. • Asia to East Coast directly via Ship using Panama Canal 21.6 days. More time BUT Cost efficiencies as all water route • Reliability of shipping from Asia to East coast via Panama Canal is another major competitive advantage versus shipping to West coast & using inter-model system to reach East Coast. Schedule Reliability is very important for shippers & their customers. • Expansion will relieve congestion at the Canal which raises costs for shippers & customers. During peak season it is not uncommon for vessels to wait 10 days to transit canal at cost of $50,000 idle cost per day 10

- 11. 11 Transit times for freight from Asia to US cities by ship & intermodal system

- 12. Implications for US Ports • East & Gulf Coast Ports are gearing up to be Post Panamax Ready; defined as a channel depth of 50 feet net of usable tide, as well as sufficient docking & crane facilities • East Coast & Gulf coast ports & railroads are deepening harbors, raising bridges, improving tunnels & railways, increasing dock facilities, installing new cranes to accommodate larger ships & much greater cargo volumes • Most competitive regions, ports & systems will end up with the greatest cargo… stealth arms race underway leading to increased investment • East Coast Ports most likely to benefit will be those serving ‘as interstate retail distribution centers for Asian imports such as Norfolk, Charleston & Savannah’ quote from US Army Engineer Institute for Water Resources 12

- 13. 13 Current Channel Depths at Selected Ports: 50 feet is required for Post Pananamax Ships

- 14. 14 US Primary and Secondary Ports

- 15. Select US East / Gulf Ports ready for larger vessels by 2015 • New York / New Jersey: 2nd busiest US port with 5.6m TEU p.a. At 50 foot depth already, will be ready once Bayonne Bridge lifted to 215 feet to accommodate post Panamax ships • Norfolk, Virginia: 7th busiest US container port with 2m TEU p.a. Currently Post Panamax ready • Baltimore, Maryland: Currently Post Panamax Ready. 650k TEU p.a • Charleston, South Carolina: 9th busiest US container port with 1.35m TEU p.a. At high tide can accommodate ships with 50 feet draft so technically already ready. • Houston, Texas: 2.1m TEU containers p.a & important for bulks & petrochemicals • Mobile, Alabama: Important for bulks transited down via Mississippi river. Airbus building a $600m plant in Mobile will bolster port. • Miami, Florida: 11th busiest US port with 950k TEU p.a. Huge for cruise traffic. Dredging to deepen port to 50 feet. Tunnel being built under Biscayne Bay to connect Port facilities & interstate highways. 15

- 16. Select US Ports likely ready post 2015 •Savannah, Georgia: 3rd busiest US port with 3m TEU per annum. Anticipated ready by 2016. •Jacksonville, Florida. Disney committed to directing all imports through the port •Wilmington, NC •Tampa, Florida: Largest fertilizer export port globally •New Orleans, Louisiana: Important port for bulks transited down via the Mississippi river 16

- 17. Implication for US Railways • US intermodal system (rail, truck, waterways) needs to remain competitive & accommodate extra cargo; this is spurring investment. For example: • Florida East Coast Railway: Investing in on-dock rail facility at Port Miami to be ready 2014. Allow double stack containers directly to Jacksonville in under 9 hours • CSX: National Gateway Project to create more efficient double-stack route between mid Atlantic Ports & Mid west. • Expanded on-dock rail facility at Savannah • New near dock, inter-modal facility near Port of Baltimore • Connectivity with Ports good, expanding inland capacity to handle extra cargo • Norfolk Southern: Heartland Corridor Project enable Double Stack Freight by increasing clearances through 30 channels between Virginia Ports & Mid West; taken 250 miles of route between Hampton Roads, Virginia to Chicago 17

- 18. 18 Norfolk Southern: Investing in Crescent Corridor to connect Louisiana & New Jersey. Will move containers more efficiently from the Gulf to major distribution & population centers

- 19. 19 Major US Railway Freight Lines

- 20. Implications for US Waterways & Grain exports • Lower Mississippi Ports like New Orleans & Mobile significant for export of dry bulks like grains, ores, coal brought down by the river. 40m tons of grains brought each year from Midwest for export via Mississippi • 25% of all traffic going through Panama Canal from Atlantic to Pacific is Grains. 30% is petroleum products & chemicals. Huge scope to increase with expansion • Shale Gas revolution to combine with PC expansion to increase LNG export potential. Recent announcement of LNG terminal in Texas • Post Expansion, in terms of Bulk Vessels Post Panamax & Capesize carriers will be able to transit, increasing the tonnage that can be transported on any one ship from current limit of 80,000 to 200,000 tons. • More efficient Cape Class ships could reduce cost of exporting grain to North East Asia from the US Gulf ports by a significant $0.35 per bushel 20

- 21. 21 Inland Waterways connecting US Heartland to the Coast

- 22. 22 Composition of tonnage transported on the Mississippi River to Gulf

- 23. Implication for US Supply Chains • Retailers & manufacturers will remake supply chains to benefit from reduced cost & higher reliability of transit to East Coast Gulf ports near major population centers • Investment in Distribution Centers and Manufacturing plants near growing South East & Gulf transit hubs happening and will increase, for example: • Ashley Furniture seeing export opportunities from Mid-Atlantic & frustrated by rail freight delays at Chicago built 3.3m manufacturing & warehouse facility in North Carolina. • Airbus building plant in Mobile, Alabama & Boeing in Charleston, SC • Industrial REIT firms such as Prologis & Eastgroup are investing in industrial and distribution assets near East Coast & Gulf ports to benefit from increased demand • Next slide shows clustering of Distribution Centers around Savannah, Georgia 23

- 24. 24

- 25. Implications for South East US & Charlotte • Boon for South East & Gulf regional economies & cities. • Port cities such as Charleston, Savannah, Norfolk, to benefit. Port traffic will be further helped by new manufacturing facilities such as Airbus (Mobile), Boeing (Charleston) • Aside from the ports cities, Charlotte, North Carolina to benefit as regional economic hub and major freight, transport distribution center between the coastal ports of the Gulf / Mid Atlantic & population centers of East Coast & Mid West. • Charlotte is connected to Charleston, Savannah, & Wilmington by Norfolk Southern Railway & freight line capacity is being expanded on these routes. • Heavy Investment underway in Charlotte: New Intermodal Center at Charlotte- Douglas Airport will connect to ‘Crescent Corridor’ Rail Freight services allowing 250,000 container throughput capacity per annum 25

- 26. Investment Implications • Significant boon for railways, truck companies active in South East & Gulf region. • Logistics firms to benefit as more complex freight patterns and options increases their customers’ desire to have 3rd parties handle complicated logistics • Increase demand for Manufacturing Bases, Distribution Centers, Warehousing Facilities to benefit value of industrial assets, land and industrial REITs active in the Gulf, Mid-Atlantic regions. • Strengthens trends of SIGNIFICANT FLOW of labor and capital into the South East US … • Residential Real Estate in cities that are impacted will benefit • Suppliers of port and rail infrastructure & equipment to benefit • Shippers who can reallocate ships to new routes will benefit • Agrarian plays & exporters in US to benefit • Bulk, container & freight markets will be severely disrupted resulting in huge winners and losers. • STRENGTHENS EVEN FURTHER CONVICTION THAT GENESIS IS PURCHASING RESIDENTIAL ASSETS IN THE RIGHT REGION OF THE US AT THE RIGHT TIME 26

- 28. 28 END