Russian Call Girls In Gurgaon ❤️8448577510 ⊹Best Escorts Service In 24/7 Delh...

The Lithuanian Economy - No 4, June 30, 2011

1. The Lithuanian Economy

Monthly newsletter from Swedbank’s Economic Research Department

by Nerijus Mačiulis No. 04 • 2011 06 30

Investments drive growth, external imbalances are slightly wider

In the first quarter of 2011, the biggest contribution to GDP growth came from

investments, followed by continued restocking and recovering domestic demand.

The rapid growth is partially explained by a very low base – in the first quarter of

last year, the index of gross fixed capital formation dipped to its lowest level in the

last decade. As the population dwindles, the high potential GDP growth can be

sustained by investments and increasing productivity.

Both private and public sectors increased investments in fixed tangible assets,

which in the first quarter of 2011 grew by 44% over the same period a year ago. As

we forecast in our economic outlook, the private sector significantly increased its

investments, especially in equipment, machinery, and transport vehicles. This trend

is likely to continue this year and the next.

Rising imports of investment goods and recovering domestic consumption will have

a negative impact on the foreign trade balance. As there is already a hint of new

imbalances, long-term growth should rely more on investments and exports, rather

than consumption.

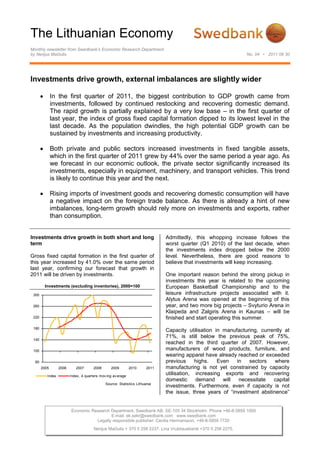

Investments drive growth in both short and long Admittedly, this whopping increase follows the

term worst quarter (Q1 2010) of the last decade, when

the investments index dropped below the 2000

Gross fixed capital formation in the first quarter of level. Nevertheless, there are good reasons to

this year increased by 41.0% over the same period believe that investments will keep increasing.

last year, confirming our forecast that growth in

2011 will be driven by investments. One important reason behind the strong pickup in

investments this year is related to the upcoming

Investments (excluding inventories), 2000=100 European Basketball Championship and to the

300 leisure infrastructure projects associated with it.

Alytus Arena was opened at the beginning of this

260 year, and two more big projects – Svyturio Arena in

Klaipeda and Zalgiris Arena in Kaunas – will be

220 finished and start operating this summer.

180

Capacity utilisation in manufacturing, currently at

71%, is still below the previous peak of 75%,

140

reached in the third quarter of 2007. However,

100 manufacturers of wood products, furniture, and

wearing apparel have already reached or exceeded

60 previous highs. Even in sectors where

2005 2006 2007 2008 2009 2010 2011 manufacturing is not yet constrained by capacity

Index Index, 4 quarters mov ing av erage

utilisation, increasing exports and recovering

domestic demand will necessitate capital

Source: Statistics Lithuania

investments. Furthermore, even if capacity is not

the issue, three years of “investment abstinence”

Economic Research Department. Swedbank AB. SE-105 34 Stockholm. Phone +46-8-5859 1000

E-mail: ek.sekr@swedbank.com www.swedbank.com

Legally responsible publisher: Cecilia Hermansson, +46-8-5859 7720

Nerijus Mačiulis + 370 5 258 2237. Lina Vrubliauskienė +370 5 258 2275.

2. The Lithuanian Economy

Economic Research Department, Swedbank

Nr 04 • 2011 06 30

has rendered some manufacturers technologically Investment in tangible fixed assets, billion LTL

backwards and inefficient. 7 160

6 140

This year, Statistics Lithuania has conducted a

population and housing census that, somewhat 5

120

unexpectedly, reveals that Lithuania has only 3.05 100

4

million inhabitants (preliminary estimate). This is 80

well below the 3.25 million inhabitants at the 3

60

beginning of this year and the 3.5 million that had

2

been estimated at the beginning of the last decade. 40

As the Lithuanian population and its labour force 1 20

dwindles rapidly – due to both emigration and the 0 0

low birth rate – the economy as a whole will have to 2005 2006 2007 2008 2009 2010 2011

rely more on another factor of production – physical Others

1

capital. Acquisition of equipment, machinery , v ehicles

Construction and repairs

Index, y oy (right scale) Source: Statistics Lithuania

Over the past 15 years, average GDP growth in

Lithuania was 4.6%, third highest in EU and only

slightly lower than Estonia’s and Ireland’s 5.0%. But Over the same period, both the private and public

to sustain potential output close to 5%, Lithuania sectors increased their investments significantly.

needs to offset its population and labour force loss. Furthermore, the private sector invested twice as

Gross fixed capital formation averaged 22.5% much as the public sector. Given the lower

during the past 15 years and 27.7% in the 5 years efficiency of public sector investments, less

after EU accession. However, a big part of these crowding out by public sector and a more active

investments were in residential real estate – useful, private sector are positive developments.

but not very productive capital. In the first quarter,

gross fixed capital formation reached 22.3% of In the first quarter, the private sector was the main

GDP, above its 2009 low of 14.3% but still below contributor to the growth of investment in equipment

the post-EU accession average. and machinery – its nominal annual growth

exceeded 58%. Overall, 78% of all investments in

Investments in machinery and equipment are machinery and equipment were made by the

essential private, not the public sector. Growth in construction

and the repair of buildings and civil engineering

In the first quarter of this year, investment in structures were, on the other hand, still dominated

tangible fixed assets increased by 44.0% over the by the public sector.

same period a year ago. The acquisition of

Investment in tangible fixed assets, 1Q 2011, m LTL

equipment, machinery, and transport vehicles grew

even faster – nominal growth (at current prices) Real estate

exceeded 52%. These kinds of investments have Electricity , gas

the biggest impact on productivity and Manuf acturing

competitiveness, and thus are essential for export- Transportation and storage

driven growth. Public administration

Wholesale and retail trade

Water supply

Inf ormation and communication

Health and social work

Construction

Prof essional, scientif ic

Agriculture, f orestry

Other

0 100 200 300 400

Source: Statistics Lithuania

1

You can read more about Lithuania’s productivity in

our recent analysis: Due to the aforementioned reasons, the real estate

http://www.swedbank.lt/lt/previews/get/2417/130674583 sector invested the most (LTL 392 million) in the

9_Swedbank_Analysis_LT_Productivity_May2011.pdf first quarter, followed closely by electricity and gas,

manufacturing, and transportation and storage. The

2 (4)

3. The Lithuanian Economy

Economic Research Department, Swedbank

Nr 04 • 2011 06 30

latter sector benefitted from rapidly increasing Imports, billion LTL

exports and imports, as well as by the growing 8

trade between Western Europe and CIS countries.

7

In the first quarter, manufacturers invested LTL 272 6

million, 59.5% more than in the same period last 5

year, but still 62.3% less than in 2008. Among the

biggest investors were producers of food, wood, 4

and metals. As mentioned above, manufacturers 3

are not yet constrained by production capacities;

2

however, this is bound to change in the near future.

1

Growing imports will cause external imbalances 0

2007 2008 2009 2010 2011

Capital goods Intermediate goods

The rapid growth of exports of goods and services, Consumption goods Others

which began at the start of last year, continued in Source: Statistics Lithuania

the first months of 2011. Annual growth peaked in

January, at 54.2%. Since then, it has decelerated a Capital goods make up 11%, consumption goods

bit (mainly due to the much higher comparative 21%, and intermediate goods 64% of total imports.

base), and in April exports were 22.3% higher than This import structure has changed noticeably since

a year ago. 2007, when imports of intermediate goods

Growth of exports and imports of goods and services (at

constituted 54% and capital goods 18% of total

current prices), yoy % imports. Recovering investment in fixed tangible

assets will continue to boost imports of capital

60%

goods, as most of the needed machinery,

equipment, and transport vehicles are not produced

40%

in Lithuania.

20%

The increasing import share of intermediate goods

relates to the rapid growth in manufacturing, where

0%

these intermediate goods are processed and

exported or consumed locally.

-20%

Current account and foreign trade balance, % of GDP

-40%

15%

-60% 10%

2007 2008 2009 2010 2011

5%

Exports Imports

Source: Bank of Lithuania

0%

-5% -1.1% -1.5% -2.3%

Although domestic demand was relatively weak,

imports were increasing at a pace similar to exports’ -10%

– in January, it was 56.7% and in April 23.6% -15%

higher than a year ago. Exports have already

-20%

exceeded pre-crisis records, and imports are rapidly -18.4%

approaching those levels. -25%

2006 2007 2008 2009 2010 2011

Current account balance, % of GDP

Goods and serv ices balance, % of GDP

Source: Bank of Lithuania

Although household consumption increased by

5.5% in the first quarter of this year, it still lags

behind exports. In May, retail trade continued its

strong growth, increasing by 23.8% over the same

period last year. Retail trade except transport

3 (4)

4. The Lithuanian Economy

Economic Research Department, Swedbank

Nr 04 • 2011 06 30

vehicles also continued growing; in May, it was The trade deficit is nowhere near the record of –

6.5% higher than a year ago. 18.4% reached in the first quarter of 2008, but it has

worsened noticeably compared with the

The rising household consumption will inevitably corresponding quarters of 2009 and 2010. As

lead to higher imports of consumption goods, household disposable income will grow, the gap will

especially as consumers will be buying more non- widen further. A call of warning is still premature,

necessities (household appliances, information and but, as recent history shows, the trade deficit is one

communication equipment, etc). This, in turn, will of the best indicators of bubbles and imbalances

further widen the trade deficit. and should be watched closely.

Nerijus Mačiulis

Swedbank

Economic Research Department Swedbank’s monthly newsletter The Lithuanian Economy is published as a service to our

SE-105 34 Stockholm customers. We believe that we have used reliable sources and methods in the preparation

Phone +46-8-5859 1028 of the analyses reported in this publication. However, we cannot guarantee the accuracy or

ek.sekr@swedbank.com completeness of the report and cannot be held responsible for any error or omission in the

www.swedbank.com underlying material or its use. Readers are encouraged to base any (investment) decisions

on other material as well. Neither Swedbank nor its employees may be held responsible for

Legally responsible publisher

losses or damages, direct or indirect, owing to any errors or omissions in Swedbank’s

Cecilia Hermansson, +46-8-5859 7720.

monthly newsletter The Lithuanian Economy.

Nerijus Mačiulis, +370 5 2582237.

Lina Vrubliauskienė, +370 5 268 4275.

4 (4)