Contenu connexe

Similaire à JLL Pittsburgh Office Insight & Statistics - Q2 2020 (20)

Plus de Tobiah Bilski (13)

JLL Pittsburgh Office Insight & Statistics - Q2 2020

- 1. © 2020 Jones Lang LaSalle IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

Q2 2020

Pittsburgh

Office Insight

Across the country, available sublease space is increasing. COVID-19 and the

move towards working remote has had a profound impact on the U.S. office

market. In Pittsburgh, the impact is noticeable, but not as severe. Less than

1.0 percent of the office inventory was made available through subleases in

the second quarter.

Although leasing activity declined in April and May, June showed a return

towards normal levels. As construction restrictions were lifted, several

speculative office projects in Pittsburgh resumed. The Vision on Fifteenth and

Liberty East both began site preparation, while Walnut Capital began

demolition of the existing buildings on the Innovation District site in Oakland.

Outlook

Absorption for the second quarter was negative by more than 500,000 square

feet due to several large blocks of sublease space becoming available, as well

as leasing activity taking a pause. But as construction picks back up and the

region moves towards the next normal, leasing activity is expected to

rebound.

Local investors are still bullish on the Pittsburgh market as Burns and Scalo,

LG Realty, and Walnut Capital continue development on the three largest

speculative office projects in the region. Demand is still evident for the new

construction projects as tenants emphasize a need for higher levels of safety

due to COVID-19. Touchless technologies and upgraded mechanicals are top-

of-mind, and landlords are adjusting accordingly. As the summer continues,

re-entry strategies will be implemented and the economy will regain some

footing. While this year may lag previous years due to uncontrollable

variables, Pittsburgh’s foundation remains strong and a recovery is not far

away.

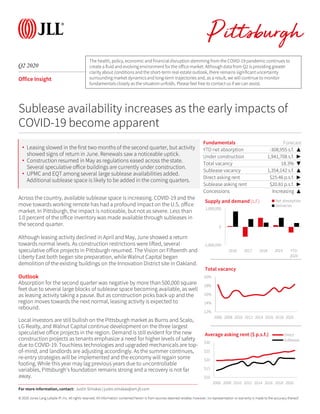

Fundamentals Forecast

YTD net absorption -308,955 s.f. ▲

Under construction 1,941,708 s.f. ▶

Total vacancy 18.3% ▼

Sublease vacancy 1,354,142 s.f. ▲

Direct asking rent $25.46 p.s.f. ▶

Sublease asking rent $20.81 p.s.f. ▶

Concessions Increasing ▲

-1,000,000

0

1,000,000

2016 2017 2018 2019 YTD

2020

Supply and demand (s.f.) Net absorption

Deliveries

Sublease availability increases as the early impacts of

COVID-19 become apparent

12%

14%

16%

18%

20%

2006 2008 2010 2012 2014 2016 2018 2020

Total vacancy

For more information, contact: Justin Simakas | justin.simakas@am.jll.com

• Leasing slowed in the first two months of the second quarter, but activity

showed signs of return in June. Renewals saw a noticeable uptick.

• Construction resumed in May as regulations eased across the state.

Several speculative office buildings are currently under construction.

• UPMC and EQT among several large sublease availabilities added.

Additional sublease space is likely to be added in the coming quarters.

$10

$15

$20

$25

$30

2006 2008 2010 2012 2014 2016 2018 2020

Average asking rent ($ p.s.f.) Direct

Sublease

The health, policy, economic and financialdisruption stemming from the COVID-19 pandemic continues to

create a fluid and evolving environment for the office market. Although data from Q2 is providing greater

clarity about conditions and the short-term real estate outlook, there remains significant uncertainty

surrounding market dynamics and long-term trajectories and, as a result, we will continue to monitor

fundamentalsclosely as the situation unfolds. Please feel free to contact us if we can assist.

- 2. © 2020 Jones Lang LaSalle IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

Class

Inventory

(s.f.)

Total net

absorption

(s.f.)

YTD total net

absorption

(s.f.)

YTD total net

absorption (%

of stock)

Direct

vacancy (%)

Total

vacancy (%)

Average

direct asking

rent ($ p.s.f.)

YTD

Completions

(s.f.)

Under

Development

(s.f.)

Northern I-79 / Cranberry Totals 4,376,907 5,577 106,081 2.4% 15.0% 21.0% $25.75 0 0

East Totals 3,053,814 -56,532 -35,774 -1.2% 26.1% 26.4% $20.13 0 0

North Totals 3,751,808 -71,273 -109,279 -2.9% 12.9% 13.5% $19.33 0 0

South Totals 2,311,420 -41,091 -14,121 -0.6% 14.1% 14.2% $20.15 0 140,000

Southpointe Totals 2,972,107 -8,184 -11,978 -0.4% 16.7% 19.5% $21.57 0 40,000

West Totals 7,229,171 -131,194 -73,032 -1.0% 17.4% 20.9% $22.00 0 220,000

Suburban Totals 23,695,227 -302,697 -138,103 -0.6% 17.0% 19.7% $21.67 0 400,000

CBD Totals 18,969,985 -244,900 -273,241 -1.4% 16.1% 18.3% $27.87 0 0

Fringe Totals 8,715,084 -32,640 106,542 1.2% 14.9% 18.4% $29.01 214,671 648,737

Oakland / East End Totals 2,334,209 -9,059 -4,153 -0.2% 4.4% 4.4% $35.72 0 892,971

Urban Totals 30,019,278 -286,599 -170,852 -0.6% 14.9% 17.3% $28.54 214,671 1,541,708

Pittsburgh Totals 53,714,505 -589,296 -308,955 -0.6% 15.8% 18.3% $25.46 214,671 1,941,708

Northern I-79 / Cranberry A 3,691,749 -10,935 93,582 2.5% 14.0% 21.2% $26.46 0 0

East A 1,580,784 -52,639 -32,220 -2.0% 31.1% 31.5% $21.46 0 0

North A 809,347 -15,618 -4,321 -0.5% 11.1% 11.3% $23.84 0 0

South A 0 0 0 0.0% 0.0% 0.0% $0.00 0 140,000

Southpointe A 1,909,754 -61,505 -57,893 -3.0% 10.1% 13.9% $22.97 0 40,000

West A 3,943,914 -88,831 -67,566 -1.7% 13.7% 18.6% $24.24 0 220,000

Suburban A 11,935,548 -229,528 -68,418 -0.6% 15.3% 19.9% $23.93 0 400,000

CBD A 13,498,998 -253,980 -315,733 -2.3% 15.4% 18.3% $30.42 0 0

Fringe A 2,880,141 -872 103,394 3.6% 8.0% 12.0% $36.96 214,671 648,737

Oakland / East End A 1,149,696 4,133 6,272 0.5% 6.4% 6.4% $38.35 0 892,971

Urban A 17,528,835 -250,719 -206,067 -1.2% 13.6% 16.5% $32.27 214,671 1,541,708

Pittsburgh A 29,464,383 -480,247 -274,485 -0.9% 14.3% 17.8% $28.97 214,671 1,941,708

Northern I-79 / Cranberry B 685,158 16,512 12,499 1.8% 20.4% 20.4% $22.38 0 0

East B 1,473,030 -3,893 -3,554 -0.2% 20.7% 21.1% $17.84 0 0

North B 2,942,461 -55,655 -104,958 -3.6% 13.4% 14.0% $17.92 0 0

South B 2,311,420 -41,091 -14,121 -0.6% 14.1% 14.2% $20.15 0 0

Southpointe B 1,062,353 53,321 45,915 4.3% 28.7% 29.7% $20.71 0 0

West B 3,285,257 -42,363 -5,466 -0.2% 21.9% 23.7% $20.47 0 0

Suburban B 11,759,679 -73,169 -69,685 -0.6% 18.6% 19.4% $19.75 0 0

CBD B 5,470,987 9,080 42,492 0.8% 18.0% 18.4% $22.85 0 0

Fringe B 5,834,943 -31,768 3,148 0.1% 18.3% 21.6% $24.47 0 0

Oakland / East End B 1,184,513 -13,192 -10,425 -0.9% 2.5% 2.5% $22.71 0 0

Urban B 12,490,443 -35,880 35,215 0.3% 16.7% 18.4% $23.66 0 0

Pittsburgh B 24,250,122 -109,049 -34,470 -0.1% 17.6% 18.9% $21.69 0 0

Q2 2020

Office Statistics

Pittsburgh

For more information, contact: Justin Simakas | justin.simakas@am.jll.com