RES auctions and CfDs in Germany

•

1 j'aime•318 vues

downloaded from the Energy Community website

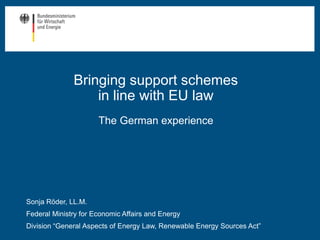

![Continuously developed policies have fostered

the deployment of renewables

3/9/2018 | 2

Source:Ecofys2016basedonAGEEStat2016

0

10

20

30

40

0

50

100

150

200

250

1990

1991

1995

2000

2005

2010

2014

2015

2017

2020

hydro

biomass

wind onshore

solar PV

wind offshore

2020 target

[right axis]

ShareofRESingrosselectricity

consumption

Grosselectricitygenerationfrom

renewablesinTWh

PV programme

“1.000 Roofs”

EEG EEG

Amendment

Electricity Feed-In Law Energy

Concept

EEG

Amendment

Share of RES

[right axis]](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

Similaire à RES auctions and CfDs in Germany

Similaire à RES auctions and CfDs in Germany (20)

Dernier

Dernier (20)

RES auctions and CfDs in Germany

- 1. Bringing support schemes in line with EU law The German experience 18-03-09 Referent 1 Sonja Röder, LL.M. Federal Ministry for Economic Affairs and Energy Division “General Aspects of Energy Law, Renewable Energy Sources Act”

- 2. Continuously developed policies have fostered the deployment of renewables 3/9/2018 | 2 Source:Ecofys2016basedonAGEEStat2016 0 10 20 30 40 0 50 100 150 200 250 1990 1991 1995 2000 2005 2010 2014 2015 2017 2020 hydro biomass wind onshore solar PV wind offshore 2020 target [right axis] ShareofRESingrosselectricity consumption Grosselectricitygenerationfrom renewablesinTWh PV programme “1.000 Roofs” EEG EEG Amendment Electricity Feed-In Law Energy Concept EEG Amendment Share of RES [right axis]

- 3. Cornerstones of the Renewable Energy Sources Act (EEG) 3/9/2018 | 3 • Guaranteed grid access; priority transmission and distribution • Fixed price (tariff or premium) for every kWh produced, granted for 20 years • Price is set for each type of technology and with regard to further provisions (e.g. site and size) • Additional costs for renewable energy production are offset through the EEG surcharge (2016: ~ 6,35 ct/kWh; 2017: ~ 6,88 ct/kWh; 2018: ~ 6,79 ct/kWh), paid by suppliers • Additional costs are offset via grid operators and independent of the public budget, as they are funded by all electricity consumers, with reductions for energy-intensive industries • Regular monitoring and evaluation; accompanying research

- 4. Legal certainty: Bringing the EEG in line with EU law 3/9/2018 | 4 GER notified non-aid measure for legal certainty EU COM considers state aid and assessed on the basis of EEAG Approval regarding the compliance of the EEG 2014 and 2017 with state aid provisions Exemptions for energy intensive industries From FiT to FiP Auctions Legal framework for RES support is set for the next years

- 5. Special Equalization Scheme ensures competitiveness of energy intensive industries 3/9/2018 | 5 • Electricity intensity: Companies that work in electricity-intensive sectors • International trade: additional sectors prone to international competition Eligibility criteria Contribution • Minimum contribution: full EEG surcharge for the first GWh • Additional contribution: 15% of the EEG surcharge for every kWh beyond, cap at 0,5 % / 4% of gross value added Source:

- 6. EEG 2014: FiP becomes the rule Speaker 18-03-09 6 • All electricity from RES installed after August 2014 has to be traded (FiP) • Small operators can still use FiT

- 7. FixedFeed-in-Tariff Market premium Premium system increases market integration of renewables Profit Risk € 3/9/2018 | 7 RemunerationunderEEG2017 Feed-in Tariff Feed-in Premium Participants bid on the reference value Auctions Reference value is defined administratively Support payments Market revenues Monthly average market revenues Market premium Low market price Market premium High market price Monthly average market revenues Market premium Source:Ecofys2017

- 8. EEG 2017: introducing auctions Switching the RES support scheme from administratively determined prices to prices set by competitive auctions

- 9. EEG 2017: introducing auctions 3/9/2018 | 9 Source:Ecofys2016basedonEEG2017 Cost efficiency Stakeholder Diversity Quantity control Guiding principles Auctions for all major renewable technologies

- 10. Deployment corridor EEG 2014 / EEG 2017 Overall target corridor: RES share in gross electricity consumption • In 2025: between 40% and 45% • In 2035: between 55% and 60% Capacity additions • PV 2.5 GW per year (600 MW in auctions), • Wind onshore 2,8 GW (2,9 GW from 2020) • Offshore wind 15 GW by 2030 • Bioenergy 150 MW (later 200 MW) per year

- 11. Specific capacity addition targets make deployment of renewables more plannable 3/9/2018 | 11 Source:EcofysbasedonBMWi2016andEEG2017 0 2000 4000 6000 2026-2030 2023-2025 2020-2022 2017-2019 onshore wind (auction) offshore wind* (auction) solar PV (auction) solar PV (other**) biomass (auction) **EEG 2017 defines 2500 MW of yearly brutto capacity additions. 600 MW are allocated via auctions, 1900 MW via administrative FIT/FIP *500 MW to be added annually in 2021 and 2022 (not in 2020) Annual capacity addition targets per technology in MW

- 12. Auctions: eligible technologies Auctions started in 2017 for Wind onshore Wind offshore Photovoltaic (pilot auctions for ground mounted PV installations were already conducted before 2017) Biomass Installations < 750 kW (biomass: < 150 kW ) are exempted. Thereby, 80% of new RES deployment are covered.

- 13. Tendering scheme in general Technology specific, but common features: • Tendering of total amount of installed capacity (MW); 1-4 auction rounds per year conducted by Federal Network Agency • Only price is decisive for awarding support • Bids will be accepted, starting with the lowest until the amount of capacity that is being auctioned is reached. In principle, the amount of funding corresponds to the individual bid (pay as bid)

- 14. PV: Significant reduction in support costs since the introduction of auctions in 2015 3/9/2018 | 14 Source:BMWi2017basedonBNetzA Values correspond to the average award values

- 15. Onshore wind: The first auctions have shown declining average reward values 3/9/2018 | 15 • Auctioned volumes were clearly exceeded • Round 1: 2.137 MW offered v. 800 MW auctioned • Round 2: 2.927 MW offered v. 1000 MW auctioned • At least 90% of awarded bids came from citizens’ energy cooperatives Source:BMWi2017basedonBNetzA

- 16. Thank you for your attention! 18-03-09 Referent 16 Sonja Röder, LL.M. Federal Ministry for Economic Affairs and Energy Division “General Aspects of Energy Law, Renewable Energy Sources Act”

- 17. Tendering scheme for onshore wind • In 2017, 2018 and 2019, 2,800 MW and from 2020, 2,900 MW (gross) will be auctioned each year, in 3 rounds (1st of May, 1st of August, 1st of November) • Prequalification: Approval pursuant to Federal Immission Control Act (final administrative decision) • Bid bond: 30 €/kW or bank guarantee to discourage non- realisation • Realisation period: 30 months

- 18. Tendering scheme for photovoltaics PV installations > 750 kW; eligible are: Ground-mounted installations Installations on buildings and on other constructial facilities (e.g. waste disposal sites) 600 MW will be auctioned each year, in 3 rounds (1st of February, 1st of June, 1st of October) Prequalification: admission by local authorities and/or area development plan (early planning stage) Bid bond: 50 €/kW to discourage non-realisation Realisation period: 24 months

- 19. Tendering scheme for biomass Existing installations (including those < 150 kW) can take part in the auctions in order to receive 10-year follow-up funding, provided that they generate electricity in a flexible and demand-based manner. New installations < 150 kW receive statutory feed-in tariff Bid bond: 60 €/kW; Realisation period: 24 months Maximum price for new installations: 14,88 ct/kWh; Maximum price for existing installations: 16,9 ct/kWh Prequalification: Approval Flexibility Obligation: Biogas plants will only be granted funding for half of the hours of a year. This is to encourage these plants to generate electricity at times when the wholesale price is high as little wind and sun is available and demand is high. 19

- 20. Tendering scheme for offshore wind The central ‘Danish’ target model will be introduced for offshore wind as of 2026: o Area Development Plan 2019 is the focal planning instrument and will replace Offshore Grid Development Plan and Spatial Offshore Grid Plan as of 2026 o Government examines in advance the sites to be auctioned for wind farms. This ensures optimal dovetailing with the grid connections. o In every other model, a stock of grid connections would have to be built. Otherwise there would be no competition. This would entail massive extra costs. o First auction according to the central model: 1. Sept. 2021; bid bond: 200 €/kW Transition phase 2021 to 2025; Deadlines April 2018/2019; 3.100 MW in total for advanced projects o Synchronisation with grid expansion: 500 MW in the Baltic Sea by 2021, 500 MW Baltic Sea/North Sea by 2022, 2023-2025: 700 MW per year; Start with market premium (Federal Network Agency) o Maximum price: 10 ct/kWh; Bid bond: 100 €/kW; Bids on „minimum volume“ and „underpinning bids“ are possible o Not awarded bidders have the “right for admittance” to the central model from 2026 in case of surrender of data 20

- 21. 21 The EEG 2014 offshore aims are still valid: until 2030, an offshore capacity of 15.000 MW shall be installed Transition period (2021 – 2015): In 2021 and 2022, additional capacity of 500 MW per year and in 2023 – 2025 of 700 MW per year is planned Offshore wind farms that are already planned may take part in the auctions In 2021, only wind farms in the Baltic Sea are eligible for the auction Central model (from 2016 onwards): From 2026 onwards the deployment increases to 840 MW per year. They will be auctioned in the so-called „Danish model“: The state investigates possible sites before the auction and ensures an optimal linkage to grid connection. Auctions for wind offshore

- 22. 22 Until sufficient transmission system capacities are available, we take three measures to reduce redispatch costs: 1. To reduce curtailments an instrument for power-to-heat is introduced as „optional load“ 2. Limitation of deployment for wind onshore in areas with grid bottlenecks A so-called „grid expansion area“ is determined since 1st March 2017 In this area deployment for wind onshore is limited to 58 per cent of the average deployment in the years 2013 – 2015 3. Steering offshore deployment 2021: 500 MW in the Baltic Sea; 2022: 500 MW in North and Baltic Sea 2023 – 2025: 700 MW per year and from 2026 onwards 840 MW per year in North and Baltic Sea Linkage to grid expansion

- 23. 23 Aim: To maintain a high degree of stakeholder diversity. This aim is reached by e.g.: The de minimis threshold of 750 kW – thereby inter alia small and middle-sized PV installations are exempted from the auction scheme. The simple and transparent design of the auction scheme. The Federal Government will also initiate special consultancy and support offers for small stakeholders. Furthermore, auction requirements for wind onshore are lowered for local so-called „citizens‘ energy communities “. Stakeholder diversity

- 24. 24 Definition of a citizens‘ energy projects: Companies, which consist of at least 10 private persons and where these private persons (located on site) have the majority of voting rights. No shareholder has more than 10 per cent of the voting rights. Maximum project size of 6 installations with an electrical capacity of no more than 18 MW. Municipalities have the chance to invest up to 10 per cent in the project. Stakeholder diversity (2/3)

- 25. 25 Easier conditions of participation, so that these projects do not have to pre-finance high costs: No permit according to the Federal Immission Control Act (BImSchG) is required, when a bid is submitted. It is sufficient to document that the site is reserved and to present a certified wind report. Half of the usual security deposit needs to be paid only after the BImSchG permit Extension of the realisation dead line to max. two years. Furthermore, the support rate for citizens‘ energy projects is not determined by the value of its bid, but by the value of the highest bid that was accepted. Thus, they are privileged financially. Stakeholder diversity (3/3)

- 26. Technology-specific payments reflect the varying cost of different types and sizes of renewables 3/9/2018 | 26 2,95 3,69 5,73 25 3,9 4,42 8,84 0 5 10 15 20 25 30 hydropower landfill, sewage & mine gas biomass geothermal wind offshore wind onshore solar PV Set support levels (based on degression) July 2017 in € cent/kWh 12.6 7.95 19.4 23.26 8.17 12.4 Source:Ecofys2016basedonBNetzA2016 Average award level at the solar PV auction in June 2017 was 5.66 €cent/kWh

- 27. vv Requirements Cooperation agreement Reciprocity Physical import effect • 50 MW of solar projects in Denmark • Projects to be built at 5.38 € cent/kWh Open auction with Denmark Auctions will be open to pan-European competition for 5% of newly installed capacity each year 3/9/2018 | 27 Source:

- 28. Cooperation pilot with Denmark • Cooperation agreement for mutually opened auctions for ground mounted PV installations signed in July 2016 • First cooperation of its kind • German and Danish opened auctions conducted in 4th quarter of 2017 • Volume of German auction: 50 MW, fully opened for installations in Denmark • Volume of Danish auction: 20 MW, of which 2.4 MW were opened for installations in Germany

- 29. Results of the German opened pilot auction with Denmark xyz Bidding deadline 23.11.16 Tendered volume 50 Bids (volume) 297 MW Successful bids (awarded volume) 5 bids with 10 MW each, all successful projects located in Denmark Ø reference value ct/kWh 5,38