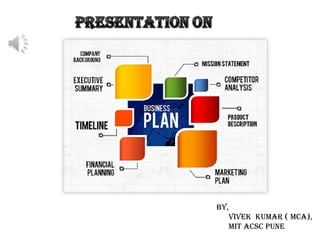

2. Overview

Description of the business

Selecting business location

Identifying the competition

Detailing a marketing strategy

Laying out a financial plan

Describing personnel/management needs

Designing a strategic plan for the present and

future

Business Plan FormulationBusiness Plan Formulation

The Key Elements For SuccessThe Key Elements For Success

3. 1) Description of the Business:

Focus on the business concept and why such a business

opportunity exists as well as the products and services being

offered, the pricing system to be used to meet costs and profits.

Distinguishing your business products/services from others

in the industry (lower prices, faster delivery, longer warranties

etc.) and identifying potential customers and suppliers.

4. 2) Selecting an Appropriate Business Location

Consideration of location choices on the basis of business

customers, accessibility and security and whether the

location is conducive to the business specific industry

needs.

5.

6. Knowledge of who the competition is

with reference to the length of time in

business, reputation, quality of

products and services, customer

service, number of employees, image

and strengths and weaknesses.

3) Identifying the Competition

7. 4) Detailing a Marketing Strategy

Development of marketing/research techniques to help promote

your business market using various advertising tools such as

television, news, trade shows, telemarketing, sales programs,

internet, radio, magazines, direct mail, long-term sponsorships,

public relations (web presence, events, press releases), and other

referral mechanisms (yellow pages).

Use of networking activities such as memberships or leadership

positions and strategic alliances to bolster your business market.

8.

9. Assessment of the financial feasibility

and profitability of a business ,

identification of funds needed and

how the funds will be spent, the

potential sources for funding

(personal resources, banks, venture

capital, angel investors, public agency

loan programs).

Three years profit and loss statements

(projections), three year cash flow

summaries, balance sheets

(assets/liabilities/net worth), and

providing for supporting documents

relevant to the plan (personal financial

history, legal documents, leases, etc.)

5) Laying out a Financial Plan

10. 6) Describing Personnel/Management Needs

Description of the human capital skills and experience needed for a

particular business, pay methods, fringe benefits, payroll taxes and

the use of independent contractors versus employees.

Division of tasks/ reporting hierarchy / final decision makers.

Creation of an advisor group and Board of Directors.

11.

12. 7) Designing a Strategic Plan for the

Present and Future

Establishment of business priorities and goals, including

branding, benchmarking, timetables for action, anticipated

plans to retain and expand current markets and having an

exit strategy.

13. Major components of a business plan

I. Executive Summary

II. Business Profile

III. Market Section

IV. Financial Statements

14. II. Business Profile

One page that states: Legal structure of the business

(e.g., proprietorship, subchapter S, corporation, etc.) as

well as the educational and professional background of

management and principle stake holders. Brief past

company history (if any), or related history of principals.

15. IV. Financial Statements

Start-up costs: licenses, equipment, inventory, remodeling,

deposits, etc.

Show a break-even analysis: how many units must be sold to

cover fixed and variable costs.

Produce pro-forma income statements: anticipated sales,

expenses, and net profit or loss projected over the next three

years.

Pro-forma balance sheets should cover: anticipated assets,

liabilities and net worth of business.

Notes de l'éditeur

List company banker, accountant, legal counsel industry expert and/or government regulations that impact on your operation. Enjoin these professionals in an advisory board that will help you with decisions.

Include an organization chart (on separate page, if necessary).

Refer to the excel templates

Important: If business is seasonal or credit is extended, create a pro-forma cash flow analysis showing business financial trends.

Finally, when going for a business loan, financial statements should be prepared by an independent accountant, collateral offered should be appraised by an independent appraiser, and collateral and any existing receivables should clearly justify the amount and risk of the loan. In other words it should be equal to or greater than the debt. Financial institutions will expect a personal guarantee and/or co-signer.