The Journey of Electronic Tax Compliance

•

1 j'aime•760 vues

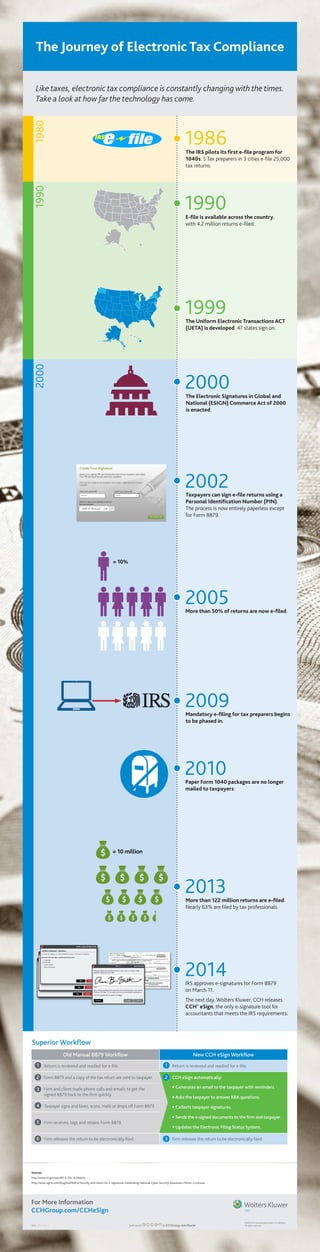

This document traces the history of electronic tax filing in the United States from 1986, when the IRS first piloted an e-filing program for 1040 tax returns, to 2014, when the IRS approved e-signatures for tax forms. Key developments included the launch of nationwide e-filing in 1990, the Uniform Electronic Transactions Act in 1999 recognizing e-signatures, and mandatory e-filing for tax preparers beginning in 2009. By 2013, over 122 million tax returns were e-filed electronically.

Recommandé

Contenu connexe

Similaire à The Journey of Electronic Tax Compliance

Similaire à The Journey of Electronic Tax Compliance (20)

Plus de Wolters Kluwer Tax & Accounting US

Plus de Wolters Kluwer Tax & Accounting US (19)

Dernier

Dernier (20)

The Journey of Electronic Tax Compliance

- 1. 1980 1990 1990 E-file is available across the country, with 4.2 million returns e-filed. 1999 The Uniform Electronic Transactions ACT (UETA) is developed. 47 states sign on. 2014 IRS approves e-signatures for Form 8879 on March 11. The next day, Wolters Kluwer, CCH releases CCH® eSign, the only e-signature tool for accountants that meets the IRS requirements. 2000 1986 The IRS pilots its first e-file program for 1040s. 5 Tax preparers in 3 cities e-file 25,000 tax returns. 2002 Taxpayers can sign e-file returns using a Personal Identification Number (PIN). The process is now entirely paperless except for Form 8879. 2010 Paper Form 1040 packages are no longer mailed to taxpayers. 2000 The Electronic Signatures in Global and National (ESIGN) Commerce Act of 2000 is enacted. 2009 Mandatory e-filing for tax preparers begins to be phased in. Like taxes, electronic tax compliance is constantly changing with the times. Take a look at how far the technology has come. The Journey of Electronic Tax Compliance Old Manual 8879 Workflow New CCH eSign Workflow Return is reviewed and readied for e-file. Return is reviewed and readied for e-file. Form 8879 and a copy of the tax return are sent to taxpayer. CCH eSign automatically: • Generates an email to the taxpayer with reminders. • Asks the taxpayer to answer KBA questions. • Collects taxpayer signatures. • Sends the e-signed documents to the firm and taxpayer. • Updates the Electronic Filing Status System. Firm and client trade phone calls and emails to get the signed 8879 back to the firm quickly. Taxpayer signs and faxes, scans, mails or drops off Form 8879. Firm receives, logs and retains Form 8879. Firm releases the return to be electronically filed. Firm releases the return to be electronically filed. Superior Workflow 1 3 1 2 3 4 5 6 2 Sources http://www.irs.gov/uac/IRS-E-File:-A-History http://www.signix.com/blog/bid/90814/Security-and-Intent-for-E-Signatures-Celebrating-National-Cyber-Security-Awareness-Month-Continues For More Information CCHGroup.com/CCHeSign 9/14 2014-0387-3 ©2014 CCH Incorporated and/or its affiliates. Join us on at CCHGroup.com/Social All rights reserved. 2005 More than 50% of returns are now e-filed. = 10% 2013 More than 122 million returns are e-filed. Nearly 63% are filed by tax professionals. = 10 million