The audit report summarizes the financial activities and internal controls of the Nicholls State University Athletic Department for the year ended June 30, 1996. It reviews revenues and expenditures of the department and the Colonel's Club outside organization. It was found that financial statements accurately represented the department's financial activity and that internal controls were properly designed and implemented.

Ecological Succession. ( ECOSYSTEM, B. Pharmacy, 1st Year, Sem-II, Environmen...

Financial statement laundry shop5

1. DR.DO NA LD J.AYO ,PRESIDENT

N IC HO LLS STA TE U N IV ERSITY

STATE O F LO UISIA NA

A uditReport,June 30,1996

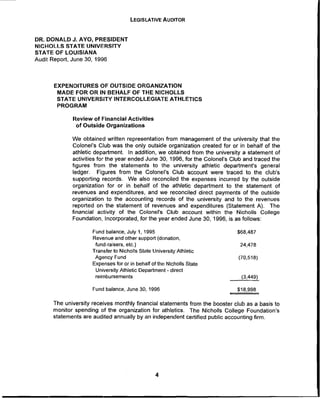

LEGISLATIVEA UDITOR

EXPENDITURES O F O UTSIDE O RGA NIZATIO N

M A DE FO R O R IN BEHA LF O F THE NICHO LLS

STATE!UNIVERSITY INTERCO LLEG IATE ATHLETICS

PRO G RA M

Review ofFinancialA ctivities

ofO utside O rganizations

W e obtained w ritten representation from m anagem entofthe university thatthe

Colonel's Club was the only outside organization created fororin behalfofthe

athletic departm ent. In addition,we obtained from the university a statem entof

activitiesforthe yearended June 30,1996,forthe Colonel's Club and traced the

figures from the statem ents to the university athletic departm ent's general

ledger. Figures from the Colonei's Club account were traced to the club's

supporting records. W e also reconciled the expenses incurred by the outside

organization for or in behalf of the athletic departm ent to the statem ent of

revenues and expenditures,and we reconciled direct paym ents ofthe outside

organization to the accounting records of the university and to the revenues

reported on the statementofrevenues and expenditures (StatementA). The

financial activity of the Colonel's Club account w ithin the Nicholls College

Foundation,Incorporated,forthe yearended June 30,1996,is asfollows:

Fund balance,July 1,1995

Revenueandothersupport(donation,

fund-raisers,etc.)

Transferto Nichorls State UniversityAthletic

Agency Fund

Expensesfororin behalfofthe Nicholls State

UniversityAthletic Departm ent-direct

reim bursem ents

Fund balance.June 30.1996

$68,487

24,478

(70,518)

(3,449)

$18.998

The university receives m onthlyfinancialstatem ents from the boosterclub as a basisto

m onitorspending ofthe organization forathletics. The Nicholls College Foundation's

statem ents are audited annually by an independentcertified public accounting firm .

2. DR.DO NA LD J.AYO ,PRESIDENT

NICHO LLS STATE UNIVERSITY

STATE O F LO UISIANA

A uditReport,June 30,1996

LEGISLATIVEAUDITOR

NTERNA L CO NTRO L PO LICIES A ND

PRO CEDURES RELATING TO

INTERCO LLEG IATE ATHLETICS -

AG REED-UPO N PRO CEDURES

M anagem entofNichofls State University is responsible forestablishing and m aintaining

a system of internalaccounting control. In fulfilling this responsibility,estim ates and

judgments by managementare required to assessthe expected benefits and related

costs ofcontrolprocedures. The objectives ofa system are to provide management

w ith reasonabte,butnotabsotute,assurance thatassets are safeguarded againstloss

from unauthorized use ordisposition and thattransactions are executed in accordance

w ith m anagem ent's authorization and recorded properly to perm it the preparation of

financialstatem ents in accordance with generally accepted accounting principles.

Because of inherent lim itations in any internal control structure, errors and/or

irregularities may,nevertheless,occurand notbe detected. Also,projection ofany

evaluation ofthe system to future periods is subjectto the riskthatprocedures may

becom e inadequate because ofchanges in conditions orthatthe degree ofcom pliance

w ith the procedures m ay deteriorate.

The m inim um agreed-upon procedures, applied to certain aspects of the athletic

departm ent's internalaccounting control,were m ore lim ited than would be necessary to

express an opinion on the system of internalaccounting controltaken as a w hole.

Because our study and evaluation was lim ited to applying m inim um agreed-upon

procedures discussed in the follow ing paragraphs to certain aspects of the internal

accounting control,w e do not express an opinion on w hether the system of internal

accounting controlofthe Nicholls State University Athletic Departm ent,in effectforthe

yearended June 30,1996,taken as a whole,was sufficientto meetthe objectives

stated previously. In connection with our appSed procedures, we noted certain

opportunities for im provem ent in the system of internal accounting control. O ur

m inim um agreed-upon procedures are as follow s:

Testofthe InternalControlEnvironm ent

W e perform ed a prelim inary review of the internalaccounting controlof the

athletic departm ent by reviewing the organizational chart prepared by the

associate athletic director and by perform ing tests on the flow oftransactions

through the accounting system .

3. DR.DO NALD J.AYO ,PRESIDENT

N IC t'IO LLS STATE U N IV ERSITY

STA TE O F LO UISIA NA

AuditReport,June 30,1996

LL:LW M :dl

LEGISLATIVEAUDITOR

BoosterG roup A ctivities

W e reviewed the university's procedures form onitoring boostergroup activities.

The vice presidentforInstitutionalAdvancem ent,who isan ex-officio m em beron

the board ofthe Nicholls College Foundation,Incorporated,and to whom the

athletic director reports,attends board m eetings and receives annualfinancial

statem ents from the foundation. In addition, the associate athletic director

m aintains the financial records of the Colonel's Club account w ithin the

foundation.

./~ ectfullysubmitted;/

DanielG .Kyle,CPA ,CFE

Legislative Auditor

4. DR.DO NA LD 3.AYO ,PRESIDENT

N IC HO LLS STATE U NIV ER SITY

STATE O F LO UISIANA

AuditReport,June 30,1996

LEGISLATIVEA UDITOR

STATEM E'NT O F REVENUES A ND EXPENDITURES

TestofStatem ent

W e obtained from m anagem entthe statem entofrevenues and expenditures for

the yearended June 30,19g6,as shown on Statem entA ,and requested written

representation from m anagem ent as to its fair presentation. In addition,we

verified the m athem aticalaccuracy ofthe am ounts on the statem entand traced

the am ounts on the statem ent to various accounts in the revenue and

expenditure ledgers of the university. W e noted no differences between the

am ounts in the revenue and expenditure ledgers and the am ounts on the

statem ent.

Com parison ofStatem ents

W e com pared the statem ents ofrevenues and expenditures forJune 30,1995,

and June 30, 1996, to determ ine the percentage of increase or decrease

between the tw o years. The university provided satisfactory responses forany

m aterialvariances betw een the tw o years.

Com parison ofBudgetto Actua

Revenues and Expenditures

W e com pared the am ount of budgeted revenues and expenditures to actual

revenues and expenditures forthe yearended June 30,1996,to determ ine if

there were any m aterialbudgetvariances. The university provided satisfactory

responsesforany m aterialvariances between budgeted and actualam ounts.

Contributions Exceeding Ten

PercentofTotalContributions

W e obtained from m anagem ent a list of contributions received by the athletic

departm ent and determ ined that there w as one individual contribution, from

State Farm Insurance Companies totaling $27,660,thatexceeded ten percent

($21,679)ofthetotalcontributions.

5. Nicholls State University is a publicly supported institution ofhighereducation. The university is

a com ponentunitofthe State ofLouisiana w ithin the executive branch ofgovernm ent. The

Nicholls State University Athletic Department, which operates the intercollegiate athletics

program ,is a partofNicholls State University. The accom panying financialstatem entpresents

inform ation only asto the transactions ofthe NichollsState UniversityAthletic Departm ent.

SUM M ARY O F SIG NIFICA NT ACC O UNTING PO LICIES

A . FUND A CCO UNTING

To observe lim itations and restrictions placed on the use of available resources,the

accounts ofNichol/s State University are m aintained in accordance with the principles of

fund accounting. Such principles prescribe the m annerin w hich resources forvarious

purposes are classified,foraccounting and reporting purposes,into funds thatare in

accordance with the activitiesorspecified objectives. Accounts are maintained forthe

transactions ofthe athletic departm entas follows:

CurrentFunds -Unrestricted

Unrestricled current funds include allfunds for operating purposes on w hich

there are no restrictions,exceptthe budgetary controlprovisions included in the

annuallegislative appropriation act,and include the G eneralFund and auxiliary

enterprise funds. The auxiliary enterprise funds include the accounts of the

athletic departm ent.

Agency Funds

This fund group represents funds forw hich the university acts as custodian or

fiscalagenton behalfofothers,such as contributions and interestearnings of

the athletic departm ent.

B. BASIS O F ACCO UNTING

The accounts of the athletic departm ent are m aintained on the accrual basis of

accounting as follows:

6. ST A T E O F L O U ISIA N A

L E G ISL A T IV E A U D IT O R

Athletic Departm ent

Nicholls State U niversity

Sta te ofLouisiana

Thibodaux,Louisiana

April23,1997

Financialand C om pliance A uditD ivision

D anielG .K yl'-~ e,

Ph.D .,C PA ,C FE

Legislative A uditor

7. LEGI.C;LATIVE A UDITOR

ATHLETIC DEPA RTM ENT

NIC HO LLS STATE U NIV ERSITY

STA TE O F LO UISIA NA

NotestotheFinancialStatement(Continued)

Revenues

Substantially allrevenuesare recognized w hen earned

Expenditures

Expenditures are generally recognized underthe accrualbasis of accounting

whenincurred,exceptthat(1)depreciationisnotrecognized;(2)annualandsick

leaveare recognizedwhenpaid;and (3)facultysalariesand related benefitsfor

June are notprorated butare deferred to the succeeding year.

C. EM PLOYEE CO M PENSATED A BSENCES

Em ployees ofthe university working in the athletic departm entearn annualand sick

leave in accordance w ith state law and adm inistrative regulations. Leave benefits are

reflected in the accom panying financialstatem entwhen paid.

D. TO TA L C O LUM N O N STATEM E-NT

The totalcolumn on StatementA iscaptioned Memorandum Only (overview)to indicate

that itis presented only to facilitate financialanalysis. Data in this colum n does not

present results of operations in conform ity with generally accepted accounting

principles. Neitheris such data com parable to a consolidation.

CONTRIBUTIONS (GIFTS-IN-KIN[))

FRO M O UTSIDE O RGA NIZATIO NS

The follow ing is a sum m ary of contributions-in-kind received and reported as revenues and

expenditures on Statem entA :

Revenues

A utom obile dealerships -use ofone courtesy careach

J.G raham Dodge,Inc.

Dantin M otors,Inc.

G reg LeBlanc Nissan

Brow n Ford,Inc.

G eriLeBlanc Pontiac Buick G M C Truck

Howard Johnson -lodging forrecruits on officialvisits

Chiropractic and PhysicalTherapy Clinic,Inc.-

chiropractic and physicaltherapy services

$3,000

3,000

3,000

3,000

3,000

2.500

3.000

8. LEGISLATIVE"-AUDITOR

ATHLETIC DEP A RTM ENT

N IC HO LLS STA TE U N IV ERSITY

STATE O F LO UISIA NA

Notestothe FinancialStatement(Conclucled)

3

Revenues(Cont.)

Kern's Drycieaning,Inc.-laundry services

Bayou Country Club -use ofgolfing facilities

EIlendale Country Club -use ofgolfing facilities

Thibodaux Driving Range -use ofgolfing facilities

E.D.W hite High School-use oftrack

Johnny's M en's Shop -uniform clothing forathleticevents

Piccadilly Cafeteria -postgam e m eals and catering serv ices

BollingerShipyard,Inc.-footballblocking sled

A nlyn System s,Inc.-facsim ile services

Totalrevenues

Expenditures

O perating services

Travel

Supplies

Professionalservices

Equipm ent

Totalexpenditures

O UTSIDE O RG A NIZATIO NS C REATED

FO R O R IN BEHA LF O F THE NICHO LLS

STATE UNIVERSITY INTERCO LI..EG IATE

ATH LETICS PRO G RA M

$1,500

100

200

1,500

500

3,000

3,000

795

250

$31,345

$19,050

2,500

6,000

3,000

795

$31,345

The Colonel's Club is the only outside organization created fororin behalfofthe Nicholls State

University Intercollegiate Athletics Program . "]he accounts forthis club are m aintained as an

athletic agency fund ofNicholls State University and as an accountw ithin the Nicholls College

Foundation, Incorporated, w hich is a separate corporation. The athletic director and the

associate athletic directordeterm ine the am ounts transferred to the University Athletic Agency

Fund forthe Foundation.

10

9. ATHLETIC DEPA RTM ENT

NICHO LLS STATE UNIVERSITY

STATE O F LO UISIA NA

Statem entofRevenues and Expenditures

Forthe YearEnded June 30,1996

REVENUES

Educationandgeneraltransfers

G ate receipts

Guarantees

Commissions

NCAA receipts

In-kindcontributions(note2)

Outsidefunds(note3)

M iscellaneous

Totalrevenues

EXPENDITURES

Personalservicesand related benefits

Travel

O perating service s

Supplies

Professionalaervi(:es

G uarantees

Scholarships

Othercharges

Equ,pment

]otalexpenditures

EXCESS O F REVENUES OVER EXPENDITURES

(PORTION OF)

CURRENT FUNDS -

UNRESTRICTED -

AUXILIARY ATHLETIC

ENTERPRISE AG ENCY

FUND FUND

$1,570,000

89,975

232,000

4,954

298.360

14.824

2,210,113

862,428

211,019

184,363

76,399

164,747

5,750

641,688

2,095

292

2.148.781

$31,345

257.308

288.653

45,309

39,765

39,005

68,818

4.450

30,648

1,049

229.044

$61,332 $59,609

250,784

223,368

145,217

169,197

5,750

641,688

32,743

1.341

2,377,825

$120,941

10. I)ANIEI,O.KYLE,P!I,D.,CPA,CFE

LEGISLATIVE AUDITOR

OFFICE:OF

LEG ISLA TIV F.A U D ITO R

STATE OF LOU ISIAN A

BATON ROUG E,1,OUISIANA 70804-9397

M arch 20.1997

nder)endentA uditor's Reoort

DR.DO NALD J.AYO ,PRESIDENT

NICHO LLS STATE UNIVERSITY

STATE O F LO UISIA NA

Thibodaux.Louisiana

1600NOR'I'|ITIIIRI)S]RI,:I~I

POS3 0|:FICE BOX 94397

TELEPtlONE:(504)339-3800

FACSIMILE: (504)339-3870

W e have audited the generalpurpose financialstatem ents of Nicholls State University, a

com ponentofthe State ofLouisiana reporting entity,as ofJune 39,1996,and forthe years

ended June 30, 1996, and June 30, 1995, and have issued our report thereon dated

Decem ber19,1996. As requested by the university,we have also applied certain m inim um

agreed-upon procedures contained in the National Collegiate Athletic Association Financial

AuditG uidelines to the accounting records and system of internalaccounting controlofthe

Nicholls State University Athletic Departm entand to the related outside organization created for

orin behalfofthe university's Intercollegiate Athletics Program forthe yearended June 30,

1996, solely to assist the university in com plying w ith the National Collegiate Athletic

Association (NCAA) Bylaw 6.2.3.1. It is understood that this report is solely for your

inform ation. How ever,by provisions ofstate law ,this reportis a public docum entand has been

distributed tothe appropriate publicofficials.

Because the follow ing m inim um agreed-upon procedures do notconstitute an auditm ade in

accordance with generally accepted auditing standards,we do notexpress an opinion on any of

the accounts or item s on the accom panying statem entof revenues and expenditures ofthe

athletic departm ent or on the sum m ary of financial inform ation of the related outside

organization included in this report. In connection with the follow ing m inim um agreed-upon

procedures,nothing cam e to ourattention thatcaused us to believe thatthe specified accounts

oritems should be adjusted. Had we performed additionalprocedures orhad we made an

auditofanyfinancialstatem ents ofthe Intercollegiate Athletics Program and the related outside

organization of the Nicholls State University, in accordance w ith generally accepted

governm entalauditing standards, m atters m ight have com e to our attention that w ould be

reported to you. This report relates only to the accounts and item s discussed on the follow ing

page,,; and does not extend to the financial statem ents of Nicholls State University, its

Intercollegiate Athletics Program ,orthe related outside organization taken as a whole. Our

m inim um agreed-upon proceduresfollow :

11. A THLETIC DEPA RTM ENT

NIC HO LLS STAT["UNIVERSITY

STATE O F LO UISIA NA

FinancialStatem entand

IndependentAuditor's Report

Forthe YearEnded June 30.1996

ndependentAuditor'sReport (including

sectiononinternalcontrol)

FinancialStatem ent-Statem entof

Revenues and F_xpenditures

Notes to the FinancialStatem ent

CO NTENTS

Statem ent Page No

A

2

7

8

12. LI'G ISLATIVE A U DIT A DVISO RY CO UNC IL

M EM BERS

Representative Francis C .Thom pson,C hairm an

SenatorRonald C .Bean,V ice C hairm an

SenatorRobertJ.Barham

SenatorW ilson E.Fields

SenatorThom as A .G reene

SenatorCraig I-'.Rom ero

Representative F.C harles M cM ains,Jr

Representative Edw in R.M urray

Representative W arren J.Triche,Jr.

Representative David Vitter

DanielG .Kyle,Ph.D.,CPA ,CFE

A lbertJ.Fi:obinson,Jr.,C PA

13. ATHLETIC DEPA RTM ENT

NIC HO LLS STATE U NIVERSITY

STATE O F:LO UISIA NA

Thibodaux,[.ouisiana

FinancialStatem entand

IndependentAuditor's Reports

Forthe YearEnded June 30,1996

April23,1997