Contenu connexe Similaire à Uae Oil & Gas Report Similaire à Uae Oil & Gas Report (20) 1. Published quarterly by BUSINESS MONITOR INTERNATIONAL LTD

BUSINESS INTERNATIONAL LTD

UAE

BUSINESS Oil & Gas

MONITOR Report Q1 2006

international

Including 4-year industry forecasts

Business Monitor International 2006 Business Monitor International. All rights reserved.

Mermaid House, 2 Puddle Dock All information contained in this publication is copyrighted in the name of

London EC4V 3DS UK Business Monitor International, and as such no part of this publication may

Tel: +44 (0)20 7248 0468 be reproduced, repackaged, redistributed, resold in whole or in any part, or

Fax: +44 (0)20 7248 0467 used in any form or by any means graphic, electronic or mechanical,

including photocopying, recording, taping, or by information storage or

email: subs@businessmonitor.com

retrieval, or by any other means, without the express written consent of the

web: http://www.businessmonitor.com publisher.

2. UAE Oil & Gas

Report Q1 2006

Including 5-year industry forecasts by BMI

Part of BMI's Industry Survey & Forecasts Series

Published by: Business Monitor International

Publication Date: March 2006

Business Monitor International © 2006 Business Monitor International.

Mermaid House, All rights reserved.

2 Puddle Dock,

London, EC4V 3DS, All information contained in this publication is

UK copyrighted in the name of Business Monitor

Tel: +44 (0) 20 7248 0468 International, and as such no part of this publication

Fax: +44 (0) 20 7248 0467 may be reproduced, repackaged, redistributed, resold in

email: subs@businessmonitor.com whole or in any part, or used in any form or by any

web: http://www.businessmonitor.com means graphic, electronic or mechanical, including

photocopying, recording, taping, or by information

storage or retrieval, or by any other means, without the

express written consent of the publisher.

DISCLAIMER

All information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time of

publishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business Monitor

International accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of the

publication. All information is provided without warranty, and Business Monitor International makes no representation of warranty of any kind as

to the accuracy or completeness of any information hereto contained.

3. UAE Oil & Gas Report Q1 2006

© Business Monitor International Ltd Page 2

4. UAE Oil & Gas Report Q1 2006

CONTENTS

New This Quarter…. .........................................................................................................................................5

SWOT Analysis.................................................................................................................................................7

United Arab Emirates Political SWOT .................................................................................................................................................................. 7

United Arab Emirates Economic SWOT ................................................................................................................................................................ 8

United Arab Emirates Business Environment SWOT............................................................................................................................................. 9

Regional Market Overview ............................................................................................................................10

Middle East/Africa Region........................................................................................................................................................................................ 10

Table: MEA Oil Consumption (000b/d) .............................................................................................................................................................. 10

Table: Middle East/Africa Oil Production (000b/d) ............................................................................................................................................ 11

Table: Middle East/Africa Oil Refining Capacity (000b/d)................................................................................................................................. 12

Table: Middle East/Africa Gas Consumption (bcm) ............................................................................................................................................ 13

Table: Middle East/Africa Gas Production (bcm) ............................................................................................................................................... 14

Table: Middle East/Africa LNG Exports/(Imports) (bcm).................................................................................................................................... 15

UAE .......................................................................................................................................................................................................................... 15

Business Environment Rankings .................................................................................................................16

UAE .......................................................................................................................................................................................................................... 16

Middle East/Africa Region........................................................................................................................................................................................ 16

Business Environment Ranking................................................................................................................................................................................. 17

Economics – long-term risk ...................................................................................................................................................................................... 18

Politics – long-term risk ........................................................................................................................................................................................... 18

Oil & Gas Growth .................................................................................................................................................................................................... 18

Oil/Gas Reserves ...................................................................................................................................................................................................... 18

Licensing/Regulation ................................................................................................................................................................................................ 18

Competitive Environment.......................................................................................................................................................................................... 18

Business Environment Overview .................................................................................................................19

Political Risk Summary............................................................................................................................................................................................. 19

Economic Risk Summary .......................................................................................................................................................................................... 19

Business Environment Risk Summary ....................................................................................................................................................................... 19

Legal Code/Corruption............................................................................................................................................................................................. 19

Red Tape................................................................................................................................................................................................................... 20

Foreign Direct Investment ........................................................................................................................................................................................ 20

Tax Regime .......................................................................................................................................................................................................... 21

Oil Market Outlook .........................................................................................................................................22

Table: Crude Price Forecasts 2006 .................................................................................................................................................................... 22

Revised Forecasts ..................................................................................................................................................................................................... 22

Table: Oil Price Forecasts.................................................................................................................................................................................. 23

Regional Supply and Demand.......................................................................................................................24

Middle East/Africa.................................................................................................................................................................................................... 24

Table: Oil Production (000b/d) – Middle East/Africa......................................................................................................................................... 25

Table: Oil Consumption (000b/d) – Middle East/Africa ..................................................................................................................................... 26

Global Market Outlook ...................................................................................................................................27

© Business Monitor International Ltd Page 3

5. UAE Oil & Gas Report Q1 2006

Table: Global Oil Consumption (000b/d) ........................................................................................................................................................... 28

Table: Global Oil Production (000b/d)............................................................................................................................................................... 29

Industry Forecast Scenario ...........................................................................................................................30

Oil and Gas Reserves................................................................................................................................................................................................ 30

Oil Supply and Demand............................................................................................................................................................................................ 30

Gas Supply and Demand........................................................................................................................................................................................... 31

LNG .......................................................................................................................................................................................................................... 32

Refining and Oil Products Trade .............................................................................................................................................................................. 32

Revenues/Import Costs ............................................................................................................................................................................................. 32

Table: UAE Oil & Gas – Historic Data & Forecasts ........................................................................................................................................ 33

Other Energy ............................................................................................................................................................................................................ 34

Table: UAE Other Energy – Historic Data & Forecasts .................................................................................................................................... 34

Key Risks to BMI’s Forecast Scenario...................................................................................................................................................................... 34

Economic Outlook..........................................................................................................................................35

Table: Macroeconomic Data and Forecasts........................................................................................................................................................ 38

Competitive Landscape .................................................................................................................................39

Table: Key Domestic And Foreign Companies In the UAE Oil And Gas Sector................................................................................................. 40

Overview/State Role.................................................................................................................................................................................................. 40

BP – Summary .......................................................................................................................................................................................................... 41

Table: Key Upstream Players ............................................................................................................................................................................. 41

Total – Summary....................................................................................................................................................................................................... 42

ConocoPhillips – Summary....................................................................................................................................................................................... 42

ExxonMobil – Summary............................................................................................................................................................................................ 42

Table: Key Downstream Players ........................................................................................................................................................................ 42

Emarat/Eppco/ENOC – Summary............................................................................................................................................................................. 43

Shell – Summary ....................................................................................................................................................................................................... 43

Dolphin – Summary .................................................................................................................................................................................................. 43

Company Monitor...........................................................................................................................................44

Abu Dhabi National Oil Company (ADNOC) ...................................................................................................................................................... 44

Dolphin Energy Ltd (DEL) .................................................................................................................................................................................. 47

Company Analysis .................................................................................................................................................................................................... 47

Emarat – Emirates General Petroleum Corporation ........................................................................................................................................... 50

Company Analysis .................................................................................................................................................................................................... 50

Emirates National Oil Company Limited (ENOC)............................................................................................................................................... 52

Company Analysis .................................................................................................................................................................................................... 52

SWOT Analysis ......................................................................................................................................................................................................... 52

BMI Forecast Modelling .................................................................................................................................54

How we generate our industry forecasts................................................................................................................................................................... 54

Energy Industry ........................................................................................................................................................................................................ 55

Cross checks ............................................................................................................................................................................................................. 55

Sources ..................................................................................................................................................................................................................... 55

© Business Monitor International Ltd Page 4

6. UAE Oil & Gas Report Q1 2006

New This Quarter….

Macroeconomic Forecasts

Real GDP growth is forecast by BMI at 5.6% for 2006, following an estimated 6.4% in 2004. We are assuming

4.6% growth in 2007 and 4.7% in 2008, followed by 4.5% in 2009-2010. Inflationary pressures are the biggest

concern in the UAE economy, particularly in Dubai where steep rental prices rises have been stoking inflation

estimated at around 15-20%. Though the emirate's capping of rental rises on leased properties in November last

year will have taken some of the pressure out of the system, price pressures will continue to be felt.

Business Environment

In the BMI Business Environment Ranking matrix, the UAE receives a lower composite score of 39, demoting the

Gulf state to third out of 16 countries included in the MEA region. The overall business environment is attractive in

a regional context, thanks largely to low levels of perceived political and economic risk, plus the country's

abundant oil and gas resources, and widespread participation by foreign companies. The UAE's reserves to

production ratio (RPR) is one of the region's highest. The state is also one of the most open and westernised Middle

Eastern countries in terms of its hydrocarbons sector.

Oil Market

In Q405, the OPEC basket price averaged around US$54.00 per barrel (/bbl), down from some US$57.50 in Q305.

The average price for 2005 was approximately US$51.10/bbl, with the US crude price reaching US$56.70. For the

opening quarter of 2006, our forecasts are for an OPEC basket price of US$51.50. Assuming some seasonal

weakness in the second quarter (which will be determined largely by US gasoline inventory positions), followed by

a hurricane-free Q3, we are predicting an OPEC basket price for 2006 averaging US$51.30/bbl – broadly

unchanged from the previous year. Our forecasts for the US, Brent and Urals are US$56.80, US$54.80 and

US$50.80/bbl respectively.

Industry Forecast Scenario

BMI expects productive capacity to have reached 3.0mn barrels per day (b/d) by 2007, falling short of government

targets. Actual production is unlikely to be above 2.84mn b/d by 2010. We are assuming 2006 production

averaging 2.7mn b/d (including gas liquids), providing exports of just under 2.4mn b/d. Overall UAE gas

consumption is forecast to reach at least 57bn cubic metres (bcm) by 2010. Production of gas is on the rise, with

70bcm achievable by 2010 – providing exports of 13bcm.

Competitive Environment

The UAE has a state-controlled oil and gas sector. The biggest government vehicle is ADNOC, which dominates

the Abu Dhabi upstream oil sector. It accounts for almost half of the UAE's oil production and 36% of refining

capacity. It operates as part of joint ventures with IOCs. Other major state companies are downstream participants

© Business Monitor International Ltd Page 5

7. UAE Oil & Gas Report Q1 2006

Emarat and ENOC. IOC upstream involvement is extensive, and set to rise as more Abu Dhabi upstream projects

are offered. Foreign groups are active in oil production, gas exports, lubricants supply and petrochemicals schemes.

© Business Monitor International Ltd Page 6

8. UAE Oil & Gas Report Q1 2006

SWOT Analysis

United Arab Emirates Political SWOT

Strengths Standards of living are high for nationals, and comfortable for most

expatriate workers. Consequently, there are few demographic pressures that

would suggest looming social problems.

Despite heightened security measures over the past few years, there is little

evidence that al-Qaeda has the capacity or the desire to attack targets within

the UAE.

The monarchy enjoys strong support nationwide.

Weaknesses Lack of democracy poses long term risks given trends towards greater

popular participation elsewhere in the region.

Sheikh Khalifa bin Zayed assumed the presidency after the death of Sheikh

Zayed al-Nahyan. However, he is equally conservative and is unlikely to

make concerted efforts to address constitutional issues.

The succession lineage is rather murky, raising concerns of longer term

instability.

Opportunities The UAE co-operates closely with other GCC states in security and

economic policy.

The UAE is typically a ‘dove’ within OPEC, sympathetic to the needs of

consumer states, which is good for its relations with the West

Dubai has experienced a smooth political succession following the death of

former ruler Sheikh Maktoum bin Rashid al-Maktoum in January 2006, with

new ruler Sheikh Mohammed bin Rashid al-Maktoum welcomed by most of

the public.

Threats There is a long-running territorial dispute with Iran, which continues to affect

bilateral relations.

The state’s openness has resulted in militants using its good international

transport connections in the past. This suggests that some, albeit limited,

risks of terrorism exist.

© Business Monitor International Ltd Page 7

9. UAE Oil & Gas Report Q1 2006

United Arab Emirates Economic SWOT

Strengths The UAE is a member of the Gulf Co-operation Council, which, as well as

being a free trade zone, is targeting a common currency by 2010.

The UAE has one of the most liberal trade regimes in the Gulf, and attracts

strong capital flows from across the region.

In common with most Gulf states, there are a high number of expatriate

workers at all levels of the economy.

The UAE has successfully diversified its economy, minimising its

vulnerability to oil price movements.

Weaknesses The UAE’s main trading partners are other Gulf states, which increases the

vulnerability of the non-oil sectors to oil price volatility.

The state’s location in a volatile region means that its risk profile is, to some

extent, affected by events elsewhere. US concerns about regional militant

groups and Iranian WMD programmes could affect investor perceptions over

the medium term.

Opportunities Oil prices are expected to stay high over the forecast period.

Economic diversification into gas, tourism, financial services and high-tech

industry offers some protection against volatile oil prices.

Its construction, tourism and financial sectors are growing rapidly, driven by

domestic and foreign investment.

Threats Heavy subsidies on utilities and agriculture and an outdated tax system

contribute to persistent fiscal deficits.

There are fears that bubbles could be forming in the construction sector and

also the stock market.

© Business Monitor International Ltd Page 8

10. UAE Oil & Gas Report Q1 2006

United Arab Emirates Business Environment SWOT

Strengths The UAE is a member of the Gulf Co-operation Council, a six member free

trade zone, and has been a member of the WTO since 1996.

The state has invested large amounts in infrastructure.

The UAE’s diversified economy reduces risks.

An effective production sharing framework means high levels of IOC

participation and growing joint venture investment.

Oil and gas reserves are vast and under-utilised, providing a high R/P ratio

that facilitates medium- to long-term production growth.

Weaknesses Due to the state’s federal nature, regulations are not identical across the

emirates.

The regional economy is oil-dependent. This has historically been very

cyclical, which increases risks for long term projects.

Growth in oil production is subject to OPEC policy and substantial ongoing

investment that can be guaranteed only with continuing IOC participation.

Opportunities Large number of free trade zones offering tax holidays and full foreign

ownership.

Comparatively relaxed rules on expatriate employment.

The UAE’s social stability and relative prosperity means that there is far less

concern for security than in some other Gulf states.

Strong global demand for oil means OPEC needs to expand capacity and

output, allowing UAE oil production to remain at a high level.

Threats The state has a good record on corruption in comparison with regional

peers, although not up to western European standards.

Strong oil prices have massively increased liquidity in the region. This has

resulted in strong financial inflows, increasing risks that projects of lower

investment potential are currently being funded.

Abu Dhabi in particular has less near- to medium-term oil and gas

production upside potential than other Gulf states and investment

opportunities elsewhere in the region could make IOCs less enthusiastic

regarding longer-term UAE participation.

© Business Monitor International Ltd Page 9

11. UAE Oil & Gas Report Q1 2006

Regional Market Overview

Middle East/Africa Region

While the Arabian Gulf states will continue to dominate oil supply in the region, backed by huge and

largely untapped reserves, West and North Africa have an important role to play, with Angola's offshore

deepwater wealth an increasingly important factor. Nigeria is faced with domestic political problems that

could hamper oil expansion, while Libya is exploiting the return of US oil companies to aim for rapid

supply growth. Gas is another important export product for the region, largely in the form of LNG. The

Gulf, North Africa and Nigeria play a growing role in the supply of the world's gas.

Table: MEA Oil Consumption (000b/d)

Country 2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

Algeria 229 242 257 272 288 306 324 343

Angola 33 37 43 50 57 65 75 87

Bahrain 35 37 38 39 40 41 42 44

Egypt 550 566 583 600 618 637 656 676

Iran 1472 1551 1598 1645 1695 1746 1798 1852

Iraq 350 450 550 600 650 700 760 800

Israel 182 185 187 190 193 196 199 202

Kuwait 238 266 271 277 282 288 294 299

Libya 227 234 241 248 255 263 271 279

Nigeria 315 321 337 354 372 390 410 430

Oman 51 53 56 59 62 65 68 71

Qatar 37 41 43 44 46 48 50 52

Saudi Arabia 1629 1728 1763 1815 1870 1926 1984 2043

South Africa 513 525 546 562 585 608 633 658

Turkey 668 688 715 744 774 805 837 870

UAE 296 306 315 325 334 344 355 365

BMI universe 6825 7229 7542 7824 8121 8428 8755 9072

other MEA 2638 2664 2691 2718 2745 2772 2800 2828

Regional total 9462 9894 10233 10542 10866 11200 11555 11900

e/f=BMI estimate/forecast. Historic data: BP Statistical Review of World Energy, June 2005/BMI Research. All

forecasts: BMI Research.

© Business Monitor International Ltd Page 10

12. UAE Oil & Gas Report Q1 2006

Oil use of 8.52mn b/d in 2001 reached an estimated 10.23mn b/d last year. It should average 10.54mn b/d

in 2006 and then rise to around 11.90mn b/d by 2010. The UAE accounted for 3.1% of 2005 regional

consumption, with its market share expected to unchanged through to 2010.

Table: Middle East/Africa Oil Production (000b/d)

Country 2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

Algeria 1857 1933 1965 1980 1985 1995 2000 2025

Angola 885 991 1230 1450 1650 1800 1950 2000

Bahrain 42 41 38 37 36 36 35 35

Egypt 749 708 696 680 660 650 630 610

Iran 3999 4081 4050 4050 4050 4100 4200 4250

Iraq 1350 2027 1900 2200 2500 3000 3200 3500

Israel 0 0 0 0 0 0 0 0

Kuwait 2238 2424 2450 2460 2500 2500 2550 2600

Libya 1488 1607 1640 1645 1650 1680 1710 1750

Nigeria 2263 2508 2550 2560 2585 2600 2650 2700

Oman 823 785 780 770 800 800 790 775

Qatar 917 990 995 1000 1000 1050 1100 1150

Saudi Arabia 10222 10584 10700 10750 11000 11100 11500 11750

South Africa 30 26 24 24 22 20 20 20

Turkey 45 42 36 33 30 27 27 25

UAE 2547 2667 2675 2700 2730 2760 2800 2835

BMI universe 29455 31414 31729 32339 33198 34118 35162 36025

Syria 590 590 580 580 570 570 570 570

Yemen 475 480 485 490 510 510 510 510

other MEA 820 930 930 920 910 900 900 900

Regional total 31340 33414 33724 34329 35188 36098 37142 38005

e/f=BMI estimate/forecast. Historic data: BP Statistical Review of World Energy, June 2005/BMI Research. All

forecasts: BMI Research.

Regional oil production was 30.41mn b/d in 2001, and last year averaged an estimated 33.72mn b/d. It is

set to rise to 38.01mn b/d by 2010. The UAE last year accounted for 7.9% of regional oil supply, but its

market share is expected to be down to 7.5% by the end of the forecast period.

Oil exports are growing steadily, because demand growth is lagging the pace of supply expansion. In

2001, the region was exporting an average 21.89mn b/d. This total had risen to an estimated 23.79mn b/d

© Business Monitor International Ltd Page 11

13. UAE Oil & Gas Report Q1 2006

in 2005 and is forecast to reach 26.11mn b/d by 2010. Angola and Iraq have the greatest production

growth potential, although the latter remains bogged down in local political issues.

Table: Middle East/Africa Oil Refining Capacity (000b/d)

Country 2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

Algeria 450 450 450 600 600 600 600 600

Angola 39 60 60 60 260 260 260 260

Bahrain 249 249 249 249 249 249 249 249

Egypt 730 730 730 730 730 730 730 730

Iran 1584 1624 1624 1700 1750 2000 2200 2200

Iraq 644 644 644 644 700 850 850 850

Israel 220 220 220 220 220 220 220 220

Kuwait 905 905 905 905 1000 1350 1350 1350

Libya 343 375 460 460 460 550 550 550

Nigeria 440 500 540 540 540 540 540 540

Oman 85 85 85 150 235 235 235 235

Qatar 137 137 137 137 137 137 137 137

Saudi Arabia 1911 2061 2061 2061 2300 2300 2500 2500

South Africa 490 490 490 490 490 490 490 490

Turkey 643 641 670 670 750 750 750 750

UAE 645 620 800 1000 1000 1000 1000 1000

BMI universe 9515 9791 10125 10616 11421 12261 12661 12661

other MEA 725 730 733 770 808 849 891 936

Regional total 10240 10521 10858 11386 12229 13110 13552 13597

e/f=BMI estimate/forecast. Historic data: BP Statistical Review of World Energy, June 2005/BMI Research. All

forecasts: BMI Research.

Refining capacity for the region was 9.61mn b/d in 2001, rising gradually to an estimated 10.86mn b/d

last year. Angola, Algeria, Oman, Iraq and Iran are all expected to increase significantly their domestic

refining capacity, with the region's total capacity forecast to reach 13.60mn b/d by 2010 – well ahead of

oil demand, therefore implying substantial net exports of refined products. The UAE's share of regional

refining capacity in 2005 was 7.4%, and its market share is set to remain at this level in 2010.

© Business Monitor International Ltd Page 12

14. UAE Oil & Gas Report Q1 2006

Table: Middle East/Africa Gas Consumption (bcm)

Country 2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

Algeria 21 21 22 25 29 33 38 44

Angola 1 1 2 2 3 4 4 5

Bahrain 10 10 10 11 12 13 14 15

Egypt 25 26 28 32 36 40 44 47

Iran 83 87 90 100 104 110 115 125

Iraq 2 2 3 3 4 5 5 5

Israel 0 2 3 5 6 7 8 8

Kuwait 9 10 10 11 13 17 19 21

Libya 6 6 6 6 7 7 8 8

Nigeria 8 8 9 10 11 11 12 12

Oman 10 11 11 17 17 17 16 16

Qatar 12 15 16 16 16 17 18 18

Saudi Arabia 61 64 67 71 76 81 87 93

South Africa 2 2 3 4 6 8 10 10

Turkey 21 22 25 30 35 40 46 50

UAE 38 40 42 45 49 52 55 57

BMI universe 307 325 345 389 423 462 498 535

e/f=BMI estimate/forecast. Historic data: BP Statistical Review of World Energy, June 2005/BMI Research. All

forecasts: BMI Research.

© Business Monitor International Ltd Page 13

15. UAE Oil & Gas Report Q1 2006

Table: Middle East/Africa Gas Production (bcm)

Country 2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

Algeria 83 82 88 94 101 110 120 130

Angola 1 1 2 2 3 6 9 12

Bahrain 10 10 10 9 8 8 8 7

Egypt 25 27 40 48 55 60 65 68

Iran 82 86 90 100 125 140 150 165

Iraq 2 2 3 4 5 6 7 8

Israel 0 2 3 5 6 7 8 8

Kuwait 9 10 10 11 12 13 14 15

Libya 6 7 8 12 15 18 20 23

Nigeria 19 21 23 25 28 31 33 35

Oman 7 7 7 8 8 8 9 9

Qatar 31 39 43 47 52 57 63 69

Saudi Arabia 61 64 67 71 76 81 87 93

South Africa 0 0 1 1 1 3 5 5

Turkey 1 1 1 1 1 1 1 1

UAE 44 46 53 58 60 64 67 70

BMI universe 381 403 447 495 555 613 665 718

e/f=BMI estimate/forecast. Historic data: BP Statistical Review of World Energy, June 2005/BMI Research. All

forecasts: BMI Research.

In terms of natural gas, the region last year consumed an estimated 345bcm, with demand of 535bcm

targeted for 2010, representing 55% growth. Production of a provisional 447bcm in 2005 should reach

718bcm in 2010, which implies net exports rising from last year's 102bcm to 184bcm by the end of the

period. The UAE's share of gas consumption in 2005 was an estimated 12.2%, while its share of

production was 11.9%. By 2010, its share of gas consumption is forecast to be 10.7%, with the country

accounting for 9.7% of supply.

© Business Monitor International Ltd Page 14

16. UAE Oil & Gas Report Q1 2006

Table: Middle East/Africa LNG Exports/(Imports) (bcm)

Country 2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

Algeria 27.4 25.8 27.8 29.0 30.5 32.4 34.5 36.3

Angola 0.0 0.0 0.0 0.0 0.0 2.5 5.5 7.0

Egypt na 3.0 6.0 8.0 9.5 10.0 10.5 10.5

Libya 0.8 1.1 0.6 1.9 2.8 3.7 4.3 5.2

Nigeria 12.7 12.6 14.0 15.0 17.5 19.8 21.5 23.0

Oman 9.0 9.0 10.0 16.1 15.8 15.4 15.0 14.6

Qatar 19.4 24.1 27.6 31.4 35.9 40.4 45.6 51.4

Turkey (6.5) (4.3) (4.9) (5.9) (6.9) (8.0) (9.2) (10.0)

UAE 6.8 7.4 10.1 11.9 10.1 11.0 11.0 11.9

BMI universe 69.6 78.7 91.3 107.5 115.1 127.3 138.9 150.1

e/f=BMI estimate/forecast. Historic data: BP Statistical Review of World Energy, June 2005/BMI Research. All

forecasts: BMI Research.

The leading LNG exporter by 2010 will be Qatar (+86%), via its many IOC-partnered schemes. There

will also be growing volumes from Egypt, Nigeria, Libya and Algeria. Angola has significant longer term

gas export potential, although the first volumes have yet to flow and the most rapid growth phase will

occur in the next decade. Turkey is set to be a key gas importer, although LNG volumes will be modest as

the country raises pipeline supplies from the likes of Azerbaijan and Iran.

UAE

The collection of states that forms the UAE has proven oil reserves estimated at 97.5bn barrels, or nearly

10% of the world total. It also houses the world's fifth biggest natural gas reserves at 6,060bcm and

exports significant amounts of LNG to Japan. Abu Dhabi dominates the UAE oil and gas sector, with

94% of its oil (over 92bn barrels). Dubai contains just 4bn barrels of reserves, followed by Sharjah and

Ras al-Khaimah, with 1.5bn and 100mn barrels respectively. The UAE is a member of OPEC and its

current production quota is 2.44mn b/d, compared with recent crude oil output of 2.48mn b/d. The UAE

has an estimated production capability of 2.65mn b/d (crude alone). There are also significant volumes of

gas liquids that are exempt from OPEC quotas. There are six operational refineries providing capacity of

approximately 620,000b/d. UAE oil consumption is around 315,000b/d, while its gas demand of 42cm

falls well short of production at an estimated 53bcm. UAE electricity generating capacity stands at 5.6

gigawatts (GW) – just 0.3% of the world total. Under the UAE's constitution, each emirate controls its

own oil production and resource development. Although Abu Dhabi joined OPEC in 1967 (four years

before the UAE was formed), Dubai does not consider itself part of OPEC or bound by its quotas.

© Business Monitor International Ltd Page 15

17. UAE Oil & Gas Report Q1 2006

Business Environment Rankings

UAE

The overall business environment is attractive in a regional context, thanks largely to low levels of

perceived political and economic risk, plus the country's abundant oil and gas resources – and widespread

participation by foreign companies. The UAE's reserves to production ratio (RPR) is one of the region's

highest, providing either a very long reserves life, or the potential to increase substantially output of oil

and gas. Scope for output growth may be more limited than in other Gulf states, but the UAE is one of the

most open and westernised Middle Eastern countries in terms of its hydrocarbons sector, with more

limited state control and an established competitive landscape featuring a number of leading IOCs

operating independently or in partnership with national entities.

Since the previous quarter, the UAE's composite score has fallen by two points to 39, with the result that

it has lost its second place in the regional league table to Qatar (which, in turn, slipped behind Libya).

Given that Qatar has more to offer IOCs at present than the UAE, in spite of its much smaller output of

oil and gas, the UAE cannot expect to overtake it. However, both Qatar and the UAE have the potential to

knock Libya from its top spot. The UAE is relatively mature in Middle Eastern terms, without the

reserves and production upside potential present in Qatar. It is, however, a stable and attractive

environment in which to do business. The only real weakness is the ability to raise production levels,

which is governed partly by OPEC policy and partly by capacity issues. We therefore believe it will be

tough for the UAE to keep up with Qatar, but it should be able to keep South Africa, Iraq and Kuwait at

bay.

Middle East/Africa Region

Since the previous quarter, there have been a number of significant changes in the league table of

business environment ratings, although the laggards have largely held position. Qatar has slipped from

first place to second, thanks to a three-point fall in its composite score. Libya has surged past both Qatar

and the UAE to take the top slot, benefiting from a single-point gain in its composite score. Given that the

ranking is being distorted by the use of a favourable short-term economic outlook rating, Libya's position

isn't a true reflection of the overall business environment. We expect slippage later in the year, with Qatar

still the best-placed country to dominate the region. South Africa remains in fourth position, even after a

two-point decline in its score. Iraq moves up to take a share of fifth place, alongside Kuwait, but is

another beneficiary of a flattering short-term economic rating. Oman drops from a share of seventh to

equal eighth, keeping company with Israel. Egypt is down from joint ninth to outright 10th, with a three-

point fall in its composite score. Nigeria has clawed its way up from 15th to a share of 14th, thanks to a

higher score of 25. It shares the penultimate position with Saudi Arabia, while Iran continues to hog the

foot of the table.

© Business Monitor International Ltd Page 16

18. UAE Oil & Gas Report Q1 2006

Main characteristics of the region are the high level of oil/gas reserves, combined with patches of strong

supply growth potential. Regulatory, licensing and competitive environments are generally improving,

with more IOC money moving in and reduced government interference. However, relatively few

countries in the region score highly on long-term political and economic risk assessment.

Table: Middle East/Africa Business Environment Ranking

Country Economics Politics – Oil/Gas Oil/Gas Licensing/ Competitive Composite Regional

– LT Risk LT Risk Growth Reserves Regulation Environment Score Rank

Libya* 10 6 5 6 8 6 41 1

Qatar 6 9 5 7 6 6 40 2

UAE 9 8 3 6 7 6 39 3

South Africa 6 9 4 1 10 6 36 4

Iraq* 2 3 9 10 4 7 35 5=

Kuwait 8 10 3 7 2 5 35 5=

Angola* 3 4 10 3 7 7 34 7

Oman 4 7 4 4 7 5 31 8=

Israel 5 7 3 1 8 7 31 8=

Egypt 4 6 3 3 8 6 30 10

Bahrain 7 5 2 2 8 6 29 11=

Algeria 4 3 5 3 8 7 29 11=

Turkey 3 6 3 3 8 5 28 13

Nigeria 1 1 5 6 5 5 23 14=

Saudi Arabia 6 4 4 5 1 3 23 14=

Iran 2 2 4 8 1 4 21 16

LT Economic Risk: Based on BMI Country Risk Service Long Term economic risk rating. LT Political Risk: Based on BMI Country Risk

Service Long Term political risk rating. Oil/Gas Growth: Based on BMI forecasts for 2005-2010 oil/gas supply growth and oil/gas

demand growth. Oil/Gas Reserves: Based on oil and gas reserves/production (R/P) ratio for last calendar year. Licensing/Regulation:

Based on BMI assessment of upstream licensing framework, regulatory regime and price controls. Competitive Environment: Based on

BMI assessment of number, size and type of oil/gas sector participants; extent of state involvement. Composite Score: Unweighted total

of preceding six scores. Regional Rank: Highest composite score = most attractive energy sector environment within the Middle

East/Africa region; lowest composite score = least attractive. Source: BMI Research. * Based on short-term economic risk rating, as long-

term economic risk rating unavailable.

Business Environment Ranking

In the BMI Business Environment Ranking matrix, the UAE receives a composite score of 39, putting the

Gulf state third out of 16 countries included in the MEA region. The component parts of UAE's score are:

© Business Monitor International Ltd Page 17

19. UAE Oil & Gas Report Q1 2006

Economics – long-term risk

Using the BMI Country Risk Rating Service, the long-term economic rating is 71.6, compared with a

global average of 60.5. In the MEA region, UAE has the second highest score, ahead of Kuwait. The

regional average is 58.0. UAE therefore scores nine out of a possible 10 in our ranking.

Politics – long-term risk

Using the BMI Country Risk Rating Service, the long term political rating is 68.3, compared with a

global average of 63.0. In the MEA region, UAE has the fourth highest score, above that of Oman. The

regional average is 58.9. UAE therefore scores eight out of a possible 10 in our ranking.

Oil & Gas Growth

Countries are ranked by oil and gas output growth and/or consumption growth. UAE's oil production

growth to 2010 is forecast at 6.0%, with gas output rising 26.4% over the same period. This growth rate is

below the middle of the range for MEA states and UAE is allocated a score of three out of a possible 10.

Oil/Gas Reserves

Countries are ranked by their reserves to production ratio (RPR), which reflects the life of oil and gas

reserves and provides an indicator of potential production upside potential. UAE's oil RPR of 100 is third

highest in the region, while the gas RPR of 114 is the 7th highest. The overall score is therefore 6.

Licensing/Regulation

The score is based on the extent of state ownership and the degree of deregulation. The UAE participates

in most upstream projects, gas export schemes and refineries, but in partnership with IOCs through clear

production sharing terms etc. The score of 7 is therefore one of the highest in the region.

Competitive Environment

This assesses the extent of competition and the scale of investment opportunity for IOCs. There is

extensive IOC involvement in the UAE's hydrocarbons sector, with foreign operators accounting for up to

half of oil production and refining capacity. We have therefore assigned the country a score of 6.

© Business Monitor International Ltd Page 18

20. UAE Oil & Gas Report Q1 2006

Business Environment Overview

Political Risk Summary

The UAE is comprised of seven emirates, of which Abu Dhabi is by far the most powerful, due to its oil

wealth. The UAE is very conservative, and is one of the last Gulf states to broaden participation in the

political process. It is unlikely that any elected institutions with more than advisory powers will be

established over the medium term. Despite the lack of democracy, the UAE’s strong economic

performance has largely fended off the social pressures affecting other Gulf states in recent years.

Consequently, militant Islam has failed to attract any significant level of support. The state is a full

member of the GCC, WTO and OPEC, where it is usually a ‘dove,’ supporting efforts by consumer

countries – especially those by key ally the US – to stabilise, rather than maximise, prices. We anticipate

continued political and social stability over the forecast period and beyond.

Economic Risk Summary

In common with most Gulf states, oil is the dominant economic sector, and directly accounts for over

20% of GDP. As elsewhere, this boon has resulted in structural economic problems, notably persistent

fiscal deficits. However, the UAE government has pursued a more enlightened strategy than its regional

peers, prioritising economic diversification – notably in the tourism, manufacturing (including high-tech)

and financial sectors – as part of its outward-oriented development strategy. We anticipate that real

growth will remain above 4% per year over the forecast period.

Business Environment Risk Summary

The UAE has one of the most open business environments in the region. It has actively welcomed foreign

investment in both the hydrocarbons and non-hydrocarbons sectors. Furthermore, the open-border foreign

labour policy has enabled the private sector to recruit expatriate workers at internationally competitive

prices. There are a large number of free zones, primarily located in Dubai, which offer tax holidays and

relaxed restrictions on foreign ownership. Furthermore, the current construction boom is improving

infrastructure. Continued efforts to improve transparency and incentives for investors are anticipated over

the forecast period, although privatisation will remain slow.

Legal Code/Corruption

The UAE's judicial system is based on British and Islamic law. The country has a comparatively good

record on transparency. The state was ranked joint 29th (out of 1463) in Transparency International's

Corruptions Perceptions Index in 2004, with its score of 6.1 markedly better than the Middle East average

of 4.1. The Western Europe average was 7.9.

© Business Monitor International Ltd Page 19

21. UAE Oil & Gas Report Q1 2006

Red Tape

Despite a reputation as a welcoming destination for investment, the UAE compares poorly with its

regional peers, and also against developed states in terms of the regulations covering business practices.

According to World Bank data, it takes 53 separate procedures to enforce a contract, which takes an

average of 614 days. The MENA average is 31 and 299 respectively, while the process involves 18

procedures and 213 in high-income OECD states. Similarly, World Bank data states that it takes 12

procedures and 54 days to start a business in the UAE, compared to an average of 9 and 41 respectively in

the MENA region, and 6 and 25 in high income OECD states. At the other end, it can take approximately

five years to close a business, compared to an average of 3.7 years in the MENA region and 1.8 years in

OECD states.

Foreign Direct Investment

Gradually, the UAE’s investment climate is becoming more clement for foreign direct investors: the

federal government, led by Abu Dhabi, has made significant headway in the past five years in increasing

the role of the private sector. Yet the overall legal framework continues to favour local over foreign

investors – a fact that partly reflects the benign macro environment in light of the country’s substantial oil

revenue windfall. This has endowed local and regional Gulf investors with substantial liquidity,

disincentivising the search for new FDI sources from outside the region.

Some procedures have been eased for investors: for example, they no longer need to obtain a labour

ministry card in addition to an immigration visa. And the absence of income tax compensates for the

restrictive investment environment. FDI figures remain difficult to verify: the finance & industry minister

has spoken of US$9bn FDI inflows for 2004, but this would represent a 20-fold increase on the

US$480mn recorded by UNCTAD in 2003; an unlikely increase in such a short space of time.

Foreign investment in the UAE is governed by the Federal Commercial Companies Law 8, last amended

in 1993, although there are three other key laws: the Commercial Agencies Law, the Federal Industry

Law, and the Government Tenders Law. Firms establishing in the emirates must have a minimum of 51%

UAE national-ownership (though full profit repatriation is permitted). Private or public shareholding

companies have to be fully owned by UAE nationals and there is no national treatment for investors in the

UAE. The branch offices of foreign companies are required to have a national agent. Outside the free

zones, foreign companies have to work through a local sponsor.

Foreign investors may not own land or real estate in the UAE – all property has to be either rented or

leased. The picture is not uniform on account of the federal make-up of the seven-member UAE. Dubai,

lacking Abu Dhabi’s oil revenues, has a more liberal approach to foreign ownership of land and has

extended foreign ownership of land and properties to some real estate developments. In 2002, it permitted

freehold real estate ownership for non-Gulf Co-operation Council (GCC) nationals – but even here there

© Business Monitor International Ltd Page 20

22. UAE Oil & Gas Report Q1 2006

are caveats. Non-GCC owners are not given access to the full range of legal protections and transactions

enjoyed by GCC investors. There are also potential concerns for investors should the UAE federal

government invoke its right to issue a law barring foreign ownership of Dubai property.

The authorities are making some headway at opening up the investment climate: Abu Dhabi has mooted a

law that may allow 100% ownership rights for foreign investors, while the telecoms market was opened

to foreign investment in January 2005 after the monopoly of the local telco, Etisalat, was revoked.

There exist no restrictions on the conversion of the UAE dirham or foreign currency. No expropriations

have affected foreign investors in the UAE for a number of years.

The main destinations for FDI are ICT and software, tourism and textiles. The main sources of FDI are

the UK, the US and India.

Tax Regime

The UAE’s substantial hydrocarbons resource revenues means government has no pressing need to raise

income via direct taxes.

Only banks and oil companies pay corporate tax, at a rate of 50% (55 % in Dubai) for oil companies. Oil

companies also pay royalties on oil and gas they produce. Net taxable income of foreign banks is subject

to tax at a flat rate of 20%, implemented in Abu Dhabi and Dubai. Alongside all the other benefits

enjoyed by companies operating in the free trade zones, there is no corporate tax for 15 years, renewable

for an additional 15 years.

There is no income tax on individuals resident in the UAE. There is no VAT in the UAE, but the federal

government, under the advice of the IMF, is discussing the introduction of a VAT system. This is unlikely

to be introduced in the near term, however. There are no withholding or capital taxes. Business properties

pay a municipal tax set at 10% of annual rental value. Double taxation agreements exist with France,

Pakistan, Poland, Turkey, China, Romania, Italy, Egypt, Germany, Singapore, Malaysia, Indonesia and

India.

© Business Monitor International Ltd Page 21

23. UAE Oil & Gas Report Q1 2006

Oil Market Outlook

After the high drama of the third quarter, with hurricane devastation leading to a volatile oil market, the

closing quarter of 2005 was a much more subdued affair. There were only two major factors at play,

namely the recovery of US production and demand, plus the arrival of winter weather. There were several

important third-party downgrades in consumption forecasts for 2005, but estimates for 2006 demand

remained relatively robust. Fears that US fuel consumption would emerge dramatically lower in the wake

of the hurricanes proved unfounded. However, US crude oil inventories rose quickly during the final

quarter and oil prices were generally on a weakening trend. Only persistently low levels of refined

products stocks in the US and some unusually low temperatures in Europe and North America kept oil

prices above US$50 per barrel. OPEC's December meeting left the production ceiling unchanged, but the

organisation promised an end-January meeting to review the situation. There are now concerns that the

cartel will recommend a supply cut in order to ease over-supply – although a revival in oil prices in the

opening days of the new year may rule out this course of action until the second quarter. Our fourth

quarter and full year price forecasts for 2005 proved accurate, but is has become clear that an upwards

revision is necessary for 2006, with average prices likely to remain close to the 2005 levels.

Table: Crude Price Forecasts 2006

Q405e Q106f Q206f Q306f Q406f

Brent (US$/bbl) 58.9 55.0 52.0 55.0 57.0

Urals (US$/bbl) 53.2 51.0 48.0 51.0 53.0

WTI (US$/bbl) 60.0 57.0 54.0 57.0 59.0

OPEC Basket (US$/bbl) 54.8 51.5 48.5 51.5 53.5

Arab Light (US$/bbl) 53.5 53.2 50.1 53.2 55.3

Source: BMI research

Revised Forecasts

In Q405, we estimate that the OPEC basket price will have averaged US$54.00/bbl, up approximately

30% from the Q404 level, but down from some US$57.50 in Q305. The average price for the whole of

2005 appears to have been US$51.10/bbl, with the US crude price reaching an impressive US$56.70,

Brent averaging around US$54.70 and Russian Urals at US$50.40/bbl. For the opening quarter of 2006,

our forecasts are for an OPEC basket price of US$51.50. The main marker blends are expected to average

US$57/bbl for the US, US$55/bbl for Brent and US$51/bbl for Urals.

© Business Monitor International Ltd Page 22

24. UAE Oil & Gas Report Q1 2006

Assuming some seasonal weakness in the second quarter (which will be determined largely by US

gasoline inventory positions), followed by a hurricane-free Q3, we are predicting an OPEC basket price

for 2006 averaging US$51.30/bbl – broadly unchanged from the previous year. Our forecasts for the US,

Brent and Urals are US$56.80, US$54.80 and US$50.80/bbl respectively.

It seems clear from our supply and demand projections that, beyond 2007, demand growth could exceed

supply expansion. However, surplus capacity is also set to develop among the OPEC nations, providing a

psychological 'safety net' for the oil market that will inevitably relieve some of the upwards pressure on

prices. If OPEC exercises production constraint, it can no doubt hold oil prices near recent levels.

Equally, if it expands capacity and shows a willingness to continue over-supplying the crude market, it

should be able to deliver somewhat lower prices. We feel relatively confident that, by the end of the

forecast period (now extended to 2010), oil prices will have fallen back to the US$40 level. This view is

shared by senior industry figures and reflects the fact that increased investment in supply is likely to

generate a surplus of capacity by the end of the decade. In the meantime, however, we see scope for

prices to remain relatively firm.

For 2007, we are now assuming an OPEC basket price of US$50/bbl, which implies US$55.40 for the

US, US$53.40 for Brent and US$49.50 for Urals. Prices are then forecast to fall by around US$5/bbl in

2008, with the OPEC price averaging US$45/bbl. For 2009/10, we are predicting as further decline to an

average US$40/bbl, providing a US price of just over US$44/bbl. Should OPEC re-introduce a price

targeting system, it may be able to sustain US$50/bbl crude for the foreseeable future.

Table: Oil Price Forecasts

2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

OPEC Basket (US$/bbl) 28.1 35.7 51.0 51.3 50.0 45.0 40.0 40.0

WTI (US$/bbl) 31.1 41.5 56.2 56.8 55.4 49.8 44.3 44.3

Brent (US$/bbl) 28.8 38.2 54.6 54.8 53.4 48.1 42.7 42.7

Urals (US$/bbl) 27.0 33.3 50.2 50.8 49.5 44.6 39.6 39.6

e/f=BMI estimate/forecast.

© Business Monitor International Ltd Page 23

25. UAE Oil & Gas Report Q1 2006

Regional Supply and Demand

Middle East/Africa

Both the Middle East and Africa are set to play an increasingly important role in world oil supply, even if

the demand story for the region is relatively unexciting. Gulf states will remain the dominant producers,

but Africa has plenty of upside potential. Overall MEA production averaged an estimated 33.72mn b/d in

2005, thanks largely to OPEC's higher production levels Gains were seen last year from most OPEC

members, as well as from Angola.

Given capacity constraints, significant expansion from here onwards lies outside of the OPEC 10 group.

Iraq remains the region's 'wild card', having near-term production potential of 2.5mn b/d and longer-term

scope for 3-4mn b/d. For the region as a whole, we expect to see output reach 38.01mn b/d by 2010,

representing a gain of 12.7% over 2005. Apart from the 60% rise in Angola's output and likely dramatic

growth in Iraq, the supply winners will be Libya and Nigeria, with Egypt the most significant loser. With

consumption set to reach 11.90mn b/d in 2010, up from a provisional 10.23mn b/d in 2005, the growing

export capability is clearly vast. Some 26.11mn b/d is likely to be exported in 2010, up from last year's

estimated 23.49mn b/d.

© Business Monitor International Ltd Page 24

26. UAE Oil & Gas Report Q1 2006

Table: Oil Production (000b/d) – Middle East/Africa

2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

Algeria 1857 1933 1965 1980 1985 1995 2000 2025

Angola 885 991 1230 1450 1650 1800 1950 2000

Bahrain 42 41 38 37 36 36 35 35

Egypt 749 708 696 680 660 650 630 610

Iran 3999 4081 4050 4050 4050 4100 4200 4250

Israel 0 0 0 0 0 0 0 0

Kuwait 2238 2424 2450 2460 2500 2500 2550 2600

Libya 1488 1607 1640 1645 1650 1680 1710 1750

Nigeria 2263 2508 2550 2560 2585 2600 2650 2700

Oman 823 785 780 770 800 800 790 775

Qatar 917 990 995 1000 1000 1050 1100 1150

Saudi Arabia 10222 10584 10700 10750 11000 11100 11500 11750

South Africa 30 26 24 24 22 20 20 20

Turkey 45 42 36 33 30 27 27 25

UAE 2547 2667 2675 2700 2730 2760 2800 2835

BMI universe 28105 29387 29829 30139 30698 31118 31962 32525

Iraq 1350 2027 1900 2200 2500 3000 3200 3500

Syria 590 590 580 580 570 570 570 570

Yemen 475 480 485 490 510 510 510 510

other MEA 820 930 930 920 910 900 900 900

Regional total 31340 33414 33724 34329 35188 36098 37142 38005

e/f=BMI estimate/forecast. Historic data: BP Statistical Review of World Energy, June 2005/BMI Research. All

forecasts: BMI Research.

© Business Monitor International Ltd Page 25

27. UAE Oil & Gas Report Q1 2006

Table: Oil Consumption (000b/d) – Middle East/Africa

2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

Algeria 229 242 257 272 288 306 324 343

Angola 33 37 43 50 57 65 75 87

Bahrain 35 37 38 39 40 41 42 44

Egypt 550 566 583 600 618 637 656 676

Iran 1472 1551 1598 1645 1695 1746 1798 1852

Iraq 350 450 550 600 650 700 760 800

Israel 182 185 187 190 193 196 199 202

Kuwait 238 266 271 277 282 288 294 299

Libya 227 234 241 248 255 263 271 279

Nigeria 315 321 337 354 372 390 410 430

Oman 51 53 56 59 62 65 68 71

Qatar 37 41 43 44 46 48 50 52

Saudi Arabia 1629 1728 1763 1815 1870 1926 1984 2043

South Africa 513 525 546 562 585 608 633 658

Turkey 668 688 715 744 774 805 837 870

UAE 296 306 315 325 334 344 355 365

BMI universe 6825 7229 7542 7824 8121 8428 8755 9072

other MEA 2638 2664 2691 2718 2745 2772 2800 2828

Regional total 9462 9894 10233 10542 10866 11200 11555 11900

e/f=BMI estimate/forecast. Historic data: BP Statistical Review of World Energy, June 2005/BMI Research. All

forecasts: BMI Research.

© Business Monitor International Ltd Page 26

28. UAE Oil & Gas Report Q1 2006

Global Market Outlook

2006: A Year Of Recovery

Demand growth is set to move back above 2.0% this year, thanks in part to a recovery from the hurricane-

induced setbacks of 2005. Supply growth should also be robust, albeit potentially lower than the rate of

demand expansion. All-in-all, we should expect a year of recovery and a continuation of high oil prices.

However, the scope for price surprises on the upside is limited unless other exceptional events occur.

Our data suggest demand of 83.88mn b/d in 2005 climbing steadily to 94.09mn b/d in 2010. This 12.2%

expansion will be the best seen for decades and assumes growth averaging more than 2% per annum

throughout the period. There is a distinct divergence of OECD and non-OECD trends. The former is

typically expanding by 1.0-1.2% per annum, with consumption forecast to rise from 43.36mn b/d in 2005

to 45.82mn b/d in 2010. For the latter segment, annual growth is likely to be nearer 3.6% as demand

climbs from 40.52mn b/d to 48.27mn b/d. By around 2008, non-OECD countries will be devouring as

much oil as the OECD states.

In terms of oil supply, there needs to be corresponding expansion in order to retain some form of 'control'

over prices. A prolonged period of under-investment, starting in 1998, may now have come to an end.

High prices are encouraging oil companies to change their investment criteria. It is, however, apparent

that major oil companies are finding it tough to deliver volume growth. The impact of higher spending

will take a while to come through, so the market is dependent increasingly on OPEC and a handful of

other growing producers such as Angola, Brazil, Azerbaijan, Kazakhstan and Russia. Higher levels of

non-OPEC production growth may not be experienced until the end of the decade, although OPEC

capacity expansion could be significant over the medium term.

© Business Monitor International Ltd Page 27

29. UAE Oil & Gas Report Q1 2006

Table: Global Oil Consumption (000b/d)

2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

MEA 9462 9894 10233 10542 10866 11200 11555 11900

NW Europe 14118 14162 14292 14416 14584 14700 14817 14931

N America 22202 22723 23039 23385 23663 23945 24230 24518

Asia/Pacific 22676 23772 24496 25253 26116 27021 27970 28966

Central/Eastern Europe 4640 4841 5049 5263 5488 5722 5968 6226

Latin America 6478 6642 6780 6926 7076 7230 7387 7547

Total 79575 82033 83887 85784 87793 89817 91926 94088

OECD 42520 42862 43365 43899 44411 44875 45345 45815

non-OECD 37056 39171 40523 41885 43382 44943 46582 48273

Demand growth % 1.7 3.1 2.3 2.3 2.3 2.3 2.3 2.4

OECD % 1.3 0.8 1.2 1.2 1.2 1.0 1.0 1.0

Non-OECD % 2.3 5.7 3.5 3.4 3.6 3.6 3.6 3.6

e/f=BMI estimate/forecast. Historic data: BP Statistical Review of World Energy, June 2005/BMI Research. All

forecasts: BMI Research.

We are forecasting global oil supply rising from 86.21mn b/d in 2005 to 94.01mn b/d in 2010. This

implies growth of 9.0%, or an average of less than 2% per annum. On the face of it, supply will struggle

to keep ahead of demand, but the scale of surplus capacity should expand if OPEC members deliver their

promised expansion. Production growth outside of OPEC is put at just 9.2% over the period (to 56.09mn

b/d). OPEC supply expansion is probably going to emerge slightly higher (+11.7%), if Iraq is included.

Expansion of OPEC productive capacity could be nearer 15% during the period, thus cooling the market

to a certain extent. Worryingly, perhaps, for the global economy is a clear increase in the world's

dependence on OPEC oil.

© Business Monitor International Ltd Page 28

30. UAE Oil & Gas Report Q1 2006

Table: Global Oil Production (000b/d)

2003 2004 2005f 2006f 2007f 2008f 2009f 2010f

MEA 31340 33414 33724 34329 35188 36098 37142 38005

NW Europe 6534 6284 5913 5827 5740 5620 5504 5398

N America 10404 10326 10225 10625 10539 10330 10172 10016

Asia/Pacific 7972 8059 8015 7938 7872 7747 7591 7498

Central/Eastern Europe 10645 11575 12024 12580 13227 13865 14413 14862

Latin America 10184 10618 10710 10898 11068 11339 11572 11826

OPEC NGLs 3400 3700 3800 4100 4300 4600 4600 4600

Processing gains 1800 1800 1800 1800 1800 1800 1800 1800

Total 82279 85776 86210 88097 89734 91398 92794 94005

OPEC 10 crude 29332 30900 31050 31195 31595 31870 32680 33315

OPEC, inc Iraq 30682 32927 32950 33395 34095 34870 35880 36815

OPEC 10 inc NGLs 32732 34600 34850 35295 35895 36470 37280 37915

Non-OPEC 49547 51176 51360 52802 53839 54928 55514 56090

supply growth (%) 3.7 4.2 0.5 2.2 1.9 1.9 1.5 1.3

OPEC 10 (%) 9.6 5.7 0.7 1.3 1.7 1.6 2.2 1.7

Non-OPEC (%) 0.2 3.3 0.4 2.8 2.0 2.0 1.1 1.0

e/f=BMI estimate/forecast. Historic data: BP Statistical Review of World Energy, June 2005/BMI Research. All

forecasts: BMI Research.

© Business Monitor International Ltd Page 29

31. UAE Oil & Gas Report Q1 2006

Industry Forecast Scenario

Oil and Gas Reserves

Our view is that the UAE's proven oil reserves will slip gradually over the period to 2010, dropping to

94bn barrels. However, we see scope for some expansion of gas reserves, perhaps to 6,300bcm over the

next five years.

Oil Supply and Demand

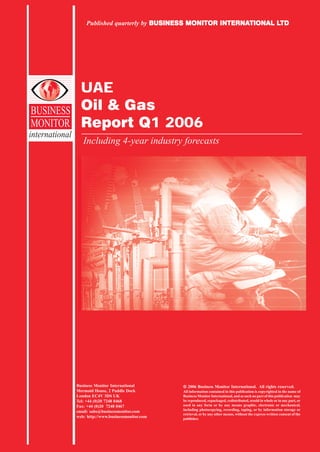

Production from the UAE in

UAE Oil Production, Consumption &

January 2006 averaged 2.48mn b/d,

Exports (2003-2010)

down from 2.56mn b/d in December 3000 2500

last year. Sustainable capacity is 2450

2500

estimated at 2.65mn b/d, so there is 2400

2000

2350

little surplus. State-owned ADNOC

1500 2300

has said that capacity at the Murban

2250

1000

field will be raised from 1.3mn b/d 2200

500

to 1.5mn b/d by March 2006. 2150

Several projects to upgrade 0 2100

2003 2004f 2005f 2006f 2007f 2008f 2009f 2010f

infrastructure at existing oil fields

oil production, 000 b/d oil consumption, 000 b/d

are on the cards or under way. oil exports, 000 b/d (RHS)

There is a US$300mn project to Source: Historic data - BP Review of World Energy; Value data - BMI

Research; Forecasts - BMI Research

increase the capacity of the onshore

Bu Hasa field. The goal is to increase capacity to 480,000b/d. A gas re-injection project also is planned

for the onshore Bab field, which is expected to increase capacity to 350,000b/d. Upgrades planned for the

onshore Asab field should boost capacity from 280,000b/d to 310,000b/d by 2006. These projects are part

of an overall goal of raising the UAE's production capacity to 3.0mn b/d by the end of 2006 – at an

estimated cost of US$1.5bn.

Earlier plans to boost capacity to 3.6mn b/d by 2005 and 4mn b/d by 2010 now look extremely optimistic.

ADNOC brought in ExxonMobil in June 2004 as a strategic partner in the development of the Upper

Zakhum field, with a 28% ownership stake. ExxonMobil is set to undertake a programme of upgrades to

the Upper Zakum field to raise its capacity from the current 550,000b/d to 750,000b/d by 2008, and to

1.2mn b/d by 2010.

BMI expects productive capacity to have reached 3.0mn b/d by 2007, falling short of government targets.

Actual production is unlikely to be above 2.84mn b/d by 2010. We are assuming 2006 production

averaging 2.7mn b/d (including gas liquids), providing exports of just under 2.4mn b/d.

© Business Monitor International Ltd Page 30

32. UAE Oil & Gas Report Q1 2006

Gas Supply and Demand

Over the last decade, gas consumption in Abu Dhabi has doubled, and was projected by local government

sources to reach 41bcm by 2005 (our estimate is for consumption of 42bcm last year). The development

of natural gas fields also results in increased production and exports of condensates, which are not subject

to OPEC production quotas. Dubai’s gas consumption has been growing by nearly 10% annually due to

expansion of the emirate's industrial sector, a switch to gas by its power stations, and the need for an

enhanced oil recovery (EOR) system based on gas injection for its mature oilfields. Overall UAE gas

consumption is forecast to reach at least 57bcm by 2010. Production of gas is on the rise, with 70bcm

achievable by 2010 – providing exports of 13bcm.

In February, the UAE's Dolphin Energy said that it plans to buy additional gas from Qatar to fill the

Gulf’s first cross-border gas pipeline project. Dolphin will apparently in 2007 seek to purchase an

additional 12.4bcm per annum of Qatari gas to feed a new gas pipeline grid connecting the Gulf states.

The gas would then be exported by pipeline to neighbouring countries and should eventually be linked

with a future GCC wide gas network. The GCC states are already in the process of linking their power

generation networks to help cope with rising demand for electricity throughout the region.

Dolphin’s desire to boost by 60% the volume of gas that will flow through its US$3.5bn underwater

pipeline from Qatar starting next year may hinge on Qatar giving it preferential treatment over other

waiting customers. Qatar had last November said that it couldn't take on any new customers before 2007

because of capacity constraints. There are suggestions that spare volumes of gas will not be available until

beyond 2012.

© Business Monitor International Ltd Page 31