Temporal Diversification in Real Estate Portfolios

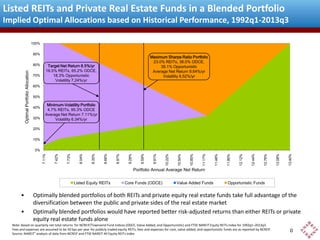

Shows the implied optimal allocations to listed U.S. equity REITs and private equity real estate funds following core, value add, and opportunistic strategies, based on net total returns reported for the historical period 1993q1-2013q3. The minimum-volatility real estate portfolio would have included nearly 5% in listed U.S. equity REITs. Private real estate return measures lag behind actual returns by about 4-5 quarters, producing a "temporal diversification" benefit: when real estate markets turn down, measured returns for private investments are usually still increasing; when measured returns on private real estate finally turn down, listed returns are often already rising. The chart shows an example of an implied optimal allocation for an 8.5% target long-term average net return. It also shows the real estate portfolio allocation that would have maximized risk-adjusted returns (Sharpe ratio) over the historical period with 39.1% invested in opportunistic real estate funds, 38.0% in core funds, and 23.0% invested in listed equity REITs. The reason this chart is not updated is that the NCREIF-Townsend Fund Indices for private equity real estate funds following value-add and opportunistic strategies were discontinued after 2013Q3. Questions? Contact me at bcase@nareit.com.

Recommandé

Contenu connexe

Tendances

Tendances (19)

Similaire à Temporal Diversification in Real Estate Portfolios

Similaire à Temporal Diversification in Real Estate Portfolios (20)

Plus de Brad Case, PhD, CFA, CAIA

Plus de Brad Case, PhD, CFA, CAIA (11)

Dernier

Dernier (20)

Temporal Diversification in Real Estate Portfolios

- 1. Listed REITs and Private Real Estate Funds in a Blended Portfolio Implied Optimal Allocations based on Historical Performance, 1992q1-2013q3 100% 90% Optimal Portfolio Allocation 80% 70% Maximum Sharpe Ratio Portfolio 23.0% REITs, 38.0% ODCE, 39.1% Opportunistic Average Net Return 9.64%/yr Volatility 8.52%/yr Target Net Return 8.5%/yr 16.5% REITs, 65.2% ODCE, 18.3% Opportunistic Volatility 7.24%/yr 60% 50% 40% 30% Minimum-Volatility Portfolio 4.7% REITs, 95.3% ODCE Average Net Return 7.11%/yr Volatility 6.34%/yr 20% 10% 13.40% 13.08% 12.76% 12.44% 12.12% 11.80% 11.48% 11.17% 10.85% 10.54% 10.22% 9.91% 9.59% 9.28% 8.97% 8.66% 8.35% 8.04% 7.73% 7.42% 7.11% 0% Portfolio Annual Average Net Return Listed Equity REITs • • Core Funds (ODCE) Value Added Funds Opportunistic Funds Optimally blended portfolios of both REITs and private equity real estate funds take full advantage of the diversification between the public and private sides of the real estate market Optimally blended portfolios would have reported better risk-adjusted returns than either REITs or private equity real estate funds alone Note: Based on quarterly net total returns for NCREIF/Townsend Fund Indices (ODCE, Value Added, and Opportunistic) and FTSE NAREIT Equity REITs Index for 1992q1–2013q3. Fees and expenses are assumed to be 50 bps per year for publicly traded equity REITs; fees and expenses for core, value added, and opportunistic funds are as reported by NCREIF. Source: NAREIT® analysis of data from NCREIF and FTSE NAREIT All Equity REITs Index 0