Q2 2014 Houston Industrial Market Report

•Télécharger en tant que PPTX, PDF•

1 j'aime•243 vues

Q2 2014 Houston Industrial Market Report

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (19)

En vedette

En vedette (17)

Similaire à Q2 2014 Houston Industrial Market Report

Similaire à Q2 2014 Houston Industrial Market Report (15)

Plus de Colliers International | Houston

Plus de Colliers International | Houston (20)

Dernier

Dernier (20)

Q2 2014 Houston Industrial Market Report

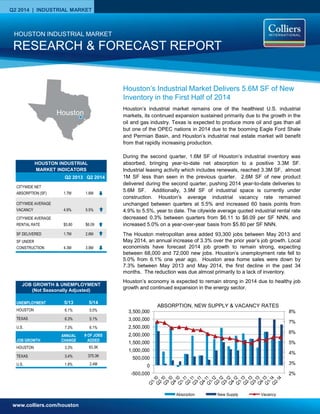

- 1. www.colliers.com/houston Q2 2014 | INDUSTRIAL MARKET 2% 3% 4% 5% 6% 7% 8% -500,000 0 500,000 1,000,000 1,500,000 2,000,000 2,500,000 3,000,000 3,500,000 Absorption New Supply Vacancy Houston’s industrial market remains one of the healthiest U.S. industrial markets, its continued expansion sustained primarily due to the growth in the oil and gas industry. Texas is expected to produce more oil and gas than all but one of the OPEC nations in 2014 due to the booming Eagle Ford Shale and Permian Basin, and Houston’s industrial real estate market will benefit from that rapidly increasing production. During the second quarter, 1.6M SF of Houston’s industrial inventory was absorbed, bringing year-to-date net absorption to a positive 3.3M SF. Industrial leasing activity which includes renewals, reached 3.3M SF, almost 1M SF less than seen in the previous quarter. 2.6M SF of new product delivered during the second quarter, pushing 2014 year-to-date deliveries to 5.6M SF. Additionally, 3.9M SF of industrial space is currently under construction. Houston’s average industrial vacancy rate remained unchanged between quarters at 5.5% and increased 60 basis points from 4.9% to 5.5%, year to date. The citywide average quoted industrial rental rate decreased 0.3% between quarters from $6.11 to $6.09 per SF NNN, and increased 5.0% on a year-over-year basis from $5.80 per SF NNN. The Houston metropolitan area added 93,300 jobs between May 2013 and May 2014, an annual increase of 3.3% over the prior year’s job growth. Local economists have forecast 2014 job growth to remain strong, expecting between 68,000 and 72,000 new jobs. Houston’s unemployment rate fell to 5.0% from 6.1% one year ago. Houston area home sales were down by 7.3% between May 2013 and May 2014, the first decline in the past 34 months. The reduction was due almost primarily to a lack of inventory. Houston’s economy is expected to remain strong in 2014 due to healthy job growth and continued expansion in the energy sector. RESEARCH & FORECAST REPORT HOUSTON INDUSTRIAL MARKET ABSORPTION, NEW SUPPLY & VACANCY RATES Houston’s Industrial Market Delivers 5.6M SF of New Inventory in the First Half of 2014 HOUSTON INDUSTRIAL MARKET INDICATORS Q2 2013 Q2 2014 CITYWIDE NET ABSORPTION (SF) 1.7M 1.6M CITYWIDE AVERAGE VACANCY 4.9% 5.5% CITYWIDE AVERAGE RENTAL RATE $5.80 $6.09 SF DELIVERED 1.7M 2.6M SF UNDER CONSTRUCTION 4.3M 3.9M Houston UNEMPLOYMENT 5/13 5/14 HOUSTON 6.1% 5.0% TEXAS 6.3% 5.1% U.S. 7.3% 6.1% JOB GROWTH ANNUAL CHANGE # OF JOBS ADDED HOUSTON 3.3% 93.3K TEXAS 3.4% 375.3K U.S. 1.8% 2.4M JOB GROWTH & UNEMPLOYMENT (Not Seasonally Adjusted)

- 2. RESEARCH & FORECAST REPORT | Q2 2014 | HOUSTON INDUSTRIAL MARKET COLLIERS INTERNATIONAL | P.2 Vacancy & Availability Houston’s industrial vacancy rate remained unchanged between quarters at 5.5%, and increased by 60 basis points from 4.9% to 5.5%, year to date. At the end of the second quarter, Houston had 26.8M SF of vacant industrial space. Among the major industrial corridors, the Northeast Corridor has the lowest vacancy rate at 3.2%, followed by the Northwest Corridor at 4.1% and then the Southern Corridor at 4.2%. The largest concentration of vacancy is located in the North Corridor, with an 8.0% vacancy rate. Houston’s industrial construction pipeline had 3.9M SF of projects underway at the end of the second quarter, the majority of which being spec development. The largest project under construction is Panattoni’s 441,000-SF spec warehouse located on N. Gessner in the Northwest Corridor. A list of buildings currently under construction can be found on Page 4 of this report. Rental Rates According to CoStar, our data service provider, Houston’s citywide average quoted industrial rental rate for all product types decreased 0.3% from $6.11 per SF NNN in the first quarter to $6.09 per SF NNN in the second quarter. According to Colliers’ internal data, actual lease transactions are in the $4.44 – $4.92 per SF NNN range for newer bulk industrial spaces, while flex rates are ranging from $6.60 to $9.00 per SF, depending on the allowance for tenant improvements and the location of the property. By property type, the average quoted NNN rental rates are as follows: $5.71 per SF for Warehouse Distribution space; $4.34 per SF for Bulk Logistics space; $10.11 per SF for Flex/Service space; with Tech/R&D space averaging $10.87 per SF, according to CoStar. Absorption & Demand Houston’s industrial market posted 1.6M SF of positive net absorption in the second quarter, with the North Corridor submarket contributing the largest amount, 821,071 SF, followed by the Northwest Corridor which posted 284,086 SF, the Southwest Corridor at 259,871 SF, and the Southern Corridor at 221,969 SF of net positive absorption. There were several major tenant move-ins contributing to net absorption gains in the second quarter, including Kauffman Tire (91,200 SF); Atlanta Food International (84,600 SF); Poly Bags (62,600 SF); International Rags, Ltd. (62,500 SF); Gas Process Equipment Co. (47,500 SF); FreshPak (44,800 SF); Chadwell Supply (43,500 SF); ToolMart (38,100 SF) and Nordyne LLC (37,500 SF). Leasing Houston’s industrial leasing activity reached 3.3M SF in the second quarter. A list of select second quarter industrial lease transactions are included in the table below. 1 Renewal 2 Expansion 3 Sublease 4Pre-lease proposed or under construction Building Name/Address Submarket SF Tenant Lease Date 1701 Crosspoint Avenue Southwest Far 72,505 BASF1 Jun-14 Carson Commerce Center East-Southeast Far 67,742 Elliott Electric Co. Apr-14 11629 N Houston Rosslyn Rd Hwy 290/Tomball Pky 47,500 Gas Process Equipment Co. Apr-14 8615 North Loop E Northeast Hwy 90 36,352 RL Building Supply, LLC May-14 Sam Houston Pkwy Dist Ctr Northwest Inner Loop 33,730 Graniti Vicentia, LLC May-14 Udelson Industrial Park North Outer Loop 30,000 Max Torque, LLC May-14 East Belt Business Park 4 East-Southeast Far 25,267 Jotun Paints Apr-14 Candlebridge Park North Hardy Toll Road Ind 20,400 Delta Subsea Apr-14 Clay-Campbell Business Park Northwest Inner Loop 19,950 Prairie Supply1 Jun-14 Greenspoint Business Center North Hardy Toll Road Ind 17,775 Tellworks Communications Jun-14 Northwoods Industrial Park West Outer Loop 13,125 Gulf Coast Conversions1 Apr-14 Q2 2014 SELECT INDUSTRIAL LEASES

- 3. RESEARCH & FORECAST REPORT | Q2 2014 | HOUSTON INDUSTRIAL MARKET COLLIERS INTERNATIONAL | P.3 Houston Industrial Market Summary Sales Activity Q2 2014 Total Sales : $570M No. of Properties: 81 Total SF: 4.3M Average $/SF: $45 Average Cap Rate: 8.6% Falcon Southwest sold a 377,752-SF 12-building industrial warehouse portfolio to Hartman Mitchelldale Business Park, LLC for $19.2M or $51 per SF. The portfolio is 87.2% leased to various tenants. The buildings in the industrial park were built in 1979 and remodeled in 2004. C&W Investments sold a 151,260-SF Class B industrial warehouse to STAG Industrial Management, LLC for $8.9M or $59 per SF. The building is 100% leased to Smart Warehousing through April 2021. The reported cap rate was 8.6%. Sources: Real Capital Analytics; CoStar Comps 5400 Mitchelldale St 12614 Hempstead Rd Market Rentable Area Direct Vacant SF Direct Vacancy Rate Sublet Vacant SF Sublet Vacancy Rate Total Vacant SF Total Vacancy Rate 2Q14 Net Absorption 1Q14 Net Absorption 2Q14 Completions 1Q14 Completions SF Under Construction Greater Houston Total 491,720,505 26,181,150 5.3% 637,355 0.1% 26,818,505 5.5% 1,583,925 1,755,866 2,645,694 2,951,422 3,930,859 CBD-NW Inner Loop 11,500,406 559,996 4.9% 31,860 0.3% 591,856 5.1% 62,709 15,767 - - - Downtown 31,814,637 1,751,102 5.5% - 0.0% 1,751,102 5.5% (1,720) 101,850 - - - North Inner Loop 5,076,141 534,906 10.5% - 0.0% 534,906 10.5% - (21,525) - - - Southwest Inner Loop 7,198,717 61,171 0.8% - 0.0% 61,171 0.8% (15,601) - - - - CBD Corridor Total 55,589,901 2,907,175 5.2% 31,860 0.1% 2,939,035 5.3% 45,388 96,092 - - - North Fwy/Tomball Pky 17,347,742 1,489,803 8.6% 5,346 0.0% 1,495,149 8.6% 225,898 (66,181) 873,068 250,255 926,180 North Hardy Toll Rd 29,108,673 2,747,187 9.4% 59,122 0.2% 2,806,309 9.6% 441,818 495,206 449,474 797,506 423,440 North Outer Loop 18,791,750 1,386,001 7.4% 1,950 0.0% 1,387,951 7.4% 89,657 178,203 381,250 174,434 120,000 The Woodlands/Conroe 14,413,958 693,531 4.8% - 0.0% 693,531 4.8% 63,698 17,420 18,800 166,900 - North Corridor Total 79,662,123 6,316,522 7.9% 66,418 0.1% 6,382,940 8.0% 821,071 624,648 1,722,592 1,389,095 1,469,620 Northeast Hwy 321 1,201,673 - 0.0% - 0.0% - 0.0% 0 600 - - - Northeast Hwy 90 15,937,684 448,855 2.8% 136,200 0.9% 585,055 3.7% (54,458) (129,095) - 41,356 - Northeast I-10 3,672,845 30,652 0.8% - 0.0% 30,652 0.8% 109,628 12,801 - - - Northeast Inner Loop 11,591,910 430,372 3.7% - 0.0% 430,372 3.7% (7,842) 11,069 - - - Northeast Corridor Total 32,404,112 909,879 2.8% 136,200 0.4% 1,046,079 3.2% 47,328 (104,625) - 41,356 - Hwy 290/Tomball Pky 16,056,280 704,622 4.4% 20,541 0.1% 725,163 4.5% 154,657 72,540 - 105,358 1,578,981 Northwest Hwy 6 4,158,737 141,314 3.4% 24,000 0.6% 165,314 4.0% (24,086) (25,392) - - 357,887 Northwest Inner Loop 58,686,032 2,301,129 3.9% 74,554 0.1% 2,375,683 4.0% 22,402 (34,334) - 177,448 - Northwest Near 17,187,843 462,963 2.7% 49,824 0.3% 512,787 3.0% 26,623 597,368 - 255,962 . Northwest Outlier 17,160,063 1,054,831 6.1% - 0.0% 1,054,831 6.1% 106,728 80,354 79,743 63,382 64,313 West Outer Loop 23,683,929 707,903 3.0% 23,600 0.1% 731,503 3.1% (2,238) 83,495 189,125 332,581 86,250 Northwest Corridor Total 136,932,884 5,372,762 3.9% 192,519 0.1% 5,565,281 4.1% 284,086 774,031 268,868 934,731 2,087,431 East I-10 Outer Loop 13,047,099 264,136 2.0% - 0.0% 264,136 2.0% (1,000) (28,000) - - - East-Southeast Far 47,305,783 4,918,042 10.4% 7,078 0.0% 4,925,120 10.4% (41,123) (76,120) 91,140 385,462 . Southeast Outer Loop 18,374,310 496,361 2.7% 117,573 0.6% 613,934 3.3% (53,665) 33,741 - - - Southeast Corridor Total 78,727,192 5,678,539 7.2% 124,651 0.2% 5,803,190 7.4% (95,788) (70,379) 91,140 385,462 - South Highway 35 31,853,434 1,071,713 3.4% 23,600 0.1% 1,095,313 3.4% 201,820 384,427 327,294 143,390 283,808 South Inner Loop 12,771,468 762,132 6.0% - 0.0% 762,132 6.0% 20,149 51,596 - - - Southern Corridor Total 44,624,902 1,833,845 4.1% 23,600 0.1% 1,857,445 4.2% 221,969 436,023 327,294 143,390 283,808 Highway 59/Highway 90 22,209,481 1,037,827 4.7% 44,500 0.2% 1,082,327 4.9% 66,434 23,694 208,800 30,000 90,000 Southwest Far 10,080,924 536,531 5.3% - 0.0% 536,531 5.3% 89,030 (45,617) - - - Southwest Outer Loop 12,708,006 624,798 4.9% - 0.0% 624,798 4.9% 120,564 (72,481) - - - Sugar Land/Ft Bend Co 18,780,980 963,272 5.1% 17,607 0.1% 980,879 5.2% (16,157) 94,480 27,000 27,388 - Total Southwest Corridor 63,779,391 3,162,428 5.0% 62,107 0.1% 3,224,535 5.1% 259,871 76 235,800 57,388 90,000 HOUSTON INDUSTRIAL MARKET STATISTICAL SUMMARY Q2 2014

- 4. RESEARCH & FORECAST REPORT | Q2 2014 | HOUSTON INDUSTRIAL MARKET COLLIERS INTERNATIONAL | P.4 Q2 2014 Industrial Under Construction – 60,000 SF or greater Q2 2014 Industrial Deliveries – 60,000 SF or greater SUBMARKET BUILDING ADDRESS RBA % LEASED DEVELOPER ESTIMATED DELIVERY DATE Hwy 290/Tomball Pky Ind 11810 N Gessner Rd 441,000 0.0% Panattoni Oct-14 Hwy 290/Tomball Pky Ind 8303 Fallbrook Dr 400,250 0.0% Liberty Property Trust Jul-14 Hwy 290/Tomball Pky Ind Gessner Road & Beltway 8 362,180 0.0% DCT Industrial Trust Nov-14 Northwest Hwy 6 Ind 20710 Hempstead Rd 357,887 0.0% Duke Realty Corporation Sep-14 North Fwy/Tomball Pky Ind 4800 W Greens Rd 350,820 0.0% Davis Commercial Development Oct-14 North Fwy/Tomball Pky Ind 660 Greens Pky 350,000 100.0% Holder Construction Mar-15 North Fwy/Tomball Pky Ind 300 Airtex Dr 225,360 0.0% Pontikes Development Dec-14 South Hwy 35 Ind 9254 Park South Vw 193,741 0.0% Transwestern Aug-14 Hwy 290/Tomball Pky Ind 11720 N Gessner Rd 155,400 0.0% Panattoni Dec-14 North Hardy Toll Road Ind 400 Century Plaza Dr 149,760 0.0% Avera Companies Aug-14 North Hardy Toll Road Ind 2020 Greens Rd 147,112 0.0% IDV Investment & Development VenutresDec-14 North Hardy Toll Road Ind 14820 North Fwy 126,568 0.0% DCT Industrial Trust Nov-14 North Outer Loop Ind JKF/Kennedy Greens Blvd 120,000 100.0% Clay Development Construction Aug-14 Hwy 290/Tomball Pky Ind 8780 West Rd 100,275 100.0% EastGroup Properties Sep-14 South Hwy 35 Ind 9258 Park South Vw 90,067 100.0% Transwestern Jul-14 Hwy 59/Hwy 90 (Alt) Ind 10401 S Sam Houston Pky W 90,000 0.0% ICO Commercial Sep-14 West Outer Loop Ind 5737 Brittmoore Rd 86,250 0.0% Taten Real Estate Parters Dec-14 Northwest Outliers Ind 22240 Merchants Way 64,313 0.0% EastGroup Properties Jul-14 Hwy 290/Tomball Pky Ind 8790 West Rd 63,000 0.0% EastGroup Properties Sep-14 SUBMARKET BUILDING ADDRESS RBA % LEASED DEVELOPER DELIVERED North Fwy/Tomball Pky 10565 Greens Crossing Blvd 600,750 82.9% Hines Jun-14 North Hardy Toll Road 8039 Humble Westfield Rd 250,200 0.0% K2 Logistics Jun-14 North Outer Loop 121 Esplanade 224,550 0.0% IDI Jun-14 South Hwy 35 11951 Spectrum Blvd 150,000 100.0% Unknown Jun-14 South Hwy 35 7232 Airport Blvd 137,297 100.0% Unknown Dec-13 Hwy 59/Hwy 90(Alt) 13615 S Gessner Rd 123,300 0.0% Stream Realty Partners Apr-14 West Outer Loop 5737 Brittmoore Rd 122,500 100.0% Taten Real Estate Partners Jun-14 North Fwy/Tomball Pky 433 Plaza Verde Dr 120,159 0.0% Hines May-14 North Fwy/Tomball Pky 545 Plaza Verde Dr 120,159 0.0% Hines May-14 North Outer Loop 71 Esplanade 106,700 0.0% IDI Jun-14 North Hardy Toll Road 15892 Diplomatic Plaza Dr 94,074 0.0% EastGroup Properties Jun-14 Hwy 59/Hwy 90(Alt) 13721 S Gessner Rd 85,500 44.5% Stream Realty Partners Apr-14 Northwest Outliers 22110 Merchants Way 67,743 54.1% InSite Realty Partners Apr-14

- 5. RESEARCH & FORECAST REPORT | Q2 2014 | HOUSTON INDUSTRIAL MARKET Accelerating success. COLLIERS INTERNATIONAL 1233 W. Loop South Suite 900 Houston, Texas 77027 Main +1 713 222 2111 LISA R. BRIDGES Director of Market Research | Houston Direct +1 713 830 2125 Fax +1 713 830 2118 lisa.bridges@colliers.com The Colliers Advantage Enterprising Culture Colliers International is a leader in global real estate services, defined by our spirit of enterprise. Through a culture of service excellence and a shared sense of initiative, we integrate the resources of real estate specialists worldwide to accelerate the success of our partners. When you choose to work with Colliers, you choose to work with the best. In addition to being highly skilled experts in their field, our people are passionate about what they do. And they know we are invested in their success just as much as we are in our clients’ success. This is evident throughout our platform—from Colliers University, our proprietary education and professional development platform, to our client engagement strategy that encourages cross-functional service integration, to our culture of caring. We connect through a shared set of values that shape a collaborative environment throughout our organization that is unsurpassed in the industry. That’s why we attract top recruits and have one of the highest retention rates in the industry. Colliers International has also been recognized as one of the “best places to work” by top business organizations in many of our markets across the globe. Colliers International offers a comprehensive portfolio of real estate services to occupiers, owners and investors on a local, regional, national and international basis. *Information herein has been obtained from sources deemed reliable, however its accuracy cannot be guaranteed. COLLIERS INTERNATIONAL | P. 5