Recommandé

Contenu connexe

En vedette

En vedette (10)

Plus de copppldsecretariat

Plus de copppldsecretariat (20)

M-PESA, Mobile-phone based Money Transfer Service

- 2. TABLE OF CONTENTS 1.0 BACKGROUND.....................................................................................................................3 2.0 The Innovation....................................................................................................................4 3.0 Benefits of the M-‐pesa Money Transfer System ................................................................6 3.1 Financial Inclusion .......................................................................................................6 3.2 Enhanced Economic Activity........................................................................................6 3.3 Reduced Cash in the Economy and Increased Transparency ......................................7 3.4 Security........................................................................................................................7 3.5 Convenience ................................................................................................................7 4.0 How M-‐PESA Services Works for pastoralistS at Keekonyokie livestock market ..............8 5.0 Challenges...........................................................................................................................8 6.0 References ..........................................................................................................................9

- 3. 1.0 BACKGROUND The Maasai pastoralist’s livelihoods revolve around their livestock and this is reflected in aspects of their rich tradition, which have been passed down for generations. One of the main problems related to pastoralists’ livestock markets in Kenya has been how to get payments through to the thousands of livestock producers who live in remote and distant areas, many of whom are women. Carrying cash from markets back to the rangelands is risky for traders. Since 2007, Kenya has been leading the way with an innovative mobile phone technology that has transformed the lives of millions of people and businesses. M-‐Pesa allows herdsmen not to carry cash around; also, people without a bank account can transfer funds as quickly and easily as sending a text message. Mobile technology has proven to be very beneficial for Maasai livestock enterprises and traders. Leveraging mobile devices has helped the Maasai people to cope with one of Kenya’s worst droughts in history; a drought that threatened their ability to graze and water their cattle. Through mobile devices and shared information, herders can find out where to bring their cattle for grazing instead of roaming in search of water and pasture. The M-‐Pesa service has helped the Maasai (who often live miles away from banks and are usually on lone grazing or livestock marketing trips with their cattle) to transfer money back home or sell their livestock easily. Finally, the service provided cash transfer security on transit from and to the rangelands, a vital element in livestock trading. One of the clearest demonstrations of the transformative power of the M-‐Pesa service is the availability of mobile network coverage in pastoralist communities. Almost 80% of herders and livestock traders have purchased mobile phones and use them as tools for trade. They communicate with their contacts at livestock markets while still being in the rangelands, and bring their cattle to those markets that offer the best prices. Prices became more uniform and predictable, which led pastoralists to increase their profits. Unsold livestock (which ranged between 5 to 10 % per day) decreased when buyers and sellers started communicating more effectively. This, in turn, results in reduced transaction costs for livestock trading. In short, M-‐Pesa provided access to formal financial services for livestock markets in Kenya and significantly improved the ability of the market’s actors to better manage their businesses.

- 4. 2.0 THE INNOVATION 2.1 What is M-‐PESA? M-‐Pesa is an innovative mobile payment solution that enables customers to complete simple financial transactions including person-‐to-‐person money transfers. M-‐Pesa is available to all Safaricom telephone subscribers in Kenya. M-‐Pesa allows making transactions in a simple, secure, fast and effective way by using SMS technology. This has many benefits for customers in terms of convenience, security and because it is user-‐friendly. In addition, pricing is competitive compared to other formal money transfer services. M-‐Pesa enables users to: • Transfer money from person to person • Transfer money from individuals to businesses • Withdraw cash at designated outlets • Receive loan receipts or repayments • Buy Safaricom airtime • Pay bills 2.2 How does M-‐PESA work? Safaricom subscribers register for the Mesa service by filling in a simple form and providing identification proof. Once registered, Safaricom replaces their SIM card with an M-‐Pesa enabled one (if they want to, all new mobile subscribers now get the M-‐Pesa enabled SIM). To charge the money in the telephone the user needs to visit the nearest agent and deposit cash in exchange for “e-‐Float”. This e-‐Float is like currency that can be used to make payments or transfers to any other person or merchant via an encrypted SMS. The receiver of the virtual currency can either use it for further transactions or cash it from M-‐Pesa designated outlets. The chart below illustrates how an M-‐Pesa transaction is carried out.

- 5. Chart 1: The M-‐Pesa system Source: Agritrade To load money into an M-‐Pesa account, the user makes a cash deposit with an Mpesa agent. The electronic money is then transferred to the user’s account, and the deposit is confirmed by an SMS received by both the agent and the customer, who can then conveniently transfer money to other mobile phone users by SMS transactions. To withdraw cash from an M-‐Pesa account, users and unregistered customers make an electronic transfer to the M-‐Pesa agent, who will exchange this for cash. The withdrawal fees for unregistered customers are usually higher. To send or put money into an M-‐Pesa account, the user tells the agent the amount he/she wishes to deposit, and gives it to the agent. The agent then sends the e-‐money by phone in exchange for the deposited amount. The operation is completed when the user receives an SMS from Safaricom confirming the transaction.

- 6. 2.2 Lessons Learned 1) M-‐Pesa, by providing access to formal financial services to livestock markets in Kenya, has significantly improved the ability of the market’s actors to better manage their trading business. 2) Network operators understand the market needs. This has brought the necessary discipline and compliance aspects that the managing of money transfers entails, and a combination of key skills have been put together to improve access to financial services -‐especially for the un-‐banked pastoralists. 3.0 BENEFITS OF THE M-‐PESA MONEY TRANSFER SYSTEM 3.1 Financial Inclusion Developing countries are severely constrained by road infrastructure, which makes financial institutions difficult to access from remote areas. This implies that a large part of the population ends up being excluded from the formal banking system. M-‐Pesa, with its over fifteen thousand agents, is much more accessible for an ordinary Kenyan. M-‐Pesa helped Micro Finance Institutions (MFIs) to effectively access distant areas without substantial increases in costs. Financial inclusion has a multiplier impact on the lives of people drawn into the formal financial system, as it leads to social inclusion. Poor people with access to financial services see an improvement in their cash flow management and enhance their financial planning, which in turn increases their saving capacity. M-‐Pesa has brought many unbanked customers into the formal financial system. Finally, it is important to say that M-‐Pesa user households are two times more likely to have a bank account than non-‐user households. 3.2 Enhanced Economic Activity People’s access to cash is more limited on the supply-‐side than on the demand-‐side. More than the shortage of funds, the blockage happens when there is no ability to move money from the sender to the receiver. Since the creation of money, the ability to send the cash from A to B—the so-‐called “velocity of money”— has been a fundamental cornerstone of economic activity. The issue at stake is knowing exactly how a money transfer can happen in an emerging market where the infrastructure is poorly developed and where very few people have or even want to have a bank account. The Mobile Money Transfer platform is

- 7. key in substituting the banking infrastructure as in most of the emerging markets the mobile phone penetration is deeper than the bank account penetration. In fact, the ratio is 3 to 1: for every three mobile phone owners there is one bank account holder. M-‐Pesa has been instrumental in generating growth and development in Kenya. This system has brought higher remittances and increased economic activity, leading to faster growth. In a survey conducted by the Consultative Group to Assist the Poor (CGAP) it was found that the incomes of rural recipients increased by 5 -‐ 30% since they started using M-‐Pesa. 3.3 Reduced Cash in the Economy and Increased Transparency In the absence of a formal banking system, most transactions are cash based and therefore no audit trail is available for regulators. M-‐Pesa brought transparency in the money transactions by reducing the cash economy and digitising financial operations. M-‐Pesa is equivalent to a credit or debit card, which allows regulators to monitor the trail. There is more visibility on the money flows as the remittances move from informal channels to formal channels. 3.4 Security M-‐Pesa provides mobile phone customers with a secure platform that uses simple, tailored menus in their devices and sends fully encrypted PIN locked messages to a thoroughly audited financial accounting system. M-‐Pesa not only increased the micro finance activity but is also used as a way of keeping money. Informal saving channels are much less secure than formal saving facilities. Being user friendly and accessible, both the banked and unbanked M-‐PESA customers are using it to store their cash. M-‐Pesa agents are higher in number than bank agents and this allow customers not to travel long distances to withdraw money. With M-‐Pesa, there is no need to carry cash and hence there is no risk of the cash getting lost or stolen. 3.5 Convenience Many people in emerging economies have to travel far from home to find work and need to be able to send money back to their families. In most parts of the world the cost of money remittance is very high -‐ranging from 3% to 10%. According to the IMF, “M-‐Pesa now processes more transactions domestically within Kenya than Western Union does globally, and provides mobile banking facilities to more than 70 per cent of the country’s adult population.”

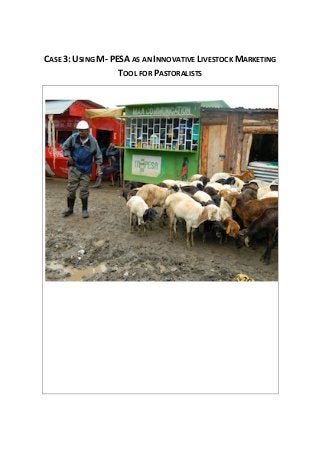

- 8. (http://thenextweb.com/africa/2011/10/24/local-‐transactions-‐by-‐kenyas-‐mobile-‐money-‐ service-‐m-‐pesa-‐exceeds-‐western-‐unions-‐global-‐transactions/). Based on that, more people depend on informal channels (through friends and family) to send money or physically deliver it. Traditionally this means high fees, risky unregulated services, or long expensive trips carrying cash in an unsafe and unpredictable environment. It has been observed that M-‐Pesa users need to make fewer trips back home to deliver money and the transaction size also comes down as transfers become more frequent. Moreover, unlike banks, the M-‐Pesa service is accessible 24 hours a day seven days a week and there are no limits for sending money. 4.0 HOW M-‐PESA SERVICES WORKS FOR PASTORALISTS AT KEEKONYOKIE LIVESTOCK MARKET The Maasai pastoralists and livestock traders at Keekonyokie livestock market use M-‐Pesa services for the following: • To purchase meat (butchers send money to meat traders to deliver supplies); • To purchase livestock from distant livestock producers; • To send money to their families, who live miles away from markets, so that they can take care of basic needs; • To buy from distant producers, thus reducing transaction costs in livestock trading and shortening transaction time; • To book hotel accommodation when travelling to distant markets to buy livestock; • To buy phone credit while in remote rangelands without agent services. “All a Maasai pastoralist needs is a mobile phone and the ability to remember his telephone number” “I don’t need to go to the bank when I have the bank in my phone” – Ole Masyi, livestock trader. 5.0 CHALLENGES A research carried out by a doctoral candidate at the University of Edinburgh1, notes however some barriers in the adoption of the M-‐Pesa service. According to it, both agents and customers complain of cash flow problems, especially in the rural areas. Because the 1 Source: http://technology.cgap.org/2008/06/17/why-has-m-pesa-become-so-popular-in-kenya/

- 9. majority of transactions in the village are withdrawals, agents must maintain their cash flow. They do this by making frequent trips to the bank. This can be problematic if the agent is not close to an urban centre, where most banks in Kenya are located. Such situation is frequent despite great efforts made by Safaricom regarding the store liquidity management. Finally, other important challenge arises when noticing that the service availability is not uniform across the country; in fact, accessing the service depends on the network coverage, which is stronger in the southwest of Kenya but not sufficient to serve the entire country. 6.0 REFERENCES http://www.safaricom.co.ke/index.php?id=745http://en.wikipedia.org/wiki/M-‐Pesa http://siteresources.worldbank.org/AFRICAEXT/Resources/258643-‐1271798012256/M-‐ PESA_Kenya.pdf http://thenextweb.com/africa/2011/10/24/local-‐transactions-‐by-‐kenyas-‐mobile-‐money-‐ service-‐m-‐pesa-‐exceeds-‐western-‐unions-‐global-‐transactions/ http://technology.cgap.org/2008/06/17/why-‐has-‐m-‐pesa-‐become-‐so-‐popular-‐in-‐kenya/