2012 Minnesota Internet Survey: The Digital Divide 2.0 and Beyond

•

1 j'aime•1,296 vues

Examining the current state of Internet access in Minnesota and how it redefines the digital divide.

Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (20)

En vedette

En vedette (20)

Similaire à 2012 Minnesota Internet Survey: The Digital Divide 2.0 and Beyond

Similaire à 2012 Minnesota Internet Survey: The Digital Divide 2.0 and Beyond (20)

Plus de Center for Rural Policy & Development

Plus de Center for Rural Policy & Development (11)

Dernier

Dernier (20)

2012 Minnesota Internet Survey: The Digital Divide 2.0 and Beyond

- 1. 2012 Minnesota Internet Survey Digital Divide 2.0 and beyond After more than ten years of asking rural Minnesotans about their access to high-speed Internet service, it is possible to draw a few conclusions: 1. It is fairly well accepted now that broadband access has become a ne- cessity for functioning at full capacity in today’s world. In other words, Internet access and broadband access are no longer considered a luxury 2. The digital divide isn’t what it used to be. The divide can be character- but rather a necessity by most people. ized as the haves and have-nots, those who have broadband and those who do not. In the early days of broadband, the main barrier to being a “have” was availability of the service itself. Now that infrastructure is nearly ubiquitous, at least in Minnesota, the other barriers, which have always been there, are becoming more apparent, particularly in the area 3. Broadband no longer ties the user to a fixed location (i.e., the home). of bandwidth. In just the past few years, technology has been introduced that makes it possible for people to access the Internet from just about anywhere. This trend is important not only to people who use the Internet and do busi- 4. The preceding points tie into what appears to be a generational change ness on it, but to those who provide access and create policy affecting it. in how people access, use, and think of the Internet. This study was completed with support from the W.K. Kellogg Foundation, the Minnesota Telecom Alliance, Networks United for Rural Voice, the Blandin Foundation, and the McKnight Foundation. Thanks also to the City of Minneapolis for their collaboration. A PDF of this report can be downloaded from the Center’s web site at www.ruralmn.org. The Center for Rural Policy and Development, based in St. Peter, Minn., is a private, not-for-profit © 2012 Center for Rural Policy policy research organization dedicated to benefiting Minnesota by providing its policy makers with and Development an unbiased evaluation of issues from a rural perspective.

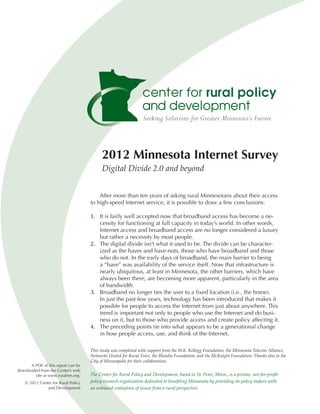

- 2. 100% Rural Computer 80% Internet Broadband Figure 1: Adoption 60% Twin Cities rates of computers, Computer Internet service, and Internet 40% broadband in the Twin Broadband Cities metro area and the rest of Minnesota 20% since 2001. 0% 2001 2002 2003 2004 2005 2006 2007 2009* 2010 2011* 2012 -2008 History of the study is similar to that of the Twin the 2012 Minnesota Internet The Center included ques- Cities. Survey. A total of 1,652 adults tions on broadband adoption in • The use of social media, in Minnesota were interviewed. its first rural Minnesota survey in voice over Internet Protocol A combination of landline and 2001. The next year, the survey (VOIP, online phone calls), cellular random digit dial (RDD) focused solely on broadband and and streaming video are up samples was used to represent the Internet. In 2005, the seven- dramatically in the last two adults in the target areas who county Twin Cities metropolitan years. have access to either a landline area was included for the first • While the home computer or cellular telephone. The margin time to provide a comparison is still by far the most com- of error for the statewide sample to rural counties. And in 2012, mon means of accessing the was ±2.53% at a 95% confidence interviewers called cell phone Internet for Minnesota house- level. The margin of error for both numbers for the first time, rec- holds, the number of people the Twin Cities sample and the ognizing the number of house- accessing the Internet outside rest of Minnesota sample was holds that have given up landline their homes continues to ±3.58%. The complete methodol- phones and now use cell phones grow, as does the number and ogy report can be found at www. as their only phone. variety of devices they are us- ruralmn.org. ing to access it. Major findings • There are a number of rea- Adoption rates • Adoption rates for computers, sons people do not purchase The survey results show that Internet access, and broad- broadband for their homes, the adoption rates for computers, band continue to go up but at but the primary ones are lack the Internet, and broadband were a slower rate in both the rural of interest and cost. up in 2012 compared to 2010, counties and the Twin Cities. although the increase was not as The Twin Cities is still several Methodology great as in past years. The state- percentage points ahead of As in past studies, the state wide rate of broadband adoption the rest of the state in terms of was divided into two regions, the went from 69.5% of households adoption: 79.2% for the Twin seven-county Twin Cities metro- to 75.4% of households. In Cities vs. 70.6% for rural politan area, or “Metro,” and the 2012, 70.6% of rural households Minnesota. remaining 80 counties making up reported purchasing broadband • Over one quarter of Minneso- the rest of Minnesota, or “Rural.” service, compared to 79.2% of ta households (27%) use cell The Social Science Research In- Twin Cities households. Figure 1 phones only, no landlines. stitute at the University of North shows how computer, Internet, The rate for rural Minnesota Dakota, Grand Forks, conducted and broadband adoption rates 2 2012 Minnesota Internet Survey

- 3. 100% 80% 60% Figure 2: Broadband adoption rates by age group for the Twin Cities metro 40% area counties and the rest of Minnesota. 20% 0% 18-24 25-34 35-44 45-54 55-64 65+ Rural Metro 100% have changed since 2001. 80% Part of the reason for a slower rate of increase may be the 60% recent recession. A 2010 Pew Internet and American Life study 40% indicated that adoption rates fell nationwide during the recession.1 20% However, it is also likely that these technologies are reaching 0% their natural saturation point. < $25,000 $25,000 –$39,000 $40,000 –$49,000 $50,000 –$74,000 $75,000 $100,000 $150,000 + –$99,000 –$150,000 The broadband adoption rate in Rural Metro Figure 1 shows a typical S-curve associated with technology adop- Figure 3: Broadband adoption by income group for the Twin Cities and rural Minnesota. tion: adoption starts slowly with the early adopters, gains momen- tum as the bulk of the population < $25,000 catches on, then slows down as the last late adopters come on $25,000 to $39,000 board and adoption nears its maximum. $40,000 to $49,000 The impact of age, income, $50,000 to $74,000 education $75,000 to $99,000 Age. In looking at who has or has not adopted broadband at $100,000 + home, age, income, and educa- 0% 20% 40% 60% 80% 100% tion are still major predictors. 2003 2012 Figure 2 shows the breakdown of broadband adoption in the home Figure 4: Broadband adoption rates by household income for rural by age group (out of all house- Minnesota in 2003 and 2012. holds). As it has been for the last decade, the adoption rate among seniors (age 65 and over) is still the lowest, but it continues to 2012 Minnesota Internet Survey 3

- 4. Less than High School HS or equivalent Figure 5: Broadband Some College adoption by level of 2-year College education attained, in the Twin Cities and rural 4-year College Minnesota. Master’s Degree Doctoral Degree Professional Degree (JD, MD) 0% 20% 40% 60% 80% 100% Rural Metro grow each year. In 2003, the first phones and other mobile devices This drop in the Twin Cities, year we reported specifically or borrowing a wireless connec- therefore, could be a reflection of on seniors, 5.6% of rural senior tion at a public hotspot. the recession. On the other hand, households had broadband. Income. Income has also considering the younger median In 2012, 48.5% of rural senior been a long-time predictor of age of the Twin Cities population, households had broadband, Internet and broadband adoption. it could also be a reflection of the while 53.7% of Twin Cities senior Figure 3 shows how broadband rise in the use of smart phones households did. adoption is affected by income, and other portable devices, as Interestingly, we see that the while Figure 4 shows how the discussed earlier. adoption rate for the youngest pattern has stayed consistent Education. Breaking out the age group is also low, particularly between 2003 and 2012. data by education levels shows a in rural Minnesota (68% com- While home broadband pattern similar to that of income, pared to 81% in the Twin Cities). adoption has risen in the lowest where the higher the level of edu- This low figure does not necessar- income group (less than $25,000) cation attained, the more likely a ily mean that people in this age over the last two years in rural household is to have a computer, group are not on the Internet or Minnesota households, going Internet, and broadband technol- not adopting broadband. It only from 25% in 2010 to 35% in ogy (Figure 5). The differences indicates a lower percentage of 2012, it appears to have dropped between rural and metro adop- households in this age group with for metro households, from 40% tion rates within each group are broadband in their homes. A clue to 32%. One reason may be the not large. comes from another 2010 study recession. As mentioned earlier, The impact of children in by the Pew Internet and Ameri- a Pew Research study found that the house. The findings show can Life Project that found that nationally, broadband adoption that households with school-age nationwide, 84% of young adults slowed dramatically in 2010.3 children are more likely to have age 18-29 go online using their cell phones or a laptop; in other Table 1: Impact of school-age children in the household on adoption rates. words, a portable device that can be taken out of the home.2 The Rural Metro low number of 18- to 24-year- Kids No kids Kids No kids olds in rural Minnesota with a Do you have a computer? 89.7% 74.0% 96.4% 81.6% broadband connection at home Do you have an Internet may indicate that this group is connection? 88.7% 69.1% 93.9% 77.5% bypassing a fixed home connec- Do you have broadband? 85.7% 64.9% 90.9% 73.1% tion altogether and are simply us- How important is being able to ac- ing the cell service on their smart cess broadband? (Very important) 58.5% 37.9% 65.2% 51.2% 4 2012 Minnesota Internet Survey

- 5. computers and broadband as Table 2: Percentage of home Internet users engaging in selected activities well (Table 1). Age of the primary in the last six months. decision makers in the household Rural Metro is presumably a major factor Send and receive email 96.2% 98.6% here. Notice the difference in the Check the weather 88.7% 89.3% perceived importance of broad- Access news web sites 79.9% 82.6% band between those with and Research a purchase you’re planning 79.6% 86.3% those without children, especially for rural Minnesota. Purchase something at an online store or auction 77.6% 84.0% Do banking, pay bills or other financial business Things we do online online 77.2% 85.4% The Minnesota Internet Study Stay informed on community news and events 69.6% 69.6% also tracks activities that home Share photos 69.3% 79.8% Internet users engage in. Table 2 Research medical information 63.9% 70.1% shows the percentage of rural and Download music or video files 55.0% 73.0% Twin Cities home Internet users Watch movies or TV shows 45.7% 70.5% engaging in these activities. Email Search for employment 42.9% 52.1% is still virtually universal. Social Do homework 39.9% 45.0% media, which has been available Place a phone call over the Internet 37.4% 44.4% to the public for only about five years, is already at 75% for rural Do work for employer at home 33.4% 43.8% Minnesota and over 80% for the Communicate with your child’s school 33.0% 39.7% Twin Cities. Sell goods or services online or advertise 27.4% 24.3% While the gap in participation Interact with the government or a government rates between rural Minnesota official 21.0% 24.4% and Twin Cities consumers has Take a high school or college class online 15.8% 21.5% closed for most activities, there Check agricultural commodity prices 13.8% 7.4% are still a handful of activities that Communicate with doctor or nurse or other home Internet users engage in caregiver 12.7% 23.4% more frequently in the Twin Cit- ies compared to rural Minnesota (Table 3). In the past two years, some activities have seen a large Table 3: Difference by percentage points in engagement, rural Minnesota Internet users compared to Twin Cities Metro Internet users. increase in popularity. Table 4 shows a list of activities that saw Rural Metro Difference some of the largest growth in Watch movies or TV shows 45.7% 70.5% 24.8 use between 2010 and 2012 in Download music or video files 55.0% 73.0% 18.0 percentage points. The growth in Communicate with doctor or these activities may reflect simply 12.7% 23.4% 10.7 nurse or other caregiver the increase in their availability Share photos 69.3% 79.8% 10.5 as new services such as stream- Do work for employer at home 33.4% 43.8% 10.4 ing video are introduced and in an increase in the availability of higher broadband speeds, mak- ing it possible to engage in these activities. 2012 Minnesota Internet Survey 5

- 6. Table 4: Activities with the largest increases in participation, by percentage point. Rural Metro 2012 2010 Change 2012 2010 Change Social media 75.1% 70.6% 4.5 81.8% 68.9% 12.9 Stay informed on community news and 69.6% 36.4% 33.2 69.6% 53.1% 16.5 events Watch movies or TV shows 45.7% 32.1% 13.6 70.5% 48.0% 22.5 Place a phone call over the Internet 37.4% 9.7% 27.7 44.4% 20.4% 24.0 Play games online with other gamers 36.2% 22.0% 14.2 40.1% 28.7% 11.4 Sell goods or services online or 27.4% 14.3% 13.1 24.3% 18.0% 6.3 advertise Communicate with doctor or nurse or 12.7% 9.2% 3.5 23.4% 13.2% 10.2 other caregiver How much time we spend if there was anything they wanted reported the same. online to do online that they couldn’t A comparison of how much When asked how many with their current speed, the households pay for their total hours per day someone in their majority of replies involved being communications bill shows that household is on the Internet, the able to do things faster and re- Twin Citians tend to pay more average response for rural Min- ferred to activities such as stream- (Figure 6). nesota was 4.2 hours, while the ing and downloading video and average for the Twin Cities was music. Going mobile and getting away 4.6 hours. As a sign of how things from the home computer have changed, this question used Cost The introduction of smart to ask how many hours per week Rural and Metro households phones, tablet computers, and someone in your household was reported paying about the same lightweight laptops, along with online. amount for their Internet service the advent of wireless Internet each month, $47.57 on average access (wi-fi) and Internet via Speed and satisfaction for rural households compared a cell connection, has made Although it is beyond the to $45.82 for Twin Cities house- it possible for Internet users to scope of this study to get a com- holds. However, 16% of rural migrate out of their homes. The plete picture of what broadband respondents said they did not Pew Research study on mobile speed is offered where, we can know how much they paid, while access reported that as of May get a more general idea of wheth- 24% of Twin Cities households 2010, 59% of all adult Americans er the available speed (or the one the consumer chose) is doing 30% the job by asking respondents if 25% they are satisfied with the speed 20% of their Internet service. Overall, Figure 6: the majority of home Internet Estimated monthly 15% users said they were satisfied, communications bill. 10% although Twin Cities customers were more satisfied than rural 5% ones: 78% of rural home Internet 0% users compared to 86% of Twin < $50 $50– $100– $150– $200– $250+ $99 $149 $199 $249 Cities home Internet users. When asked in an open-ended question Rural Metro 6 2012 Minnesota Internet Survey

- 7. 100% from home, they must find places 80% to access the Internet. We asked everyone, regardless of whether 60% they have Internet access at 40% home, where they go to access Figure 7: Devices used 20% to connect to the Internet the Internet outside their homes. from home, among One-fifth of rural households 0% Home Tablet Cell Game Other households with Internet. (20%) and nearly one-quarter of computer phone device Twin Cities households (23%) Rural Metro reported that they had accessed the Internet at their public library in the past six months. We also asked everyone: Be- sides home, the library, or work, Table 5: Preferred device used to connect to the Internet at home, among households with Internet. are there any other places they go on a regular basis to access the Rural Metro Internet? For rural Minnesotans, Home computer 73.8% 69.9% 38% responded yes, they do go Cell phone 9.6% 11.0% someplace outside the home reg- Tablet computer 12.3% 11.0% ularly; 43% of Twin Cities house- holds responded yes as well. Gaming device 2.9% 5.3% Coffee shops were by far the most Other 1.4% 2.8% popular. Of those responding that Other devices included laptops, iPods, video streaming devices. they access the Internet outside of home or work, 30% of rural households and 40% of Twin Cit- were going online wirelessly, us- becoming apparent in the last ies households reported visiting ing either a laptop or cell phone.4 few years is a trend toward in- a coffee shop for Internet access. A look at what devices Internet creased spending by households (This breaks down to 5% of all users in Minnesota use to con- on their cell phones. A recent rural households and 10% of all nect at home (Figure 7) shows analysis by the Wall Street Jour- Twin Cities households.) that while the computer is still nal of Bureau of Labor Statistics the most prevalent, other de- consumer spending data showed Importance of access at home vices are catching up, especially that between 2007 and 2011, Despite the new attention to among younger people. When Americans increased their an- mobility and being able to access asked if there were any other nual spending on cell phones by the Internet from anywhere, the devices they used to access the $116, while decreasing in other survey found that many respon- Internet at home besides those areas of discretionary spending, dents still believe it is very impor- given, respondents also men- such as eating out (-$48), apparel tant that they be able to access tioned laptops, iPods, e-readers, and other services (-$141), and broadband at home. and streaming video devices such purchasing vehicles (-$575).5,6 Figure 8 shows that 44% of as Roku. Respondents were also As more consumers move to cell rural households and 56% of asked which device they use the phone-based Internet service, Twin Cities households rated most in connecting to the Internet the trends in cell-based Internet having access to broadband at at home (Table 5). service pricing and limits on home as very important. When Expense has always been a monthly data service will bear broken down by age, however, factor in choosing to purchase monitoring. it is apparent that home broad- broadband service. One aspect When people want to use band access is less important to of mobile Internet access that is their wifi-enabled devices away the oldest and the youngest age 2012 Minnesota Internet Survey 7

- 8. 60% 80% 70% 50% 60% 40% 50% 30% 40% 30% 20% 20% 10% 10% 0% 0% Not Somewhat Neutral Somewhat Very Important 18-24 25-34 35-44 45-54 55-64 65+ important not important important Rural Metro Rural Metro Figure 8: Importance of having access to broadband at Figure 9: Percentage of respondents reporting that hav- home. ing broadband access at home is “very important,” by age group. groups in the survey (Figure 9). have to do with affordability, rel- answer in rural households was Of respondents age 18-25, only evance, and digital literacy: they “Too expensive,” while in Twin 46% of rural households and can’t afford it, they don’t see how Cities households “Too expen- 43% of Twin Cities households it would benefit them, or they sive” was nearly tied with “Has said having broadband at home believe they wouldn’t know how access to the Internet someplace was very important. The answer to use it.7 else.” “Not available where I live” is very likely found in the studies When Minnesotans were was at or near the bottom of the showing that a large percentage asked why they chose not to list. of young adults are accessing the adopt Internet service for their To make a direct comparison Internet using devices they can homes, similar reasons were between rural and Twin Cities take anywhere. This would imply given. Approximately 25% of ru- households, however, we need that a broadband connection in ral households and 17% of Twin to look at the data based on all the home is less of a requirement. Cities households said they did households. While the percent- not have Internet access at home. ages in Table 6 look small, it must Understanding the “have nots” When these households were be remembered that they repre- At the heart of the digital asked why, the most frequent sent thousands of households in divide is a concern with getting response in each group was that both regions. broadband access to the “have they didn’t need Internet ac- When responses were broken nots.” But now that the barrier cess. The second most common down by age, interesting pat- of basic infrastructure has been largely removed in Minnesota, Table 6: Reasons for not having Internet access at home, among all other barriers show up more households. clearly. A 2010 analysis of data Rural Metro collected by the Federal Commu- Doesn’t need Internet access 12.2% 7.0% nications Commission found that Has access to Internet someplace else 1.8% 2.7% the main indicators separating those who adopt broadband from Not available where they live 0.5% 1.0% those who do not are education, Too expensive 4.5% 2.5% income, and age. The same study Doesn’t know how to use the Internet 2.6% 1.5% found the main reasons people Concerned about the security of their information 1.6% 0.6% gave for not adopting broadband Other reason 2.3% 1.5% 8 2012 Minnesota Internet Survey

- 9. 100% 80% 65+ 50-64 60% 35-49 25-34 40% 18-24 20% ever, the response rate for “Do not need Internet” was more than 0% < $25,000 $25,000 $40,000 $50,000 $75,000 $100,000 $150,000+ double that in both groups (33% –$39,999 –$49,999 –$74,999 –$99,999 -$149,000 for rural, 26% for Twin Cities). Figure 10: Income groups broken out by age groups. Each income group is The clue again is in age. As 65+ dominated by certain age groups. Figure 10 shows, the oldest Min- 50-64 nesotans in the survey are more 35-49 likely to have the lowest incomes. 25-34 Seniors are less likely to have In- 18-24 ternet at home and are less like to terns appeared. “Doesn’t need reporting an annual income of consider having Internet at home Internet access” was still a fre- less than $25,000, 33% said they “very important.” At the same quent answer in most age groups. didn’t need Internet, and 16% time, one-third of households It was understandably highest said it was too expensive. Out of in this income group are under among older respondents. How- all Twin Cities households in the age 35. This is also the age group ever, “Has access to the Internet same income group, 26% said most likely to access the Internet someplace else” was a frequent they did not need Internet access, using a mobile device. They have answer among younger respon- while 9% said it was too expen- the technology available not to dents, especially in the Twin sive. Also, 5% of rural house- have to buy fixed-location broad- Cities. holds in this income group said band access, just as they have the In looking at all rural Min- they had access to the Internet technology that makes it possible nesota households, seniors (age elsewhere, while nearly 13% of not to have to buy a landline 65 and over) were the most likely Twin Cities households in this phone. Their thought process may to say they didn’t need Internet income group said the same. be, “So why spend the money?” access; a full 30% of rural senior For years we have known that households said so, while in the older persons and lower income Conclusions and areas for Twin Cities, the figure was 23%. persons are the least likely to further study The next closest age groups were adopt broadband and Internet For rural communities, the half these percentages. In rural technology. The analysis above term “digital divide” has referred Minnesota, households in the indicates why, and the answer for the most part to geography: 18-34 age range were the most appears to be largely due to a Access was determined largely likely to say home Internet access belief that they do not need it, by the presence of infrastructure, was too expensive (13.4%), while followed by a belief that it is too and most of that infrastructure in the Twin Cities, that same age expensive. It is understandable was concentrated in larger popu- group came in at 1.8%. The Twin for senior citizens, who have lation centers. The result was a Cities’ 55-64 age group was more survived most of their lives quite tendency for rural residents to be likely to say home Internet was well without Internet access, to behind in adopting broadband too expensive (6.9% of all house- say they do not need the Internet. technology. As a 2010 study by holds in that age group). But why low-income earners? Daily et al noted, over the last ten Income groups also reveal Logic would suggest that the years, broadband access has in- clues. Out of all rural households service is too expensive. How- creasingly become a requirement 2012 Minnesota Internet Survey 9

- 10. of socio-economic inclusion, as of seniors adopting Internet and ing what technologies they use opposed to just an outcome of it.8 broadband continues to grow and where they upgrade it, but In other words, broadband has each year. how businesses should spend crossed the threshold from being • Affordability: Interestingly, their technology and marketing a luxury to becoming a necessity among rural households, the dollars, where consumers decide to function in today’s world. youngest age groups (18-34) ex- to spend their time, and how The good news is that Minne- pressed the biggest problem with policymakers design regulations sota, including rural Minnesota, affordability among those who do that apply to access, distribution, is ahead of many states when it not have a home Internet connec- and use. comes to broadband access. The tion yet. On the other hand, the infrastructure to get online is an same age group of non-adopters • Speed. issue for fewer and fewer house- in the Twin Cities expressed virtu- The issue of bandwidth may holds every year. ally no issue with cost. be the most important of all. As we continue to track the • Access to alternatives: At While the percentage of house- development of broadband in the same time, nearly twice as holds with broadband continues Minnesota, though, we find that many Twin Cities non-adopters as to rise, what speed a household the trends have shifted now from rural ones said they could access gets is still very much a function the issue of access to the issues of the Internet someplace besides of where it is located in relation mobility and bandwidth. their homes. to key infrastructure. The demand There are three areas in par- for more speed will only increase ticular where we can draw some • The mobile Internet. as new bandwidth-eating tech- conclusions and that we believe The Internet and broadband nologies are introduced. The will require continuing attention: are going mobile via smart concern for many household- the remaining non-adopters, the phones, lightweight laptops, tab- ers right now is the ability to do new mobile Internet, and the im- let computers, and other hand- things faster, especially stream portance of increased bandwidth. held devices. With the spread of video and music smoothly. Speed these portable devices, how are has larger public implications, • The digital divide and the re- our expectations about access to however. Business demands maining non-adopters. the Internet changing? How does an ever-increasing bandwidth Today, the lack of broadband this mobility affect our expecta- capacity. Education and health infrastructure is a barrier to ac- tions regarding reliability and our care are moving more programs cess for fewer and fewer house- perceived need for speed? And and services online, and distance holds. But now that most of those how are people affected who live learning and remote health care who really want broadband can in areas with no good mobile are continuously put forward as get it, that leaves a group of peo- Internet options, including cell solutions to the problems rural ple who could be characterized access? Access outside the home areas have with distance and a as the more tenacious non-adopt- is significant in the same way sparse population. Universities ers, those who have a different that cell phone-only homes are and health care facilities are still set of barriers: Attitudes (“I don’t significant: the nature of the ser- experimenting with providing need Internet,” “I wouldn’t know vice is changing. Consumers do education and services online, how to use it”); affordability; and not necessarily need to purchase and therefore these activities access to alternatives. a broadband connection specifi- still go somewhat unnoticed by • Attitudes: The most com- cally for their home, and they in the general public. However, in mon reason expressed by non- fact may not need to purchase the years to come, if rural com- adopters was that they did not broadband at all. Fixed-location munities are not able to keep up see a need for Internet. This home broadband, like the land- capacity-wise, they will not be belief was most common among line phone, is becoming optional. able to take advantage of these seniors, and especially rural These factors not only affect the new technologies, creating the seniors. However, the percentage decisions providers make regard- distinct possibility that they will 10 2012 Minnesota Internet Survey

- 11. fall further behind, with seri- Endnotes 8 Daily, D., Bryne, A., Powell, A., ous implications for income and 1 Smith, A. (2010, August). Home Karaganis, J., & Chung, J. (2010). population. Broadband 2010. http://www.pewin- Broadband adoption in low-income ternet.org/Reports/2010/Home- communities. Retrieved Sept. 25, Broadband-2010.aspx 2012, from http://webarchive.ssrc. As the findings from the org/pdfs/Broadband_Adoption_ survey showed, these barriers are 2 Smith, A. (2010, July). Mobile v1.1.pdf more common in rural areas and Access 2010. http://www.pewin- are another example of why deci- ternet.org/Reports/2010/Mobile- sion makers working on these is- Access-2010.aspx sues may take into consideration 3 Smith, A. (2010, August). whether the solution will work in 4 Smith, A. (2010, July). the same way or as effectively for rural areas as for urban areas. 5 Troianovski, A. (2012). Cell phones are eating the family budget [Elec- Internet service providers are tronic version]. Wall Street Journal. well aware of these trends in the http://online.wsj.com/article/SB1000 demand for mobility and band- 0872396390444083304578018731 width. And since the younger 890309450.html demographic groups are the ones 6 U.S. Department of Labor, Bureau most focused on going mobile of Labor Statistics, Consumer Expen- and doing more things on the ditures. (2012). Consumer Expendi- Internet, these are trends that are ture Survey. http://www.bls.gov/cex/ not going away. Policymakers csxstnd.htm and other decision makers should 7 Horrigan, J.B. (2010). Broadband keep these trends in mind when it adoption and use in America. Re- comes time for creating policies trieved Sept. 25, 2012, from http:// aimed at providing or encourag- online.wsj.com/public/resources/ ing Internet service. documents/FCCSurvey.pdf 2012 Minnesota Internet Survey 11

- 12. www.ruralmn.org Twitter @ruralpolicymn www.facebook.com/ruralmn 2012 Minnesota Internet Survey