1) Reen Lawns, Inc., performs adjusting entries every month, but c.docx

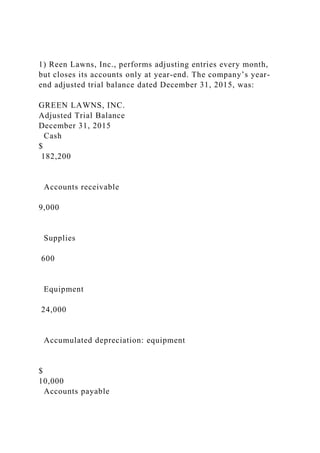

1) Reen Lawns, Inc., performs adjusting entries every month, but closes its accounts only at year-end. The company’s year-end adjusted trial balance dated December 31, 2015, was: GREEN LAWNS, INC. Adjusted Trial Balance December 31, 2015 Cash $ 182,200 Accounts receivable 9,000 Supplies 600 Equipment 24,000 Accumulated depreciation: equipment $ 10,000 Accounts payable 3,000 Income taxes payable 7,000 Capital stock 50,000 Retained earnings 90,000 Dividends 4,000 Lawn care revenue earned 192,000 Salary expense 104,000 Supply expense 2,400 Advertising expense 600 Depreciation expense: equipment 2,000 Income taxes expense 23,600 $ 352,000 $ 352,000 a-1. Prepare an income statement for the year ended December 31, 2015. a-2. Prepare a statement of retained earnings for the year ended December 31, 2015. a-3. Prepare the company's balance sheet dated December 31, 2015. (Amounts to be deducted should be indicated by a minus sign.) b. Does the company appear to be liquid? No Yes c. Has the company been profitable in the past? No Yes 2) Reen Lawns, Inc., performs adjusting entries every month, but closes its accounts only at year-end. The company’s year-end adjusted trial balance dated December 31, 2015, was: GREEN LAWNS, INC. Adjusted Trial Balance December 31, 2015 Cash $ 182,200 Accounts receivable 9,000 Supplies 600 Equipment 24,000 Accumulated depreciation: equipment $ 10,000 Accounts payable 3,000 Income taxes payable 7,000 Capital stock 50,000 Retained earnings 90,000 Dividends 4,000 Lawn care revenue earned 192,000 Salary expense 104,000 Supply expense 2,400 Advertising expense 600 Depreciation expense: equipment 2,000 Income taxes expense 23,200 $ 352,000 $ 352,000 a. Prepare all necessary closing entries at December 31, 2015. 1. Record the entry to close Lawn Care Revenue earned to income summary 2. REcord the entry to close all expense accounts to income summary 3. Record the entry to transfer net income earned in 2015 to retained earnings account 4. Record the entry to close dividends declared in 2015 to retained earnings account. Prepare an after-closing trial balance dated December 31, 2015. · Record the entry to close all expense accounts to income summary. · Record the entry to close all expense accounts to income summary. 3) Cat Fancy, Inc., has provided the following information from its most current financial statements: Total revenue $ 125,000 Total expenses 80,000 Total current assets 32,000 Total current liabilities 8,000 Total stockholders' equity, January 1, 2015 74,000 Total stockholders' equity, December 31, 2015 76,000 Compute the company’s net income per ...

Recommandé

Recommandé

Contenu connexe

Similaire à 1) Reen Lawns, Inc., performs adjusting entries every month, but c.docx

Similaire à 1) Reen Lawns, Inc., performs adjusting entries every month, but c.docx (20)

Plus de dorishigh

Plus de dorishigh (20)

Dernier

Dernier (20)

1) Reen Lawns, Inc., performs adjusting entries every month, but c.docx

- 1. 1) Reen Lawns, Inc., performs adjusting entries every month, but closes its accounts only at year-end. The company’s year- end adjusted trial balance dated December 31, 2015, was: GREEN LAWNS, INC. Adjusted Trial Balance December 31, 2015 Cash $ 182,200 Accounts receivable 9,000 Supplies 600 Equipment 24,000 Accumulated depreciation: equipment $ 10,000 Accounts payable

- 2. 3,000 Income taxes payable 7,000 Capital stock 50,000 Retained earnings 90,000 Dividends 4,000 Lawn care revenue earned 192,000 Salary expense 104,000 Supply expense 2,400

- 3. Advertising expense 600 Depreciation expense: equipment 2,000 Income taxes expense 23,600 $ 352,000 $ 352,000

- 4. a-1. Prepare an income statement for the year ended December 31, 2015. a-2. Prepare a statement of retained earnings for the year ended December 31, 2015. a-3. Prepare the company's balance sheet dated December 31, 2015. (Amounts to be deducted should be indicated by a minus sign.) b. Does the company appear to be liquid? No Yes

- 5. c. Has the company been profitable in the past? No Yes 2) Reen Lawns, Inc., performs adjusting entries every month, but closes its accounts only at year-end. The company’s year- end adjusted trial balance dated December 31, 2015, was: GREEN LAWNS, INC. Adjusted Trial Balance December 31, 2015 Cash $ 182,200 Accounts receivable 9,000

- 6. Supplies 600 Equipment 24,000 Accumulated depreciation: equipment $ 10,000 Accounts payable 3,000 Income taxes payable 7,000 Capital stock 50,000 Retained earnings 90,000 Dividends

- 7. 4,000 Lawn care revenue earned 192,000 Salary expense 104,000 Supply expense 2,400 Advertising expense 600 Depreciation expense: equipment 2,000 Income taxes expense 23,200

- 8. $ 352,000 $ 352,000 a. Prepare all necessary closing entries at December 31, 2015. 1. Record the entry to close Lawn Care Revenue earned to income summary 2. REcord the entry to close all expense accounts to income summary 3. Record the entry to transfer net income earned in 2015 to retained earnings account 4. Record the entry to close dividends declared in 2015 to retained earnings account. Prepare an after-closing trial balance dated December 31, 2015. · Record the entry to close all expense accounts to income summary. · Record the entry to close all expense accounts to income summary.

- 9. 3) Cat Fancy, Inc., has provided the following information from its most current financial statements: Total revenue $ 125,000 Total expenses 80,000 Total current assets 32,000 Total current liabilities 8,000 Total stockholders' equity, January 1, 2015 74,000 Total stockholders' equity, December 31, 2015 76,000

- 10. Compute the company’s net income percentage in 2015 Compute the company’s return on equity in 2015 Compute the company’s current ratio at December 31, 2015. 4) Terrific Temps fills temporary employment positions for local businesses. Some businesses pay in advance for services; others are billed after services have been performed. Advanced payments are credited to an account entitled Unearned Fees. Adjusting entries are performed on a monthly basis. An unadjusted trial balance dated December 31, 2015, follows. (Bear in mind that adjusting entries have already been made for the first 11 months of 2015, but not for December.) TERRIFIC TEMPS UNADJUSTED TRIAL BALANCE DECEMBER 31, 2015 Cash $ 27,020 Accounts receivable 59,200

- 11. Unexpired insurance 900 Prepaid rent 3,000 Office supplies 600 Equipment 60,000 Accumulated depreciation: equipment $ 29,500 Accounts payable

- 12. 4,180 Notes payable 12,000 Interest payable 320 Unearned fees 6,000 Income taxes payable 4,000 Unearned revenue 20,000 Retained earnings

- 13. 49,000 Capital stock 25,000 Dividends 3,000 Fees earned 75,000 Travel expense 5,000 Insurance expense 2,980 Rent expense 9,900

- 14. Office supplies expense 780 Utilities expense 4,800 Depreciation expense: equipment 5,500 Salaries expense 30,000 Interest expense 320 Income taxes expense 12,000

- 16. 1. Accrued but unrecorded fees earned as of December 31, 2015, amount to $1,500. 2. Records show that $2,500 of cash receipts originally recorded as unearned fees had been earned as of December 31. 3. The company purchased a six-month insurance policy on September 1, 2015, for $1,800. 4. On December 1, 2015, the company paid its rent through February 28, 2016. 5. Office supplies on hand at December 31 amount to $400. 6. All equipment was purchased when the business first formed. The estimated life of the equipment at that time was 10 years (or 120 months). 7. On August 1, 2015, the company borrowed $12,000 by signing a six-month, 8 percent note payable. The entire note, plus six months' accrued interest, is due on February 1, 2016. 8. Accrued but unrecorded salaries at December 31 amount to $2,700. 9. Estimated income taxes expense for the entire year totals $15,000. Taxes are due in the first quarter of 2016. Instructions a. For each of the numbered paragraphs, prepare the necessary adjusting entry 1. Record the accrued but uncollected fees earned

- 17. 2. Record fees earned as of December 31st 3. Record the December insurance expense 4. REcord the December rent expense 5. Record the offices supplies used in December 6. Record the December depreciation expense 7. Record the interest accrued in December 8. Record the salaries accrued in December 9. Record the income taxes accrued in December B. Determine that amount at which each of the following accounts will be reported in the company’s 2015 income statement: 1. FEES EARNED 2. TRAVELS EXPENSE 3. INSURANCE EXPERIENCE 4. RENT EXPENSE 5. OFFICE SUPPLIES EXPERIENCE 6. UTILITIES EXPENSE 7. DEPRECIATION EXPENSE: EQUIPMENT. 8. INTERNET EXPENSE 9. SALARY EXPENSE 10. INCOME TAX EXPENSE. The unadjusted trial balance reports dividends of $3,000. As of December 31, 2015, have these dividends been paid?

- 18. Yes No