Recommandé

Recommandé

Contenu connexe

Tendances

Tendances (18)

En vedette

En vedette (20)

Similaire à No Bubble

Similaire à No Bubble (20)

Dernier

Dernier (20)

No Bubble

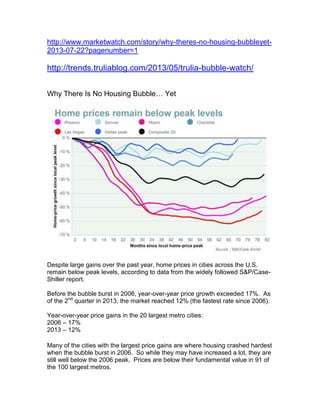

- 1. http://www.marketwatch.com/story/why-theres-no-housing-bubbleyet- 2013-07-22?pagenumber=1 http://trends.truliablog.com/2013/05/trulia-bubble-watch/ Why There Is No Housing Bubble… Yet Despite large gains over the past year, home prices in cities across the U.S. remain below peak levels, according to data from the widely followed S&P/Case- Shiller report. Before the bubble burst in 2006, year-over-year price growth exceeded 17%. As of the 2nd quarter in 2013, the market reached 12% (the fastest rate since 2006). Year-over-year price gains in the 20 largest metro cities: 2006 – 17% 2013 – 12% Many of the cities with the largest price gains are where housing crashed hardest when the bubble burst in 2006. So while they may have increased a lot, they are still well below the 2006 peak. Prices are below their fundamental value in 91 of the 100 largest metros.

- 2. ―What’s important to keep in context is that those double-digit gains are off of very low prices. Even with those gains prices are still relatively low,‖ said Frank Nothaft, chief economist at federally controlled mortgage buyer Freddie Mac. Despite the year-over-year price increase, home prices are undervalued 7% nationally and regionally in 91 of the 100 largest metros in the 2nd quarter of 2013. During last decade’s bubble, prices were as high as 39% overvalued in 2006 Q1, then during the bust, fell to 15% undervalued in 2011 Q4. Therefore, even with the recent price increases, home prices nationally remain undervalued relative to fundamentals and much lower than in the last bubble. That’s why today’s price gains are actually still a rebound, not a bubble. A reading of 100 means that a household with median income would have exactly enough income to qualify for buying a median-priced existing single- family home. Affordability has declined 18% since January, hitting 172.7 in May, but is 17% above its average over the past decade. In an alternative view of affordability, Trulia’s Kolko calculates the gap between the cost to buy versus rent, including items such as maintenance, insurance, mortgage payments. For June, he found that it was about 40% cheaper to buy a

- 3. home than rent, compared with 46% cheaper in March 2012. Back in September 2006, it was 15% more expensive to buy than to rent. ―Because mortgage rates are still near long-term lows, and because prices fell so much after the housing bubble burst and remain low relative to rents even after recent price increases, buying is still much cheaper than renting,‖ Kolko blogged. ―Mortgage rates would have to rise a huge amount — to 10.5% — to tip the math in favor of renting.‖ So far this year about 250,000 single-family homes have been sold that were previously sold within the past 12 months, according to RealtyTrac, an online foreclosure marketplace. If that pace is maintained, there could be about half a million flipped homes by the end of the year, up 4% from last year and almost double the total in 2005. “Yes, there is a red flag. High levels of flipping are indicative a market that is speculative and at risk of becoming overheated,” said Daren Blomquist, vice president at RealtyTrac. If flipping continues at a high level then it could indicate another housing bubble forming in some markets. The return of flipping to pre-recession levels surprised Richard Green, director of the USC Lusk Center for Real Estate.

- 4. "Back then, you could buy a house without any money down," Green said. "When people failed to repay their loans, it led to a cascading effect." Bankers have since tightened access to credit considerably. That means investors are putting their own money at risk, which gives Green some comfort that the flipping resurgence doesn't necessarily signal a new round of irrational investing. "If people are acquiring houses with very low down payments, then I would be very worried," he said. Credit standards for would-be home owners have been rising for years, and may have even become too tight, experts say. The bad loans that plunged the country into a deep recession slashed credit access. A key difference between the current housing-market rebound and prior run ups is how tough it is to obtain a mortgage.

- 5. “Credit seized up. Now access to credit isn’t as easy as it once was,” said Nicolas Retsinas, senior lecturer in real estate at Harvard Business School. Some credit- worthy borrowers are unable to access mortgages. This year the average FICO score for loans acquired by Fannie Mae is 757, up from 719 in 2005. Over that same period, FICO scores for Freddie Mac-acquired loans rose to 752 from 711. A separate gauge of mortgage credit signaled an increase in availability in June. According to the Mortgage Bankers Association, its gauge of mortgage-credit availability ticked up to 109.8 in June from 108.9 in May, compared with a benchmark level of 100 in March 2012. Despite last month’s gain, the index is far lower than readings of about 800 in 2007. When it comes to new homes, construction starts have been growing at a year-over- year double-digit pace since late 2011, but this rebound is relatively slow. The seasonally adjusted annual rate of new home starts hit 836,000 in June, the lowest pace in almost a year, and down 63% from a peak annualized rate of almost 2.3 million, which was reached in January 2006.